ID : MRU_ 433485 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

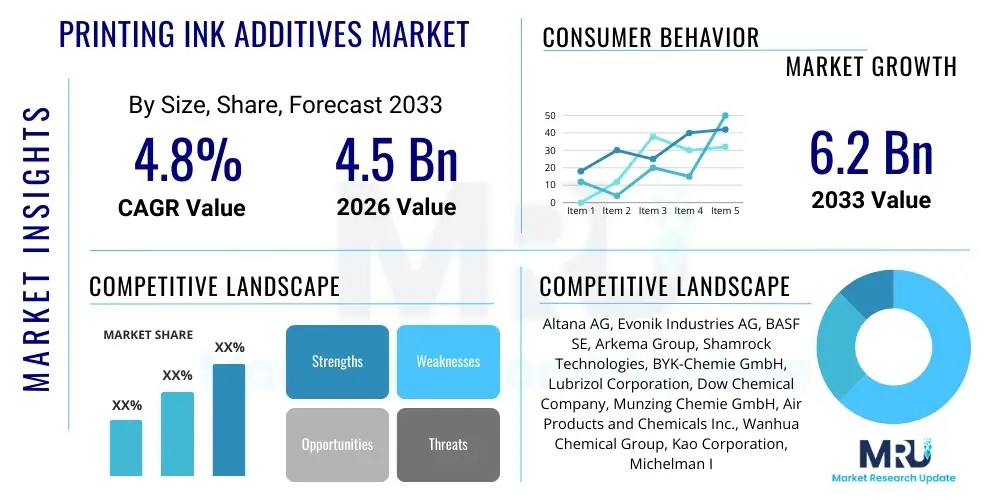

The Printing Ink Additives Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 6.2 Billion by the end of the forecast period in 2033.

Printing ink additives constitute a critical category of specialty chemicals essential for optimizing the performance, durability, and aesthetic qualities of various printing formulations, ensuring successful application across diverse substrates and technological platforms. These chemical compounds, which include rheology modifiers, waxes, defoamers, dispersants, surfactants, and resins, are incorporated in minimal quantities but exert significant control over the ink’s functional characteristics, such as viscosity, flow behavior, pigment stability, drying speed, and resistance to environmental factors like abrasion, heat, and chemical solvents. The necessity for these specialized components stems from the evolving demands of modern printing processes, particularly the rapid shift toward high-speed production, complex packaging geometries, and stringent quality control standards, making additives indispensable for meeting both regulatory mandates and consumer expectations for high-fidelity graphics and durable print finishes.

The major applications of printing ink additives span across the expansive packaging industry, including flexible packaging, corrugated boxes, and labels, where functional properties like migration resistance and low odor are paramount, especially for food contact materials. Beyond packaging, these additives are heavily utilized in commercial printing, publication printing (magazines, newspapers), and increasingly in the burgeoning digital printing sector, specifically in inkjet and toner formulations where particle stability and jetting reliability are non-negotiable performance metrics. The continuous innovation within the ink formulation domain is centered on developing additives that enable faster press speeds without compromising print quality, while simultaneously enhancing the final product’s resistance features, such as gloss retention, scratch resistance, and adhesion to challenging substrates like treated plastics and metallic foils.

Key driving factors propelling the growth of this market include the global expansion of the packaging industry, driven by e-commerce proliferation and urbanization, which necessitates vast quantities of printed materials with superior protective and aesthetic coatings. Furthermore, the growing consumer and regulatory preference for environmentally sustainable solutions is accelerating the adoption of water-based and UV-cured ink systems, creating high demand for specialized additives—such as bio-based resins and advanced rheology modifiers—that facilitate optimal performance in these low-VOC formulations. The benefits derived from using specialized additives are manifold, encompassing enhanced productivity through reduced downtime, improved color strength and consistency, and extended durability of the printed image, ultimately contributing to the cost-effectiveness and competitive advantage of ink producers and printing houses worldwide.

The Printing Ink Additives Market is characterized by robust growth driven primarily by the escalating demand from the flexible packaging sector and the pervasive shift towards sustainable printing technologies, particularly in the Asia Pacific region. Business trends indicate a strong focus on research and development aimed at replacing traditional solvent-based additives with high-performance, low-migration alternatives suitable for food and pharmaceutical packaging, leading to increased investment in UV/EB curing agents and advanced dispersion technology. Regulatory pressures, especially concerning Volatile Organic Compounds (VOCs) and material safety in Europe and North America, are mandating rapid innovation, forcing manufacturers to reformulate existing products and concentrate on specialized polymer chemistry that offers equivalent or superior functional properties while adhering to strict environmental compliance standards.

