ID : MRU_ 432355 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

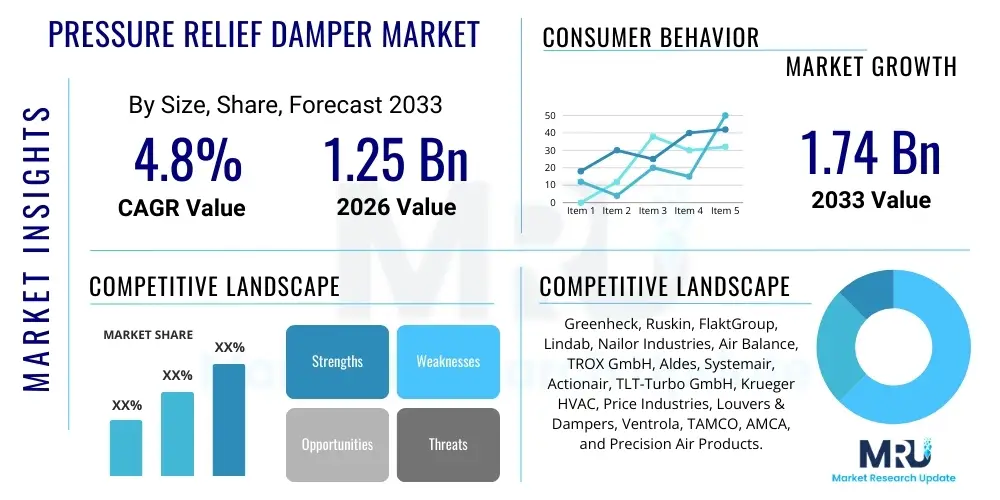

The Pressure Relief Damper Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 1.25 Billion in 2026 and is projected to reach USD 1.74 Billion by the end of the forecast period in 2033. This consistent expansion is primarily fueled by stringent safety regulations across industrial and commercial sectors, particularly in high-risk environments such as petrochemical plants, power generation facilities, and explosion-prone manufacturing sites where reliable pressure management is non-negotiable for operational safety and asset protection.

Pressure relief dampers are highly specialized mechanical devices engineered to mitigate potentially damaging pressure differentials within enclosed environments, ducts, or specific process chambers. These devices operate passively or actively to open automatically when internal pressure exceeds a pre-set threshold, venting the excess pressure to maintain structural integrity and prevent catastrophic equipment failure or injury. They are crucial components in HVAC systems for critical infrastructure, industrial dust collection systems, and specialized applications requiring explosion protection or rapid pressure equalization following deflagration events.

The core product description centers on robust construction, often utilizing galvanized steel, stainless steel, or advanced composite materials, designed to withstand extreme conditions including high temperatures and corrosive atmospheres. Major applications span petrochemical facilities, pharmaceutical clean rooms, nuclear power stations, data center cooling systems, and critical military installations, where maintaining precise environmental control and ensuring safety against unexpected pressure spikes are paramount. The design complexity varies significantly, ranging from simple gravity-operated dampers to sophisticated, electronically controlled motorized systems integrated into Building Management Systems (BMS).

The primary benefit of deploying pressure relief dampers lies in their ability to enhance operational safety, protect valuable assets from structural damage caused by over-pressurization or vacuum conditions, and ensure regulatory compliance with standards such as NFPA (National Fire Protection Association) and ATEX (Atmosphères Explosibles). Key driving factors for market growth include the global expansion of the oil and gas infrastructure, the rising number of data centers demanding precise internal pressure control for cooling efficiency, and increasingly stringent global industrial safety mandates requiring certified pressure mitigation equipment, thereby increasing the replacement and retrofit demand in aging industrial infrastructures worldwide.

The Pressure Relief Damper Market is characterized by steady, regulation-driven growth, emphasizing high reliability and certification standards. Business trends indicate a strong move toward customized, application-specific solutions, particularly those offering explosion resistance (blast dampers) and those made from corrosion-resistant materials like 316L stainless steel for marine and chemical processing environments. Manufacturers are focusing heavily on developing smart dampers equipped with integrated sensors and connectivity features, allowing real-time monitoring of pressure conditions and automated reporting, thereby enhancing predictive maintenance capabilities and overall system efficiency for end-users operating large, interconnected industrial facilities.

