ID : MRU_ 433730 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

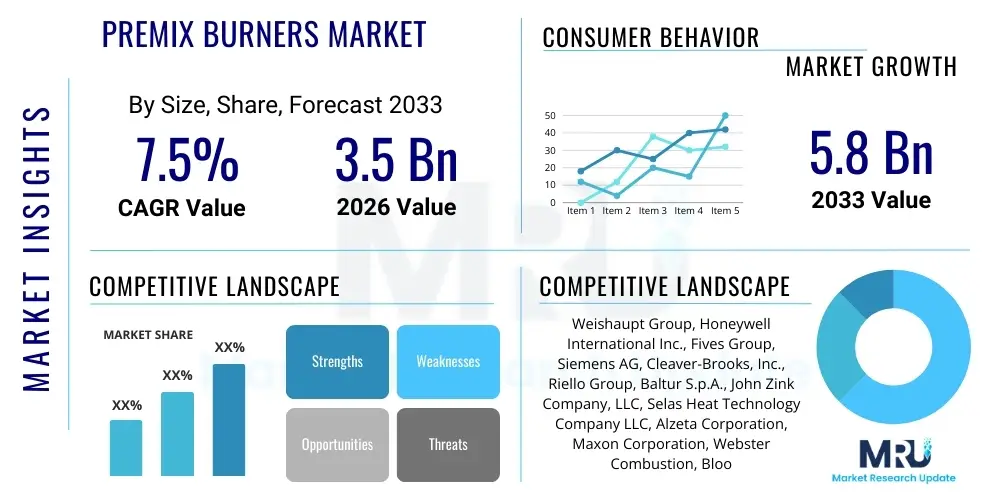

The Premix Burners Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at USD 3.5 Billion in 2026 and is projected to reach USD 5.8 Billion by the end of the forecast period in 2033.

The Premix Burners Market encompasses specialized combustion equipment designed to achieve high efficiency and significantly reduce pollutant emissions, primarily nitrogen oxides (NOx) and carbon monoxide (CO). Premix technology involves mixing the fuel (such as natural gas, propane, or hydrogen blends) and the oxidant (air) thoroughly before the mixture reaches the combustion zone, ensuring a lean, uniform flame structure. This approach results in lower peak flame temperatures compared to conventional diffusion burners, which is the primary mechanism for suppressing thermal NOx formation. The demand for these burners is intrinsically linked to stringent global environmental regulations mandating reductions in industrial and commercial boiler and heater emissions.

Premix burners are essential components across various sectors, including residential heating, commercial hot water generation, and heavy industrial processes such as chemical manufacturing, power generation, and oil and gas refining. Their application spans from small residential condensing boilers to large-scale industrial furnaces, driven by the imperative for energy conservation and sustainability goals. Key benefits of utilizing premix technology include enhanced fuel flexibility, extended equipment lifespan due to stable combustion, and superior turndown ratios, allowing boilers and heaters to operate efficiently across a wide range of loads. The inherent efficiency gains associated with minimizing excess air also contribute directly to reduced operational costs for end-users.

Driving factors for the adoption of premix burners include continuous technological innovation focused on achieving Ultra-Low NOx (ULN) compliance, growing consumer awareness regarding environmental impact, and massive investments in infrastructure development, particularly in Asia Pacific and North America. Furthermore, the global shift towards decarbonization and the increasing integration of renewable energy sources necessitate combustion equipment capable of handling hydrogen or bio-fuel blends, a capability where advanced premix designs excel. Government incentives and subsidies promoting energy-efficient appliances further accelerate market penetration, establishing premix burners as a standard for modern thermal process applications.

The Premix Burners Market is characterized by robust growth driven primarily by global environmental policies, technological advancements in low-emission combustion, and the imperative for industrial decarbonization. Business trends indicate a strong shift towards modular and smart burner systems integrated with advanced sensor technology and connectivity (IoT), allowing for real-time monitoring, predictive maintenance, and optimized fuel consumption. Key manufacturers are focusing on developing burners capable of efficiently utilizing non-fossil fuels, such as 100% hydrogen or hydrogen-natural gas blends, positioning the market for sustained expansion as global energy systems transition towards cleaner alternatives. Strategic mergers, acquisitions, and partnerships aimed at expanding regional manufacturing capabilities and specialized product portfolios, particularly in highly regulated Western markets, define the competitive landscape.

