ID : MRU_ 436620 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

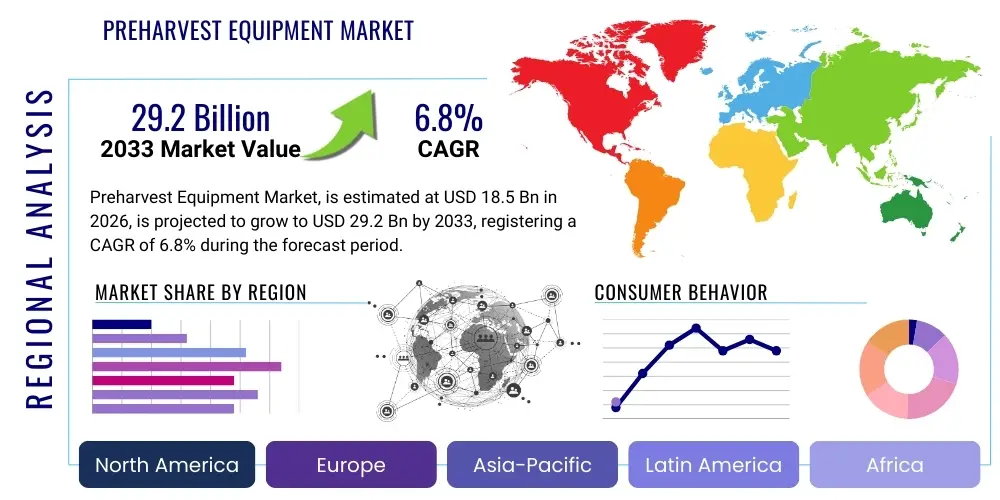

The Preharvest Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 18.5 Billion in 2026 and is projected to reach USD 29.2 Billion by the end of the forecast period in 2033.

The Preharvest Equipment Market encompasses a wide range of machinery and implements essential for preparing land, cultivating crops, and managing farm inputs prior to the actual harvest phase. This crucial market segment includes equipment such as tractors, planters, seeders, sprayers, tillage equipment, cultivators, irrigation systems, and specialized machinery designed for precision agriculture tasks like soil monitoring and variable rate application. The primary function of this machinery is to optimize crop growth, maximize yield potential, reduce manual labor requirements, and enhance overall farm efficiency through technologically advanced methods. Global demand is heavily influenced by factors such as increasing global population necessitating higher food production, diminishing arable land resources, and the widespread adoption of mechanization, particularly in developing economies.

Major applications of preharvest equipment span across diverse farming types, including conventional row cropping (corn, soybeans, wheat), specialty crops (fruits, vegetables), and large-scale industrial agriculture. Product descriptions emphasize durability, fuel efficiency, integration capabilities with GPS and telematics systems, and adherence to environmental standards regarding soil health and chemical usage. The benefits derived from deploying modern preharvest machinery are substantial, primarily focusing on labor cost reduction, enhanced planting accuracy leading to better crop stand, efficient pest and weed control via precise spraying, and improved soil structure through optimized tillage practices. These improvements directly contribute to higher farm profitability and sustainability.

Driving factors propelling the market include government subsidies supporting farm modernization, the increasing necessity for resource efficiency (water, fertilizer, seeds) due to rising input costs, and technological advancements such as the integration of sensor technology and artificial intelligence into standard equipment. Furthermore, the rising adoption of conservation agriculture practices, which require specialized minimum or no-till equipment, is opening new revenue streams for manufacturers. The market environment is competitive, characterized by continuous innovation focused on developing autonomous and semi-autonomous machinery capable of operating round-the-clock with minimal human intervention, thereby addressing persistent labor shortages in the agricultural sector globally.

The Preharvest Equipment Market is experiencing robust expansion driven by global trends toward precision farming and farm automation, reflecting a paradigm shift from traditional methods to data-driven agricultural management. Business trends indicate a strong focus on strategic mergers, acquisitions, and partnerships aimed at integrating complementary technologies, especially in software and sensor development, which are critical for enhancing the functionality of modern tractors and implements. Manufacturers are also prioritizing the development of electric and hybrid machinery to meet increasing regulatory demands for lower emissions and improved fuel efficiency. The market structure is moderately consolidated, with major global players dominating the high-horsepower equipment segment, while regional manufacturers thrive in specialized and localized machinery categories, providing tailored solutions for specific cropping needs and soil types.

Regionally, the market exhibits divergent growth profiles. Asia Pacific (APAC) is projected to be the fastest-growing region, fueled by government initiatives promoting mechanization, particularly in large agrarian economies like India and China, and supported by favorable subsidy programs designed to improve smallholder productivity. North America and Europe, representing mature markets, will see growth driven primarily by the replacement cycle of existing equipment and the high adoption rate of sophisticated, high-cost precision agriculture technologies, including autonomous guidance systems and advanced variable rate applicators. Latin America is also emerging as a significant growth area, powered by the expansion of large-scale commercial farming operations focused on exports of staple crops like soybeans and maize, creating high demand for powerful, durable equipment.

