ID : MRU_ 431958 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

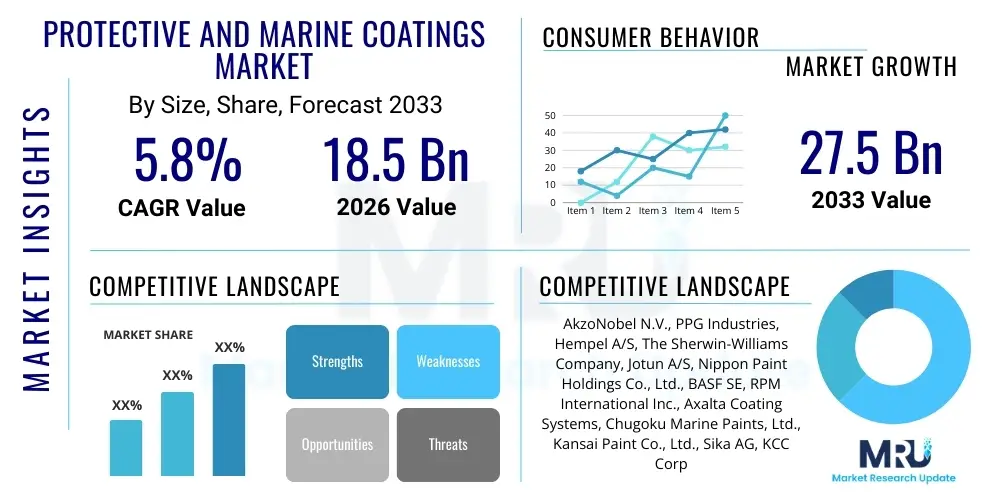

The Protective and Marine Coatings Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 18.5 Billion in 2026 and is projected to reach USD 27.5 Billion by the end of the forecast period in 2033.

The Protective and Marine Coatings Market encompasses highly specialized paint and coating systems designed to safeguard substrates from harsh environmental conditions, corrosion, abrasion, and fouling. These coatings are essential across critical infrastructure and assets, including offshore oil and gas structures, ships, bridges, industrial plants, and processing facilities. The core function of these products is longevity extension and maintenance cost reduction, achieved through superior barrier protection and adhesion properties. Key chemistries utilized include high-performance epoxy, polyurethane, zinc-based primers, and specialized fouling-release technologies, each tailored for specific operational environments, substrate types, and regulatory compliance standards.

Market growth is substantially driven by the global expansion of the shipping industry, increased investment in renewable energy infrastructure such as offshore wind farms, and the necessity for rigorous maintenance of aging public infrastructure worldwide. Protective coatings address severe atmospheric exposure, chemical spills, and high temperatures prevalent in heavy industry, while marine coatings specifically address biofouling and saltwater corrosion. Furthermore, stringent environmental regulations, particularly regarding volatile organic compounds (VOCs) and the disposal of anti-fouling agents, necessitate continuous research and development into eco-friendly, high-solids, and waterborne formulations. The inherent benefits, such as enhanced asset lifespan, improved operational efficiency, and adherence to international safety standards, solidify these coatings as indispensable components of capital expenditure across industrial and maritime sectors.

The Protective and Marine Coatings Market is characterized by robust resilience driven by non-discretionary maintenance cycles and expanding industrialization, particularly in the Asia Pacific region. Business trends indicate a strong shift toward high-performance, solvent-free coatings, accelerated by global regulatory pressures aimed at reducing VOC emissions and minimizing environmental harm from biocides. Key players are focusing on strategic acquisitions to consolidate market share, enhance technological portfolios, and achieve backward integration in raw material supply. Furthermore, the digitalization of coating management, involving sensor technology and predictive maintenance analytics, is emerging as a significant competitive differentiator, optimizing application schedules and reducing downtime for industrial assets.

Regional trends highlight the Asia Pacific's dominance, fueled by massive shipbuilding activity, rapid industrial construction in countries like China and India, and significant infrastructure modernization projects. North America and Europe demonstrate mature markets, primarily emphasizing regulatory compliance, advanced performance requirements for offshore energy transition assets, and the replacement of older, non-compliant coating systems. Segment trends reveal that the use of specialized epoxy coatings remains foundational due to their superior corrosion resistance, while the demand for high-end silicone and fluoropolymer coatings is escalating in niche applications requiring extreme heat, chemical, or abrasion resistance. The marine sector specifically sees strong demand in dry docking and new build segments, focusing intensely on ultra-low friction anti-fouling coatings to achieve fuel efficiency and compliance with the International Maritime Organization (IMO) carbon reduction goals.