Regional dynamics highlight Asia Pacific (APAC) as the fastest-growing market, primarily fueled by rapid industrialization, urbanization, and increasing regulatory pressure, particularly in China and India, to mitigate severe air quality issues associated with traditional industrial combustion. North America and Europe, while mature markets, continue to lead in technological innovation and standardization, focusing heavily on retrofitting existing facilities with ultra-low NOx solutions to meet stringent localized environmental standards like those enforced by the EPA and EU directives. Market growth in emerging economies is further buoyed by governmental support for energy efficiency programs and the modernization of aging industrial infrastructure, creating substantial demand for high-efficiency premix systems in new construction and replacement markets.

Segmentation trends reveal significant traction in the Residential and Commercial Boilers segment, owing to mass adoption of high-efficiency condensing units that rely heavily on premix technology for optimal performance and emission control. By fuel type, natural gas remains dominant, but the Hydrogen Ready segment is witnessing exponential investment and growth anticipation, reflecting the industry's preparation for a hydrogen-centric future. Furthermore, the market for Forced Draft Burners within industrial applications maintains a strong presence due to their robust performance in high-load, heavy-duty environments, although atmospheric premix burners are gaining ground in smaller commercial applications due to their simplicity and lower initial cost. The shift towards digitalization is also creating a new segment focused on intelligent burner controls and software solutions.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Premix Burners Market center around three primary themes: how AI enhances combustion efficiency and emission control, the role of AI in predictive maintenance and operational uptime, and the feasibility of AI-driven optimization for managing complex fuel blends (like hydrogen/natural gas). Users seek assurance that AI can contribute meaningfully to ultra-low NOx goals by optimizing air-fuel ratios dynamically in real-time, adapting instantly to changes in ambient conditions or fuel composition. There is a strong expectation that AI will move the industry beyond static control systems to truly responsive, self-tuning combustion processes, thereby lowering operational expenditure and improving compliance margins for highly regulated industrial users.

AI's integration provides unprecedented opportunities for optimizing the performance envelope of premix burners. By analyzing vast datasets generated by sensors monitoring flame characteristics, flue gas composition, temperature profiles, and air flow dynamics, machine learning algorithms can identify non-linear relationships that traditional control loops often miss. This allows for proactive adjustments to the mixture ratios, ensuring continuous optimization for minimum emissions and maximum thermal efficiency, particularly crucial in fluctuating industrial load demands. Furthermore, AI models are trained on historical performance data to detect minute anomalies indicative of wear or impending failure, shifting maintenance strategies from reactive or calendar-based schedules to highly efficient predictive maintenance regimes.

The application of AI extends significantly into the realm of fuel flexibility, a critical future requirement for the market. As industrial users increasingly transition to diverse fuel sources—including biogas, syngas, or varying hydrogen concentrations—AI-driven control systems become indispensable. These systems can learn the optimal combustion parameters for complex, non-uniform fuel streams in real-time, ensuring stable, efficient, and low-emission operation without extensive manual recalibration. This capability is vital for accelerating the adoption of sustainable fuels, reducing the technical risk associated with blending operations, and ultimately driving the long-term viability of advanced premix burner technology in a decarbonized energy infrastructure.

The Premix Burners Market is primarily driven by rigorous global regulatory frameworks focused on reducing industrial emissions, particularly NOx and CO, compelling manufacturers and end-users to adopt Best Available Technology (BAT) standards. The increasing cost of energy and the corresponding emphasis on thermal efficiency across all sectors further act as a significant driver, as premix technology inherently offers superior efficiency compared to traditional diffusion combustion methods. Conversely, the market faces restraints such as the higher initial capital expenditure associated with sophisticated premix systems, requiring specialized installation and maintenance expertise, which can deter small and medium enterprises (SMEs). However, substantial opportunities exist in the rapid penetration of hydrogen-ready technologies and the extensive demand for retrofitting existing, inefficient boiler installations in mature markets to meet new emission caps.

Key drivers include the global mandate for sustainability and decarbonization initiatives, pushing heavy industries to transition away from high-polluting equipment. Governmental incentives, such as tax credits and rebates for installing energy-efficient and low-emission equipment (e.g., condensing boilers), accelerate residential and commercial adoption. Moreover, the inherent efficiency benefits of premix combustion, which typically result in lower fuel consumption, provide a strong economic justification for the upfront investment, delivering favorable long-term Total Cost of Ownership (TCO). The necessity for flexible combustion systems capable of handling variability in fuel quality and availability also drives the requirement for advanced premix designs.

