ID : MRU_ 440591 | Date : Jan, 2026 | Pages : 248 | Region : Global | Publisher : MRU

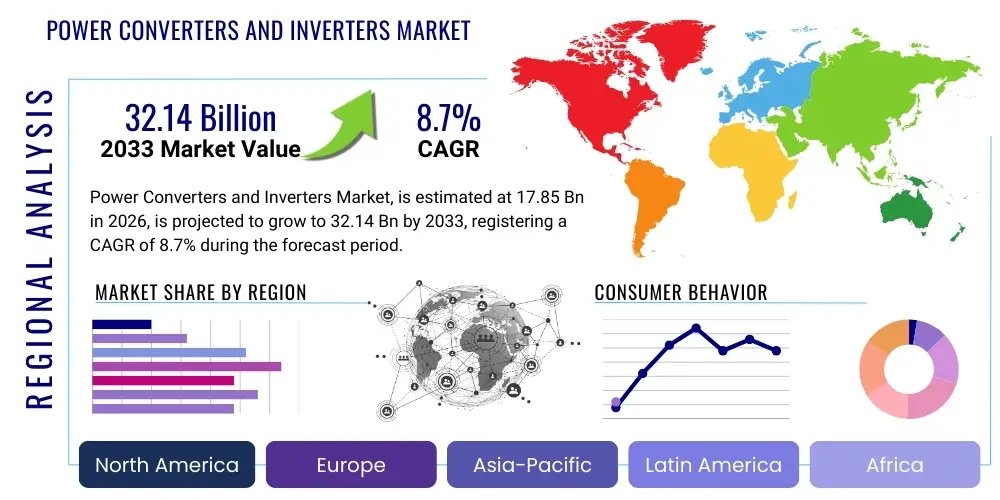

The Power Converters and Inverters Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2026 and 2033. The market is estimated at USD 17.85 billion in 2026 and is projected to reach USD 32.14 billion by the end of the forecast period in 2033. This robust expansion is primarily driven by the escalating demand for efficient energy management solutions across various industrial, commercial, and residential applications, coupled with rapid advancements in renewable energy integration and electric vehicle infrastructure.

The Power Converters and Inverters Market encompasses a wide range of electronic devices designed to convert electrical energy from one form to another, specifically alternating current (AC) to direct current (DC) and vice versa, or to modify voltage and frequency. These crucial components are fundamental to modern electrical systems, ensuring compatibility between power sources and loads, optimizing energy usage, and enhancing system reliability. Products range from small consumer electronics chargers to large-scale industrial motor drives and grid-tied solar inverters, each engineered for specific voltage, current, and power requirements. The core function involves sophisticated power electronics, semiconductor devices, and control algorithms to achieve precise and efficient energy conversion.

Major applications for power converters and inverters span numerous sectors, including renewable energy systems such as solar photovoltaic (PV) installations and wind turbines, where they convert variable DC or AC power into stable grid-compatible AC power. They are indispensable in electric vehicles (EVs) and charging infrastructure, facilitating battery charging and motor control. Industrial applications involve motor drives for manufacturing processes, uninterruptible power supplies (UPS) for critical systems, and power quality solutions. Residential use cases include backup power systems, home energy storage, and appliance operation, demonstrating the pervasive nature of these technologies across diverse environments.

The benefits derived from adopting advanced power converters and inverters are substantial. They enable improved energy efficiency, reducing operational costs and environmental impact by minimizing energy losses during conversion. Enhanced system reliability and stability are key advantages, particularly in sensitive applications and grid integration. Furthermore, these devices facilitate the seamless integration of distributed energy resources, contributing to grid modernization and resilience. Key driving factors propelling market growth include the global push for decarbonization and renewable energy adoption, significant investments in electric vehicle infrastructure, increasing industrial automation, and the rising demand for efficient power management solutions in data centers and telecommunications.

