ID : MRU_ 432993 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

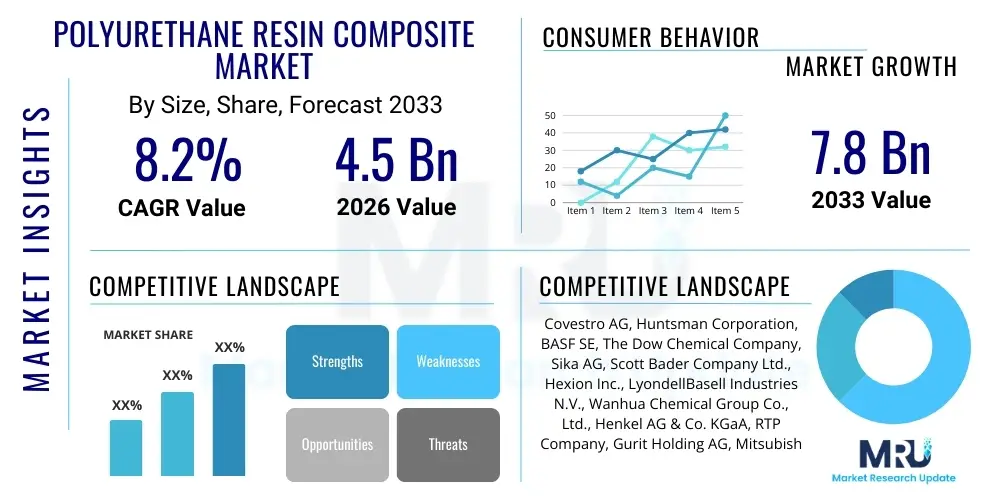

The Polyurethane Resin Composite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 7.8 Billion by the end of the forecast period in 2033.

The Polyurethane (PU) Resin Composite Market involves the integration of polyurethane resins, often thermosetting polymers, with reinforcing materials such as glass, carbon, or natural fibers, resulting in materials that exhibit superior mechanical strength, stiffness, and durability compared to traditional plastics or unreinforced polymers. Polyurethane’s inherent versatility allows for its use in diverse composite forms, ranging from rigid foam structures utilized in insulation and construction to high-performance elastomers used in protective coatings and automotive components. These composites are highly valued for their lightweight characteristics, excellent impact resistance, and customizable formulation, enabling engineers to tailor the material properties precisely for demanding applications.

Major applications of polyurethane resin composites span across critical industries, including infrastructure, transportation (automotive and aerospace), wind energy, and consumer goods. In the automotive sector, PU composites contribute significantly to vehicle lightweighting, aiding in fuel efficiency and compliance with stringent emissions regulations. For wind energy, these composites are essential for manufacturing large, durable, and structurally sound wind turbine blades. The core benefit driving market expansion is the material’s ability to offer a robust strength-to-weight ratio, chemical resistance, and ease of processing, such as through high-speed manufacturing techniques like pultrusion and Reaction Injection Molding (RIM).

Key driving factors accelerating the adoption of polyurethane resin composites include the global push for sustainable infrastructure development, the increasing demand for high-performance materials in electric vehicles (EVs), and the need for durable, corrosion-resistant solutions in harsh environments. Furthermore, advancements in composite manufacturing techniques, particularly those supporting continuous production of fiber-reinforced parts, are lowering production costs and expanding the scope of feasible applications. The inherent insulation properties of many PU composite formulations also make them indispensable in energy-efficient building systems.

The Polyurethane Resin Composite Market is currently undergoing significant transformation, characterized by rapid technological advancements in bio-based polyurethane development and a strong focus on circular economy principles, especially concerning end-of-life composite recycling. Business trends indicate a shift towards strategic partnerships between resin manufacturers and automotive Tier 1 suppliers to co-develop next-generation lightweight components optimized for electric vehicle architectures. This collaboration is crucial for standardizing material specifications and integrating advanced materials seamlessly into high-volume manufacturing lines. The primary business objective across the value chain remains cost reduction through process efficiency while simultaneously enhancing composite performance metrics like thermal stability and flame retardancy.

Regional trends highlight the Asia Pacific (APAC) region as the dominant market, propelled by massive infrastructure projects, burgeoning automotive production—especially in China and India—and significant investments in renewable energy, particularly wind farm installations. North America and Europe, while mature, are focusing heavily on regulatory-driven composite adoption, particularly concerning fire safety standards in construction and the implementation of stringent lightweighting targets for transportation. Segment trends reveal that the Glass Fiber Reinforced Polyurethane segment holds the largest market share due to its balance of performance and cost-effectiveness, though the Carbon Fiber Reinforced Polyurethane segment is poised for the fastest growth, driven by its superior mechanical properties required in aerospace and high-performance automotive applications.

