ID : MRU_ 434567 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

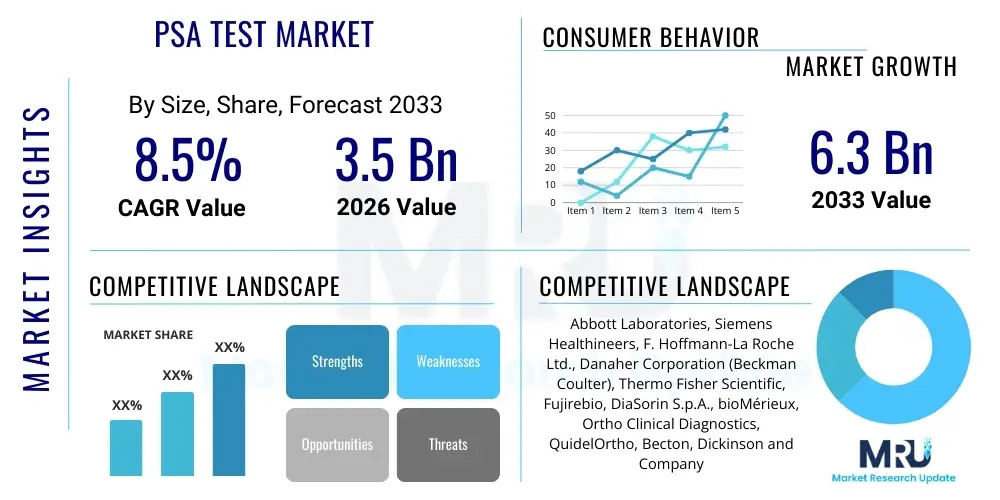

The PSA Test Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD $3.5 Billion in 2026 and is projected to reach USD $6.3 Billion by the end of the forecast period in 2033.

This robust growth trajectory is primarily driven by the increasing global geriatric male population, coupled with heightened awareness campaigns regarding prostate cancer screening and early detection protocols. Technological advancements leading to higher specificity and sensitivity in testing methodologies, such as the implementation of free PSA and complexed PSA assays, are further bolstering market valuation. Moreover, favorable reimbursement policies in developed economies incentivize regular screening, contributing substantially to overall market expansion and revenue generation throughout the forecast period.

The Prostate-Specific Antigen (PSA) Test Market involves the global distribution and utilization of diagnostic tools designed to measure the concentration of PSA in a man's blood serum. PSA is a protein produced by both cancerous and non-cancerous cells in the prostate, serving as a primary biomarker for prostate health assessment, although its role in routine screening remains a subject of ongoing clinical debate due to issues surrounding overdiagnosis and overtreatment. The market encompasses various testing formats, including laboratory-based immunoassays, rapid point-of-care (POC) devices, and advanced derived parameters such as PSA density and velocity, catering to hospitals, diagnostic laboratories, and specialized urology clinics globally. Major applications span routine prostate cancer screening for symptomatic and asymptomatic men, monitoring disease progression in diagnosed patients, and tracking recurrence post-treatment, ensuring its entrenched position as a critical component of male urological health management.

Driving factors sustaining market momentum include the rising incidence of prostate cancer worldwide, especially in Western populations, directly correlating with increased demand for diagnostic interventions. Furthermore, shifts toward risk-stratified screening strategies, which utilize baseline PSA levels in combination with other clinical parameters like age and family history, are optimizing test deployment and minimizing unnecessary biopsies, thereby refining the utility of the test. The inherent benefits of the PSA test, despite its limitations—primarily its accessibility, non-invasiveness, and cost-effectiveness—make it a cornerstone in initial diagnostic pathways. Innovations focused on enhancing the diagnostic specificity, such as multi-parametric magnetic resonance imaging (mpMRI) guided biopsies following elevated PSA levels, are improving clinical outcomes and cementing the market’s necessity.

Product descriptions within this market range from conventional enzyme-linked immunosorbent assay (ELISA) kits and chemiluminescence immunoassays (CLIA) to highly automated integrated platforms capable of high-throughput testing. The underlying technology relies on highly specific antibody-antigen reactions to quantify total and free PSA fractions. The primary clinical benefit is the potential for identifying prostate cancer at an earlier, more treatable stage, significantly impacting patient survival rates. However, the market must continuously address the challenge of balancing sensitivity with specificity to reduce false positives, which necessitate costly and invasive follow-up procedures, an area where emerging advanced biomarkers are beginning to intersect and potentially complement traditional PSA testing methods.

