ID : MRU_ 437478 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

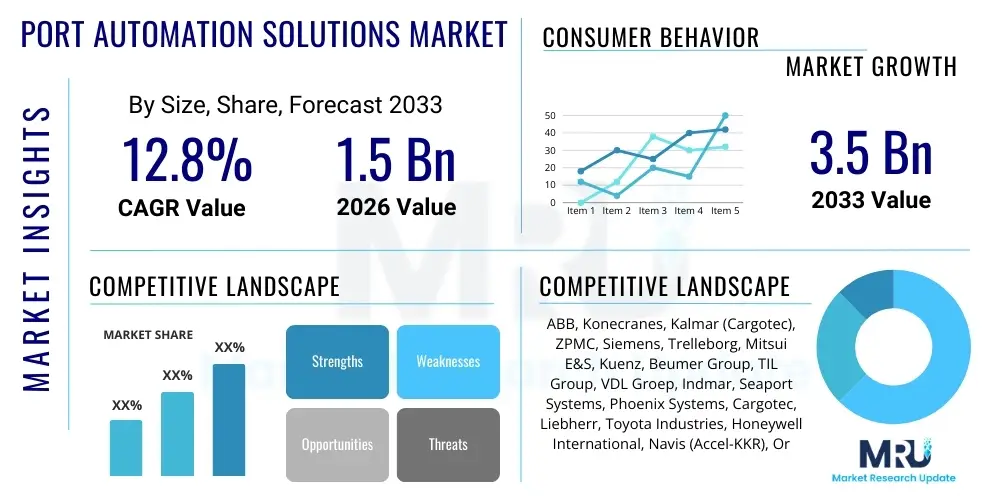

The Port Automation Solutions Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2026 and 2033. The market is estimated at $1.5 Billion USD in 2026 and is projected to reach $3.5 Billion USD by the end of the forecast period in 2033. This significant expansion is primarily driven by the escalating global demand for efficient supply chain management, the necessity for enhanced safety protocols in terminal operations, and substantial investment in digitalization and infrastructure upgrades across major international shipping hubs. The adoption of advanced technologies, including Artificial Intelligence (AI) and Internet of Things (IoT), is crucial for achieving the operational efficiencies required to handle increasing cargo volumes, especially within congested urban port environments.

The Port Automation Solutions Market encompasses technologies, equipment, and services designed to minimize human intervention and maximize efficiency, throughput, and safety in marine terminals and ports. Key solutions include Automated Guided Vehicles (AGVs), Automated Stacking Cranes (ASCs), Automated Rail-Mounted Gantry (ARMG) cranes, advanced Terminal Operating Systems (TOS), and sophisticated sensing technologies that manage the complex movement of containers from ship to shore and storage areas. These solutions are vital for modernizing aging infrastructure and addressing labor shortages while ensuring that global trade can move resiliently, irrespective of external disruptions or regulatory mandates. The core function of these systems is to optimize the planning, execution, and monitoring of container handling processes in real time, leading to reduced turnaround times for vessels and lower operational costs per container move.

Major applications of port automation span across container terminals, bulk cargo ports, and specific facilities handling roll-on/roll-off (RoRo) cargo, with container operations representing the largest and most complex segment for integrated automation. The benefits realized from implementing these systems are substantial, extending beyond mere cost savings to include higher accuracy in inventory management, reduced carbon emissions through optimized equipment usage, and significantly improved worker safety by removing personnel from hazardous operational zones. The shift toward electrification of automated equipment further supports sustainability goals, aligning with international maritime regulations aimed at decarbonization. The integration complexity of these solutions, however, requires strong partnerships between port authorities, technology vendors, and system integrators to ensure seamless deployment and long-term operational success.