Overall, the market is characterized by high competitive intensity, necessitating continuous innovation in polymerization techniques and fiber wetting processes to maximize composite performance. Sustainability is emerging as a critical differentiator, prompting manufacturers to invest in polyols derived from natural oils or recycled polyurethanes. The convergence of high-speed manufacturing methods, such as HP-RTM (High-Pressure Resin Transfer Molding), with specialized polyurethane resin systems is enabling mass production capabilities previously exclusive to traditional materials, thereby expanding the market penetration of PU composites across various industrial verticals.

Analysis of common user questions regarding AI's influence on the Polyurethane Resin Composite Market reveals strong interest in optimizing complex material formulations and accelerating the material discovery phase. Users frequently inquire about how AI can predict the long-term durability and mechanical performance of novel composite structures under varying stress conditions, thereby reducing the reliance on costly, time-consuming physical testing. There is significant concern about integrating sensor data from manufacturing processes—such as pultrusion or RTM—into AI models to achieve real-time quality control and minimize material waste, particularly considering the expensive nature of advanced fibers like carbon fiber. Furthermore, supply chain resilience is a key theme, with users seeking to understand how predictive analytics can mitigate risks associated with fluctuating raw material prices, specifically isocyanates and polyols.

The core expectations revolve around AI enabling 'smart' manufacturing where parameters like temperature, pressure, and resin cure rates are dynamically adjusted by machine learning algorithms to ensure flawless part consistency, which is vital in safety-critical applications like aerospace and automotive crash structures. This integration promises to unlock efficiencies in custom composite manufacturing, making high-performance PU materials accessible for medium-volume production runs. AI-driven simulation tools are expected to replace traditional Finite Element Analysis (FEA) partially, offering faster, more accurate predictions of structural integrity and performance across various environmental exposures, fundamentally shortening the time-to-market for new composite products.

Consequently, the application of Artificial Intelligence is moving the polyurethane composite industry from empirical material design to data-driven material informatics. This transformation impacts everything from initial monomer selection to optimizing the final processing conditions. The immediate market focus is on leveraging AI for prescriptive maintenance of expensive composite processing machinery and enhancing the sustainability profile by optimizing resin usage and facilitating the traceability of recycled and bio-based content within the composite matrix.

The dynamics of the Polyurethane Resin Composite Market are powerfully shaped by a complex interplay of demand drivers, material constraints, and emerging technological opportunities, which collectively determine the market's trajectory and profitability. The primary driving force is the imperative for lightweighting across the transportation sectors, particularly in electric vehicles, where reduced mass directly translates into extended battery range and improved energy efficiency. This is augmented by increasing regulatory pressures globally to enhance infrastructure resilience and sustainability, prompting greater adoption of durable, low-maintenance PU composites in construction and civil engineering projects. However, the market faces significant headwinds due to the inherent volatility and dependence on fossil fuel sources for key raw materials, primarily MDI (Methylene diphenyl diisocyanate) and TDI (Toluene diisocyanate), which subjects the industry to geopolitical and petrochemical market risks.

Restraints are also imposed by the challenges associated with the end-of-life recycling of thermoset polyurethane composites. While PU materials offer excellent durability, the current infrastructure for separating and reusing fiber reinforcement from the resin matrix remains underdeveloped and costly, posing an environmental challenge and hindering the market’s full commitment to circularity. This constraint necessitates significant investment in advanced chemical or mechanical recycling technologies. Conversely, substantial opportunities arise from the rapid development and commercialization of bio-based polyols derived from renewable sources like castor oil or soy, which offer a pathway to reduce the environmental footprint and stabilize raw material sourcing, aligning with global corporate sustainability goals.

The impact forces influencing the market are high, driven by technological leaps in fiber-matrix adhesion and processing automation. The successful scale-up of techniques like Continuous Compression Molding (CCM) and high-throughput pultrusion systems is dramatically reducing cycle times and enabling composites to compete economically with traditional materials like steel and aluminum in mass-market applications. These technological advancements, coupled with robust demand from the wind energy sector for increasingly large and efficient turbine blades, create a powerful positive feedback loop, ensuring sustained market growth despite the persistent challenge of managing input costs and developing scalable recycling solutions.