Regionally, Asia Pacific (APAC) currently dominates the market share due to its status as a global manufacturing hub for printing and packaging, coupled with massive domestic demand across China, India, and Southeast Asian economies. This region exhibits high growth potential, fueled by the rapid expansion of the middle class and subsequent increased consumer spending on packaged goods. Conversely, mature markets like North America and Europe, while exhibiting slower volume growth, lead in technology adoption, particularly in the premium segments focused on digital printing, high-security inks, and functional coatings, thus driving innovation in specialized high-value additives designed for complex digital and hybrid printing presses.

Segment trends reveal that the resins and binders segment commands the largest revenue share, given their fundamental role in establishing ink structure, adhesion, and gloss characteristics, with acrylic and polyurethane resins seeing significant uptake due to their versatility in water-based and UV formulations. Technology-wise, the flexographic printing application segment remains dominant, underpinned by its versatility and efficiency in large-volume packaging printing; however, the digital printing segment (especially inkjet) is projected to record the highest Compound Annual Growth Rate (CAGR) over the forecast period, necessitating specialized, ultra-fine particle additives and dispersing agents to maintain optimal fluid dynamics and prevent nozzle clogging in high-resolution inkjet heads. The increasing fragmentation in end-user demand requires additive manufacturers to offer highly customized solutions tailored to specific substrate and curing methods, shifting the market towards specialty chemicals over commodity grades.

Common user questions regarding AI's impact on the Printing Ink Additives Market typically revolve around predictive formulation stability, optimization of complex chemical synthesis routes, and automation of quality control during additive production and ink manufacturing. Users frequently inquire about AI's capability to predict the shelf life and long-term performance characteristics of novel bio-based additives, which often exhibit less predictable behavior than traditional petrochemical derivatives. Furthermore, there is significant interest in using machine learning algorithms to analyze vast datasets of raw material characteristics and finished ink properties, thereby dramatically reducing the required time and resources for the iterative R&D cycles needed to achieve optimal rheology, color dispersion, and curing kinetics for new ink systems. AI is viewed as the key enabling technology for personalized chemical synthesis, allowing ink producers to quickly adapt additive packages to short-run, highly customized printing jobs or rapidly respond to fluctuations in raw material quality and availability, enhancing supply chain resilience and accelerating market responsiveness.

The dynamics of the Printing Ink Additives Market are profoundly shaped by a confluence of powerful drivers, significant restraints, and emerging strategic opportunities, collectively defining the competitive landscape and future trajectory of the industry. Drivers primarily stem from the unrelenting expansion of the global packaging sector, particularly flexible packaging, which relies heavily on high-performance inks demanding specialized additives for adhesion, barrier properties, and superior aesthetic appeal. The continued technological transition toward eco-friendly printing methods, specifically water-based and energy-curable (UV/EB) systems, acts as a pivotal force, creating an immediate and substantial requirement for new generations of additives designed specifically to function optimally in these low-VOC environments, further accelerating the obsolescence of solvent-heavy formulations.

Restraints exerting pressure on market growth include the increasingly rigorous global regulatory environment, exemplified by strict mandates like the European Union’s REACH regulations and various food contact material directives that severely limit the use of certain chemicals, forcing costly and time-consuming reformulation efforts. Furthermore, the volatility of key raw material prices, particularly those derived from petrochemical feedstocks (e.g., monomers for acrylic and polyurethane resins), presents a consistent operational challenge, impacting production costs and profit margins across the value chain. These restraints necessitate sophisticated risk management strategies and a strategic shift towards securing supply chains based on renewable or less volatile source materials to maintain business continuity.

Opportunities for expansion are primarily concentrated in the realm of advanced material science and sustainable chemistry, specifically the development of highly specialized, high-margin functional additives such as anti-microbial agents, smart pigments, and bio-degradable components designed for compostable packaging substrates. The rapid adoption of high-speed digital printing across industrial applications, coupled with the need for specialized inkjet formulations that ensure long printhead life and exceptional print fidelity, opens lucrative avenues for advanced dispersants and surface tension modifiers. The combined impact forces—driven by regulatory mandates and technological pull—compel manufacturers to prioritize sustainable innovation, dictating that only those companies capable of investing in green chemistry R&D and securing specialized material patents will maintain long-term competitive advantages and capture emerging market segments focused on circular economy principles.

The Printing Ink Additives Market is extensively segmented across multiple dimensions, including additive type, technology, application method, and end-use application, each reflecting unique performance requirements and market dynamics. This detailed segmentation allows manufacturers to target specific niche markets and align product development with evolving technological needs, such as the increasing demand for additives optimized for single-pass digital inkjet printing or ultra-high-speed rotogravure operations. The differentiation by additive type, for instance, highlights the complexity of ink formulation, where components like waxes primarily offer slip and abrasion resistance, while specialized rheology modifiers manage the flow and leveling behavior crucial for defect-free application on challenging surfaces.