Regional trends highlight that North America and Europe currently dominate the market share due to mature industrial safety frameworks and rigorous adherence to standards like OSHA and relevant EU directives. However, the Asia Pacific (APAC) region is forecasted to exhibit the highest CAGR, propelled by massive infrastructure investments in manufacturing, power generation, and chemical sectors, particularly in developing economies such as China, India, and Southeast Asian nations. This growth is accelerating the adoption of international safety standards and driving significant new construction demand for certified pressure management systems, often bypassing older, less efficient technologies.

Segment trends reveal that the stainless steel material segment is experiencing premium growth due to its durability and suitability for harsh environments, while the petrochemical and power generation application segments remain the largest consumers. Furthermore, within the Type segmentation, counterbalanced and specialized explosion-proof dampers are witnessing increased adoption, reflecting the growing industrial requirement to manage high-energy events reliably. The market structure is moderately consolidated, with key players investing heavily in material science R&D and sophisticated aerodynamic testing to improve response time and pressure accuracy, making regulatory compliance and performance certification critical differentiators in competitive tender processes.

Common user questions regarding AI's influence on the Pressure Relief Damper Market often revolve around predictive maintenance, optimization of set points, and integration with wider smart building or industrial control systems. Users frequently ask if AI can predict when a damper might fail or if software can eliminate the need for manual calibration and testing. Key themes emerging from this analysis include the expectation that AI and Machine Learning (ML) will transform passive safety devices into intelligent, interconnected components. There is strong user interest in leveraging AI to interpret large datasets (e.g., historical pressure fluctuations, vibration readings, and ambient temperature changes) to autonomously recalibrate damper response thresholds, ensuring maximum operational efficiency while maintaining strict safety margins, particularly in dynamic industrial environments where operating parameters frequently shift.

The primary concern users express is ensuring the reliability and cyber-security of smart damper systems. While AI offers immense potential for optimization, industrial operators require assurance that the core safety function remains robust and failsafe, independent of software failures or cyber threats. Consequently, manufacturers are exploring hybrid control architectures where AI manages optimization and predictive failure analysis, but the physical actuation mechanism retains an independent, mechanical failsafe mode. This dual-layer approach addresses the critical balance between enhanced efficiency derived from AI-driven insights and the fundamental need for uncompromised mechanical reliability in safety-critical applications.

The integration of AI is expected to significantly impact the downstream services sector, shifting the maintenance model from routine inspection schedules to condition-based and predictive interventions. AI-enabled diagnostics will reduce unnecessary physical inspections, lower downtime, and extend the operational lifespan of the equipment. This evolution is vital for end-users in remote or difficult-to-access installations, such as offshore oil rigs or subterranean infrastructure, where manual maintenance is costly and hazardous. The focus is moving towards providing holistic pressure management solutions, where the physical damper is merely one component of an AI-optimized safety network, thereby increasing the value proposition of integrated safety system providers over commodity damper suppliers.

The Pressure Relief Damper Market is primarily driven by rigorous global industrial safety regulations and the necessity for asset protection, counterbalanced by high initial installation costs and long product lifecycles which slow replacement cycles. Opportunities exist in retrofitting older facilities with advanced, intelligent dampers, particularly in emerging economies where regulatory oversight is catching up to international standards. The market faces significant impact forces, including intense scrutiny over product certification and performance reliability, demanding robust supply chain management for specialized materials and aerodynamic expertise in design, influencing pricing power and competitive positioning among manufacturers.

A key driver is the escalating demand from high-energy sectors; the expansion of Liquefied Natural Gas (LNG) terminals and large-scale battery storage facilities necessitates specialized explosion protection and pressure venting solutions, driving innovation in heavy-duty damper technologies. However, a significant restraint is the technological complexity required for customized solutions, leading to extended lead times and high engineering costs for end-users. Furthermore, the reliance on specialized testing facilities for certification (e.g., blast testing) creates high barriers to entry for new market participants and concentrates market share among established, certified manufacturers, limiting broader competition.

The strategic opportunity lies in the convergence of safety technology with digitalization. Developing comprehensive safety platforms that integrate dampers, sensors, control panels, and cloud-based analytics offers substantial growth potential, moving beyond hardware sales into recurring software and service revenue streams. The major impact forces are shifting towards sustainability and material provenance; customers are increasingly demanding dampers made from recycled or lower-carbon footprint materials, pushing manufacturers to innovate in metallurgy and fabrication processes while maintaining stringent performance standards. Regulatory updates, especially concerning ATEX zones and seismic resilience in certain geographies, constantly reshape product requirements and drive mandated retrofits.

