ID : MRU_ 433213 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

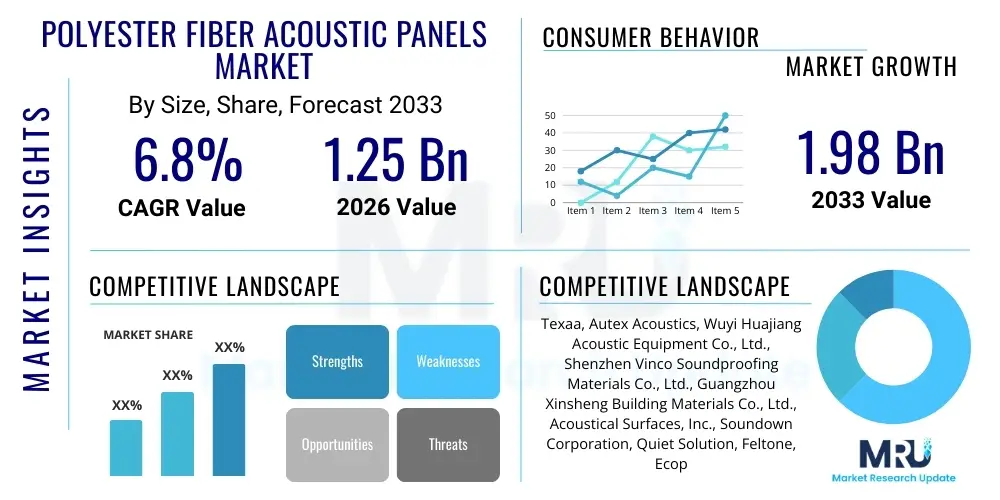

The Polyester Fiber Acoustic Panels Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $1.25 Billion in 2026 and is projected to reach $1.98 Billion by the end of the forecast period in 2033. This robust expansion is primarily driven by increasing awareness regarding indoor environmental quality, stringent noise pollution control regulations, and the growing incorporation of sustainable building materials across commercial and residential infrastructure projects globally. The shift towards open-plan office designs and specialized architectural acoustics in hospitality and educational sectors further fuels this demand.

The Polyester Fiber Acoustic Panels Market encompasses the production and distribution of sound-absorbing panels primarily manufactured from polyester fibers, predominantly recycled Polyethylene Terephthalate (PET). These non-woven, thermally bonded panels are celebrated for their exceptional acoustic performance, offering high Noise Reduction Coefficients (NRCs) essential for controlling reverberation and managing indoor soundscapes. They are dimensionally stable, highly durable, lightweight, and inherently resistant to moisture and bacteria, making them superior alternatives to traditional materials like mineral wool or foam in many applications. The panels are customizable in terms of color, texture, and shape, integrating seamlessly into contemporary architectural aesthetics while meeting strict fire safety standards.

Major applications of these panels span a diverse range of sectors, including corporate offices, educational institutions, healthcare facilities, recording studios, theatres, and increasingly, high-end residential spaces seeking optimal sound isolation and comfort. Their popularity is significantly boosted by their eco-friendly profile, as panels containing up to 60-80% recycled content directly address sustainability mandates within the construction industry. Furthermore, the ease of installation and maintenance, coupled with their structural integrity and aesthetic versatility, positions polyester fiber acoustic panels as a preferred solution for architects and interior designers focused on both functionality and sustainable design principles.

Key benefits driving market adoption include their superior thermal and acoustic insulation properties, non-toxic composition (free from formaldehyde and harsh chemicals), and resistance to mold and mildew. Driving factors are multifaceted, rooted in regulatory pressure concerning workplace noise exposure, the rising global trend of green building certifications (such as LEED and WELL standards), and continuous innovation in manufacturing processes leading to cost-effective, high-performance product offerings. The demand for improved auditory environments, particularly in shared or multi-purpose spaces, remains a fundamental driver for sustained market growth.