The value chain for the Printing Ink Additives Market is complex, beginning with the upstream sourcing of diverse raw materials, moving through specialized chemical synthesis, and culminating in distribution to global ink manufacturers. Upstream analysis highlights reliance on petrochemical derivatives (for synthetic resins, polymers, and solvents) and natural sources (such as vegetable oils, natural waxes, and cellulosic materials). Volatility in crude oil markets and increasing sustainability mandates place significant pressure on raw material procurement, compelling additive producers to diversify their sourcing and invest in bio-based feedstocks. The manufacturing stage involves intricate chemical processing, including polymerization, emulsification, and functionalization, requiring high capital investment in specialized reactor technology and rigorous quality control to ensure batch consistency and regulatory compliance, particularly concerning heavy metals and extractables.

Midstream activities involve the core business of specialized chemical companies that formulate and produce the additives. These producers typically maintain extensive R&D facilities to tailor additives that solve specific performance challenges encountered by ink manufacturers, such as enhancing pigment dispersion stability or optimizing surface energy for high-speed coating. The relationship between the additive supplier and the ink manufacturer is often collaborative, involving technical consultation to integrate the additives effectively into proprietary ink formulations, making technical service a key differentiating factor in competitive positioning. This collaboration is particularly crucial in the high-growth water-based and UV-cured segments where formulation windows are tight and performance requirements are stringent.

Downstream analysis focuses on the distribution channels and the final end-users. Distribution is managed through both direct sales and specialized chemical distributors. Major, large-volume additive suppliers often employ a direct sales model to large multinational ink companies (e.g., Sun Chemical, Flint Group), ensuring optimized supply logistics and deep technical support. Conversely, smaller ink manufacturers and regional players rely heavily on indirect distribution channels, where specialized chemical distributors manage inventory, provide localized delivery, and often offer pre-mixing or repackaging services. The final buyers are primarily ink manufacturers, followed by converters and packaging companies that may purchase pre-mixed coatings or specialty lacquers containing these additives, reinforcing the critical role of the additive manufacturer in the performance of the final printed product.

The primary customer base for printing ink additives consists of global and regional ink manufacturing companies that rely on these specialized chemical components to formulate high-performance inks tailored for specific printing technologies and end-use applications. These customers, ranging from large multinational corporations dominating the packaging and publication sectors to niche players specializing in digital or security inks, demand additives that offer high purity, functional consistency, and full regulatory documentation to ensure their final products meet international safety standards, especially concerning food contact materials (FCM) and low volatile organic compound (VOC) emissions. The purchasing decisions of these manufacturers are heavily influenced by the technical performance metrics, such as the additive’s ability to improve pigment wetting, control foam formation during high-speed mixing, and impart essential properties like scuff resistance and high gloss to the printed surface.

A secondary, yet rapidly growing, customer segment includes specialized coating manufacturers and compounders who produce varnishes, primers, and specialized lacquers used by converters and packaging houses to enhance or modify the substrate surface before or after printing. These customers often require functional additives, such as matting agents, anti-slip compounds, and UV stabilizers, which are incorporated into clear or functional coatings rather than the color ink itself. The demand from this segment is driven by the trend towards multilayer packaging and specialized functional printing, where surface enhancement is paramount for product integrity and consumer appeal, necessitating close technical collaboration with additive suppliers to achieve bespoke coating performance specifications for materials like flexible films, specialty papers, and metallized substrates.

Furthermore, major converters and large, integrated packaging companies that operate their own in-house ink mixing or blending facilities represent a crucial segment of direct buyers for high-volume additives. These organizations seek to achieve precise control over their ink quality and cost structures, often procuring commodity additives directly to streamline their production workflows and customize ink properties for proprietary printing presses. The growing interest in sustainable substrates and compostable packaging is also creating a new wave of demand from environmentally conscious end-users who require certified bio-degradable or non-toxic additives, driving procurement focused on compliance with certifications such as the European EN 13432 standard for industrial composting, thereby broadening the customer scope beyond traditional ink houses.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 6.2 Billion |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Altana AG, Evonik Industries AG, BASF SE, Arkema Group, Shamrock Technologies, BYK-Chemie GmbH, Lubrizol Corporation, Dow Chemical Company, Munzing Chemie GmbH, Air Products and Chemicals Inc., Wanhua Chemical Group, Kao Corporation, Michelman Inc., Lawter, Toyo Ink SC Holdings Co., Ltd., DIC Corporation, Huber Group, Solvay SA, Momentive Performance Materials Inc., Lonza Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The contemporary technology landscape of the Printing Ink Additives Market is heavily influenced by the necessity for sustainability, high-speed performance, and multi-functional characteristics. One of the most significant technological shifts involves the widespread adoption of energy-curing chemistries, specifically UV (Ultraviolet) and EB (Electron Beam) curable systems, which require highly specialized photoinitiators, oligomers, and reactive diluents that serve as additives, enabling instantaneous drying and high resistance properties without relying on solvent evaporation. This shift necessitates constant innovation in the synthesis of oligomers and monomers that offer low viscosity, rapid cure speed, and excellent adhesion to non-porous substrates, representing a departure from traditional thermo-curing or oxidative drying ink additive requirements, and fundamentally changing the chemical profile of the industry.

