ID : MRU_ 431591 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

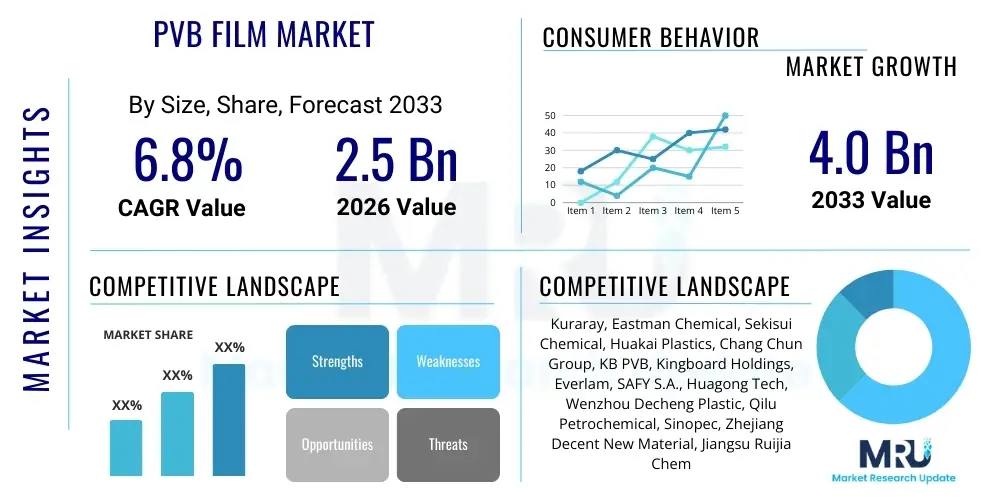

The PVB Film Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at $2.5 Billion in 2026 and is projected to reach $4.0 Billion by the end of the forecast period in 2033.

The Polyvinyl Butyral (PVB) film market encompasses the production and distribution of thermoplastic interlayer films primarily used in the lamination of glass. PVB film is crucial for manufacturing laminated safety glass, which is characterized by high impact resistance and shatter retention properties. Its chemical structure, derived from the reaction of polyvinyl alcohol with butyraldehyde, grants it excellent adhesion to glass, superior optical clarity, and elasticity, making it indispensable in applications where safety and structural integrity are paramount. The film acts as a protective barrier, preventing glass fragments from scattering upon impact, thereby significantly reducing the risk of injury in accidents or natural disasters.

Major applications for PVB film span across the automotive, architectural, and solar energy sectors. In the automotive industry, PVB is foundational for vehicle windshields and increasingly for side and rear windows, providing both safety and acoustic dampening. Within architecture, it is widely used in façades, skylights, railings, and windows in both residential and commercial buildings, driven by stringent building codes emphasizing safety, security, and noise reduction. The inherent benefits of PVB films include enhanced security against breakage, UV light blocking capabilities, and improved sound insulation, which contributes significantly to energy efficiency and occupant comfort in modern construction.

The market is predominantly driven by the escalating demand for laminated safety glass globally, fueled by stricter governmental regulations concerning vehicular and building safety. Furthermore, the rapid growth in the construction industry, particularly in emerging economies, coupled with increasing consumer awareness regarding safety features, is accelerating market expansion. Technological advancements focusing on developing specialty PVB films—such as those offering enhanced acoustic performance, heat reflection, or integration into smart glass technologies—further solidify PVB's crucial role in various high-performance applications, ensuring sustained growth throughout the forecast period.

The PVB Film market is experiencing robust growth characterized by shifting manufacturing landscapes and intense focus on high-performance applications. Business trends indicate a strong push towards sustainable and specialty films, notably acoustic PVB films addressing noise pollution in urban settings, and thicker, highly durable films for severe weather resistance. Consolidation among major players and strategic investments in production capacity expansion, particularly in Asia Pacific, define the competitive environment. The automotive sector remains a critical growth engine, driven by the expanding production of electric vehicles (EVs) and autonomous vehicles, which require advanced safety glass solutions for integrated sensors and heads-up displays (HUDs), demanding films with exceptional optical quality and minimal distortion.

Regionally, Asia Pacific (APAC) stands out as the dominant market, propelled by massive infrastructure development in countries like China and India, coupled with rapid urbanization that necessitates modern, safety-compliant architectural structures. Europe and North America demonstrate mature markets, primarily driven by stringent environmental regulations and the replacement of existing structures with energy-efficient, laminated glass solutions. These developed regions are the primary adopters of premium and specialized PVB films, including those designed for thermal insulation and solar control, reflecting a trend towards higher average selling prices (ASPs) for advanced products compared to standard films prevalent in high-volume construction in APAC.

Segmentation trends highlight the increasing importance of the high-performance segment over standard PVB films. While standard films continue to dominate volume in general architectural applications, the growth rate is significantly higher in segments addressing noise reduction and advanced solar energy integration. The construction segment leads in market share by application, yet the automotive segment is projected to exhibit the fastest growth CAGR, supported by regulatory requirements for enhanced safety features (e.g., mandatory laminated side glass) and the increasing complexity of vehicle glazing systems. Manufacturers are focusing R&D on cross-linking technologies to improve film adhesion in challenging environmental conditions and developing thinner, lighter films to meet automotive weight reduction goals.

