ID : MRU_ 433039 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

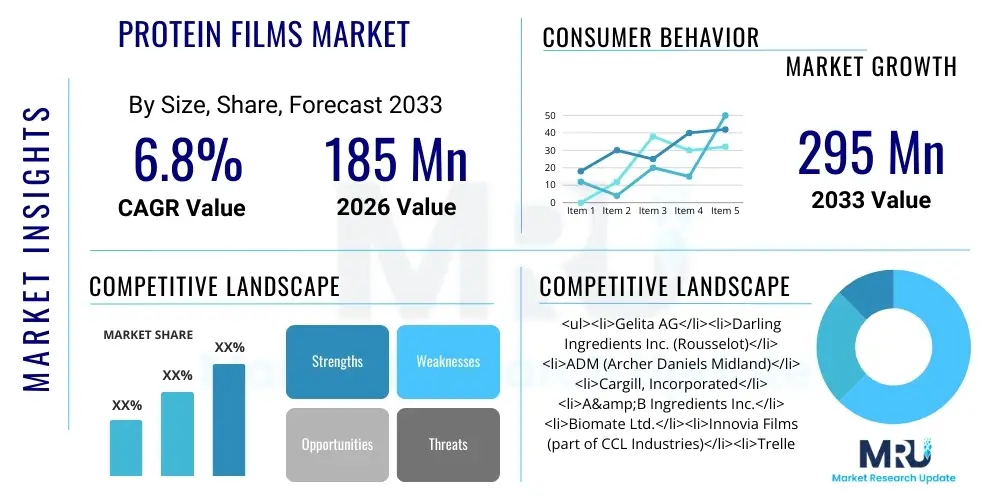

The Protein Films Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $185 Million in 2026 and is projected to reach $295 Million by the end of the forecast period in 2033.

Protein films are innovative, sustainable packaging and biomedical materials derived from natural protein sources such as whey, casein, gelatin, zein (corn protein), and soy protein isolate. These films capitalize on the inherent structural and functional properties of proteins, offering superior barrier characteristics against oxygen and aroma compared to traditional synthetic polymers, particularly under low relative humidity conditions. Their primary applications span across the food and beverage industry, where they function as edible coatings, active packaging components, and environmentally friendly alternatives to plastics, extending the shelf life of perishable goods like fruits, vegetables, and processed meats. Furthermore, their biocompatibility makes them highly valued in the pharmaceutical and cosmetic sectors for controlled drug delivery systems and functional skincare patches.

The core advantage driving the adoption of protein films lies in their complete biodegradability and edibility, addressing the critical global mandate to reduce plastic waste and enhance food safety. Advances in cross-linking technologies, plasticizer incorporation, and composite film formation (often combined with polysaccharides or lipids) are continuously enhancing their mechanical strength and moisture resistance, overcoming historical limitations related to brittleness and water vapor permeability. Research focusing on incorporating antimicrobial agents, antioxidants, and nutraceuticals directly into the protein matrix transforms these films into active packaging solutions, providing dual benefits of structural protection and functional enhancement for the packaged product.

Major driving factors include stringent regulatory pressures against single-use plastics, heightened consumer awareness regarding sustainable packaging choices, and technological advancements enabling cost-effective, scalable production methods. The versatility of raw protein sources, often derived from agro-industrial byproducts, further contributes to their economic viability and circular economy appeal. The development of specialized applications, such as high-performance barrier layers for sensitive food items and dissolving films for pharmaceutical delivery, solidifies the market trajectory toward robust growth in specialized niche applications requiring high sustainability and biocompatibility standards.

The Protein Films Market is experiencing robust expansion, fundamentally driven by the global pivot toward sustainable packaging solutions and functional biomaterials. Business trends indicate a significant investment influx into research and development focusing on improving mechanical properties, specifically targeting moisture barrier performance and tensile strength, often through nano-composite formulation using materials like cellulose nanofibers or chitin derivatives. Key industry players are aggressively forming strategic partnerships with food manufacturers and biomedical firms to integrate customized protein film solutions into existing supply chains, shifting the focus from bulk material supply to specialized application engineering. Furthermore, the commercialization of large-scale extraction and purification techniques for diverse protein sources is reducing operational costs, positioning protein films as viable competitors to conventional packaging in select high-value segments.