Restraints center around the technical complexity and sensitivity of premix systems to installation errors or fluctuations in gas pressure, which can potentially lead to flashback or unstable operation if not meticulously managed. The lack of standardized codes for hydrogen combustion equipment across all regions also creates market uncertainty for manufacturers investing in next-generation fuel technologies. Nonetheless, opportunities are abundant in emerging applications such as waste heat recovery systems and integrated co-generation plants (CHP), where high turndown ratios and precise control are essential. Furthermore, the development of affordable, high-performance materials resistant to the corrosive effects of highly reactive fuels represents a substantial area for market growth and innovation.

The Premix Burners Market is intricately segmented based on core variables including burner type, fuel type, application, and capacity, each reflecting distinct market demands and technological maturity levels. Segmentation by burner type differentiates between forced draft and atmospheric burners, catering to industrial/high-capacity versus residential/low-capacity needs, respectively. The core segmentation drivers relate directly to achieving specific emission targets and thermal output requirements across diverse operational environments, ranging from highly regulated municipal power plants to domestic hot water systems.

Analysis of fuel type segmentation reveals the growing importance of flexibility, moving beyond conventional natural gas and LPG to include bio-fuels and, critically, hydrogen. The market is increasingly separating into 'traditional' and 'hydrogen-ready' categories, indicating a fundamental shift in product development cycles aimed at future-proofing industrial assets. Application segmentation highlights the dominance of the residential and commercial boiler sectors, followed closely by specific high-temperature industrial processes where precise heat control and emission compliance are paramount, such as drying processes in the food and beverage industry and heat treatment in metallurgy.

Capacity segmentation allows manufacturers to target specific market needs, distinguishing between burners for small residential units (typically under 1 MMBtu/hr) and ultra-large industrial systems (over 100 MMBtu/hr). This granular segmentation ensures that products meet both the regulatory requirements (which often vary by capacity class) and the economic expectations of the end-user. The convergence of hardware and digital controls has also led to a segmentation focus on 'Smart Burners' that incorporate IoT and AI, offering superior performance monitoring and integration capabilities compared to basic manual control systems.

The value chain for the Premix Burners Market begins with upstream activities involving the sourcing and processing of specialized raw materials, primarily high-temperature resistant metals (like stainless steel and specific alloys) and ceramic components crucial for the combustion head and mixing chamber. Suppliers of sophisticated electronic controls, sensors (e.g., flame sensors, oxygen sensors), and air handling equipment (fans, blowers) form the critical tier of component provision. Manufacturing activities involve precision engineering, casting, machining, and assembly, requiring high capital investment due to the stringent quality control necessary to ensure product safety, efficiency, and compliance with ultra-low emission standards.

Midstream activities focus heavily on distribution and system integration. Distribution channels are bifurcated into direct sales for large industrial clients (often involving customized engineering and installation support) and indirect sales through a network of specialized HVAC distributors, wholesale plumbing suppliers, and Original Equipment Manufacturers (OEMs). OEMs, particularly in the boiler and furnace market, constitute a massive indirect channel, embedding premix burner technology directly into their finished products. The selection of a distribution strategy is highly dependent on regional regulatory requirements and the complexity of the final installation, with highly technical industrial projects relying more on direct manufacturer involvement.

Downstream activities include installation, commissioning, maintenance, and aftermarket services. Certified technicians and engineering firms play a crucial role in ensuring optimal performance upon installation. The reliance on indirect channels for installation creates challenges in maintaining consistent quality control. Aftermarket services, including the supply of replacement parts (e.g., igniters, electrodes, control boards) and specialized maintenance contracts, represent a significant revenue stream. The transition to smart, IoT-enabled burners is increasingly driving the need for software updates, remote diagnostics, and data-driven optimization services, fundamentally altering the service component of the value chain.

Potential customers for premix burners span a wide array of sectors, unified by the common need for high thermal efficiency and strict adherence to environmental emission limits. The largest purchasing segment remains the Original Equipment Manufacturers (OEMs) of residential and commercial condensing boilers and water heaters, who procure burners in large volumes for integration into their flagship energy-efficient products, driven by consumer demand and regulatory compliance (e.g., Energy Star ratings). This segment is characterized by long-term supply contracts and stringent technical specifications regarding footprint and integration compatibility.

The industrial sector represents the second major customer base, encompassing heavy industries such as chemical processing, petroleum refining, metallurgy, and food and beverage manufacturing. These end-users typically require high-capacity, robust forced draft premix burners tailored for demanding operational cycles and critical process heating applications. Purchasing decisions in this domain are heavily influenced by the burner's turndown ratio, fuel flexibility (especially hydrogen readiness), and demonstrated long-term reliability in harsh environments, often involving highly customized engineering solutions rather than off-the-shelf products.