User questions related to AI's impact on the PVB Film market frequently revolve around how artificial intelligence and machine learning (ML) can improve manufacturing yield, ensure film quality consistency (especially regarding optical clarity and adhesion properties), and optimize complex supply chain logistics for raw materials like polyvinyl alcohol and butyraldehyde. Key themes also include the application of predictive analytics in forecasting raw material price volatility and managing inventory, as well as AI's potential role in accelerating the research and development (R&D) cycle for novel PVB formulations, such as those integrated into smart windows or advanced ballistic glass. Concerns often focus on the required capital investment for implementing AI systems in traditional chemical manufacturing environments and the need for skilled labor to manage these highly automated processes, indicating a high user expectation for efficiency gains but cautiousness regarding implementation cost and complexity.

The dynamics of the PVB Film market are shaped by a complex interplay of driving forces, restraining factors, and promising opportunities, collectively defining the impact forces influencing market trajectories. A principal driver is the globally increasing emphasis on safety and security standards in both vehicle manufacturing and building codes, mandating the use of laminated glass in various applications. Coupled with this is the robust growth in the construction and automotive sectors, particularly in developing nations, fueling volume demand. Restraints, conversely, include the high price volatility of key raw materials, primarily commodity chemicals derived from oil and gas, which significantly impacts manufacturing costs and profit margins, forcing manufacturers to implement complex hedging strategies. Additionally, the challenge posed by alternative interlayer materials, although currently less dominant, provides potential substitution pressure, particularly for niche applications.

Opportunities within the market largely center on innovation and diversification of application areas. The transition towards electric and autonomous vehicles presents a significant avenue for growth, as these vehicles necessitate sophisticated glazing solutions for integrated sensors, improved cabin acoustics, and lighter weight construction materials. Furthermore, the burgeoning demand for specialized PVB films integrated into solar panels (photovoltaic modules) and high-end architectural projects, such as energy-efficient or smart glass installations, offers high-value revenue streams. These forces collectively dictate capital investment decisions, technological research priorities, and geographical market expansion strategies for all participants in the PVB supply chain.

The immediate impact forces are dominated by regulatory shifts and economic stability in major end-use markets. Regulatory tightening in regions like the European Union regarding energy efficiency and noise pollution ensures sustained demand for high-performance acoustic and thermal PVB films. Conversely, global economic slowdowns or severe disruptions in the petrochemical supply chain can exert immediate downward pressure on profitability and construction activity. Long-term market sustainability, however, hinges on continuous product innovation to maintain a competitive edge over alternatives and securing stable, cost-effective sources of raw materials, ensuring PVB remains the preferred interlayer for critical safety glass applications worldwide.

The PVB Film market is primarily segmented based on Type, Application, and End-Use, offering a granular view of market dynamics and product specialization. The Type segmentation distinguishes between standard PVB films, which are utilized for general safety and structural integrity purposes, and high-performance PVB films, which incorporate additives or specialized manufacturing processes to offer enhanced functional properties such as superior acoustic damping, increased thermal insulation (solar control), or advanced bullet and blast resistance. This high-performance segment is rapidly gaining traction due to increasing regulatory demands for energy-efficient buildings and quieter vehicle cabins, driving higher revenue growth despite lower volume compared to standard films.

The Application analysis reveals that the market heavily relies on the Automotive and Construction sectors. Automotive applications demand strict adherence to safety standards (e.g., ECE R43, ANSI Z26.1) and require high optical quality, especially for HUD integration. The Construction segment, which includes both residential and commercial buildings, dominates volume due to extensive use in windows, skylights, and protective barriers. A smaller but rapidly growing application is the Solar sector, where PVB film is used as an encapsulant for photovoltaic modules, valued for its durability and moisture resistance, ensuring the long-term operational integrity of solar panels.

The End-Use structure primarily targets laminated glass manufacturers, who serve as the direct purchasers, processing the film into final safety glass products for subsequent supply to Original Equipment Manufacturers (OEMs) in the automotive industry and general contractors/fabricators in the construction sector. Understanding the specific technical requirements of these lamination facilities—such as roll size, thickness uniformity, and pre-treatment needs—is crucial for PVB film suppliers. The strategic differentiation within segmentation lies in optimizing film properties to meet niche demands, such as extra-clear PVB for art conservation or specialized colors for architectural aesthetics, allowing suppliers to capture premium market share outside of commodity sales.

The PVB Film market value chain commences with the upstream analysis, primarily centered on the procurement and processing of raw materials. The crucial inputs are Polyvinyl Alcohol (PVOH), which is derived from Polyvinyl Acetate, and Butyraldehyde, typically sourced from petrochemical processes. Since these foundational chemicals are often supplied by large chemical conglomerates, the volatility in oil and gas prices significantly dictates the manufacturing costs for PVB resin producers. Efficiency in synthesizing the PVB resin through acetylation and careful management of purification stages are critical upstream activities that determine the quality, yield, and ultimately, the market price of the final PVB film product, necessitating strong relationships with reliable feedstock suppliers.