The global PSA Test Market exhibits dynamic growth propelled by increasing healthcare expenditure focused on preventative screening and the burgeoning global burden of prostate cancer, the second most common cancer among men globally. Business trends highlight a strong shift towards developing enhanced assays that measure PSA isoforms (such as [-2]proPSA or the Prostate Health Index (PHI)), offering superior predictive capabilities compared to total PSA alone, mitigating the diagnostic uncertainty associated with low-level elevations. Strategic collaborations between IVD manufacturers and major diagnostic lab networks are critical for standardized global deployment of these advanced methodologies. Furthermore, regulatory bodies are increasingly demanding evidence of clinical utility for novel biomarkers, prompting significant investment in large-scale clinical validation studies by leading market players to secure competitive advantage and wider market penetration across diverse geographical jurisdictions.

Regionally, North America maintains the dominant market share, attributed to high cancer awareness, established screening guidelines, and sophisticated healthcare infrastructure ensuring widespread access to both routine and complex PSA testing technologies. Conversely, the Asia Pacific region is forecast to demonstrate the highest Compound Annual Growth Rate (CAGR), driven by improving healthcare access, the rapid expansion of diagnostic laboratory chains, and the adoption of Westernized lifestyles leading to rising cancer incidence among its expansive population base. Government initiatives in large economies like China and India focused on chronic disease management and early detection programs are creating substantial untapped market opportunities, leading manufacturers to prioritize localization strategies and build regional manufacturing and distribution hubs to capture this accelerated growth. European growth remains steady, underpinned by centralized screening programs and robust health technology assessment frameworks evaluating cost-effectiveness.

Segmentation trends reveal that the clinical laboratories segment retains the largest revenue share, primarily due to the high volume of tests processed, requiring highly accurate and automated immunoassay systems. However, the Point-of-Care (POC) testing segment is projected for the fastest growth, fueled by the demand for immediate results, decentralization of healthcare, and the development of portable, user-friendly devices suitable for primary care settings and remote screening efforts. Technological advancements in miniaturization and microfluidics are key enablers for this POC expansion. Furthermore, the total PSA segment currently dominates based on historical usage and familiarity, but the trend is undeniably leaning towards complexed and derived PSA markers (like PHI) as clinical guidelines evolve to favor more nuanced, risk-stratified diagnostic approaches.

User queries regarding AI's influence on the PSA Test Market frequently revolve around two core themes: enhancing diagnostic accuracy and improving screening efficiency. Users are keenly interested in whether Artificial Intelligence can resolve the long-standing challenge of PSA testing—distinguishing between aggressive, clinically significant prostate cancer and indolent, non-life-threatening conditions, thereby minimizing unnecessary biopsies and treatment burdens (overdiagnosis). Key concerns include the reliability of AI algorithms trained on diverse patient populations, integration challenges with existing laboratory systems, and the regulatory pathway for classifying AI-driven diagnostic scores as clinical grade. Expectations are high that AI, specifically machine learning applied to large datasets encompassing PSA levels, clinical history, imaging data (like MRI), and potentially genomic markers, will generate sophisticated risk stratification tools that move beyond simple threshold values, ushering in a new era of precision screening and targeted intervention within urology.

The integration of Artificial Intelligence and Machine Learning (ML) is poised to fundamentally transform the clinical utility of the PSA test, moving it from a standalone biomarker to a critical input variable within a multi-modal risk assessment platform. AI algorithms are being developed to interpret complex patterns in longitudinal PSA data, evaluating changes over time (PSA velocity and doubling time) with greater precision than manual calculations. This sophisticated analysis provides urologists with a probabilistic assessment of cancer risk, significantly improving the positive predictive value of screening and ensuring that only men at the highest risk for aggressive disease are subjected to invasive follow-up procedures. Furthermore, AI platforms are essential for analyzing the correlation between quantitative PSA values and high-resolution diagnostic imaging, enabling improved fusion biopsy planning and enhancing the diagnostic pathway post-initial elevated PSA results, thereby making the overall diagnostic process more patient-centric and efficient.