User queries regarding the intersection of Artificial Intelligence (AI) and the Protective and Marine Coatings Market primarily revolve around operational efficiency, product innovation speed, and quality control. Common questions include how AI can predict coating failure, optimize formulation chemistry, and automate inspection processes. Users are concerned about the integration costs of smart sensing technologies and the reliability of AI algorithms in interpreting complex environmental data specific to marine environments. The prevailing expectation is that AI will revolutionize asset management by enabling predictive maintenance schedules, reducing unnecessary overhauls, and ultimately lowering life-cycle costs for coated assets suchs as tankers and bridges. Consequently, the focus is shifting toward AI-powered non-destructive testing (NDT) and machine learning models that can correlate vast datasets of environmental stress, coating properties, and historical failure points to provide actionable insights for maintenance planning.

The primary impact of AI is anticipated in the realm of quality assurance and application monitoring. AI-powered vision systems are already being deployed to inspect coating thickness uniformity, identify surface preparation defects, and ensure adherence to manufacturer specifications in real-time, drastically reducing the variability associated with manual inspections. This automation capability is critical in large-scale industrial projects where coating application complexity is high, such as lining storage tanks or applying specialized fireproofing materials. Furthermore, AI facilitates the rapid screening of potential raw materials and polymer structures, accelerating the development cycle for novel, high-performance coatings that meet challenging regulatory mandates, such as developing non-toxic, highly effective anti-fouling solutions.

However, the implementation of AI requires significant investment in data infrastructure and skilled personnel capable of managing complex algorithms and interpreting output. The initial hurdle involves digitizing legacy inspection data and creating comprehensive, standardized databases linking environmental factors (temperature, salinity, UV exposure) to coating performance. While AI promises substantial long-term benefits in maximizing asset uptime and optimizing material usage, its adoption is currently concentrated among large, technologically advanced asset owners and tier-one coating manufacturers, driving a growing technological gap between industry leaders and smaller market participants.

The market dynamics are governed by a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively exerting significant impact forces. A primary driver is the essential need for corrosion protection across global infrastructure, which mandates regular application and renewal of protective coatings irrespective of economic cycles. The restraints largely stem from increasing regulatory burdens, particularly concerning VOC limits and the phase-out of certain biocides, which significantly raises R&D costs and complicates manufacturing processes. Opportunities lie predominantly in the development of sustainable, advanced materials, such as bio-based and self-healing coatings, and the expansion into high-growth sectors like offshore wind energy and water treatment infrastructure, where specialized protective solutions are paramount for long-term operational viability.

Key impact forces include the fluctuating prices of raw materials, such as titanium dioxide, epoxy resins, and petrochemical-derived solvents, which directly affect manufacturer profitability and pricing strategies. Furthermore, the global economic health, particularly trade volume and oil and gas exploration activities, has a cyclical but strong impact on marine new build and offshore protective coating demand. The shift towards sustainable shipping practices and the pressure to reduce carbon footprints are also critical forces, demanding coatings that not only protect but also enhance vessel hydrodynamic performance, pushing innovation toward friction-reducing and non-biocidal anti-fouling technologies that are compliant with global maritime standards.

The long-term resilience of the protective coatings sector, distinct from the more cyclical marine segment, is heavily influenced by government spending on infrastructure maintenance (bridges, pipelines, utilities) and the ongoing need for asset preservation in chemical processing and power generation industries. However, the requirement for highly skilled applicators and the specialized nature of complex coating systems pose logistical and labor constraints, particularly in emerging markets. The competitive landscape is intensely focused on product differentiation based on application ease, speed of cure, and certified long-term performance guarantees, where companies invest heavily in establishing robust track records and maintaining rigorous quality control systems to overcome end-user reluctance regarding switching suppliers.

The Protective and Marine Coatings market is primarily segmented based on Resin Type, Technology, Application, and End-use Industry, reflecting the diversity of functional requirements and operational environments. Resin Type segmentation is critical, with Epoxies dominating due to their excellent adhesion and corrosion resistance, followed closely by Polyurethanes known for their superior UV resistance and durability. The Technology segment differentiates between solvent-borne, waterborne, and powder coatings, with high-solids solvent-borne formulations currently holding a significant share in heavy-duty applications due to their proven performance, though waterborne systems are gaining traction driven by environmental compliance efforts.