The Polyester Fiber Acoustic Panels Market is characterized by strong upward momentum, largely attributed to compelling global business trends emphasizing corporate social responsibility and sustainable material sourcing. Business trends indicate a marked increase in demand for customized panel solutions, integrating advanced digital printing and precision CNC cutting technologies to cater to bespoke architectural requirements. Regional trends highlight the Asia Pacific (APAC) region as the fastest-growing market, propelled by rapid urbanization, significant infrastructure development, and increasing foreign investment in commercial real estate, particularly in China and India. Europe maintains a strong growth trajectory driven by stringent environmental regulations and a high adoption rate of circular economy principles, favoring recycled PET products.

Segment trends reveal that the panel segment focusing on high-density materials (above 200 kg/m³) is experiencing accelerated adoption, specifically within professional audio environments and industrial noise barriers, due to superior sound absorption properties. Concurrently, the application segment dominated by the Office and Corporate sector remains the largest consumer, reflecting the global transition to open-plan, collaborative workspaces that necessitate effective sound mitigation solutions. Furthermore, the Residential segment is emerging as a high-potential area, spurred by consumers' focus on home theaters and work-from-home setups requiring enhanced acoustic comfort. Manufacturers are increasingly focusing on vertical integration and strategic partnerships with design firms to capture specialized market niches and ensure consistent material supply chains.

Strategic movements within the competitive landscape include significant investments in capacity expansion and technological advancements aimed at improving material recycling efficiency and panel aesthetics. The market equilibrium is continuously influenced by the fluctuating cost and availability of recycled PET feedstock, pushing companies toward establishing stable, long-term procurement agreements. Overall, the market outlook is overwhelmingly positive, driven by the convergence of environmental mandates, technological innovation in material processing, and an escalating global valuation of acoustic comfort and indoor air quality.

Common user questions regarding AI's impact on the Polyester Fiber Acoustic Panels Market center around efficiency gains, material optimization, and design automation. Users frequently inquire how AI can optimize the non-woven manufacturing process, specifically regarding fiber blending, density control, and thermal bonding parameters to ensure consistent NRC performance. There is also significant user interest in utilizing AI for predictive maintenance of complex machinery, thereby reducing downtime and operational costs. Furthermore, architects and designers seek AI tools capable of generative design, where acoustic requirements (reverberation time, frequency response) are input, and the AI suggests optimal panel placements, shapes, and thicknesses, thus revolutionizing customized solution development and minimizing material waste. The primary concerns revolve around the initial investment costs for implementing AI-driven systems and the need for highly specialized personnel to manage these advanced manufacturing environments.

AI's primary influence is observed in enhancing production efficiency and predictive quality assurance. By leveraging machine learning algorithms, manufacturers can analyze vast datasets from production runs, identifying subtle variations in raw material inputs (recycled PET quality) and adjusting process variables in real-time. This sophisticated control minimizes material scrap rates and ensures that every batch meets stringent acoustic and fire safety specifications consistently. Furthermore, computer vision systems integrated with AI monitor panel surface integrity during cutting and finishing, instantly flagging defects that human inspectors might miss, resulting in superior product quality and enhanced customer satisfaction. The incorporation of AI-driven robotics in handling, sorting, and packaging also contributes significantly to streamlined logistics and reduced labor intensity in manufacturing facilities.

The application of generative AI in the design phase is set to dramatically shorten the product development cycle for bespoke acoustic solutions. Designers are moving beyond simple geometric patterns; AI tools can simulate complex sound wave interactions within specific room geometries, allowing for rapid iteration of panel arrays optimized for specific audio frequencies. This personalized acoustic engineering enables manufacturers to offer highly precise solutions for demanding applications such as concert halls, broadcast studios, and specialized healthcare waiting areas. Ultimately, AI fosters a shift towards 'smart acoustics,' where panels are not merely static absorbers but components within an optimized, data-driven sound management system, thereby increasing the intrinsic value of polyester fiber solutions.