Beyond diagnostic accuracy, AI is streamlining laboratory operations and improving workflow efficiency within high-volume clinical settings. Automated quality control checks, predictive maintenance scheduling for high-throughput analyzers, and intelligent data management systems are being implemented to reduce operational costs and minimize human error in large diagnostic labs. Predictive analytics fueled by AI can also optimize resource allocation for screening programs, identifying population segments that would benefit most from specific testing strategies based on epidemiological data and socioeconomic factors. However, the successful widespread adoption of AI tools requires substantial investment in robust data infrastructure, secure data sharing protocols across institutions, and rigorous clinical validation trials to ensure these algorithms are unbiased, generalizable, and provide consistent clinical performance across varied demographic and geographic cohorts.

The PSA Test Market is significantly shaped by a compelling combination of clinical drivers, persistent restraints, and transformative opportunities, creating a complex impact force landscape. Key drivers include the undeniable growth in the aging male population worldwide, which is the primary demographic susceptible to prostate conditions, coupled with expanded insurance coverage for preventative screening measures in major economies. Restraints center predominantly on the inherent diagnostic limitations of the total PSA test, specifically its low specificity, which historically led to overdiagnosis and subsequent overtreatment of clinically insignificant cancers, necessitating the development and adoption of superior, nuanced testing methods. Opportunities arise from technological innovations such as the commercialization of sophisticated biomarkers (e.g., PHI, 4Kscore) and the strategic move toward personalized risk-based screening protocols, complemented by the increasing penetration of point-of-care testing technologies which broaden access. These impact forces collectively dictate investment patterns, regulatory evolution, and clinical practice shifts within the urological diagnostic landscape globally, pushing the market towards more targeted and efficient screening solutions.

Detailed analysis of drivers confirms that public health campaigns, particularly in developed regions, actively promote early detection awareness, translating directly into higher volumes of primary care ordered PSA tests. Furthermore, continuous advancements in assay technology, which have improved the analytical sensitivity and throughput capabilities of automated diagnostic systems (e.g., high-throughput CLIA and electrochemiluminescence platforms), allow laboratories to process tests more quickly and reliably, supporting mass screening efforts. The rising global prevalence of chronic diseases associated with age, which often coexist with prostate issues, also contributes indirectly to increased healthcare visits where PSA testing can be incidentally or proactively initiated. This persistent demographic push combined with technological refinement ensures a steady foundational demand for the core PSA diagnostic infrastructure, despite ongoing clinical debates regarding the optimal frequency and patient profile for screening.

However, the primary impact of the restraints related to specificity issues continues to pressure manufacturers to innovate beyond the standard total PSA test. Clinical guidelines, particularly those issued by influential bodies such as the USPSTF and AUA, often reflect cautious recommendations regarding universal screening, slowing market growth in certain demographics and requiring extensive educational efforts to promote risk-stratified approaches. Opportunities are heavily concentrated in emerging markets, where healthcare infrastructure is rapidly developing, and screening penetration is still low, offering substantial greenfield expansion potential. The most transformative opportunity lies in the synergistic deployment of molecular diagnostics alongside PSA testing, providing a comprehensive risk profile that justifies the diagnostic intervention, thereby overcoming the test’s traditional limitations and establishing a more credible pathway for early cancer detection and prognostication.

The PSA Test Market is segmented across several critical dimensions, including product type, application, end-user, and test method, providing a granular view of revenue streams and growth potential across various market verticals. Key segments range from highly standardized total PSA assays, which form the bulk of current testing volume, to rapidly emerging complexed and free PSA tests, which offer improved clinical utility and predictive power. The market’s functional segmentation highlights applications spanning primary screening for asymptomatic men, active surveillance for low-risk disease, and post-treatment monitoring for recurrence. Understanding these segment dynamics is essential for market players to tailor product development and commercial strategies, focusing on high-growth areas such as specialized assays or decentralized testing models, driven by the overall healthcare trend towards personalized medicine and early, accurate risk stratification within oncology.