The Pressure Relief Damper market segmentation provides a granular view of product diversification required to meet the specific safety and operational demands of varied end-use industries. Segmentation is critically dependent on the operational mechanism, the materials used for construction to handle different fluid and corrosive environments, and the intended application which dictates the required pressure rating and response speed. Understanding these segments is vital for stakeholders to align their product portfolios with high-growth sectors, such as the increasing demand for specialized, corrosion-resistant dampers in offshore platforms and chemical processing plants, which require high-performance alloys like specialized stainless steels or composite materials.

The segmentation by type reflects the operational philosophy—whether the pressure relief function is purely mechanical (gravity or counterbalanced) or electronically integrated (motorized). Counterbalanced dampers, for instance, are highly sought after in applications requiring precise, repeatable relief settings, while specialized explosion-proof dampers, which are often heavily reinforced, cater exclusively to extremely hazardous industrial areas. Segmentation by application allows manufacturers to focus R&D on specific performance envelopes; for example, data center dampers prioritize precise low-pressure control to optimize air handling, whereas power generation dampers require high-temperature resistance and robustness against rapid pressure fluctuations.

This structured market view enables strategic planning, indicating that while traditional galvanized steel dampers remain cost-effective and dominate standard commercial HVAC, the premiumization of the market is occurring within the specialty material segments. This trend is driven by regulatory pressures and the need for longevity in hostile environments. The analysis of these segments confirms that market growth will be disproportionately driven by industrial applications demanding customized material composition and advanced operational features, moving the market away from standardized, general-purpose products toward highly engineered safety components.

The value chain for the Pressure Relief Damper market begins with the upstream procurement of raw materials, primarily specialized steel alloys (galvanized and stainless), aluminum, and increasingly, composite resins, which are selected based on the required corrosive resistance and structural rigidity. Fabrication involves precision cutting, welding, and advanced coating processes to ensure material integrity and compliance with stringent environmental specifications, particularly for ATEX-certified products. Manufacturing is a high-precision activity requiring specialized tooling and quality control to ensure repeatable pressure settings and rapid response times, which are essential for the core safety function of the product.

Downstream analysis focuses heavily on certified installation, system integration, and post-sales servicing. Because these dampers are safety-critical components, the installation process often requires specialized engineering contractors familiar with HVAC specifications, fire codes, and explosion protection mandates. Distribution channels are generally specialized, relying heavily on professional engineering firms, system integrators (who incorporate dampers into larger HVAC or blast mitigation systems), and authorized distributors who maintain inventories of common sizes while facilitating custom orders. Direct sales are common for highly specialized projects, particularly those involving nuclear or heavy petrochemical applications, where direct consultation between the manufacturer and the project owner is required.

The efficiency of the distribution channel is highly reliant on technical support and certification validation. Indirect channels, such as large industrial supply houses, handle standard, high-volume products, whereas direct channels manage customized, high-margin, engineered-to-order solutions. Value creation is maximized at the integration stage, where the damper’s performance is optimized within the context of the entire safety system. Consequently, manufacturers that offer comprehensive engineering support, training, and certification documentation throughout the product lifecycle gain a significant competitive advantage over those that merely supply hardware, reinforcing the strategic importance of expert distribution partners capable of providing integrated safety solutions.

The primary customers for pressure relief dampers are entities operating critical infrastructure or industrial processes where unexpected pressure surges or rapid evacuations are potential hazards. These end-users typically prioritize reliability, compliance with international safety standards, and long-term durability over immediate cost savings. Key procurement decisions are made by facility engineers, safety managers, procurement specialists within large EPC (Engineering, Procurement, and Construction) firms, and specialized system integrators tasked with designing complex ventilation and safety systems for new facilities or major retrofits.

A significant segment of buyers comprises operators in the oil and gas industry, including refineries, offshore platforms, and LNG processing plants, where the risk of deflagration or catastrophic failure due to uncontrolled pressure is exceptionally high. Similarly, utility providers, particularly those managing fossil fuel or nuclear power generation facilities, constitute a major customer base due to the need for strict containment and pressure control within steam cycles and auxiliary systems. These customers require highly certified, specialized dampers resistant to corrosion, high temperatures, and seismic activity, ensuring uninterrupted operation and compliance with critical safety requirements.

