ID : MRU_ 435086 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

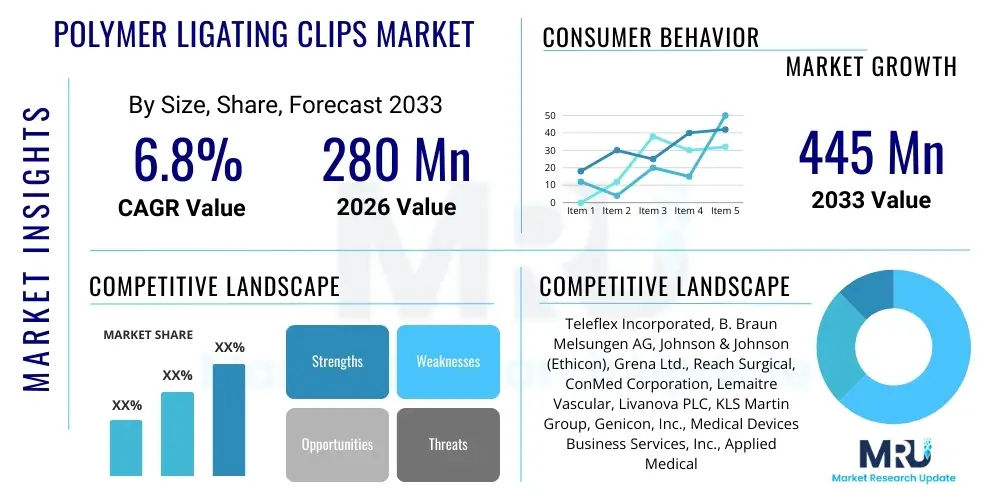

The Polymer Ligating Clips Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $280 million in 2026 and is projected to reach $445 million by the end of the forecast period in 2033.

The Polymer Ligating Clips Market encompasses specialized, non-metallic surgical devices utilized for occluding blood vessels and tissue structures during various operative procedures, primarily in minimally invasive surgery (MIS) such as laparoscopy. These clips, typically manufactured from non-absorbable polymers like polyether ether ketone (PEEK) or biocompatible polyacetal, offer significant advantages over traditional metal ligating clips, including reduced artifact interference in imaging modalities such as MRI or CT scans, and non-conductivity during electrosurgery. The inherent inertness and superior biocompatibility of these polymeric materials minimize patient risk related to allergic reactions or long-term tissue irritation, driving their increasing adoption across high-volume surgical disciplines globally. The design of these clips often incorporates interlocking mechanisms or distinct V-shapes to ensure secure ligation and prevent migration post-placement, a critical factor in complex procedures.

Major applications for polymer ligating clips span general surgery, involving cholecystectomy, appendectomy, and bowel resection; gynecology, particularly in hysterectomy and tubal ligation; urology; and cardiothoracic procedures. The fundamental benefit is enabling effective hemostasis and tissue sealing without necessitating the use of sutures or staples in many scenarios, thereby reducing operative time and enhancing surgical efficiency. Furthermore, the development of advanced clip appliers, both reusable and disposable, has facilitated precise, single-handed deployment within constrained anatomical spaces characteristic of laparoscopic environments. This shift towards standardized, reliable ligation methods is pivotal in hospitals and ambulatory surgical centers (ASCs) focusing on high throughput and reduced recovery times for patients undergoing MIS.

Driving factors for sustained market expansion include the global increase in the prevalence of chronic diseases requiring surgical intervention, the accelerating transition from open surgery to minimally invasive techniques worldwide, and continuous innovation in polymer science resulting in safer, stronger, and more radiolucent clips. Regulatory approvals supporting their use in increasingly complex surgeries, coupled with professional clinical guidelines recommending non-metallic alternatives, further solidify the market trajectory. Moreover, cost-effectiveness in comparison to expensive energy-based sealing devices and the proven clinical track record of polymer clips ensure their continued acceptance as a foundational tool in modern surgical suites.