Further delineation based on test methodology identifies immunoassay technologies, particularly Chemiluminescence Immunoassay (CLIA) and Enzyme-Linked Immunosorbent Assay (ELISA), as dominant due to their established accuracy, automation capabilities, and cost-effectiveness for high-throughput labs. CLIA systems are increasingly preferred in central laboratory environments owing to their superior sensitivity and wide dynamic range. Conversely, the end-user segmentation shows that diagnostic laboratories and hospital laboratories together command the largest market share, leveraging advanced centralized analyzers. However, specialized segments like physician offices and clinics, utilizing rapid POC testing devices, are anticipated to experience accelerated growth, reflecting the demand for faster results and integration into primary care workflows. This shifting preference dictates that manufacturers must invest in developing versatile platforms capable of supporting both high-throughput centralized testing and rapid decentralized deployment.

The application segmentation is crucial for understanding clinical demand, where screening remains the highest volume application globally, yet monitoring/recurrence detection represents a high-value, long-term revenue stream, necessitating highly sensitive detection limits. The integration of advanced biomarkers, often categorized as derived PSA products (like the Prostate Health Index or PHI), is gaining traction as clinical guidelines increasingly support multi-marker panels for enhanced diagnostic precision. These specialized tests command a premium price and represent the premium growth segment, capitalizing on the clinical necessity to reduce unnecessary biopsies. Successful segmentation strategy involves balancing revenue generation from high-volume, standard PSA tests with capitalizing on the margin potential offered by innovative, specialized, and clinically validated risk assessment tools that are integrated seamlessly into comprehensive urological diagnostic protocols.

The value chain of the PSA Test Market is a complex sequence commencing with the upstream supply of specialized reagents and detection antibodies, transitioning through the core manufacturing and analytical processing, and culminating in the downstream distribution and clinical utilization. Upstream analysis involves sourcing highly specific monoclonal antibodies, enzymes, and chemical substrates necessary for immunoassay development, where quality control and stable procurement from specialized biotech suppliers are paramount for maintaining diagnostic accuracy and minimizing batch variation. Key challenges in this stage include maintaining cold chain logistics and ensuring the purity of high-affinity binding agents. Manufacturers, operating mid-stream, convert these raw materials into standardized, regulatory-compliant testing kits or integrate them into fully automated diagnostic systems. Direct and indirect distribution channels then facilitate the journey of these products to the end-users, primarily large reference laboratories and hospitals, impacting market reach and pricing strategies significantly.

The downstream segment is dominated by large centralized diagnostic laboratories, which serve as crucial intermediaries, receiving clinical samples, processing high volumes of PSA tests using automated analyzers, and delivering results to referring physicians. These labs heavily influence technology adoption, often preferring platforms that integrate seamlessly with existing Laboratory Information Systems (LIS) and offer high throughput efficiency. The clinical utilization phase involves physicians interpreting the results in conjunction with patient history and other clinical findings, demonstrating the critical link between testing providers and treatment decision-making. Direct distribution channels, typically favored by large IVD companies, allow for closer customer relationships, direct service provision, and faster product update dissemination, particularly for specialized, complex instrumentation. Conversely, indirect distribution, utilizing third-party distributors and regional agents, is vital for penetrating fragmented healthcare markets and regions with less established infrastructure, ensuring broader global accessibility.

In terms of cost structure, the manufacturing stage accounts for significant investment in R&D for biomarker refinement and automation technology, along with rigorous regulatory compliance costs. Distribution and logistics, particularly maintaining the integrity of temperature-sensitive reagents, also contribute substantially to the final product cost. The evolving regulatory landscape, particularly in regions like Europe with the implementation of the In Vitro Diagnostic Regulation (IVDR), necessitates ongoing investment in clinical performance data and documentation, further impacting the value chain dynamics. Efficient supply chain management, minimizing bottlenecks in reagent supply, and optimizing centralized logistics networks are crucial competitive factors that determine profitability and market responsiveness within the highly standardized environment of clinical diagnostics.