The Power Converters and Inverters Market is experiencing dynamic business trends characterized by intense innovation and strategic collaborations aimed at developing higher efficiency, smaller footprint, and more intelligent conversion solutions. Key players are focusing on integrating advanced semiconductor technologies like Silicon Carbide (SiC) and Gallium Nitride (GaN) to enhance performance and reduce losses, positioning these materials as pivotal for next-generation products. Additionally, there there is a growing emphasis on modular and scalable designs to meet diverse application requirements, from micro-inverters in solar installations to large-scale grid infrastructure projects. Market expansion is also being driven by mergers, acquisitions, and partnerships, as companies seek to consolidate market share, leverage complementary technologies, and expand their geographical presence in rapidly evolving energy markets.

Regional trends indicate significant growth opportunities across various geographies. Asia Pacific continues to dominate the market, propelled by massive investments in renewable energy infrastructure, rapid industrialization, and the burgeoning electric vehicle market, particularly in countries like China, India, and Japan. North America and Europe are witnessing substantial growth due to stringent government regulations promoting renewable energy adoption, strong incentives for EV deployment, and ongoing modernization of electrical grids. Latin America, the Middle East, and Africa are emerging markets, showing promising growth driven by increasing access to electricity, developing industrial bases, and rising awareness of sustainable energy solutions, albeit with unique challenges related to infrastructure development and investment.

Segment trends highlight distinct growth trajectories within the Power Converters and Inverters Market. The solar inverter segment remains a primary growth engine, continuously evolving with advancements in string inverters, central inverters, and micro-inverters to meet diverse solar PV deployment scales. The electric vehicle powertrain and charging infrastructure segment is experiencing exponential growth, fueled by global commitments to e-mobility and the expansion of charging networks. Industrial applications, particularly those involving variable frequency drives (VFDs) for motor control, are seeing steady demand driven by automation and energy efficiency imperatives. Furthermore, the market for energy storage inverters, crucial for grid stability and renewable energy integration, is expanding rapidly as battery storage solutions become more widespread and economically viable.

Users frequently inquire about how Artificial Intelligence (AI) will revolutionize the design, operation, and maintenance of power converters and inverters, seeking to understand the tangible benefits of AI integration in terms of efficiency, reliability, and predictive capabilities. Common concerns revolve around the complexity of AI implementation, data security in smart power systems, and the skill gap required to manage AI-driven solutions. Expectations are high regarding AI's potential to optimize energy conversion processes, enable intelligent grid management, and facilitate advanced fault detection and diagnostics, ultimately leading to more resilient and autonomous power systems. There is also significant interest in AI's role in predictive maintenance, extending the lifespan of critical equipment and reducing downtime across various applications.

The Power Converters and Inverters Market is significantly shaped by a confluence of driving factors, critical restraints, and emerging opportunities. Drivers primarily include the aggressive global push towards renewable energy adoption, particularly solar and wind power, which fundamentally rely on inverters for grid integration and efficient power delivery. The rapid electrification of transportation through electric vehicles (EVs) and the corresponding build-out of charging infrastructure also represent a monumental demand driver. Furthermore, increasing investments in smart grid technologies, industrial automation, and data centers necessitate highly efficient and reliable power conversion solutions. These factors collectively exert immense upward pressure on market growth, pushing innovation and product development.

However, the market also faces notable restraints. High initial capital costs associated with advanced power conversion systems, especially those incorporating cutting-edge semiconductor materials like SiC and GaN, can deter adoption in price-sensitive markets. The complexity of grid integration, particularly with distributed renewable energy sources, poses technical challenges and regulatory hurdles that can slow deployment. Additionally, the availability of skilled labor for installation, maintenance, and system management remains a constraint in many regions, impacting operational efficiency and scalability. Competition from traditional fossil fuel-based energy solutions, while diminishing, still presents a challenge in specific economic contexts.

Despite these challenges, vast opportunities are emerging, particularly from technological advancements and evolving regulatory landscapes. The continuous development of more efficient and compact power electronics, coupled with declining manufacturing costs, makes advanced converters more accessible. The burgeoning market for energy storage solutions, both at grid-scale and residential levels, presents a significant avenue for inverter manufacturers. Moreover, the increasing focus on power quality and grid resilience, driven by the expansion of distributed generation, opens doors for specialized inverter solutions that offer advanced grid support functions. The growing demand for specialized converters in applications like high-speed trains, marine vessels, and aerospace further diversifies market potential, creating a strong impact force for sustained growth and innovation.