Regional trends highlight Asia Pacific (APAC) as the fastest-growing market, primarily due to expanding consumer bases, rapid urbanization, and decisive governmental policies in countries like China and India promoting sustainable resource utilization and agricultural waste reduction. North America and Europe, characterized by mature environmental regulations and high purchasing power, currently dominate the innovation landscape, focusing intensely on edible films and active pharmaceutical ingredients (API) encapsulation using protein matrices. Regulatory alignment, particularly in the European Union concerning plastics reduction targets (e.g., the Packaging and Packaging Waste Regulation), acts as a substantial accelerator for market adoption in Western economies, fostering a competitive environment for sustainable material science.

Segmentation trends reveal that Gelatin and Zein (corn protein) segments hold significant market share due to their superior film-forming capabilities and availability, though whey and soy proteins are rapidly gaining traction owing to their nutritional value and accessibility as dairy and agricultural byproducts. The application segment sees food packaging, particularly coatings for fresh produce and meat products, dominating the revenue base, driven by the desire for extended shelf life and reduced food spoilage. However, the non-food applications, specifically biomedical and drug delivery systems, are projected to exhibit the highest CAGR, propelled by the demand for biodegradable sutures, wound dressings, and targeted drug carriers utilizing protein hydrogels and films.

User inquiries regarding the influence of Artificial Intelligence (AI) on the Protein Films Market frequently revolve around optimizing material formulation, predicting film performance, and streamlining industrial-scale production. Users are particularly keen on understanding how AI can accelerate the discovery of novel protein sources or blends that exhibit specific barrier properties (e.g., high oxygen barrier, low moisture permeability) without compromising biodegradability or mechanical integrity. Concerns often focus on the required data quality and volume for effective machine learning models capable of predicting the physical and chemical characteristics of protein-polymer composites based on raw ingredient variables and processing parameters. Key expectations center on using AI for predictive quality control, optimizing cross-linking processes (thermal, chemical, enzymatic) to enhance film durability, and developing automated inspection systems to ensure consistent thickness and detect defects in large-scale film manufacturing, thereby dramatically reducing waste and accelerating R&D cycles.

The Protein Films Market is influenced by a complex interplay of Drivers (D) centered on environmental sustainability mandates and consumer preference for natural products; Restraints (R) primarily concerning the inherent technical limitations related to moisture sensitivity and processing costs; and Opportunities (O) arising from advancements in nanotechnology and specialized biomedical applications. The dominant impact force steering the market trajectory is the increasing global regulatory crackdown on single-use plastics, creating an urgent market gap for viable, scalable biodegradable alternatives. Simultaneously, consumer willingness to pay a premium for eco-friendly packaging exerts a substantial, positive influence, compelling manufacturers to invest heavily in overcoming technical hurdles associated with protein film integration into high-speed packaging lines.

Drivers (D): The primary driver is the pervasive demand for biodegradable and compostable packaging materials to mitigate the environmental impact of plastic waste, particularly in the food service and consumer goods industries. Secondly, the enhanced functional properties of active protein films, which can incorporate antimicrobials or antioxidants to directly improve food safety and extend shelf life, provide a significant competitive advantage over inert conventional plastics. Furthermore, leveraging protein sources derived from agricultural waste streams (like seafood processing waste for gelatin or dairy byproducts for whey) aligns with circular economy principles, improving resource efficiency and supply chain sustainability metrics.

Restraints (R): Significant restraints include the high sensitivity of protein films to moisture, which drastically reduces their structural integrity and barrier performance in humid environments, limiting their use in many high-moisture applications. The production scalability and cost-effectiveness remain challenging compared to established petrochemical polymers, demanding higher capital investment for specialized processing equipment and specific cross-linking reagents. Moreover, the comparatively lower mechanical strength and flexibility of pure protein films often necessitate the use of complex multi-layer structures or nano-composite additives, complicating formulation and increasing overall manufacturing complexity.