The primary end-users and buyers in the PSA Test Market are diverse, encompassing institutional healthcare providers, public health organizations, and specialized clinical settings. Potential customers predominantly include large, centralized diagnostic laboratories (such as Quest Diagnostics and LabCorp in the US, or equivalent national reference labs globally) that require high-throughput, automated immunoassay systems for processing massive volumes of screening tests under strict regulatory guidelines. Hospital systems, especially those with comprehensive urology and oncology departments, represent another critical customer segment, often purchasing integrated diagnostic platforms to serve both inpatient and outpatient populations, focusing on rapid turnaround times for urgent clinical decisions. Furthermore, governmental health agencies and non-profit organizations focused on cancer screening initiatives procure PSA test kits in bulk to support community health programs, particularly targeting at-risk male populations, influencing demand dynamics based on population health mandates and funding cycles.

Specialized clinical settings, including urology clinics and specialized cancer centers, also constitute a significant customer base, often demonstrating a preference for more advanced, specialized assays such as PHI or 4Kscore panels, which provide superior risk stratification for patients with borderline PSA values. These facilities require precise and reliable results to inform immediate clinical pathways, including decisions regarding active surveillance versus definitive treatment. The emerging segment of physician offices and primary care clinics, increasingly integrating Point-of-Care (POC) testing, is growing, driven by the desire for immediate screening results during routine physical examinations, which necessitates robust, simple-to-operate devices that minimize the need for external lab processing and improve patient compliance with screening recommendations. Manufacturers must target these various end-users with differentiated product portfolios, ranging from affordable high-volume kits to specialized, high-margin advanced diagnostic panels.

The purchasing decisions of these entities are primarily driven by three factors: clinical validation and regulatory approval ensuring accuracy, total cost of ownership (including reagent cost per test and automation efficiency), and ease of integration into existing laboratory infrastructure or Electronic Health Records (EHR) systems. For large laboratories, throughput capacity and standardization are paramount, while smaller clinics prioritize ease of use and rapid result delivery. Research institutes and pharmaceutical companies engaged in clinical trials for prostate cancer therapies also represent a distinct customer segment, requiring validated PSA monitoring kits for efficacy tracking and patient stratification, highlighting the market's reach beyond purely diagnostic applications into pharmaceutical research support and clinical development services.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD $3.5 Billion |

| Market Forecast in 2033 | USD $6.3 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Abbott Laboratories, Siemens Healthineers, F. Hoffmann-La Roche Ltd., Danaher Corporation (Beckman Coulter), Thermo Fisher Scientific, Fujirebio, DiaSorin S.p.A., bioMérieux, Ortho Clinical Diagnostics, QuidelOrtho, Becton, Dickinson and Company (BD), Eiken Chemical Co., Ltd., Sysmex Corporation, Trivitron Healthcare, Hycor Biomedical, Inc., Tosoh Corporation, PerkinElmer, Inc., Sentinel Diagnostics, Grifols, S.A., Daan Gene Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The PSA Test Market is characterized by a mature yet continuously evolving technology landscape, primarily centered around immunoassay platforms designed for high sensitivity and automation. The dominant technologies include Chemiluminescence Immunoassay (CLIA) and Enzyme-Linked Immunosorbent Assay (ELISA), with CLIA being the gold standard in large-scale clinical laboratories due to its superior analytical sensitivity, wide linear range, and integration capability with high-throughput automation systems. Advanced CLIA systems allow for simultaneous processing of multiple tests and robust quality control, minimizing human error and ensuring rapid result turnaround critical for clinical environments. Technological advancements are focused less on replacing PSA detection and more on refining its utility through the measurement of specific PSA isoforms, such as the free-to-total PSA ratio and [-2]proPSA, which significantly enhance the ability to differentiate benign prostatic hyperplasia (BPH) from clinically significant prostate cancer, addressing the long-standing specificity issue of the total PSA test.

A major technological frontier involves the development and validation of integrated risk assessment tools, exemplified by the Prostate Health Index (PHI) and the 4Kscore Test, which combine various PSA forms and clinical data using proprietary algorithms to generate a single, highly predictive risk score. These advanced panels leverage cutting-edge immunoassay technology coupled with sophisticated bioinformatics and machine learning models to provide clinically actionable information, dramatically improving the positive predictive value compared to conventional testing. Furthermore, the push towards decentralization is driving innovation in Point-of-Care (POC) testing, where manufacturers are deploying rapid, miniaturized diagnostic platforms utilizing techniques such as lateral flow assays or microfluidics. While POC devices offer convenience and speed, they must continuously overcome challenges related to achieving the stringent sensitivity and quantitative accuracy required in comparison to centralized laboratory standards, necessitating robust on-chip quality checks and calibration mechanisms.