Additional significant customers include utility companies utilizing Combined Heat and Power (CHP) units or small-scale power generation facilities, where low NOx emissions are critical for grid stability and local compliance. Institutional buyers, such as hospitals, universities, and large commercial property managers, are also key consumers, frequently replacing older, inefficient boiler systems with modern premix technology to reduce utility costs and achieve internal sustainability goals. Furthermore, independent HVAC contractors and system integrators act as influential intermediaries, recommending and purchasing systems for residential and small commercial retrofit projects based on regional energy efficiency incentives.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 5.8 Billion |

| Growth Rate | CAGR 7.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Weishaupt Group, Honeywell International Inc., Fives Group, Siemens AG, Cleaver-Brooks, Inc., Riello Group, Baltur S.p.A., John Zink Company, LLC, Selas Heat Technology Company LLC, Alzeta Corporation, Maxon Corporation, Webster Combustion, Bloom Engineering, Ecoflam Bruciatori S.p.A., Hoval Group, Ecostar Burners, Esprit Energy, Combustion & Energy Systems, Oilon Group Oy, Santasalo. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Premix Burners Market is defined by continuous innovation aimed at pushing the boundaries of emission reduction and operational flexibility. A central focus is on achieving Ultra-Low NOx (ULN) levels, often below 9 ppm, requiring sophisticated burner head designs, such as matrix burners or surface stabilization techniques using porous media (e.g., ceramics or metal fiber). These advanced geometries ensure exceptionally lean fuel-air mixtures remain stable and combust efficiently without experiencing flame lift-off or flashback, which are common challenges in highly lean operations. Furthermore, the development of specialized materials that can withstand high thermal loads and corrosive environments is critical for extending the lifespan of these precision components.

A significant technological development is the implementation of advanced electronic control systems. Modern burners utilize sophisticated digital controllers (often integrating PID and specialized algorithms) to manage air dampers, modulating gas valves, and overall combustion sequencing. These controllers are crucial for maintaining optimal air-fuel ratios dynamically, adapting instantaneously to varying boiler loads or shifts in ambient air temperature and humidity. The integration of high-speed sensor technology, including UV flame scanners and advanced flue gas analyzers, provides the necessary feedback loop for these electronic systems, moving the industry beyond legacy mechanical linkage systems to purely digital, high-precision control.

The most transformative current trend is the focus on "Future-Proof" burner technology, specifically centered around hydrogen readiness. Manufacturers are actively redesigning mixing heads and flame holders to safely and efficiently combust pure hydrogen (H2) or high-percentage H2/Natural Gas (NG) blends. Due to hydrogen's unique combustion characteristics—high flame speed and low ignition energy—these new designs require specialized injection techniques and robust safety protocols to prevent premature ignition and manage the higher energy density. This technological shift is essential for supporting energy transition goals and maintaining market relevance in sectors committed to deep decarbonization by 2050.

The global Premix Burners market exhibits diverse growth patterns influenced by regional regulatory environments, industrial concentration, and energy policy.

Premix burners offer superior thermal efficiency and significantly lower emissions, particularly nitrogen oxides (NOx) and carbon monoxide (CO). By mixing fuel and air thoroughly before combustion, they achieve lower peak flame temperatures, inhibiting thermal NOx formation, which is essential for meeting modern ultra-low emission standards.

The global shift toward hydrogen as a clean fuel strongly accelerates demand for specially designed 'hydrogen-ready' premix burners. Premix technology is inherently better suited than diffusion technology to handle hydrogen's high flame speed and low ignition energy safely and efficiently, ensuring stability during the combustion of H2/NG blends.

Advanced premix burners, often utilizing ceramic fiber or porous media, are capable of achieving Ultra-Low NOx (ULN) emissions, routinely operating below 9 parts per million (ppm) and often reaching levels as low as 5 ppm or less, far surpassing the requirements of standard industrial compliance limits.

The highest growth is driven by the residential and commercial condensing boiler sector due to mandatory energy efficiency standards. Industrial process heating and power generation facilities, particularly those seeking to modernize aging equipment for strict environmental compliance and energy savings, also represent significant growth segments.

The primary technical challenges include managing the risk of flashback or flame instability when operating with very lean fuel mixtures. This requires highly precise control systems and advanced burner geometry to maintain optimal air-fuel ratios across various load conditions and ensure continuous safe and efficient operation.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.