The market dynamics are significantly influenced by a confluence of accelerating drivers, persistent restraints, and compelling opportunities that define the strategic landscape. The core driver is the escalating global focus on health and well-being, where acoustic comfort is recognized as a vital component of indoor environmental quality (IEQ), particularly under certifications like WELL Building Standard. This is reinforced by governmental and municipal regulations establishing mandatory noise limits in public, commercial, and educational environments, forcing compliance through the adoption of high-performance acoustic materials. Simultaneously, the inherent sustainability of polyester panels, derived largely from recycled plastic bottles, aligns perfectly with corporate sustainability goals and circular economy initiatives, providing a substantial competitive edge over non-recyclable alternatives. The architectural trend toward aesthetically integrated, multi-functional panels further accelerates adoption across various sectors.

However, the market faces notable restraints, primarily centered on the volatility of raw material pricing. As the panels rely heavily on recycled PET, the supply chain is susceptible to fluctuations in global plastic waste management costs, petroleum prices, and recycling infrastructure efficiency, which can impact manufacturing costs and final product pricing unpredictability. Another restraint involves the perception of high initial installation costs compared to minimal aesthetic treatments, despite the long-term operational savings and health benefits. Furthermore, while the panels offer excellent fire safety, adherence to highly varied international fire codes (e.g., Euroclass, ASTM) requires complex and sometimes costly fire-retardant treatments, adding layers of complexity to global market penetration and standardization.

Opportunities for growth are abundant, notably in specialized sectors such as the rapidly expanding electric vehicle (EV) market, where lightweight, sound-dampening materials are essential for reducing cabin noise caused by silent powertrains. The modular construction and prefabricated building industry presents another vast opportunity, requiring quickly installable, high-performance acoustic solutions that are integrated during the manufacturing phase. Geographical expansion into emerging economies with nascent but rapidly developing construction standards, particularly in Southeast Asia and Africa, offers significant untapped potential. Moreover, product innovation focusing on combined functionality—such as panels incorporating integrated lighting, air purification, or heating elements—will open new high-value market segments, enhancing the overall utility proposition of the polyester fiber acoustic panels.

The Polyester Fiber Acoustic Panels market is extensively segmented based on several critical factors, including product type, density, application, and end-use sectors, enabling manufacturers to target specific market needs efficiently. Product segmentation often distinguishes between standard flat panels, customized 3D/sculptural panels, and specialized ceiling baffles or hanging screens, each optimized for different acoustic environments and aesthetic requirements. Density segmentation (low, medium, high) directly correlates with the panel's NRC rating and structural rigidity, determining its suitability for industrial sound control versus decorative architectural applications. The high-density segment is critical for noise barrier applications, whereas medium density (150-200 kg/m³) is typically used in commercial office environments, balancing absorption with cost efficiency.

Application-based segmentation highlights the dominant role of the Commercial sector, encompassing corporate offices, retail spaces, and public facilities, where mitigating noise is paramount for productivity and customer experience. Educational and Healthcare facilities form a vital subset, driven by regulatory requirements for specific acoustic environments that aid learning and patient recovery, respectively. The fastest-growing segment, however, is the Residential sector, spurred by increasing consumer disposable income, the proliferation of sophisticated home entertainment systems, and the normalization of remote work, requiring dedicated quiet spaces. Manufacturers must therefore tailor marketing strategies, focusing on technical performance for B2B segments and aesthetic integration for the consumer market.

Geographically, market segmentation is pivotal, with mature markets in North America and Europe demanding panels that excel in sustainability certifications and offer advanced customization features. In contrast, developing markets in Asia Pacific prioritize cost-effectiveness and volume production, often focusing on standard panel designs for large-scale infrastructure projects. Understanding these differentiated regional demands is crucial for optimizing supply chain logistics and developing localized product lines. This comprehensive segmentation allows market players to accurately assess competitive intensity and allocate R&D resources toward high-growth product categories and applications that offer the highest return on investment.