The Polymer Ligating Clips Market is defined by intense competition centered on applicator mechanism innovation and supply chain efficiency, reflecting a broader trend in the medical device industry toward user-friendly, specialized instruments compatible with diverse surgical platforms. Key business trends involve strategic mergers and acquisitions among established players aiming to consolidate market share and acquire specialized polymer technology patents, alongside a strong focus on expanding disposable applicator systems which mitigate reprocessing costs and sterilization concerns for end-users. Furthermore, companies are increasingly targeting emerging markets in the Asia Pacific and Latin America, driven by rising healthcare infrastructure investment and growing penetration of laparoscopic techniques, leveraging localized distribution networks to overcome geographical barriers and price sensitivity.

Regional trends indicate North America and Europe currently dominate the market value due to high surgical volumes, established reimbursement frameworks, and early adoption of advanced surgical technologies, particularly in specialized centers for complex oncological and bariatric procedures. However, the Asia Pacific region is projected to exhibit the highest CAGR, primarily fueled by rapid urbanization, increasing medical tourism, expansion of insurance coverage, and government initiatives promoting minimally invasive surgery training. Within these regions, there is a distinct segment trend favoring large-size polymer clips, necessitated by the increasing complexity of cases involving larger vessels or pedicles, requiring greater retention strength and broader sealing capacity. This technological pull is pushing manufacturers to enhance clip material strength without compromising biocompatibility.

Segmentation analysis reveals that the disposable polymer clip applicator segment is growing faster than reusable systems, aligning with hospital efforts to reduce infection risk and operational overhead associated with reprocessing complex instruments. Furthermore, hospitals maintain the largest end-user share, driven by their capacity to handle high-volume surgical procedures and capital expenditure budgets necessary for advanced surgical suites. The market outlook is overwhelmingly positive, contingent on continued regulatory support for novel polymer formulations and the seamless integration of ligating clips into robotic and navigated surgical systems, ensuring precision placement and verifiable occlusion, thereby cementing their irreplaceable role in contemporary surgical practice.

Common user questions regarding AI's influence on the Polymer Ligating Clips Market often revolve around how artificial intelligence can enhance surgical outcomes, specifically focusing on the precision of clip placement, the reduction of procedural complications, and optimization of supply chain logistics for these critical devices. Users are intensely interested in AI's potential role in pre-operative planning, where algorithms could analyze patient-specific anatomy from imaging data (e.g., CT, MRI) to predict optimal clip size and placement strategy, thereby reducing operative variability and minimizing the risk of vessel slippage or unintended tissue injury. Another central theme is the integration of AI-driven visualization aids during the procedure, where systems might highlight critical vascular structures and suggest appropriate ligation points in real-time, especially within the constrained viewing fields of laparoscopy or robotic surgery, directly impacting the effective use of polymer clips.

The immediate impact of AI is most pronounced in the operational efficiency sector, where sophisticated algorithms are being deployed to manage hospital inventories, forecast demand for specific clip sizes and applicator types based on scheduled surgeries, and optimize procurement cycles. This predictive inventory management reduces instances of stock-outs during critical procedures and minimizes waste from expired or unused stock, leading to significant cost savings for healthcare providers—a crucial factor given the high volume of clips used annually. Furthermore, AI is beginning to play a role in training and simulation. Virtual reality and augmented reality platforms, powered by AI models, offer surgeons realistic environments to practice complex clip deployment techniques and manage complications, leading to a standardized improvement in clinical skill acquisition related to polymer clip usage.

Looking ahead, the integration of AI into robotic surgical platforms will likely involve enhanced feedback mechanisms where sensors in the robotic instruments provide data on tissue tension and clip retention strength, processed instantly by an AI core. This real-time quality control ensures that the polymer clip is deployed with optimal force and placement geometry, surpassing human perceptual capabilities in verifying procedural correctness. While AI does not directly alter the manufacturing of the polymer clips themselves, its influence on decision-making, surgical planning, execution accuracy, and supply chain optimization fundamentally elevates the clinical utility and cost-effectiveness of these devices, thereby reinforcing their market growth trajectory and addressing concerns related to procedural variability and error reduction.