Segment trends highlight the dominance of the Tillage and Seeding/Planting equipment segments, which form the foundational requirements of crop production. However, the fastest growth is anticipated in the Crop Protection and Fertilization segment, largely due to the increasing adoption of high-tech sprayers and applicators equipped with drones, sensors, and AI-driven mapping systems to minimize environmental impact and reduce input waste. Furthermore, the market for rental and subscription-based equipment services is gaining traction, particularly among small and medium-sized farms that seek access to cutting-edge technology without the massive upfront capital investment, signaling a crucial shift in equipment procurement models.

User queries regarding the impact of Artificial Intelligence (AI) on the Preharvest Equipment Market overwhelmingly focus on automation, decision support systems, and yield optimization. Users frequently ask about the feasibility and cost-effectiveness of fully autonomous tractors, how AI integrates with existing farm machinery (retrofittability), and whether AI systems can genuinely improve crop input efficiency (e.g., fertilizer and pesticide reduction) beyond what current GPS systems offer. Key concerns revolve around data privacy, the requirement for robust connectivity (5G infrastructure in rural areas), and the skill gap required to maintain and operate these sophisticated, data-intensive systems. There is high expectation that AI will solve the persistent agricultural labor crisis by enabling 24/7 autonomous operation and providing predictive maintenance insights that minimize costly equipment downtime during critical planting windows.

The integration of AI into preharvest equipment is rapidly transitioning from theoretical concepts to commercial reality, fundamentally transforming how cultivation and crop management tasks are executed. AI algorithms process vast amounts of data collected by integrated sensors, satellite imagery, and weather station inputs to provide prescriptive insights, rather than just descriptive reports. For example, AI-powered systems deployed in precision planters can dynamically adjust seed depth and population based on real-time soil type analysis and historical yield maps, ensuring optimal conditions for emergence across heterogeneous fields. This predictive capability moves farming toward true site-specific management, minimizing waste and maximizing genetic potential.

Furthermore, AI significantly enhances the capabilities of crop protection equipment. Advanced computer vision and machine learning models enable smart sprayers to perform real-time identification of weeds versus crops, allowing for targeted, spot application of herbicides rather than blanket spraying. This reduction in chemical usage offers substantial economic benefits for farmers and meets growing consumer and regulatory pressure for sustainable farming practices. While adoption requires significant capital investment in highly instrumented machinery, the operational savings and yield improvements generated by AI-driven efficiency are establishing a compelling return on investment, solidifying AI as a pivotal disruptive force in the market.

The Preharvest Equipment Market is governed by a dynamic interplay of Drivers, Restraints, Opportunities (DRO), and overarching Impact Forces that dictate market direction and growth trajectory. Key drivers include the acute global shortage of agricultural labor, which necessitates increased reliance on mechanization and automation to maintain productivity levels. Furthermore, the imperative to increase global food production to feed a rapidly expanding population, coupled with limited expansion of arable land, forces farmers to seek technology that can drastically improve yield per unit area. Simultaneously, robust government support, particularly in emerging economies, through subsidies and financing schemes for farm machinery, provides a substantial impetus for market expansion and rapid adoption of new technology.

However, significant restraints temper this growth. The high initial capital cost associated with modern, technologically advanced preharvest equipment, especially precision farming machinery (e.g., autonomous tractors, advanced VRT sprayers), acts as a primary barrier for small and medium-sized farmers worldwide, who often face difficulties securing adequate financing. Additionally, the lack of sufficient technical expertise and training among the agricultural workforce in many regions hinders the effective utilization and maintenance of complex, sensor-heavy machinery. Fluctuations in commodity prices and uncertain weather patterns also contribute to volatile farm incomes, making large equipment investments risky and often delaying purchasing decisions.

The opportunities within this sector are centered on technological innovation and market penetration into underserved regions. The development of smaller, more affordable, and modular electric or battery-powered equipment specifically designed for smallholder farms presents a major opportunity for market democratization. Furthermore, the rise of the equipment-as-a-service (EaaS) model and rental services offers pathways for technology adoption without high capital outlay. The core impact forces influencing the market involve intense competitive pressure driving continuous innovation in fuel efficiency and autonomous capabilities, regulatory requirements mandating reduced chemical use and improved environmental stewardship (e.g., stricter emission standards for diesel engines), and the pervasive digital transformation that demands seamless data integration and connectivity across the farm operation.