The market is predominantly driven by macroeconomic factors such as increasing global seaborne trade volumes, intense competition among ports to serve as preferred logistical gateways, and governmental initiatives supporting smart port development. The necessity to operate terminals 24/7 in various weather conditions, coupled with the rising cost of manual labor, makes the economic case for automation compelling. Furthermore, geopolitical shifts requiring rapid and adaptable supply chain responses have underscored the strategic value of highly automated ports capable of dynamic throughput adjustment. Continuous innovation in sensor technology, machine learning algorithms for predictive maintenance, and the rollout of 5G connectivity within port areas are further accelerating the rate of adoption globally.

The global Port Automation Solutions Market is characterized by robust growth, driven primarily by the pursuit of operational excellence and supply chain resilience across the maritime logistics sector. Business trends indicate a strong move toward full-scale digitalization, often leveraging subscription-based models for advanced Terminal Operating Systems (TOS) and maintenance services, shifting capital expenditure (CapEx) to operational expenditure (OpEx) for port operators. Leading technology providers are focusing on developing highly interoperable systems, utilizing open standards to facilitate easier integration of diverse equipment from multiple vendors, addressing a historical challenge of proprietary lock-in. Strategic mergers and acquisitions are common as major players seek to consolidate expertise in specific automation components, such as automated guided vehicles (AGVs) or specialized software analytics platforms, thereby offering comprehensive, end-to-end solutions to global port authorities and private terminal operators.

Regionally, Asia Pacific (APAC) stands as the dominant market, particularly driven by heavy investment in new mega-ports in China, South Korea, and Southeast Asian nations that are designed for high throughput from inception, favoring greenfield automation projects. North America and Europe, while having higher initial automation penetration, primarily focus on brownfield modernization projects, retrofitting existing terminals with modular automation elements such as remote crane operation and enhanced gate automation systems to maximize utilization of constrained land space. Latin America and the Middle East & Africa (MEA) are emerging as high-potential growth regions, backed by state-funded initiatives aimed at establishing regional transshipment hubs, necessitating competitive, high-throughput capabilities that only automation can provide efficiently. The development of the Suez Canal economic zones and strategic maritime corridors further stimulates automation demand in the MEA region.

Segment trends reveal that the Equipment segment, specifically automated material handling equipment like cranes and AGVs, holds the largest market share due to high capital investment requirements, while the Software and Services segment is projected to exhibit the fastest growth rate. This accelerated growth in services is fueled by the critical need for sophisticated integration services, cybersecurity solutions tailored for operational technology (OT) networks in ports, and long-term maintenance contracts ensuring maximum uptime. Within the technology component, solutions integrating artificial intelligence for predictive congestion management and optimizing stacking strategies are gaining significant traction, proving essential for ports operating near their capacity limits. Furthermore, there is a distinct segmentation shift towards modular and scalable automation packages, catering specifically to smaller or mid-sized ports that cannot undertake complete terminal overhauls but still require productivity gains.

Common user questions regarding the impact of AI on port automation center around its ability to truly optimize complex operational decisions, the required investment in data infrastructure, and the potential displacement of skilled labor. Users frequently inquire about how AI-driven predictive maintenance can reduce equipment downtime, how machine learning algorithms improve the efficiency of yard management (especially dynamic stacking and retrieval), and the role of computer vision in enhancing security and operational flow at the gate and quay side. A primary concern is the complexity of integrating AI models into existing legacy Terminal Operating Systems (TOS) and ensuring data privacy and security across connected operational assets. Overall, users expect AI to be the fundamental catalyst for moving from mere automation (performing tasks automatically) to intelligent autonomy (performing tasks optimally and adapting to real-time changes), ultimately transforming ports into self-learning, hyper-efficient entities that can handle volatility in global shipping schedules and cargo volumes.

The dynamics of the Port Automation Solutions Market are dictated by a powerful combination of driving factors (D), inherent restraints (R), emerging opportunities (O), and pervasive impact forces that shape investment decisions and technological adoption. The primary drivers include the urgent need for operational efficiency to manage rising global trade volumes, mandatory safety regulations, and the strategic push by governments to develop smart infrastructure hubs. Restraints primarily involve the substantial upfront capital expenditure required for full automation implementation, the complexity of integrating new automated systems with outdated legacy infrastructure (especially in brownfield sites), and significant resistance from labor unions concerning job displacement. However, these restraints are often balanced by the major opportunity inherent in the development of modular and scalable automation solutions tailored for mid-sized ports, the expansion into emerging markets, and the potential for leveraging 5G and IoT for remote operations and enhanced data analytics, which drastically reduces operational vulnerability and increases efficiency.

