ID : MRU_ 433376 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

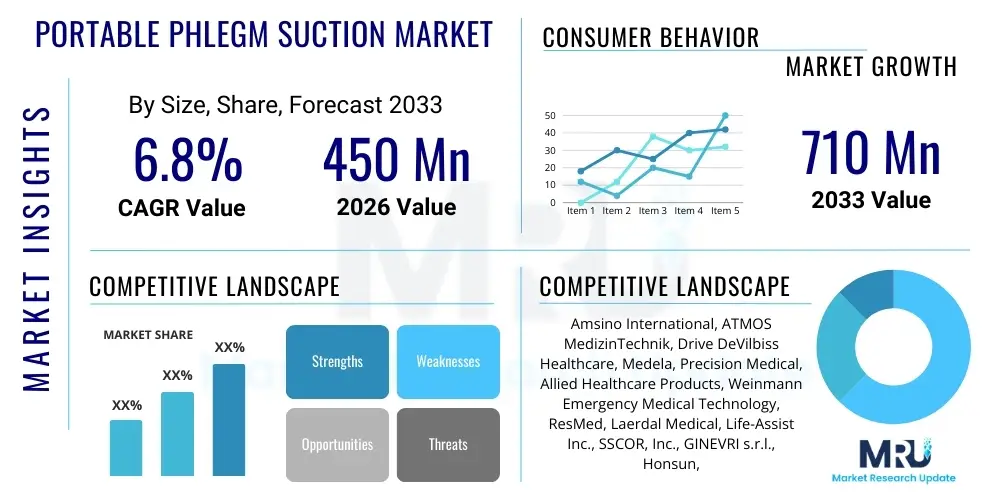

The Portable Phlegm Suction Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 710 Million by the end of the forecast period in 2033.

The Portable Phlegm Suction Market encompasses the manufacturing, distribution, and utilization of medical devices designed to remove excess mucus, saliva, blood, or other secretions from the respiratory tract of patients. These devices, often battery-operated and lightweight, are crucial for maintaining airway patency in emergency settings, home care environments, ambulances, and non-acute hospital wards. The primary function of these aspirators is to prevent aspiration pneumonia, improve breathing, and aid patients suffering from conditions such as Chronic Obstructive Pulmonary Disease (COPD), cystic fibrosis, neurological disorders affecting swallowing, or those recovering from surgery requiring tracheal intubation. Their portability enhances their utility, making immediate airway management accessible outside traditional clinical settings.

The core product category includes manual and electric suction units, categorized primarily by their vacuum capabilities (high, medium, and low) and power sources. Major applications span pre-hospital care, institutional care (hospitals, clinics), and the rapidly expanding segment of home healthcare. The increasing geriatric population, which is highly susceptible to respiratory illnesses and difficulty in clearing secretions, acts as a foundational driver for market growth. Furthermore, the rising global prevalence of chronic respiratory diseases, coupled with growing awareness regarding the importance of timely airway clearance, reinforces the demand for these essential medical devices. The shift towards patient-centric care and the preference for managing chronic conditions at home significantly boost the adoption rate of user-friendly portable models.

Key benefits derived from these devices include immediate intervention capability, reduced risk of secondary infections associated with poor secretion management, and improved quality of life for long-term respiratory patients. Driving factors include technological advancements leading to more efficient, quieter, and lighter units, favorable reimbursement policies in developed economies supporting home-based medical equipment purchases, and the expanding presence of emergency medical services (EMS) which rely heavily on these devices for field operations. The ongoing decentralization of healthcare, driven by cost-containment measures and patient preference, positions the portable phlegm suction market for robust and sustained expansion throughout the forecast period.

The Portable Phlegm Suction Market is experiencing dynamic growth, propelled by robust business trends emphasizing miniaturization, enhanced battery life, and integration of smart features for better patient monitoring and compliance. Leading manufacturers are focusing on mergers and acquisitions to consolidate market share and invest in research and development to address critical restraints such as noise pollution and the need for standardized sterile disposable components. Key business strategies revolve around expanding distribution networks, especially in high-growth emerging economies in the Asia Pacific, and securing long-term contracts with major ambulance services and nursing homes. The shift in manufacturing emphasis toward energy-efficient, high-flow rate yet gentle suction systems is redefining competitive advantage in this sector, moving away from bulky, static hospital-grade equipment towards compact, personal medical solutions.