The Preharvest Equipment Market is segmented based on several key parameters, including Equipment Type, Application, and Region, providing a detailed view of market dynamics across various product categories and end-user requirements. The market analysis heavily relies on segmenting by equipment type, as the technological complexity and price points vary drastically between foundational equipment like tractors and specialized implements like precision sprayers or high-speed planters. Understanding these segments helps manufacturers tailor their research and development efforts and allocate marketing resources effectively, focusing on areas with the highest projected growth and technological uptake.

Segmentation by application, such as primary tillage, secondary tillage, seeding/planting, and crop protection, directly reflects the chronological needs of the farming cycle. The adoption rates of advanced machinery are often highest in the seeding/planting and crop protection phases, where precision yields the most immediate and quantifiable return on investment. Furthermore, the analysis differentiates between various power outputs and specifications required for different crop types (row crops vs. specialty crops) and farm sizes, ensuring the market model accurately reflects the diverse requirements of the global agricultural landscape. This granular segmentation is crucial for strategic planning and forecasting future demand patterns based on changing farming practices globally.

The value chain for the Preharvest Equipment Market is complex, beginning with upstream activities focused on raw material procurement, particularly steel, specialized alloys, plastics, and advanced electronic components (sensors, GPS modules, software). Key upstream players include specialized metal producers and major component suppliers who provide engines, transmissions, hydraulic systems, and increasingly sophisticated embedded systems essential for smart equipment. Manufacturers focus heavily on optimizing their supply chain resilience due to the volatile pricing of raw commodities and the critical reliance on high-tech component suppliers, often necessitating long-term contracts and dual-sourcing strategies to mitigate risk and ensure uninterrupted production lines.

The midstream involves the core manufacturing process, where major Original Equipment Manufacturers (OEMs) design, assemble, and test the finished machinery. This stage includes extensive R&D dedicated to improving fuel efficiency, integrating digital technologies (telematics and AI), and enhancing ergonomic and safety features. Distribution channels are predominantly indirect, relying heavily on a global network of authorized dealers who handle sales, financing, spare parts management, and crucial after-sales service and maintenance. These dealers serve as the primary interface with the end-user, providing essential local knowledge and technical support that is vital for the successful deployment and operation of complex modern farm equipment.

Downstream analysis focuses on the end-users—large commercial farms, small and medium-sized farms, and agricultural service providers. Direct sales channels, while less common for general-purpose equipment, are sometimes utilized for specialized, high-value, custom-built machinery or through corporate agreements with mega-farms. However, the indirect channel remains dominant, providing financing options, leasing agreements, and ensuring that technical expertise is readily available locally. The profitability of the value chain is increasingly shifting towards the after-market services, including predictive maintenance, software upgrades, and precision farming consultation services, indicating a move towards a holistic technology-and-service model rather than a purely hardware-centric approach.

The primary customer base for the Preharvest Equipment Market is highly diversified, encompassing professional agricultural entities globally. The largest volume buyers are typically large commercial farms and corporate farming operations, particularly prevalent in North America, Europe, Australia, and parts of Latin America (e.g., Brazil and Argentina). These customers prioritize high-horsepower, durable, and fully automated equipment that can cover vast acreage efficiently, demanding the latest precision technology to maximize scale and minimize operational costs. Their purchasing decisions are heavily influenced by return on investment calculations, total cost of ownership, and the ability of the equipment to integrate seamlessly with existing farm management software platforms.

A significant, high-growth segment includes small and medium-sized (SMEs) farms, particularly dominant across Asia Pacific and Africa. While SMEs often have less capital, they represent a massive cumulative demand pool for low-to-medium horsepower, multi-functional, and affordable equipment. Manufacturers are increasingly developing specialized product lines tailored to the scale and financial constraints of these farmers, often focusing on mechanization that replaces manual labor without requiring full automation. The rising adoption of rental and pay-per-use models is specifically catering to this segment, allowing them to utilize advanced equipment when needed without the burden of outright ownership.

Furthermore, agricultural contractors and rental service providers constitute a rapidly expanding customer group. These entities purchase specialized or high-capacity machinery (such as advanced boom sprayers or specialized planters) which they then lease or contract out to multiple individual farmers. This model allows technology diffusion faster than direct sales to individual farmers. Government agencies and agricultural research institutions also represent niche customers, purchasing equipment for demonstration, research, and educational purposes to promote modern farming techniques across the agricultural community.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 29.2 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, Claas KGaA mbH, Yanmar Holdings Co. Ltd., Mahindra & Mahindra Ltd., TAFE - Tractors and Farm Equipment Limited, SDF Group, J C Bamford Excavators Ltd. (JCB), Bucher Industries AG, Alamo Group Inc., HORSCH Maschinen GmbH, Grimme Landmaschinenfabrik GmbH & Co. KG, Oxbo International Corporation, Fendt (A brand of AGCO), Krone Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Preharvest Equipment Market is rapidly evolving, moving far beyond basic mechanical functions to embrace sophisticated digital integration and automation. Global Positioning System (GPS) technology forms the foundational layer, enabling precise steering (autosteer), section control for sprayers, and parallel tracking, which collectively reduce overlap and minimize fuel and input consumption. This foundation supports Variable Rate Technology (VRT), which uses geo-referenced data maps to automatically adjust the application rates of seeds, fertilizers, or chemicals according to specific localized field conditions, maximizing efficiency and minimizing environmental waste.