The Power Converters and Inverters Market is comprehensively segmented across various dimensions including product type, power rating, application, and end-user, offering a granular view of market dynamics and opportunities. This detailed segmentation allows for a precise understanding of specific market niches and the technologies driving growth within each. The diversity in product offerings, from standard rectifiers and choppers to sophisticated grid-tie inverters and motor drives, caters to a broad spectrum of industrial, commercial, and residential requirements. Each segment is influenced by unique technological advancements, regulatory frameworks, and consumer preferences, contributing to the overall complexity and potential of the market landscape.

The value chain for the Power Converters and Inverters Market is a complex ecosystem, beginning with upstream raw material suppliers and extending through to end-users, highlighting the intricate interdependencies across various stages. Upstream activities involve the procurement of essential raw materials such as silicon wafers, copper, aluminum, and various rare earth elements crucial for manufacturing semiconductors, magnetic components, and circuit boards. This stage also includes the development and production of specialized components like insulated gate bipolar transistors (IGBTs), MOSFETs, diodes, capacitors, and inductors, which are the fundamental building blocks of any power conversion device. Innovation at this stage, particularly in semiconductor materials like SiC and GaN, significantly impacts the performance and cost of the final product.

Midstream activities primarily encompass the design, manufacturing, and assembly of the power converters and inverters themselves. This involves sophisticated engineering processes, including circuit design, software development for control algorithms, thermal management solutions, and packaging. Manufacturers integrate various components, perform rigorous testing for efficiency, reliability, and safety compliance, and package the final products according to specific application requirements. This stage is characterized by high capital expenditure in advanced manufacturing facilities, significant R&D investment, and a skilled workforce specializing in power electronics engineering. Quality control and adherence to international standards are paramount at this juncture to ensure product integrity and performance.

Downstream analysis focuses on the distribution channels, sales, installation, and after-sales services. Distribution channels are varied, including direct sales to large industrial clients and utility companies, as well as indirect channels through distributors, wholesalers, and system integrators for smaller-scale projects and consumer markets. Direct sales are often preferred for highly customized, high-power solutions requiring close technical collaboration, while indirect channels leverage broader reach and localized support. Post-sales services, including technical support, maintenance, warranty, and repair, are crucial for customer satisfaction and long-term product lifecycle management. The effectiveness of these channels and services directly impacts market penetration and brand reputation, ensuring that products reach their intended applications efficiently and are supported throughout their operational life.

Potential customers for power converters and inverters span a broad and diverse spectrum of industries and individual consumers, reflecting the foundational role these technologies play in modern electrical systems. A primary segment of end-users includes utility companies and independent power producers, who require high-power inverters for integrating renewable energy sources such as solar farms and wind power plants into national grids. These entities also utilize converters for grid stabilization, reactive power compensation, and high-voltage direct current (HVDC) transmission, making them crucial stakeholders in grid modernization and expansion efforts.

Another significant customer base comprises manufacturers across various industrial sectors. This includes companies involved in automation, robotics, machinery, and process control, which heavily rely on variable frequency drives (VFDs) and other industrial converters to precisely control motors, optimize energy consumption, and enhance operational efficiency. Data centers and telecommunication providers are also major consumers, deploying uninterruptible power supplies (UPS) and specialized DC-DC converters to ensure continuous and reliable power to critical IT infrastructure, safeguarding against power outages and voltage fluctuations.