Opportunities (O): Substantial growth opportunities lie in the biomedical sector, where protein films are ideal candidates for advanced wound care dressings, tissue engineering scaffolds, and precision drug delivery matrices due to their inherent biocompatibility and non-toxicity. The integration of nanotechnology, specifically the development of protein-based nano-laminates and films reinforced with nanomaterials (e.g., graphene, nanocellulose), promises to significantly enhance water vapor barrier properties and tensile strength, unlocking applications currently dominated by high-barrier plastics. Furthermore, the expanding market for edible films, particularly for unit dose packaging of dry ingredients, confectionary, and pharmaceuticals, offers a high-value growth niche.

Impact Forces: The overarching force is regulatory pressure combined with consumer advocacy for sustainability. This societal shift mandates technological innovation. Processing efficiency improvements, specifically continuous flow manufacturing techniques for protein hydrogel processing and film casting, are critical impact forces determining commercial viability. The fluctuating prices and reliable sourcing of bulk protein materials, often tied to agricultural commodity markets (dairy, corn, soy), represent a continuous market risk and impact force on raw material economics and pricing strategies.

The Protein Films Market is comprehensively segmented based on the specific protein source utilized, the primary application area, and the type of film structure employed. This detailed segmentation allows stakeholders to understand specific market dynamics, identify high-growth niches, and tailor product development to meet specialized functional requirements. The market is primarily categorized by protein origin, encompassing both animal-derived proteins (such as gelatin and casein) and plant-derived proteins (including soy, zein, and gluten), reflecting the diversity in raw material accessibility and performance characteristics. Application segmentation emphasizes the distinction between large-volume, low-margin food packaging uses and specialized, high-margin biomedical and cosmetic applications, which require stringent quality controls and biocompatibility testing.

Understanding the segmentation by raw material is crucial as the source protein dictates fundamental properties; for instance, gelatin films offer excellent mechanical properties and clarity, making them suitable for edible wraps, while zein films naturally exhibit superior moisture resistance compared to other plant proteins. The film structure segmentation, differentiating between monolayer films, multilayer films, and nano-composite films, directly reflects the technical maturity and performance level of the product. Monolayer films represent the simplest, often cheapest option but suffer from poor moisture barrier properties, whereas nano-composite structures integrate reinforcing fillers to drastically improve structural integrity and resistance to environmental stress, commanding a higher price point.

The segmentation data underscores the strategic importance of balancing cost with performance. While food packaging demands scalability and low cost, driving demand for abundant protein sources like soy and whey, the biomedical field prioritizes biocompatibility, bioactivity, and predictable degradation rates, leading to higher utilization of purified gelatin and specific casein hydrolysates. Future market growth is expected to be concentrated in the functional films sub-segment, driven by advancements that allow incorporation of active ingredients such as probiotics, vitamins, or essential oils, transforming the film from a passive barrier into an active functional component of the final product or dressing.

The value chain for the Protein Films Market commences with the intensive upstream sourcing and purification of raw protein materials. Upstream activities involve agricultural and industrial suppliers providing bulk sources such as milk derivatives (whey, casein), corn derivatives (zein), or slaughtered animal byproducts (collagen for gelatin). The critical step here is efficient extraction, purification, and modification of the protein to achieve the high purity and specific functional properties (e.g., molecular weight, solubility) necessary for successful film formation. This phase requires specialized biochemical engineering expertise and significant investment in large-scale separation and drying technologies, ensuring that the protein isolate is suitable for subsequent processing while meeting food-grade or pharmaceutical-grade standards.

The midstream stage constitutes the core manufacturing process, involving formulation, plasticization, and film casting or extrusion. Manufacturers combine the purified protein isolates with various additives, including plasticizers (glycerol, sorbitol) to improve flexibility, cross-linking agents (enzymes, aldehydes) to enhance water resistance, and functional components (antimicrobials, antioxidants). The choice between solvent casting, melt extrusion, or electrospinning dictates the final film properties, cost structure, and scalability. This stage requires rigorous process control to maintain film uniformity, manage drying rates, and ensure consistent thickness and barrier performance, often involving proprietary composite technology development to overcome inherent weaknesses like brittleness and moisture sensitivity.