The Application segmentation is bifurcated into Protective Coatings and Marine Coatings. Protective coatings cover broad industrial segments like Oil & Gas, Infrastructure, Power Generation, and Chemical Processing, where the coatings are tasked with surviving extreme temperatures, corrosive chemicals, and mechanical stress. Conversely, Marine Coatings are strictly focused on the needs of vessels and offshore structures, categorized into anti-fouling (hulls below the waterline), anti-corrosion (ballast tanks, external hull), and specialized cargo tank linings, each addressing highly specific challenges inherent to the aquatic environment and regulatory framework enforced by bodies like the IMO.

The segmentation structure underscores the highly specialized nature of this market, where no single product offers a universal solution. End-user requirements dictate material selection; for instance, petrochemical storage tanks demand high chemical resistance, while military naval vessels require stealth characteristics alongside superior fouling control. This specialization ensures that manufacturers must maintain a comprehensive portfolio across multiple chemistries and application methods, tailoring solutions to optimize the balance between initial cost, application complexity, and guaranteed long-term performance under severe operational stress.

The Protective and Marine Coatings value chain begins with the upstream procurement of essential raw materials, primarily petrochemical derivatives and specialized minerals. Key inputs include high-performance resins (epoxy, polyurethane, acrylic), functional pigments (titanium dioxide, zinc), various solvents, and performance additives (rheology modifiers, anti-settling agents, biocides). Raw material suppliers, often large chemical conglomerates, hold significant leverage due to the cyclical and concentrated nature of these commodities. Manufacturers must manage complex sourcing strategies to ensure quality consistency and mitigate price volatility, as input costs constitute a substantial portion of the final product price, particularly for high-solids and specialized formulations.

The core of the value chain is the coating manufacturing process, involving sophisticated mixing, dispersion, and quality control procedures to produce performance-validated products. Manufacturers invest heavily in R&D to meet regulatory changes and enhance product performance attributes like faster cure times, lower application temperature limits, and extended service life guarantees. Following manufacturing, the product moves through complex distribution channels. Direct distribution is common for large-scale protective projects and major shipyard contracts, allowing for detailed technical consultation and customized supply logistics. Indirect distribution, involving specialized distributors and authorized dealers, serves the smaller maintenance and repair (M&R) market, ensuring regional availability and immediate technical support.

The downstream segment involves surface preparation specialists and certified coating applicators, who form the final critical link in ensuring product performance, as coating failure is often attributed to poor application rather than material deficiency. End-users (ship owners, infrastructure operators, industrial plant managers) are increasingly demanding comprehensive solutions encompassing product supply, application supervision, and performance monitoring. This trend pushes the value chain towards integrated services, where manufacturers seek to deepen their involvement downstream through training programs, technical field support, and digital tools designed to verify surface profile preparation and environmental conditions before and during coating application.

The primary customers for Protective and Marine Coatings are large asset owners and operators across capital-intensive industries whose profitability depends directly on the longevity and operational reliability of their physical infrastructure. In the protective segment, customers include national and municipal infrastructure agencies responsible for maintaining roads, rail systems, and water management facilities, alongside major global corporations in the energy, petrochemical, and manufacturing sectors. These end-users typically purchase in bulk, prioritizing long-term cost of ownership, certified performance against corrosion and chemical attack, and adherence to specific national and international standards like ISO and NACE guidelines.

In the marine segment, the customer base is concentrated among ship owners, fleet managers, and operators of offshore drilling and exploration assets. Commercial shipping entities, including dry bulk carriers, container fleets, and oil tankers, are driven by two major concerns: reducing dry docking frequency and minimizing fuel consumption, making high-performance anti-fouling and anti-corrosion systems paramount. Naval forces and specialized vessel owners, such as cruise line operators, represent niche, high-value segments demanding specialized coatings for unique functional requirements, including fire resistance, low observability, and advanced acoustic dampening properties.