Furthermore, the rapidly expanding data center industry represents a high-growth customer segment. Data centers require precision pressure relief dampers to manage the differential pressure between hot and cold aisles and to protect sensitive electronics from damage caused by rapid pressure changes during fire suppression system activation (e.g., clean agent discharge). This customer group values precision, energy efficiency, integration with BMS, and low maintenance requirements, driving demand for motorized, smart damper solutions that can be remotely monitored and calibrated to maintain optimal operational airflow conditions within tightly controlled computing environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 1.74 Billion |

| Growth Rate | CAGR 4.8% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Greenheck, Ruskin, FlaktGroup, Lindab, Nailor Industries, Air Balance, TROX GmbH, Aldes, Systemair, Actionair, TLT-Turbo GmbH, Krueger HVAC, Price Industries, Louvers & Dampers, Ventrola, TAMCO, AMCA, and Precision Air Products. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Pressure Relief Damper market is primarily driven by material science advancements and the integration of precision electromechanical control systems. Modern dampers utilize high-performance alloys and specialized coatings, such as epoxy or vinyl esters, to resist corrosion and extreme temperatures, thereby extending the operational lifespan in challenging environments like chemical vapor zones or marine settings. Key technological focus areas include improving the aerodynamic profiles of damper blades and frames to minimize pressure drop during normal operation while ensuring a swift, controlled response during relief activation, demanding advanced Computational Fluid Dynamics (CFD) modeling during the design phase.

A significant technological shift is the move towards 'smart' or 'intelligent' dampers. This involves embedding microprocessors, high-precision pressure transducers, and communication modules (e.g., Modbus, BACnet) directly into the damper assembly. These integrated systems allow for continuous self-monitoring, remote diagnostics, and instantaneous pressure fluctuation data logging, which is crucial for compliance reporting and performance verification. Motorized pressure relief dampers are utilizing advanced stepper motors and actuators to allow dynamic, highly accurate adjustment of the relief pressure set point, moving away from fixed mechanical settings and catering to systems requiring variable operational conditions.

Furthermore, technology related to certification and testing remains paramount. Manufacturers employ advanced testing methodologies, including full-scale blast testing facilities and wind tunnel simulations, to validate performance metrics under extreme conditions, ensuring adherence to standards set by organizations like AMCA (Air Movement and Control Association) and specific explosion standards like ATEX or IECEx. The adoption of additive manufacturing techniques (3D printing) is also being explored for producing complex components, particularly in the actuator mechanisms and custom sealing elements, potentially reducing manufacturing complexity and improving response reliability by reducing component tolerance variability.

The primary function of a pressure relief damper is to automatically open and vent excess pressure from an enclosed space or duct system when internal pressure exceeds a pre-determined, safe limit. This prevents structural damage, equipment failure, and potential catastrophic safety hazards, making them critical safety components in environments like petrochemical processing, pharmaceutical clean rooms, and explosion-prone industrial zones, ensuring regulatory compliance and asset protection through reliable, rapid pressure equalization.

Certification standards critically influence market participation and product specification. ATEX (for Europe) mandates safety requirements for equipment operating in explosive atmospheres, requiring specialized explosion-proof dampers. AMCA International provides standardized testing and certification for performance metrics such as air leakage, pressure drop, and structural integrity. Adherence to these standards is mandatory for market entry into critical sectors, validating a damper's performance claims and ensuring installer confidence in the safety reliability of the product.

The Stainless Steel (specifically 316L grade) and specialized Composite Materials segment is driving premium growth. Stainless steel offers superior corrosion resistance, essential for chemical plants, marine, and offshore applications, ensuring longevity in harsh environments. Composite materials are gaining traction in specialized applications requiring lightweight, non-conductive, or highly customizable structures. These material choices reflect the increasing industrial demand for durable, low-maintenance safety solutions capable of withstanding extreme operational parameters.

Digitalization transforms passive dampers into smart safety assets. Modern motorized and counterbalanced dampers integrate sensors, actuators, and communication protocols (IIoT connectivity) to provide real-time operational data, remote monitoring, and dynamic pressure set-point adjustment. This integration facilitates predictive maintenance, improves energy efficiency by optimizing airflow, and ensures continuous performance verification, allowing sophisticated integration into overarching Building Management Systems (BMS) for enhanced industrial control and compliance reporting.

Gravity dampers rely purely on internal pressure overcoming gravity to open, offering simple, cost-effective relief. Counterbalanced dampers utilize weights to allow fine-tuning of the precise relief pressure set point, providing higher accuracy and repeatability, crucial for regulated environments. Specialized explosion-proof (blast) dampers are heavily reinforced to withstand and mitigate high-intensity shockwaves following a deflagration event, designed for extreme hazard protection rather than standard HVAC pressure equalization, demanding robust construction and rigorous certification.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.