The value chain for the Polyester Fiber Acoustic Panels Market begins with the upstream sourcing of raw materials, primarily recycled PET (rPET) flakes or pellets derived from post-consumer plastic waste. This initial stage is crucial as the quality and stable supply of rPET directly influence the final panel's acoustic performance and cost structure. Key upstream players include specialized plastic recycling firms and chemical producers who ensure the rPET meets purity standards before thermal processing. Energy consumption during the recycling and compounding phases is also a critical factor, pushing manufacturers to seek energy-efficient processing technologies to maintain environmental credentials and cost competitiveness. Ensuring traceability of the recycled content is vital for certification purposes, adding complexity to the supply chain management.

The core manufacturing process involves the conversion of rPET fibers into non-woven panels, typically through carding, needle punching, and thermal bonding (melt pressing) without the need for chemical binders, which is a key differentiator for the product's non-toxic profile. This midstream stage is highly capital intensive, requiring specialized machinery for density uniformity, precise thickness calibration, and surface finishing. Downstream activities involve customization, including advanced CNC cutting for complex shapes, digital printing for decorative surfaces, and integration with mounting systems. The effectiveness of the value chain relies heavily on achieving high production yields and minimizing waste during these fabrication steps, which are crucial for maintaining profitability in a highly competitive material market.

Distribution channels are multifaceted, employing both direct and indirect strategies. Direct distribution involves sales teams targeting large architectural firms, interior designers, and major construction companies, often providing bespoke design consultation and installation support for large commercial projects. Indirect distribution relies on established networks of building material distributors, specialized acoustic solution providers, and e-commerce platforms, particularly for standardized residential or small office panels. The "pull" strategy, driven by architects specifying the material early in the design phase, is highly influential. Successful market penetration demands strong relationships across the architectural and design community, making robust channel partnerships and technical support essential for market success.

Potential customers for Polyester Fiber Acoustic Panels are diverse, spanning multiple institutional, commercial, and private sectors, united by the need for effective noise control and improved indoor aesthetics. The primary buyers are not always the end-users but highly influential intermediaries such as architects, interior design firms, and general contractors who specify the materials based on acoustic requirements, aesthetic criteria, and sustainability mandates. These specifiers require detailed technical data, including NRC ratings, fire classifications, and environmental certifications, making B2B engagement and technical marketing essential for manufacturers. Large-scale construction developers involved in building new corporate campuses, hotel chains, or multi-family residential units constitute major purchasing blocks due to the high volume requirement.

End-users across the commercial segment represent substantial buying power. This includes technology companies and corporate headquarters operating open-plan offices, where productivity loss due to noise distraction is a significant concern. The education sector—ranging from universities and K-12 schools—is a major consumer, utilizing panels to improve classroom intelligibility and compliance with specialized acoustic standards for learning environments. Furthermore, the healthcare industry purchases these panels for use in patient rooms, corridors, and waiting areas to create calming, quieter environments conducive to healing, often requiring panels with enhanced anti-microbial treatments.

A growing segment of high-value customers includes professional audio environments such as recording studios, post-production facilities, and broadcast centers, where highly precise sound treatment is non-negotiable. These customers demand specialized, high-density panels tailored for specific frequency absorption characteristics. Finally, the retail and hospitality sectors, including restaurants, shopping centers, and hotels, seek aesthetically pleasing, durable panels to enhance the customer experience by mitigating excessive background noise, demonstrating the panels' versatility beyond strictly functional soundproofing into critical atmospheric design elements.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.25 Billion |