The most transformative technology currently being integrated is the development of fully or semi-autonomous machinery. Manufacturers are leveraging advanced sensor fusion—combining LiDAR, radar, and high-resolution cameras—with sophisticated AI algorithms to allow tractors and implements to operate unsupervised. These systems are crucial for addressing labor shortages and enabling 24-hour fieldwork. Furthermore, connectivity standards, including advanced telematics and the increasing utilization of 5G networks in rural areas, are crucial for facilitating real-time data transfer to cloud-based farm management platforms, enabling remote diagnostics, predictive maintenance, and fleet optimization across large farming operations.

Sustainability-focused technologies are also paramount. This includes the development of electric and alternative fuel tractors, which offer lower emissions and reduced operating noise, aligning with stricter environmental regulations, particularly in Europe. Additionally, specialized implements designed for conservation agriculture, such as minimum tillage and no-till drills, are seeing strong growth. These technologies help preserve soil health, increase carbon sequestration, and improve water retention, directly addressing long-term sustainability goals and responding to growing global demand for environmentally conscious farming practices.

The Preharvest Equipment Market demonstrates significant regional variation in technology adoption, equipment size, and growth rates, influenced heavily by local farming structures, government policies, and climatic conditions.

North America (NA) is characterized by large-scale commercial farming, driving high demand for high-horsepower, fully automated, and connected equipment. The region is a pioneer in precision agriculture, showing the highest adoption rates for VRT, autosteer, and telematics systems. Market growth is sustained by the continuous replacement of aging fleets with more fuel-efficient and technologically advanced models. Investment is heavily concentrated in sophisticated planting and crop protection machinery that minimizes input costs and maximizes yield consistency across massive fields.

Europe represents a mature market focusing intensely on sustainability and regulatory compliance. Demand is strong for highly efficient, fuel-saving machinery that adheres to stringent European Union environmental standards, particularly those concerning pesticide reduction and soil health (e.g., minimum tillage requirements). The region shows strong demand for smaller, versatile equipment suitable for diverse farm sizes and highly sophisticated specialty crop machinery (vineyards, orchards). Innovation is frequently driven by the integration of electric and hybrid drive systems into mid-range tractors and implements.

Asia Pacific (APAC) is the fastest-growing region globally, propelled by increasing mechanization rates, particularly in China, India, and Southeast Asia. The market here is volume-driven, primarily demanding low-to-medium horsepower tractors and basic tillage equipment suitable for small land holdings. Government subsidies and initiatives promoting agricultural modernization are the major catalysts. While the overall technology adoption is lower than in NA or Europe, high-tech adoption is accelerating in large corporate farms in Australia and parts of China, creating dual market dynamics.

Latin America (LATAM) exhibits high demand for robust, high-durability machinery, essential for handling challenging soil conditions and supporting the massive scale of cash crop production (soybeans, corn, sugarcane) predominantly focused on export. Brazil and Argentina are the major hubs, requiring powerful tractors and specialized planters capable of high-speed, high-acreage performance. Market growth is closely tied to global commodity prices and agricultural expansion into new frontier areas.

Middle East and Africa (MEA) is characterized by strong demand for specialized irrigation equipment due to water scarcity and a growing need for mechanization to offset labor constraints. While still emerging, the market potential is significant, driven by government efforts to enhance food security and develop commercial agriculture projects, particularly in countries utilizing advanced water management technologies like Saudi Arabia and Egypt.

The primary driver is the accelerating global labor shortage in agriculture, coupled with the necessity to enhance food production efficiency and optimize input resources (seeds, fertilizer, water) through the adoption of advanced precision farming technologies and automation.

AI is employed for autonomous navigation of machinery, real-time decision-making systems (such as Variable Rate Application for inputs), predictive maintenance, and computer vision systems for highly precise tasks like targeted weed spraying (spot spraying).

North America and Europe currently lead in the adoption of sophisticated precision agriculture technologies, including autonomous solutions and high-horsepower connected machinery, driven by large commercial farm sizes and favorable regulatory environments supporting efficiency.

The market is broadly segmented by Equipment Type (Tractors, Tillage, Seeding/Planting, Spraying) and Application (Primary Tillage, Seeding, Fertilization). Tractors and Seeding/Planting equipment are historically the largest segments by value.

Small and medium-sized farmers primarily face challenges related to the high initial capital investment required for modern equipment and a lack of technical training necessary to operate and maintain sophisticated, data-driven precision farming systems.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.