The market faces several significant impact forces. Economic volatility, particularly related to global trade disputes or recessions, can immediately affect port investment cycles, causing project delays or scope reductions. Conversely, the environmental impact force, driven by global climate targets and IMO regulations, pushes ports towards electric and autonomous equipment, which often requires a higher degree of automation integration. Technological impact forces, centered on the rapid advancement of AI, machine learning, and sensor fusion, continuously redefine what is achievable in terms of throughput and optimization, requiring companies to constantly update their product offerings to remain competitive. Furthermore, geopolitical stability plays a crucial role; regions that are strategically important for global trade routes tend to prioritize and fund automation projects to secure their logistical competitiveness, thereby accelerating market growth in key maritime corridors.

Understanding these intertwined forces is crucial for stakeholders. Drivers compel action, restraints necessitate innovative mitigation strategies (like phased implementation or modular design), and opportunities guide R&D investments. The ultimate impact force is competitive differentiation; ports that successfully automate and optimize their operations gain a decisive competitive advantage in attracting major shipping alliances and high-value cargo, reinforcing a cycle of adoption and growth across the entire ecosystem. The shift towards autonomous operation is not just an efficiency upgrade but a fundamental requirement for maintaining relevance in the rapidly evolving global supply chain network, where speed and reliability are paramount.

The Port Automation Solutions Market is intricately segmented based on technology type, level of automation, equipment utilized, and application area, allowing for tailored deployment strategies across various port sizes and operational needs. A core segmentation approach differentiates between equipment, software, and services, reflecting the high capital investment associated with physical assets versus the high recurring revenues derived from sophisticated software licenses and ongoing maintenance contracts. The market also distinguishes between greenfield projects (newly built ports designed for full automation) and brownfield projects (existing ports undergoing phased retrofitting), with brownfield modernization currently dominating mature markets like Europe and North America due to land constraints and the high cost of new infrastructure development. This nuanced segmentation is critical for market players to develop targeted sales strategies, focusing on either high-margin equipment sales or stable, long-term service contracts that provide recurring revenue streams.

The value chain for the Port Automation Solutions Market begins with upstream activities focused on advanced manufacturing, involving specialized component suppliers for robotics, heavy machinery, sophisticated sensors, and high-performance computing hardware necessary for control systems. These suppliers, often specialized industrial companies, provide critical input such as robust electric motors, high-precision positioning sensors (GPS, LiDAR), and industrial communication hardware (5G/private LTE components). The core value addition occurs at the system integration and technology development stage, where key automation vendors (like Konecranes, Kalmar, and ZPMC) design, assemble, and integrate the complex interplay of physical equipment (cranes, vehicles) and proprietary software (TOS, ECS). This integration phase requires immense expertise in maritime logistics, mechanical engineering, and software development, representing the highest value capture point in the chain, as it transforms disparate components into a unified, operational terminal system.

Downstream activities involve the deployment, installation, commissioning, and long-term maintenance of the automated systems. Port authorities or private terminal operators are the primary end-users, working closely with the automation vendors during the often multi-year deployment process. The distribution channel is predominantly direct, given the custom nature and high cost of these integrated solutions; sales cycles are long and require direct engagement, detailed technical specifications, and competitive bidding processes. Indirect channels might include specialized consulting firms or engineering procurement and construction (EPC) contractors who bundle automation solutions into larger infrastructure development projects, especially in new port construction within emerging markets, facilitating the entry of major vendors into complex international tenders.