The Polymer Ligating Clips Market dynamics are critically influenced by a robust interplay of Drivers promoting growth, Restraints challenging adoption, and Opportunities guiding future strategic investments, collectively generating significant Impact Forces across the healthcare ecosystem. The primary Driver is the overwhelming global preference for minimally invasive surgical (MIS) procedures, which inherently rely on efficient, secure ligation solutions compatible with small operative fields, a role perfectly suited to polymer clips. Coupled with this is the imperative to reduce surgical site infections (SSIs) and streamline workflow, which disposable, sterile clip systems effectively address. However, a significant Restraint remains the comparatively higher unit cost of certain advanced polymer clips and their dedicated applicators versus older, lower-cost metal alternatives, posing a challenge in price-sensitive developing economies. Additionally, concerns among some surgeons regarding the potential for non-absorbable polymer clips to migrate or interfere with subsequent diagnostic imaging, although largely mitigated by modern materials, still present a perceptual barrier to universal adoption.

Opportunities for market expansion are substantial, primarily centered on technological convergence and material science breakthroughs. The development of bioabsorbable or resorbable polymer ligating clips represents a major opportunity, allowing the clips to dissolve safely after their functional purpose is served, eliminating long-term foreign body presence and addressing migration concerns entirely. Furthermore, the increasing integration of surgical robotics requires highly compatible, specialized instruments, offering manufacturers a niche for premium, high-precision polymer clip application systems tailored for robotic end-effectors. These technological advancements create a compelling value proposition that justifies increased investment in R&D and clinical trials to demonstrate superior long-term patient outcomes, thereby driving market penetration.

These dynamics generate powerful Impact Forces on the market structure. The push for safety and procedural efficacy driven by regulatory bodies and clinical societies mandates the use of reliable ligation methods, favoring advanced, non-metallic solutions. The economic force is bifurcated: while providers seek cost-efficiency (pushing demand toward disposable systems), patients and payors demand efficacy and reduced complications (favoring high-quality, potentially higher-cost polymer devices). Ultimately, the dominant force shaping the market trajectory is the ongoing evolution of surgical techniques towards precision and minimal invasiveness, ensuring polymer clips remain an indispensable tool for securing critical structures, placing pressure on manufacturers to continuously enhance material performance and application mechanics to meet increasingly stringent clinical demands for secure hemostasis.

The Polymer Ligating Clips Market is comprehensively segmented based on product type, application, and end-user, providing a granular view of demand distribution and growth opportunities across distinct market verticals. The segmentation by product type is foundational, dividing the market into the clips themselves and the associated application devices (appliers or cartridges). Clips are further categorized by size (small, medium-to-large, large), reflecting the varied anatomical requirements encountered in surgery. The distinction between reusable and disposable applicators is critical; while reusable appliers offer a lower capital expenditure over time, the disposable cartridge systems are increasingly preferred due to their inherent sterility, simplified logistics, and reduced risk of cross-contamination, particularly in high-volume surgical centers where procedural safety protocols are prioritized above initial equipment cost. This segmentation helps manufacturers tailor their product portfolio to specific user needs, addressing both cost-sensitivity and operational efficiency requirements.

Application-based segmentation highlights the primary surgical fields driving consumption. General surgery, encompassing procedures such as gastrointestinal, bariatric, and hernia repair, constitutes the largest segment due to the sheer volume of cases requiring vessel and duct ligation. Specialized areas like gynecology (hysterectomy, ectopic pregnancy management) and urology (nephrectomy, prostatectomy) follow, characterized by the need for precise ligation in delicate, complex anatomical regions. The fastest growth rates are often observed in cardiovascular and thoracic surgery, where the non-conductive and radiolucent properties of polymer clips are highly advantageous for procedures involving critical vascular structures or where post-operative imaging is frequently utilized. Understanding these application segments allows for targeted clinical education and marketing efforts, aligning product specifications with the unique demands of each specialty.

The market is also delineated by end-users, primarily hospitals and ambulatory surgical centers (ASCs). Hospitals, particularly large university and multi-specialty centers, currently account for the dominant market share due to their extensive surgical case load, higher complexity procedures requiring specialized clips, and greater purchasing power. However, ASCs are emerging as a major growth engine, driven by the shift towards outpatient settings for elective and less complex surgeries, emphasizing efficiency and cost control. ASCs often favor streamlined, disposable clip systems to maintain rapid turnover and minimize sterilization burdens. This shift necessitates that clip manufacturers develop competitive pricing models and bulk purchasing agreements suitable for the operational scale and economic structure of the rapidly expanding ASC sector, ensuring accessibility and ease of integration into their standardized protocols.