Furthermore, the rapidly expanding electric vehicle (EV) market represents a massive segment of potential customers, encompassing EV manufacturers, charging station operators, and individual EV owners. Inverters are integral to EV powertrains for converting battery DC power to AC for motors, and in charging infrastructure for converting grid AC to DC for battery charging. Lastly, residential and commercial building owners, seeking energy independence, backup power solutions, or integration of rooftop solar panels and battery storage systems, constitute a growing segment. These diverse end-users drive continuous innovation and demand across the entire power converters and inverters market, underscoring its broad applicability and essential nature.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 17.85 Billion |

| Market Forecast in 2033 | USD 32.14 Billion |

| Growth Rate | 8.7% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ABB Ltd., Siemens AG, Schneider Electric SE, Eaton Corporation plc, Delta Electronics, Inc., SMA Solar Technology AG, SolarEdge Technologies, Inc., Huawei Technologies Co., Ltd., Enphase Energy, Inc., FIMER S.p.A., GoodWe Technologies Co., Ltd., Sungrow Power Supply Co., Ltd., Power-One (ABB subsidiary), Vertiv Holdings Co, TMEIC Corporation, Mitsubishi Electric Corporation, Danfoss A/S, Vacon (Danfoss subsidiary), Fuji Electric Co., Ltd., ON Semiconductor Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Power Converters and Inverters Market is characterized by a rapidly evolving technological landscape, driven by the incessant demand for higher efficiency, greater power density, and enhanced reliability. A pivotal trend is the widespread adoption of Wide Bandgap (WBG) semiconductors, particularly Silicon Carbide (SiC) and Gallium Nitride (GaN). These materials offer superior performance compared to traditional silicon-based devices, enabling operation at higher voltages, frequencies, and temperatures, which translates into smaller, lighter, and more efficient converter and inverter designs. SiC is increasingly favored in high-power applications such as electric vehicle chargers, solar inverters, and industrial motor drives, while GaN is gaining traction in lower to medium power consumer electronics, data centers, and telecommunications due to its ultra-fast switching speeds.

Beyond material science, advancements in control algorithms and digital signal processing (DSP) are transforming the functionality of power converters and inverters. Sophisticated control strategies, often incorporating artificial intelligence (AI) and machine learning (ML), enable real-time optimization of power conversion, advanced fault detection, and predictive maintenance capabilities. These intelligent controls contribute significantly to improving overall system efficiency, extending equipment lifespan, and enhancing grid stability. Furthermore, modular and scalable designs are becoming standard, allowing manufacturers to offer flexible solutions that can be easily adapted to various power ratings and application environments, facilitating easier installation and maintenance while reducing overall system complexity.

Another critical area of technological innovation involves advanced thermal management techniques. As power density increases, effectively dissipating heat becomes paramount to ensure the longevity and reliability of power electronic devices. Liquid cooling, advanced heatsink designs, and innovative packaging technologies are being developed to manage thermal stress efficiently. Moreover, the integration of communication interfaces and cybersecurity features is becoming standard, as inverters and converters are increasingly becoming interconnected components within smart grids and IoT ecosystems. This ensures secure data exchange, remote monitoring, and control, which are essential for the next generation of intelligent energy management systems.

Power converters transform electrical energy from one form to another (e.g., AC to DC, DC to DC, or AC to AC), while inverters specifically convert DC power to AC power. Their primary function is to ensure electrical compatibility, optimize energy transfer, and enable efficient operation of various electrical devices and systems, from renewable energy sources to electric vehicles.

Key market drivers include the global shift towards renewable energy sources like solar and wind power, the rapid expansion of electric vehicle adoption and associated charging infrastructure, increasing industrial automation requiring precise motor control, and the growing demand for energy-efficient power management solutions in data centers and telecommunications.

AI is significantly impacting the market by enabling advanced capabilities such as optimized energy conversion efficiency through dynamic control algorithms, predictive maintenance for reduced downtime, intelligent grid integration for enhanced stability, and more precise fault detection. These AI applications lead to more reliable, efficient, and autonomous power systems.

The Asia Pacific region currently holds the largest market share and is experiencing the fastest growth, driven by extensive investments in renewable energy and the burgeoning electric vehicle sector in countries like China and India. North America and Europe also show significant growth due to strong regulatory support and technological advancements.

Crucial emerging technologies include Wide Bandgap (WBG) semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN) for higher efficiency and power density, advanced control algorithms integrated with AI and machine learning for optimized performance, and innovative thermal management solutions to support increased power requirements and miniaturization.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.