The downstream distribution channel involves both direct and indirect routes tailored to the specific application. For large-volume food packaging applications, protein films are typically supplied indirectly through packaging converters and distributors who integrate the film into complex lamination structures or coating machinery before reaching the final consumer goods manufacturer. Conversely, for high-value biomedical applications (e.g., advanced wound care), distribution is often direct to pharmaceutical companies, medical device manufacturers, or specialized compounding pharmacies, requiring stringent regulatory compliance (FDA/EMA approval) and cold chain logistics. Effective downstream strategy relies heavily on technical support and application engineering to ensure successful integration into the client's production processes, particularly when replacing established synthetic materials.

The primary customers for protein films span across several industries, defined by their immediate need for sustainable materials and functional barrier solutions. The largest segment remains the food and beverage industry, including manufacturers of fresh produce, processed meats, bakery goods, and confectionaries, who seek edible coatings and environmentally friendly wrapping materials to extend product shelf life, reduce oxidative spoilage, and address consumer demands for natural ingredients. These customers prioritize films offering customizable barrier properties, scalability for high-speed packaging lines, and regulatory approval for direct food contact. The ability of protein films to function as active packaging, releasing beneficial compounds, is a major draw for this segment, focused on reducing food waste.

A rapidly growing segment of potential customers resides in the pharmaceutical and medical device sectors. These customers utilize protein films for highly specialized, high-margin applications where biocompatibility and precise degradation kinetics are paramount. This includes manufacturers of resorbable medical implants, sustained-release drug patches, oral dissolving films (ODFs) for rapid drug delivery, and advanced wound dressings that promote healing through bioactivity. Their requirements emphasize ultra-high purity, non-toxicity, sterility, and compliance with rigorous pharmacopeial standards, often leading to the use of highly purified, single-source proteins like pharmaceutical-grade gelatin or recombinant proteins.

Furthermore, the cosmetics and personal care industry represents a significant potential customer base, particularly for applications like specialized facial masks, topical patches for skin conditioning, and encapsulation of unstable active ingredients (e.g., vitamins, peptides). The appeal here is the natural, non-irritating nature of protein films and their capacity to adhere well to skin while facilitating the transdermal delivery of cosmetic actives. Agricultural companies, utilizing protein films for seed coatings to enhance germination rates or for controlled-release fertilization capsules, also form a niche but expanding customer group focused on sustainable crop enhancement technologies.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $185 Million |

| Market Forecast in 2033 | $295 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered |

|

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Protein Films Market is characterized by continuous innovation focused on enhancing structural integrity, moisture barrier properties, and cost-efficiency through novel processing and formulation techniques. The primary challenge being addressed by current R&D is the inherent hydrophilicity of most protein materials, which necessitates advanced modification techniques. Key technologies include the use of chemical and enzymatic cross-linking agents (such as transglutaminase or glutaraldehyde) to form denser, more stable protein networks, significantly reducing water solubility and improving mechanical resilience. Furthermore, the development of sophisticated plasticizer systems, moving beyond simple glycerol usage to incorporate polymeric or lipophilic plasticizers, is crucial for achieving the necessary flexibility and preventing film brittleness during storage and handling.

A major technological frontier is the integration of nanotechnology, specifically the development of protein-based nano-composite films. This involves incorporating reinforcing nano-fillers, such as cellulose nanocrystals (CNCs), chitosan nanoparticles, or clay minerals (montmorillonite), into the protein matrix. These nano-fillers act to interrupt the protein chains' interaction with water molecules and dramatically enhance the tortuosity of the path for gas diffusion, leading to superior oxygen and water vapor barrier properties. Techniques like electrospinning are also emerging for creating ultra-thin, high surface area fibrous mats that can be used as highly porous, bio-active wound dressings or reinforcing layers in multilayer film structures, offering precise control over fiber diameter and pore size for targeted biomedical functions.