The Polyurethane Resin Composite Market is systematically segmented based on various criteria, including the type of fiber used for reinforcement, the final product type or form, and the end-use application. Understanding these segmentations is critical for market stakeholders as it highlights where the highest growth opportunities lie and which material combinations are gaining traction across different industrial verticals. The market segmentation reflects the tailored nature of polyurethane composites, where the choice of reinforcement—such as glass, carbon, or natural fibers—directly dictates the composite's mechanical performance, weight, and cost profile, catering to specific regulatory and performance requirements in sectors like aerospace versus construction.

Analysis by fiber type shows that glass fiber composites dominate the volume share due to their widespread use in pultruded profiles and panel manufacturing, offering an excellent balance of strength, corrosion resistance, and affordability. However, the fastest growth is observed in carbon fiber composites, primarily driven by niche, high-value applications requiring extreme stiffness, low weight, and fatigue resistance, typical in high-performance automotive platforms and advanced industrial robotics. Furthermore, the segmentation by product form, notably into structural composites (for load-bearing applications) and non-structural composites (for insulation and cladding), helps categorize the market based on functional requirements and processing complexity.

The application segmentation is the most impactful driver, with the construction sector leading consumption volume due to the demand for energy-efficient insulation materials and durable structural components like window frames and door skins. Meanwhile, the transportation segment, encompassing automotive, rail, and marine, represents the most significant value growth segment, as OEMs prioritize polyurethane composites for complex components like battery enclosures, exterior body panels, and chassis components to achieve aggressive lightweighting targets critical for the electrification transition. These diverse needs necessitate continuous R&D investment across all segments to refine resin chemistries and processing techniques.

The value chain of the Polyurethane Resin Composite Market begins with the upstream sourcing of crucial chemical precursors: polyols (polyether or polyester based) and isocyanates (MDI, TDI, HDI). This upstream stage is dominated by large petrochemical and chemical corporations, and it heavily influences the composite material cost and quality, particularly given the volatility of crude oil and natural gas prices, which are essential feedstocks. Securing stable and sustainable sourcing, including the increasing integration of bio-based polyols, is a strategic focus area for composite manufacturers seeking resilience and a reduced environmental footprint. Following the production of these liquid resins, the chain moves to the processing of reinforcement fibers, primarily glass fiber rovings or carbon fiber tows, which are often purchased from specialized textile and fiber companies.

The midstream segment involves the core composite manufacturing processes, including compounding, lamination, pultrusion, and various molding techniques like Reaction Injection Molding (RIM) or Resin Transfer Molding (RTM). This stage requires significant capital investment in highly specialized machinery and technology to ensure optimal fiber wetting and resin curing. Direct manufacturers often specialize in specific composite forms (e.g., pultruded profiles for construction or injection-molded parts for automotive interiors). Quality control and process efficiency in the midstream determine the final performance and structural integrity of the composite part, making technological expertise in polymerization and processing critical for competitive advantage.

The downstream segment encompasses the distribution and application of the finished composite products to end-users. Distribution channels are typically dual: direct sales are common for large volume customers like automotive OEMs and major wind turbine manufacturers, enabling customized material specifications and just-in-time delivery. Indirect distribution utilizes specialized distributors and fabricators, particularly for standard products like construction panels and generic industrial components. The ultimate success in the downstream market depends on technical service and application support, helping engineers integrate these advanced materials effectively into complex designs. Key stakeholders in the downstream segment include construction firms, automotive assemblers, and specialized system integrators in the energy sector.

The primary potential customers and end-users of Polyurethane Resin Composites are diverse industrial entities that require materials offering a unique combination of lightweight properties, high mechanical strength, corrosion resistance, and exceptional durability. The automotive industry represents a cornerstone customer base, particularly Original Equipment Manufacturers (OEMs) focused on the rapid expansion of Electric Vehicle (EV) platforms. These customers utilize PU composites extensively for components such as battery housings and protective structures, exterior body panels, and interior load-bearing parts, where weight reduction is paramount for maximizing vehicle range and energy efficiency, positioning them as high-volume, high-value purchasers.

Another major customer segment resides in the global construction and infrastructure sector. This includes commercial building developers, civil engineering firms, and manufacturers of prefabricated housing elements. These entities seek PU composites for window and door profiles, structural insulation panels (SIPs), bridge components, and cladding materials due to their excellent thermal insulation capabilities, resistance to moisture and chemicals, and long service life, significantly lowering long-term maintenance costs compared to traditional materials like wood or metal. Regulatory mandates for energy efficiency in buildings further solidify this customer base.