Regionally, North America and Europe currently dominate the market due to established healthcare infrastructure, high incidence of chronic respiratory conditions, and strong reimbursement frameworks for medical devices. However, the Asia Pacific region is poised to exhibit the highest CAGR, primarily fueled by massive infrastructural investments in healthcare, increasing disposable incomes, and the sheer volume of the patient base requiring respiratory support in countries like China and India. Regional trends also indicate a growing preference for single-use catheters and collection canisters to mitigate infection risks, driving parallel growth in the consumables segment. Regulatory harmonization efforts across regions are beginning to streamline market entry for international players, increasing cross-border trade and investment flows.

Segmentation trends highlight the dominance of the electric-powered segment over manual suction units, attributed to superior efficiency and consistency in vacuum delivery. Within end-users, the Home Care setting is projected to be the fastest-growing segment, significantly outpacing hospitals, clinics, and pre-hospital settings, reflecting the global migration of healthcare services outside the conventional institutional environment. Furthermore, the market segmentation by product type indicates increased demand for canister-based systems over bag-based systems due to ease of disposal and enhanced safety protocols. Strategic differentiation based on features like adjustable pressure settings, lightweight design, and low maintenance requirements is crucial for manufacturers targeting specific market segments, particularly vulnerable patient groups such as pediatrics and geriatrics.

User queries regarding AI's influence in the Portable Phlegm Suction Market predominantly focus on optimizing performance, predictive maintenance, and integrating devices into broader telehealth ecosystems. Common questions inquire about whether AI can automatically adjust suction pressure based on patient biofeedback (e.g., changes in oxygen saturation or heart rate), how AI diagnostics can predict filter clogs or battery failures before they occur, and the potential for AI-powered monitoring systems to alert caregivers remotely if suction is required or if the patient is experiencing a high risk of aspiration. Users are keenly interested in the possibility of AI enhancing personalized care through data analytics gathered by smart suction devices, transforming them from passive tools into active, responsive components of respiratory management. This anticipation summarizes the expectation that AI will lead to smarter, safer, and more personalized phlegm suction routines, significantly lowering caregiver burden and improving patient outcomes in chronic care settings.

The market dynamics of the Portable Phlegm Suction Market are governed by a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively manifesting as powerful impact forces shaping the industry trajectory. The primary drivers include the accelerated global aging population leading to higher prevalence of respiratory conditions requiring mechanical assistance, the rapid expansion of emergency medical services (EMS) necessitating compact and reliable equipment, and the growing preference for home healthcare settings where portable devices are indispensable. These factors collectively push market growth by increasing the installed base and frequency of device usage across diverse geographical and clinical environments. Technological advancements, such as the development of lightweight lithium-ion batteries and quieter pump mechanisms, further enhance device appeal and adoption rates, securing their position as standard components in patient care kits.

Conversely, the market faces significant restraints that dampen its full growth potential. High acquisition costs associated with advanced, feature-rich portable suction units, particularly in developing economies, limit widespread adoption among lower-income demographics or smaller healthcare facilities. Furthermore, stringent regulatory approval processes, especially concerning battery safety and sanitation standards for reusable parts, can slow down product introduction and increase operational expenses for manufacturers. A critical restraint is the need for specialized training for caregivers and family members using these devices in home settings, coupled with the potential risk of aspiration or injury if the suction technique is applied incorrectly, necessitating robust user education programs.

Opportunities in the market are abundant and strategically aligned with global healthcare trends. There is a strong potential for penetration in untapped emerging markets where healthcare infrastructure is rapidly developing and disposable income is rising. The development of intelligent, connected devices integrated with telehealth platforms presents a massive opportunity for remote monitoring and chronic care management. Furthermore, focusing on product line diversification, specifically developing cost-effective, high-volume consumables (such as disposable canisters and sterile catheters), represents a stable revenue stream and an avenue for market expansion. These impact forces—high demand versus regulatory hurdles and cost constraints—will dictate competitive strategies, pushing companies toward innovation in battery technology and simplified user interfaces over the forecast period.

The Portable Phlegm Suction Market is comprehensively segmented across several crucial parameters including product type, end-user, and power source, enabling detailed analysis of market dynamics and targeted strategic investment. Understanding these segmentations is paramount for manufacturers to align their product offerings with specific clinical needs and budgetary constraints. The market segmentation reveals varying growth rates and adoption patterns, with technological sophistication heavily influencing the performance of specific segments. For instance, the transition from piston pumps to diaphragm pumps impacts the noise level and efficiency of portable units, directly affecting patient acceptance in sensitive settings like pediatric care or hospice.