| Market Forecast in 2033 | $1.98 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Texaa, Autex Acoustics, Wuyi Huajiang Acoustic Equipment Co., Ltd., Shenzhen Vinco Soundproofing Materials Co., Ltd., Guangzhou Xinsheng Building Materials Co., Ltd., Acoustical Surfaces, Inc., Soundown Corporation, Quiet Solution, Feltone, Ecophon (Saint-Gobain), Knauf Insulation, Kingspan Group, Armstrong World Industries, Panel Processing, Inc., Hangzhou Ruichen Decoration Material Co., Ltd., Foshan Tiange Acoustic and Decor Material Manufacturer, STAR-NET, Sound Zero, BuzziSpace, ReForm Materials. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Polyester Fiber Acoustic Panels market is fundamentally defined by advancements in non-woven textile manufacturing and digital fabrication, aimed at optimizing material performance, production efficiency, and aesthetic versatility. A core technology is the thermal bonding process, which uses heat and pressure, rather than chemical adhesives, to fuse the PET fibers, ensuring the finished panel is non-toxic and retains its high recyclability. Recent innovations focus on precise temperature control during bonding to achieve uniform density distribution, which is critical for consistent sound absorption across the panel surface. Furthermore, research is ongoing into enhancing the inherent fire retardancy of the polyester without resorting to heavy halogenated additives, aligning with stricter green building requirements for safety and low toxicity.

Digital fabrication technologies, particularly highly precise Computer Numerical Control (CNC) cutting and routering systems, have revolutionized the market's aesthetic offerings. These machines allow manufacturers to create complex, geometric, and 3D sculpted panels with intricate patterns and tight tolerances, previously challenging or impossible with traditional cutting methods. This capability supports the trend toward highly customized interior design, enabling panels to serve as architectural features rather than just functional acoustic treatments. Advanced digital printing technology is also crucial, allowing for the direct application of high-resolution graphics, textures, and even photo-realistic images onto the panels, maintaining acoustic integrity while vastly increasing decorative options, thereby capturing the lucrative interior design segment.

Additionally, the market is leveraging material science to introduce enhanced functionalities. This includes the development of hydrophobic coatings to improve moisture resistance for high-humidity environments (such as pools or industrial kitchens) and the incorporation of specialized mineral fillers during fiber production to boost sound attenuation at lower frequencies. The integration of "smart" elements, such as embedded LED lighting systems, micro-perforations for integrated ventilation, or IoT sensors for monitoring room acoustics in real-time, represents the next frontier. These technological integrations transform the panels from passive absorbers into active components of a comprehensive indoor environment management system, driving premium pricing and increased utility for the end-user.

The primary environmental benefit lies in their composition, typically incorporating between 60% to 80% recycled Polyethylene Terephthalate (rPET) derived from post-consumer plastic bottles. This substantially reduces landfill waste and decreases reliance on virgin petrochemical resources, strongly supporting circular economy initiatives in the construction industry.

Acoustic performance is primarily measured using the Noise Reduction Coefficient (NRC), which quantifies the average sound absorption across specific frequency ranges (typically 250 Hz to 2,000 Hz). Polyester panels generally achieve high NRC values, often ranging from 0.85 to 0.95, indicating excellent efficiency in reducing reverberation and echo in indoor spaces.

Yes, polyester fiber is inherently hydrophobic and non-hygroscopic, meaning it resists moisture absorption. Unlike many traditional fibrous materials, these panels will not sag, warp, or promote mold and mildew growth in humid conditions, making them ideal for applications such as swimming pool areas, industrial kitchens, and specific healthcare settings.

Polyester Fiber Acoustic Panels must generally meet stringent international fire safety standards. In North America, this typically involves ASTM E84 Class A ratings, while in Europe, compliance with Euroclass B-s1, d0 standards is often required. Manufacturers achieve these ratings through specialized fiber treatments and thermal bonding processes, ensuring the panels are self-extinguishing and do not produce excessive smoke.

Panel density (measured in kg/m³) directly correlates with both acoustic performance and cost. Higher density panels (above 190 kg/m³) offer superior low-frequency absorption and increased structural rigidity, making them suitable for specialized studio or industrial noise barrier applications, thus commanding a higher price. Lower to medium density panels are more cost-effective and commonly used for general reverberation control in commercial offices and classrooms.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.