Furthermore, the renewable energy sector, specifically wind turbine manufacturers, constitutes a critical customer group. As turbine blades become progressively larger to capture more wind energy, the demand for high-stiffness, low-weight, and fatigue-resistant polyurethane composites for blade manufacturing continues to accelerate. These manufacturers require specialized PU resin systems that offer rapid curing and excellent adhesive properties to bond massive composite structures efficiently. Other potential customers include aerospace contractors (for non-structural interior and minor exterior parts), marine vessel builders (for deck components and hulls requiring corrosion resistance), and manufacturers of electrical and electronic enclosures.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.8 Billion |

| Growth Rate | 8.2% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Covestro AG, Huntsman Corporation, BASF SE, The Dow Chemical Company, Sika AG, Scott Bader Company Ltd., Hexion Inc., LyondellBasell Industries N.V., Wanhua Chemical Group Co., Ltd., Henkel AG & Co. KGaA, RTP Company, Gurit Holding AG, Mitsubishi Chemical Corporation, PolyOne Corporation (Avient), DSM N.V., DIC Corporation, Toray Industries Inc., Solvay S.A., AOC Resins, and Zhejiang Huafon Spandex Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Polyurethane Resin Composite Market is defined by advanced processing methods designed to maximize production speed, minimize cure times, and ensure excellent fiber impregnation, which are critical for high-volume applications like automotive parts. Reaction Injection Molding (RIM) and its high-pressure variant, HP-RTM (High-Pressure Resin Transfer Molding), stand as pivotal technologies. These methods allow for the rapid injection and curing of low-viscosity polyurethane resin systems within a closed mold containing the fiber reinforcement, dramatically reducing cycle times compared to traditional epoxy or polyester systems. The ability of PU resins to cure quickly at relatively low temperatures without generating excessive heat is a core competitive advantage, enabling faster throughput and lower energy consumption during manufacturing.

Pultrusion technology is another vital process, specifically dominating the production of continuous, constant cross-section profiles, widely used in construction (e.g., window lineals, bridge decks). Recent innovations in PU pultrusion focus on developing faster-curing systems and optimizing die design to increase pull speeds while maintaining high fiber volume fraction and structural quality. Furthermore, the increasing complexity of composite parts in the automotive sector has spurred significant investment in automated processes, including robotic handling of preforms and automated fiber placement (AFP), ensuring precise placement of reinforcement for optimal load distribution and structural performance in safety-critical components.

Beyond processing, significant technological attention is directed towards sustainable material development. This includes the catalytic synthesis of bio-based polyols, utilizing renewable resources to replace petrochemical derivatives, which improves the overall sustainability profile of the composite. Additionally, advanced surface treatment technologies for fibers are being researched to improve the adhesion between the PU matrix and the reinforcement, a crucial factor in achieving maximum composite strength and long-term durability, especially when exposed to moisture or temperature extremes. These technological thrusts are collectively aimed at lowering manufacturing costs, increasing material performance metrics, and meeting rising environmental expectations.

Polyurethane (PU) composites offer significant advantages, primarily faster processing times (rapid cure cycles, especially via HP-RTM), excellent toughness, superior impact resistance, and inherent flexibility in formulation. PU systems typically exhibit better adhesion to various fibers and can be processed at lower temperatures, making them highly suitable for automated, high-volume production in the automotive and construction industries.

The market is actively pursuing sustainability through two main avenues: utilizing bio-based polyols derived from renewable resources (e.g., castor or soy oil) to reduce reliance on petrochemicals, and investing heavily in advanced chemical recycling technologies. Chemical recycling, such as glycolysis or hydrolysis, aims to break down the PU matrix back into usable polyols and reclaim the reinforcing fibers, moving the thermoset materials towards a viable circular economy model.

The Transportation segment, particularly sub-segments related to Electric Vehicle (EV) manufacturing and aerospace, is anticipated to register the highest Compound Annual Growth Rate (CAGR). This acceleration is driven by the necessity for advanced lightweight materials, like Carbon Fiber Reinforced Polyurethane (CFR-PU), for critical components such as battery enclosures, chassis structures, and high-performance body panels, directly impacting vehicle range and safety standards.

RIM and HP-RTM technologies are fundamental enablers of market growth as they allow for the fast and economical manufacturing of large, complex PU composite parts. These methods utilize the rapid reactivity of polyurethane chemistry, significantly reducing the cure time to minutes or even seconds, thereby making PU composites competitive for mass-market applications that require quick cycle times and high part integrity.

The market faces significant cost fluctuations stemming from the upstream petrochemical industry, which supplies isocyanates (MDI, TDI) and polyols. Volatility in crude oil and natural gas prices directly affects the cost of these precursors. Geopolitical instability and supply chain disruptions can exacerbate these price swings, pressuring profit margins for composite manufacturers and driving the strategic necessity for diversifying into bio-based and recycled raw material sources.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.