The value chain for the Portable Phlegm Suction Market begins with upstream activities involving the sourcing of raw materials and specialized components, such as high-grade plastics for device casings and consumables, advanced microprocessors for control systems, and critical battery technology (lithium-ion cells). Key upstream players include specialized component suppliers, technology providers for quiet pump mechanisms, and battery manufacturers. Maintaining rigorous quality control and securing reliable, ethical sourcing for these components is vital for ensuring the safety and performance of the final medical device. Cost efficiencies achieved at this stage, particularly through bulk procurement of standardized components, directly influence the final retail price and market competitiveness of the suction units.

Midstream activities encompass the core manufacturing and assembly processes, including device design, sterile assembly, regulatory compliance checks, and packaging. Direct distribution involves manufacturers selling directly to large institutional buyers such as hospital chains or governmental health agencies, often characterized by high-volume, lower-margin transactions. Indirect distribution, conversely, relies heavily on a network of third-party medical device distributors, regional wholesalers, and specialized e-commerce platforms. These intermediaries play a critical role in inventory management, providing localized technical support, and navigating complex regional regulatory landscapes, especially in fragmented markets where direct manufacturer presence is limited. The efficiency of this distribution channel significantly impacts the time-to-market and accessibility for home care users.

Downstream activities focus on reaching the end-users: hospitals, emergency services, and individual home care patients. Downstream analysis includes the role of specialized equipment providers, pharmacies, and online retailers that cater directly to consumers. Post-sale services, including technical support, maintenance, calibration, and replacement of consumables, form a crucial part of the downstream value proposition. The nature of this device necessitates a robust consumables supply chain, as ongoing sales of sterile catheters and collection canisters generate recurring revenue. Optimization of the logistics network to ensure timely delivery of both the primary device and its necessary disposables is paramount for enhancing customer satisfaction and reinforcing brand loyalty in this clinically sensitive market.

The potential customer base for the Portable Phlegm Suction Market is diverse and spans both institutional healthcare providers and individual users managing chronic conditions in non-clinical settings. Primary institutional buyers include hospitals, ranging from large university medical centers to small rural clinics, particularly their emergency departments, intensive care units (ICUs), and respiratory therapy wards. Emergency Medical Services (EMS) organizations, including public ambulance services and private air/ground transport teams, represent another critical customer segment, relying on the compact, robust nature of these devices for immediate field resuscitation and stabilization. Long-term care facilities, nursing homes, and rehabilitation centers also constitute significant buyers, as they manage a high volume of geriatric patients with swallowing difficulties or chronic respiratory challenges.

On the non-institutional side, the fastest-growing customer group comprises individual patients and their caregivers managing chronic diseases such as COPD, neuromuscular disorders (e.g., ALS, muscular dystrophy), or post-operative patients requiring temporary airway assistance at home. This demographic increasingly seeks devices that are intuitive, quiet, and easily portable for travel and daily routines. Furthermore, military medics and disaster relief organizations are niche but important customers, requiring ultra-reliable, field-ready portable suction units for deployment in challenging environments where access to standard medical infrastructure is compromised. The customer acquisition strategy must therefore be bifurcated, addressing the specific procurement cycles and regulatory compliance needs of institutional purchasers, while simultaneously focusing on user-friendliness and insurance coverage for home-based consumers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 710 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Amsino International, ATMOS MedizinTechnik, Drive DeVilbiss Healthcare, Medela, Precision Medical, Allied Healthcare Products, Weinmann Emergency Medical Technology, ResMed, Laerdal Medical, Life-Assist Inc., SSCOR, Inc., GINEVRI s.r.l., Honsun, Vadi, Yuwell, Kangshun Medical, Drive Medical, Integra LifeSciences, Becton Dickinson (BD), Sunset Healthcare Solutions |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Portable Phlegm Suction Market is rapidly evolving, driven primarily by the need for enhanced portability, quiet operation, and improved suction efficacy while minimizing tissue damage. Key technological advancements center around the development of high-efficiency, oil-free vacuum pumps, predominantly diaphragm or piston-based systems, which reduce maintenance requirements and increase device longevity. Modern units feature precise, microprocessor-controlled pressure regulation systems that allow caregivers to fine-tune the negative pressure level, essential for tailoring treatment to diverse patient populations, particularly neonates and individuals with fragile respiratory tracts. The standardization of disposable collection systems, utilizing hydrophobic filters and gel solidification agents, represents a significant technological leap in infection control, reducing biohazard risk during disposal.