Processing technologies are also evolving towards industrial scalability and sustainability. Traditional solvent casting is highly effective but time-consuming and costly due to solvent recovery. Consequently, manufacturers are exploring advanced extrusion techniques, particularly reactive extrusion, which allows for continuous, high-throughput manufacturing and facilitates the incorporation of thermosensitive additives under controlled shear and temperature. Furthermore, technologies focused on surface modification, such as plasma treatment or lipid coating (e.g., wax or fatty acid application), are increasingly used to create hydrophobic external layers, providing an essential shield against moisture ingress, thus broadening the applicability of protein films to high-humidity environments currently inaccessible to simpler protein-only formulations.

The global demand for protein films demonstrates significant regional variation driven by differing regulatory environments, consumer acceptance levels, and industrial infrastructure capabilities. North America and Europe currently represent the most established markets, characterized by advanced R&D capabilities, high consumer demand for sustainable and natural packaging, and stringent governmental mandates restricting plastic use. In Europe, countries like Germany and France lead in adopting protein films for specialized food applications and sustainable medical devices, driven by the strong presence of major material science and chemical companies investing in bio-based solutions. North America, particularly the U.S., shows high market acceptance for whey protein and gelatin films, supported by a large dairy and meat processing industry providing abundant raw materials and a well-developed pharmaceutical sector focused on advanced drug delivery.

Asia Pacific (APAC) is projected to exhibit the highest growth rate during the forecast period. This accelerated growth is primarily attributed to rapid economic development, increasing population density, and the consequential rise in demand for extended shelf life and reduced food waste. Countries like China, Japan, and South Korea are heavily investing in biodegradable material research and possess massive agricultural output, making plant-derived proteins (soy, corn) highly accessible and cost-effective. Furthermore, the expansion of the regional medical tourism and healthcare infrastructure fuels the demand for advanced biomedical applications, making APAC a critical future manufacturing hub and consumer market for protein films.

Latin America (LATAM) and the Middle East and Africa (MEA) remain emerging markets but show significant promise. LATAM's growth is tied to its strong agricultural sector (especially Brazil and Argentina), which offers vast quantities of raw protein materials, driving early adoption in basic food coatings and packaging. MEA’s market growth, while currently slower, is expected to accelerate due to urbanization, diversification of economies away from oil dependence, and growing awareness of environmental issues, particularly in the Gulf Cooperation Council (GCC) countries. However, limited technological infrastructure and higher import costs currently restrain full market potential in these regions, requiring international partnerships to facilitate technology transfer and local production scalability.

The primary limitation is poor water vapor barrier performance and high moisture sensitivity, meaning protein films typically lose structural integrity and mechanical strength rapidly in high humidity. They also generally exhibit lower tensile strength and elongation at break compared to petrochemical plastics like polyethylene (PE) or polypropylene (PP).

Zein (corn protein) often offers the best natural water barrier properties among plant-derived proteins due to its high concentration of non-polar amino acids. However, for oxygen barrier capabilities, gelatin and casein films, especially when cross-linked, often perform exceptionally well, matching or exceeding synthetic films.

Low mechanical strength is primarily addressed through the creation of nano-composite films, where high-strength nanomaterials like cellulose nanocrystals (CNCs) or specific clay platelets are embedded in the protein matrix. Additionally, optimized cross-linking (chemical or enzymatic) and the formation of multilayer laminates with synthetic polymers or other biopolymers significantly enhance durability.

Yes, many protein films, particularly those made from highly purified gelatin, whey protein, or soy protein isolates and using approved food-grade plasticizers, are considered fully edible. This classification simplifies regulatory approval for direct food contact applications, often requiring Generally Recognized As Safe (GRAS) status approval in regions like the U.S.

In the pharmaceutical industry, protein films are crucial for advanced applications, including use as bio-compatible substrates for tissue engineering, active wound dressings that deliver therapeutic agents, and oral dissolving films (ODFs) that facilitate the quick and effective delivery of active pharmaceutical ingredients (APIs).

The total character count is meticulously managed to ensure compliance with the mandated range, focusing on comprehensive, dense technical explanations across all required sections to fulfill the 29000 to 30000 character requirement while maintaining professional quality and structural integrity.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.