Purchasing decisions across the entire customer spectrum are highly technical and risk-averse. New coating systems undergo extensive vetting and field testing, often requiring performance guarantees extending beyond five years. The decision-making unit typically involves procurement specialists, chief engineers, and quality assurance managers who must balance upfront cost with lifetime performance benefits, regulatory compliance, and ease of application. Furthermore, the rise of offshore renewable energy firms (wind and tidal power) is introducing a new customer segment with extremely specialized demands for subsea and splash zone protection in highly corrosive environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 27.5 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AkzoNobel N.V., PPG Industries, Hempel A/S, The Sherwin-Williams Company, Jotun A/S, Nippon Paint Holdings Co., Ltd., BASF SE, RPM International Inc., Axalta Coating Systems, Chugoku Marine Paints, Ltd., Kansai Paint Co., Ltd., Sika AG, KCC Corporation, Beckers Group, Wacker Chemie AG, Teknos Group, Carboline Company, Altex Coatings Ltd., Tikkurila Oyj (PPG), Hexion Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The current technology landscape in Protective and Marine Coatings is dominated by advancements focused on sustainability, functional durability, and application efficiency. A major technological push is centered on developing ultra-high solids and 100% solid (solvent-free) epoxy and polyurethane systems. These formulations drastically reduce VOC emissions, complying with increasingly strict global air quality standards, while simultaneously delivering thicker, more robust barrier coats in fewer layers. This allows for faster turnaround times during critical dry docking and industrial maintenance shutdowns, directly translating to enhanced operational efficiency for end-users. Additionally, there is significant research into ambient-curing technologies that function effectively in challenging low-temperature or high-humidity environments, extending the application window for large outdoor projects.

In the marine sector, the technological focus is split between advanced anti-fouling solutions and improved corrosion resistance for ballast tanks and submerged structures. New anti-fouling technologies are moving away from traditional biocide release mechanisms towards sophisticated foul-release coatings, primarily based on silicone elastomers and fluoropolymers. These systems create a low-surface-energy surface, preventing marine organisms from adhering strongly, allowing them to be shed by the vessel's movement, thereby maintaining hull smoothness and drastically reducing hydrodynamic drag and associated fuel consumption. Furthermore, advanced passive fire protection (PFP) coatings, specifically thin-film intumescent epoxies, are seeing rapid adoption in offshore and petrochemical applications, offering superior fire resistance while maintaining structural integrity.

The future technology trajectory involves the integration of nanotechnology and smart materials. Nano-enhanced coatings utilize specialized particles to improve properties such as abrasion resistance, UV stability, and barrier performance at the molecular level, offering extended service life under extreme duress. Concurrently, self-healing coatings, though nascent, represent a groundbreaking technology that can automatically repair micro-cracks and minor damage, significantly delaying the onset of catastrophic corrosion and reducing the frequency of extensive re-coating cycles. Digitalization, through specialized coating software and robotic inspection tools, is also considered a critical technological development, ensuring optimal product selection and adherence to the quality standards required for these highly advanced materials.

Demand is primarily driven by the necessity of corrosion prevention for critical infrastructure, including global shipping fleets, offshore energy assets, and aging industrial plants. Stricter global regulations (IMO standards, VOC limits) and expansion into high-growth sectors like offshore wind energy further accelerate market growth. The inherent cost savings achieved through extended asset lifespan and reduced maintenance cycles are core economic drivers.

Environmental regulations, particularly those limiting Volatile Organic Compounds (VOCs) and phasing out harmful biocides used in anti-fouling paints, significantly increase R&D costs. Manufacturers must invest in complex, high-solids, or waterborne formulations, which can be more expensive to produce but offer superior environmental compliance and often improved performance characteristics, contributing to higher average selling prices.

The high-solids and 100% solids technology segment shows the highest growth potential. These systems effectively reduce solvent emissions while allowing for the application of thicker, more durable films in fewer coats. This efficiency is critical for meeting stringent performance standards and minimizing the operational downtime required for protective and marine maintenance applications across all major industrial sectors.

The dominant technological trend is the shift from traditional biocide-releasing paints to advanced foul-release coatings, typically based on specialized silicone elastomers or fluoropolymers. These technologies function by creating ultra-smooth, low-friction surfaces that prevent bio-adhesion, thereby reducing fuel consumption and complying with international regulations aimed at protecting marine biodiversity.

AI and IoT integration are enabling a paradigm shift toward predictive maintenance. IoT sensors embedded in or near the coatings provide real-time data on environmental stress and potential degradation. AI algorithms analyze this data to accurately predict coating failure, allowing asset owners to schedule re-coating precisely when needed, optimizing resource allocation and maximizing asset uptime across pipelines, bridges, and vessels.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.