The value chain for the Polymer Ligating Clips Market begins with the acquisition and refinement of specialized medical-grade polymers, which constitutes the critical upstream analysis. Manufacturers rely heavily on a specialized few suppliers for materials such as polyacetal, PEEK, and sometimes bioabsorbable polymers like Poly-L-lactic acid (PLLA) or Poly(lactic-co-glycolic acid) (PLGA), which must meet rigorous biocompatibility and mechanical strength standards. The manufacturing phase involves high-precision injection molding, followed by intricate assembly of the clips and their delivery systems (appliers). Quality control, including meticulous dimensional checks and sterilization validation, is paramount in this stage due to the critical nature of the devices in patient safety. Strategic relationships with upstream suppliers that guarantee material quality and consistent supply are essential to mitigate risks associated with regulatory compliance and production scalability.

The midstream segment focuses on distribution and logistics, a complex process influenced by regulatory requirements and the global footprint of the key market players. Distribution channels are categorized as direct and indirect. Direct sales involve manufacturers utilizing their in-house sales teams to engage large hospital networks, Group Purchasing Organizations (GPOs), and governmental health systems, offering deeper control over pricing and clinical support. Indirect distribution relies on third-party distributors, wholesalers, and specialized medical device agents, particularly prevalent in geographically fragmented or emerging markets. Efficiency in the midstream is vital for maintaining product sterility and ensuring timely delivery of inventory, particularly the fast-moving disposable clip cartridges. GPOs play a central role by negotiating bulk contracts, significantly impacting which brands are adopted across major healthcare networks.

Downstream analysis centers on the end-user clinical application and post-sales support. The main downstream buyers are surgical departments within hospitals and ASCs, where the clips are utilized by surgeons and surgical staff. Post-sales activities include clinical training for new applicators, maintenance services for reusable components, and rigorous pharmacovigilance (monitoring for adverse events). The success of a product downstream is heavily dependent on user experience—specifically, the reliability of the clip retention, the ergonomic design of the applicator, and the ease of integration into existing surgical workflows. Manufacturers must continually gather feedback from surgeons to drive iterative improvements, ensuring that the final product offers verified clinical efficacy and superior handling characteristics compared to competitor offerings.

The primary customers and end-users of Polymer Ligating Clips are institutions within the global healthcare delivery network that perform high volumes of surgical procedures, specifically those focused on minimally invasive techniques. The most significant customer base comprises the procurement departments of large general and specialized hospitals. These institutions require a vast range of clip sizes and high quantities of disposable cartridges to manage diverse surgical workloads across general surgery, orthopedics, gynecology, and cardiac units. Decision-making in this segment is driven by clinical efficacy data, contract pricing negotiated through Group Purchasing Organizations (GPOs), and the reliability of the supplier's inventory and regulatory compliance record. Surgeons and surgical nurses, while being the direct users, act as influential stakeholders whose preferences for specific applicator mechanisms or clip material quality significantly dictate purchasing choices.

Ambulatory Surgical Centers (ASCs) represent the fastest-growing segment of potential customers. As healthcare economics push procedures toward outpatient settings, ASCs are increasingly adopting polymer ligating clips for streamlined, same-day surgeries, such as laparoscopic cholecystectomies and hernia repairs. For ASCs, the key purchasing drivers are cost-efficiency, standardized protocols, and the use of disposable instruments to eliminate sterilization complexity and cost. Manufacturers must offer flexible procurement solutions and high-quality, reliable disposable systems that support rapid turnover and maintain low operational costs. The purchasing teams in ASCs are highly sensitive to initial capital outlay and favor products with proven clinical records that minimize the risk of costly complications or readmissions.