Post-installation, the value chain shifts to services, which are becoming increasingly critical. Maintenance and support services, often delivered remotely through secure network connections, ensure system uptime and continuous performance optimization. The collection and analysis of operational data, often requiring advanced AI tools, provides feedback loops that help port operators refine their strategies and aid vendors in developing improved software updates. This ongoing service relationship generates stable, high-margin revenue streams and solidifies customer loyalty. The entire value chain is characterized by a high degree of technical expertise, regulatory compliance requirements, and significant intellectual property concentrated in the software and system integration layers, creating high barriers to entry for new competitors.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.5 Billion USD |

| Market Forecast in 2033 | $3.5 Billion USD |

| Growth Rate | 12.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB, Konecranes, Kalmar (Cargotec), ZPMC, Siemens, Trelleborg, Mitsui E&S, Kuenz, Beumer Group, TIL Group, VDL Groep, Indmar, Seaport Systems, Phoenix Systems, Cargotec, Liebherr, Toyota Industries, Honeywell International, Navis (Accel-KKR), Orbcomm |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological foundation of the Port Automation Solutions Market is rapidly evolving, driven by the convergence of industrial automation with advanced digital technologies. Core technologies include sophisticated Terminal Operating Systems (TOS) that act as the central nervous system, coordinating all movements and inventory, often now incorporating cloud-based architectures for enhanced scalability and real-time data processing. Crucially, the deployment of high-bandwidth, low-latency communication networks, specifically private 5G and industrial IoT (IIoT) frameworks, is essential for enabling reliable communication between the central control room and mobile automated equipment such as AGVs and remote-controlled cranes. This robust connectivity facilitates remote operations and enables the collection of massive datasets necessary for subsequent analysis.

Furthermore, the market relies heavily on precision positioning and navigation technologies. Differential GPS (DGPS), Real-Time Kinematics (RTK) GPS, LiDAR, and various sensor fusion techniques are integrated into equipment to ensure millimeter-level accuracy required for automated stacking and loading operations, mitigating risks of collision and maximizing density. The hardware landscape is dominated by heavy-duty, ruggedized equipment designed for 24/7 operations in harsh marine environments, including highly specialized Automated Stacking Cranes (ASCs) and rail-mounted gantry (RMG) systems that are increasingly electrified to meet sustainability targets and reduce operating expenses. The shift towards electrification necessitates advanced battery management systems and integrated power solutions that can handle the massive energy demands of a fully automated terminal.

Finally, the growing maturity of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally changing the optimization layer. AI algorithms are employed for predictive analytics (maintenance forecasting), decision support (dynamic resource allocation), and process automation (unmanned gate processing). Additionally, robotics and autonomous vehicles, particularly Automated Guided Vehicles (AGVs) and Auto-Strads, utilizing sophisticated navigation algorithms and safety protocols, form the backbone of automated horizontal transport within the terminal. Cybersecurity solutions tailored for operational technology (OT) networks are also mandatory, protecting the sensitive control systems from increasing cyber threats, ensuring operational resilience against external attacks that could halt trade flow.

The primary driver is the necessity for enhanced operational efficiency and increased throughput capacity to handle soaring global container volumes reliably, coupled with the need to mitigate rising operational costs, especially labor expenses, and comply with international safety regulations.

Greenfield automation involves building entirely new ports designed for full automation from the ground up, offering maximum optimization potential. Brownfield projects involve retrofitting and upgrading existing operational terminals, which often requires phased implementation and modular solutions to overcome integration challenges with legacy infrastructure.

AI improves operational effectiveness by enabling intelligent decision-making, including predictive maintenance to minimize equipment failure, optimizing yard stacking strategies for maximum density and faster retrieval, and dynamically adjusting resource allocation in real-time based on fluctuating demands and external factors.

The Software and Services segment, particularly advanced Terminal Operating Systems (TOS) and specialized integration and maintenance services, is anticipated to exhibit the fastest growth, driven by the increasing complexity of AI and IoT integration and the growing demand for continuous optimization and secure remote management.

The most significant restraint is the extremely high initial Capital Expenditure (CapEx) required for acquiring and integrating specialized automated equipment, software, and the necessary underlying infrastructure, often compounded by long project timelines and integration risk.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.