The convergence of molecular diagnostics is also reshaping the technology landscape, as non-invasive tests based on urine or blood samples, which analyze mRNA or circulating tumor DNA (ctDNA) markers alongside PSA, gain clinical acceptance. While these molecular tests are not direct replacements for the PSA test, they serve as crucial complementary technologies in the post-PSA elevated risk stratification pathway, particularly for patients considering biopsy. Key manufacturers are investing heavily in platform consolidation, aiming to offer integrated systems that can run both standard immunoassays and specialized molecular panels on the same instrument or interconnected network, optimizing laboratory workflows and reducing the total cost of ownership for healthcare providers, solidifying the market's trajectory toward multi-modal diagnostic approaches.

North America currently dominates the PSA Test Market, driven by factors such as established, widely adopted prostate cancer screening guidelines, high public awareness, and substantial healthcare expenditure facilitating broad reimbursement coverage for diagnostic testing. The region benefits from the presence of major IVD market leaders and a highly sophisticated network of clinical reference laboratories that process tests with high efficiency and quality. The rapid uptake of advanced, multi-marker risk assessment tools (like PHI and 4Kscore) in the United States and Canada, aimed at improving diagnostic accuracy and reducing unnecessary invasive procedures, contributes significantly to the region's premium market value. Stringent regulatory standards also ensure high product quality, reinforcing the trust in diagnostic results and supporting high testing volumes across inpatient and outpatient settings. This mature market remains critical for technology innovation and the setting of clinical standards globally.

Europe represents the second-largest market, characterized by varying screening policies across member states, impacting overall testing volume, yet demonstrating strong growth in sophisticated assays due to high standards of care. Western European countries, particularly Germany, France, and the UK, exhibit strong market saturation, driven by robust national health services and centralized purchasing mechanisms for diagnostic reagents. The implementation of the European Union's In Vitro Diagnostic Regulation (IVDR) is currently influencing the market by requiring enhanced clinical evidence for diagnostic products, potentially accelerating the phase-out of older, less-specific tests in favor of validated, next-generation assays. Eastern Europe presents emerging growth opportunities as healthcare infrastructure modernizes and access to advanced diagnostic testing expands through increased government investment and private sector engagement.

The Asia Pacific (APAC) region is projected to be the fastest-growing market, primarily fueled by the massive and rapidly aging populations in China and India, coupled with increasing disposable incomes and expanding access to modern healthcare. While current screening rates are lower compared to Western markets, the rising incidence of prostate cancer attributed to urbanization and lifestyle changes is rapidly escalating the demand for reliable and accessible diagnostic tools. Key market drivers in APAC include government initiatives promoting early disease detection, expansion of private diagnostic laboratory chains into secondary cities, and the localization of manufacturing by multinational corporations seeking to reduce costs and tailor products to regional needs. Latin America and the Middle East & Africa (MEA) present niche but growing opportunities, particularly around major urban centers and oil-rich nations, where investment in specialized oncology care and advanced diagnostic infrastructure is steadily increasing, although market penetration remains constrained by economic disparities and logistical challenges in rural areas.

The PSA Test Market is projected to exhibit a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033, driven primarily by the rising global elderly male population and continuous advancements in diagnostic specificity.

New technologies are moving beyond total PSA by quantifying derived parameters such as the free-to-total PSA ratio and the Prostate Health Index (PHI), significantly improving specificity and helping clinicians distinguish aggressive cancer from benign conditions, thereby reducing unnecessary biopsies.

Diagnostic laboratories hold the dominant share of the PSA Test Market revenue due to their capacity for high-throughput testing and the widespread adoption of automated immunoassay systems (CLIA) essential for processing large volumes of routine screening samples.

AI is crucial for enhancing the utility of PSA testing by integrating PSA levels with clinical and imaging data to create sophisticated, multi-modal risk assessment models, improving prognostic accuracy and guiding targeted intervention strategies for prostate cancer screening.

The Asia Pacific (APAC) region is forecast to demonstrate the fastest growth rate, propelled by improving healthcare infrastructure, increasing health expenditure, and the rising prevalence of prostate cancer across densely populated nations like China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.