Beyond hospitals and ASCs, specialized clinics focusing on bariatric or gynecological procedures, as well as academic and research institutions, also form important segments of potential customers. Academic centers often serve as early adopters of new clip technologies, such as bioabsorbable variants, driven by research interests and complex surgical requirements. Furthermore, large governmental and military healthcare systems constitute specific customer groups globally, often procuring through large-scale tenders based on stringent quality requirements and highly competitive pricing structures. Engaging these diverse customer groups requires tailored commercial strategies, balancing the clinical need for advanced technology with the pervasive institutional mandate for economic value and supply chain resilience.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $280 Million |

| Market Forecast in 2033 | $445 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Teleflex Incorporated, B. Braun Melsungen AG, Johnson & Johnson (Ethicon), Grena Ltd., Reach Surgical, ConMed Corporation, Lemaitre Vascular, Livanova PLC, KLS Martin Group, Genicon, Inc., Medical Devices Business Services, Inc., Applied Medical, Medtronic, Inc., Dextera Surgical, Inc., Changzhou Haiers Medical Device Co., Ltd., Waston Medical Device Co., Ltd., BioMetrix Ltd., Olympus Corporation, Optinav, LLC, Surgical Innovations Group plc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Polymer Ligating Clips Market is primarily characterized by advancements in material science and the mechanical precision of delivery systems, aiming to enhance security and ease of use during complex procedures. Material innovation focuses heavily on optimizing polymers for superior mechanical properties, particularly tensile strength and modulus of elasticity, ensuring the clip maintains secure closure even under high internal pressure without fracturing or degrading prematurely. Next-generation polymers, such as advanced polyacetals and PEEK derivatives, are engineered to be completely inert, minimizing inflammatory responses and ensuring zero interference with post-operative diagnostic imaging, addressing a critical concern associated with older clip generations. Furthermore, the development of proprietary color-coding systems for different clip sizes, often integrated into the cartridge design, enhances procedural safety by allowing surgical teams to quickly identify the correct clip dimension, reducing the risk of errors in rapid operative environments.

The primary technological focus for market differentiation resides in the design of the clip applier mechanisms. Modern polymer clip appliers, particularly those designed for laparoscopic and robotic use, feature sophisticated mechanisms that ensure consistent, controlled deployment force and verifiable closure. Key features include tactile and audible feedback systems confirming successful clip placement, ratcheted handles for ergonomic operation, and specialized loading systems that prevent jamming or misfires, which are crucial for minimizing procedure interruptions. Continuous innovation is centered on developing multi-fire disposable applicators that can rapidly deploy several clips without reloading, significantly decreasing operative time during extensive ligation sequences. Moreover, manufacturers are incorporating articulation capabilities into the applicators, allowing surgeons to access vessels located at challenging angles during robotic or single-port access surgery.

Another major technological trend involves the transition toward bioabsorbable polymer clips, often utilizing materials like polylactic acid (PLA) or polyglycolic acid (PGA). These clips are engineered to provide the necessary mechanical strength for immediate hemostasis but are designed to gradually hydrolyze and be absorbed by the body over weeks or months. The challenge lies in controlling the absorption rate to match the time required for complete tissue healing, ensuring that the vascular structure remains safely occluded during the critical recovery phase before the clip fully degrades. This technology represents a significant clinical benefit by eliminating the permanent presence of foreign material, reducing the potential for chronic inflammation or interference with future surgeries, and is set to command a substantial premium in the market, driving specialized R&D investment among leading players.

Polymer ligating clips are primarily manufactured from high-performance, biocompatible polymers such as polyacetal (e.g., POM) or polyether ether ketone (PEEK). Newer, technologically advanced clips utilize bioabsorbable polymers like Polylactic Acid (PLA) to eliminate permanent foreign body presence post-surgery, offering superior long-term clinical safety profiles.

Polymer ligating clips are inherently non-metallic and radiolucent, meaning they produce minimal to zero artifact interference in advanced imaging modalities such as Magnetic Resonance Imaging (MRI) and Computed Tomography (CT) scans. This is a significant clinical advantage over metal clips, which often obscure anatomical structures near the clip placement site.

The shift towards disposable polymer clip applier systems is mainly driven by the imperative to enhance procedural safety, eliminate the costs and risks associated with reprocessing (sterilization and maintenance) of complex reusable instruments, and standardize workflow efficiency in high-volume surgical environments like Ambulatory Surgical Centers (ASCs).

North America currently holds the largest revenue share in the Polymer Ligating Clips Market, primarily due to its advanced and established healthcare infrastructure, high volume of minimally invasive surgical procedures, strong reimbursement systems, and rapid assimilation of new medical technologies into clinical practice.

The Polymer Ligating Clips Market is projected to experience robust growth, anticipating a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033, fueled by the rising global demand for minimally invasive surgery and ongoing material science innovations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.