Battery technology forms the cornerstone of portable device performance. The shift from heavier Nickel-Cadmium or Sealed Lead Acid batteries to lightweight, high-density Lithium-ion batteries has dramatically extended operating times while reducing the overall weight and size of the units, making them genuinely portable and suitable for extended field use or international travel. Furthermore, integrating smart technology, such as Bluetooth connectivity and near-field communication (NFC) capabilities, allows the portable suction units to interface with smart device applications. This integration facilitates automated logging of suction events, monitors battery health remotely, and provides real-time maintenance feedback to both users and maintenance providers, enhancing operational reliability and data capture for clinical research.

The future of the technology landscape is geared towards miniaturization and integration with other respiratory care technologies. The adoption of silent operation modes, often achieved through advanced dampening materials and motor isolation techniques, is crucial for patient comfort in home care settings. Additionally, ongoing research focuses on developing non-invasive sensing technologies integrated within the suction catheter that can provide real-time feedback on mucosal contact, aiming to prevent mucosal trauma. The push towards Internet of Medical Things (IoMT) compliance ensures that these devices can securely communicate patient usage and diagnostic data, cementing their role within the broader digital health ecosystem, optimizing resource allocation, and providing proactive care interventions based on analytical insights gathered directly from the device usage profile.

Regional dynamics play a crucial role in shaping the Portable Phlegm Suction Market, reflecting disparities in healthcare spending, disease prevalence, and regulatory frameworks. North America, comprising the United States and Canada, currently holds the largest market share, characterized by advanced healthcare infrastructure, high incidence of chronic respiratory illnesses, robust emergency medical services (EMS), and high adoption rates of technologically advanced devices. Strong reimbursement policies and high consumer awareness further cement the region's dominance. The market here is mature but continues to grow steadily, driven by replacements and upgrades to smart, connected portable units.

Europe follows North America, demonstrating significant market value due to established healthcare systems in countries such as Germany, the UK, and France. Strict European Union (EU) medical device regulations (MDR) influence product specifications, prioritizing safety and quality. The increasing geriatric population and high expenditures on home healthcare services are key growth catalysts across Western European nations, while Central and Eastern European markets show increasing potential as healthcare modernization efforts accelerate. The regional trend is towards lightweight, easy-to-sterilize portable units suitable for both professional and non-professional use.

Asia Pacific (APAC) is projected to be the fastest-growing region during the forecast period. This rapid growth is attributable to massive populations, improving healthcare access, and rising prevalence of respiratory diseases exacerbated by pollution in heavily populated nations like China and India. Government initiatives aimed at upgrading public health facilities and promoting preventative care are fueling demand. Although cost sensitivity remains a factor, the sheer volume of potential patients, coupled with increasing investments from multinational corporations expanding their manufacturing and distribution footprints in the region, makes APAC a critical growth engine.

Latin America (LATAM), and the Middle East and Africa (MEA) represent emerging markets with substantial long-term potential. Growth in these regions is driven by improvements in economic conditions, increasing penetration of global medical device manufacturers, and necessity-driven demand in underserved rural areas. While LATAM markets such as Brazil and Mexico benefit from growing private healthcare sectors, the MEA region sees demand concentrated in high-income Gulf Cooperation Council (GCC) countries, focusing on high-end medical tourism and institutional infrastructure upgrades, particularly in pre-hospital and trauma care settings.

The Portable Phlegm Suction Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between the years 2026 and 2033, driven primarily by the rising prevalence of chronic obstructive pulmonary disease (COPD) and the expansion of home healthcare services globally.

The Home Care setting segment is anticipated to witness the fastest growth rate among all end-users. This trend reflects the global decentralization of chronic patient management, increasing patient preference for at-home recovery, and improvements in portable device design facilitating non-professional use.

Key innovations include the adoption of high-density lithium-ion batteries for extended operating time, development of silent or low-noise pump mechanisms for patient comfort, and integration of microprocessor controls for precise vacuum pressure regulation, ensuring safe and effective secretion removal.

North America holds the largest share of the market, attributed to its advanced medical infrastructure, high awareness regarding respiratory care, established emergency services, and strong reimbursement coverage for essential medical equipment, supporting high product adoption rates.

Major restraints include the relatively high cost of advanced portable suction units, especially in budget-constrained emerging markets, and the persistent challenge associated with the need for specialized training for caregivers using these devices in unsupervised home environments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.