Another dominant technological trend focuses on green chemistry and the development of high-performance water-based formulations, requiring advancements in specialized dispersing agents and polymeric thickeners. Water-based inks require additives capable of stabilizing pigments in an aqueous environment, controlling rheology over a wide temperature range, and ensuring rapid drying without impacting substrate integrity. This involves utilizing advanced emulsification techniques and designing polymer architectures (e.g., highly branched or block copolymers) that function effectively as binders and dispersants while maintaining low VOC content. Furthermore, the incorporation of nanotechnology is becoming increasingly prevalent, where nano-sized silica or specialized polymeric particles are used as additives to significantly enhance scratch resistance, abrasion durability, and barrier properties in protective coatings and ink layers without sacrificing transparency or flexibility.

Finally, the rapid expansion of digital printing, particularly industrial inkjet, drives intensive technological focus on ultra-fine chemistry and high-purity additives to ensure reliable jetting and long printhead lifespan. This segment requires advanced surfactants and rheology modifiers that precisely control the surface tension and fluid dynamics of the ink droplet for accurate deposition at micro-level resolutions. The requirement for thermal stability and anti-settling characteristics in inkjet formulations, which often contain complex mixtures of pigments and solvents, mandates the use of proprietary polymeric dispersants and specialty waxes designed to maintain colloidal stability under high-shear stress and heat exposure within the printhead system, positioning chemical precision and particle management as paramount technological priorities.

The primary functional benefits of printing ink additives in modern packaging center on enhancing durability, print quality, and food safety compliance. Key functions include improving scratch and abrasion resistance (via waxes and slip agents), controlling viscosity for high-speed printing (rheology modifiers), preventing pigment settling (dispersants), and ensuring rapid, complete curing in UV systems (photoinitiators). Crucially, specialty additives ensure low migration and low odor, which is mandatory for compliance in food and pharmaceutical contact materials, thereby safeguarding consumer health and product integrity.

Environmental regulations, particularly those restricting Volatile Organic Compounds (VOCs) in mature markets like Europe and North America, are fundamentally reshaping additive demand by driving a critical shift away from solvent-based formulations toward water-based and energy-curable (UV/EB) ink systems. This mandate increases the demand for high-performance specialty additives—such as water-reducible resins, non-toxic dispersing agents, and reactive monomers—that can deliver equivalent or superior performance characteristics while maintaining minimal or zero VOC content, ensuring sustainable compliance and reduced environmental impact.

The segment related to digital printing technology, particularly high-definition industrial inkjet, is exhibiting the fastest growth rate in the Printing Ink Additives Market. This accelerated growth is attributed to the increasing demand for customized packaging, variable data printing, and shorter print runs. This requires a specific class of high-purity, ultra-stable dispersing agents, and advanced rheology modifiers designed to prevent nozzle clogging, maintain colloidal stability, and ensure precise jetting performance in highly sensitive inkjet printheads, differentiating them significantly from traditional flexographic requirements.

Nanotechnology plays a crucial role in future additive development by enabling the creation of materials with enhanced functional properties at the microscopic level. Nano-additives, such as nano-silica and specialized polymeric nanoparticles, are used to significantly increase the abrasion resistance, hardness, and barrier properties of printed inks and coatings without affecting transparency or flexibility. This technology is vital for producing high-durability inks for protective packaging and electronic applications, allowing for multi-functionality that is unattainable with conventional micron-sized additives.

Manufacturers producing bio-based printing ink additives face primary challenges related to performance consistency, cost structure, and supply chain reliability. Bio-based alternatives, often derived from natural oils or renewable resources, can exhibit greater batch-to-batch variability and may struggle to match the technical performance (such as solvent resistance or rapid curing speed) of petrochemical-derived additives without complex modification. Furthermore, securing a stable, economically viable supply of certified sustainable raw materials at industrial scale remains a significant hurdle, often resulting in higher production costs compared to conventional ingredients.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.