Midstream activities involve the conversion of PVB resin into the finished PVB film through extrusion and casting processes. Manufacturers must maintain high levels of technological sophistication to ensure precise film thickness, optimal adhesion properties, and, most critically, flawless optical clarity, especially for automotive and architectural applications. The distribution channel analysis shows a reliance on specialized logistics, ensuring the film is handled and stored correctly (often requiring controlled temperature and humidity) before reaching the downstream users—the laminated glass manufacturers. Direct distribution, often managed by major global producers, allows for better quality control and technical support, whereas indirect channels (agents and distributors) are frequently utilized for reaching smaller fabricators or penetrating complex emerging markets.

Downstream analysis focuses on the end-use applications and the direct buyers, which are predominantly the laminated glass fabricators. These customers integrate the PVB film between two or more layers of glass using heat and pressure (autoclave process) to produce safety glass. The final products are then sold to OEMs (e.g., automotive assembly lines) or construction project developers. The efficiency of the film—its ability to bond securely and its functional attributes (acoustic, thermal)—determines its perceived value downstream. The market structure is highly influenced by the technical requirements demanded by the end-users; for instance, automotive OEMs impose extremely stringent specifications, creating a high barrier to entry for film suppliers in that lucrative segment.

The primary potential customers and direct buyers within the PVB Film market are laminated glass manufacturers globally. These entities operate large-scale facilities dedicated to processing raw glass and PVB interlayers into finished safety glass products. Their purchasing decisions are heavily influenced by the film's technical specifications, including adhesion strength, optical properties, dimensional stability, and compliance with various international safety certifications (e.g., EN, ASTM, JIS). Since lamination is a highly energy-intensive process, the consistency and ease of processing of the PVB film directly impact their operational efficiency and waste reduction metrics, making reliability a critical factor in supplier selection.

Indirectly, the market serves major Original Equipment Manufacturers (OEMs) in the automotive industry and large-scale construction developers and glazing contractors. Automotive OEMs, such as General Motors, Volkswagen, and Toyota, specify the type and performance characteristics of the laminated glass required for their vehicles, influencing the demand curve for high-specification PVB films, particularly acoustic and thin, lightweight variants. As vehicles become increasingly reliant on heads-up displays (HUDs) and integrated sensors behind the windshield, the demand for ultra-high optical quality PVB films free from distortion or refraction issues escalates significantly, positioning these OEMs as the ultimate drivers of specialized product innovation.

Furthermore, major photovoltaic module manufacturers represent a growing customer segment, seeking PVB films specialized for solar encapsulation. Unlike architectural or automotive films, solar-grade PVB must offer superior moisture barrier properties and long-term UV resistance to protect the sensitive solar cells, ensuring a 25-year operational lifespan for solar panels. This shift towards renewable energy infrastructure globally positions solar encapsulation companies as a key, high-growth demographic for PVB suppliers focused on stability and durability in extreme environmental conditions, diversifying the potential customer base beyond traditional safety glass applications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $2.5 Billion |

| Market Forecast in 2033 | $4.0 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Kuraray, Eastman Chemical, Sekisui Chemical, Huakai Plastics, Chang Chun Group, KB PVB, Kingboard Holdings, Everlam, SAFY S.A., Huagong Tech, Wenzhou Decheng Plastic, Qilu Petrochemical, Sinopec, Zhejiang Decent New Material, Jiangsu Ruijia Chemical, Xiamen Laminated Materials, PVB Interlayer Technologies, Guangdong Junda New Material, VJ Interlayers, Chematur Engineering |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the PVB Film market is continuously evolving, focusing primarily on enhancing the functional performance characteristics of the laminated glass assembly while improving manufacturing efficiency. A core technology involves optimizing the extrusion and calendering process used to produce the film, ensuring exceptionally tight tolerances for thickness uniformity and surface smoothness. This process optimization is vital for minimizing optical distortion, a critical requirement for modern automotive glazing, especially those integrating advanced driver-assistance systems (ADAS) sensors and heads-up displays (HUDs). Furthermore, advancements in plasticizer technology are essential, as the type and concentration of plasticizer directly influence the film’s adhesion, flexibility, and acoustic dampening capabilities, driving the development of specialized acoustic-grade PVB films that absorb a wider range of sound frequencies.

Another significant technological focus is the development of multi-layer or composite PVB films designed for high-performance applications. This involves co-extrusion techniques that allow manufacturers to combine different polymers or specialized PVB layers to achieve dual functionality, such as enhanced structural stiffness coupled with superior thermal insulation. For instance, manufacturers are integrating additives that selectively block specific wavelengths of solar radiation (IR and UV) without compromising visible light transmission, creating energy-saving laminated glass for modern green buildings. The ongoing research into chemically modified PVB resins aims to improve resistance to moisture and heat, which is particularly relevant for PVB used in solar module encapsulation, ensuring product longevity in harsh environments.

Furthermore, automation and digital twin technology are increasingly being adopted in the production line. Advanced sensor technologies and process control systems are used to monitor and adjust extrusion parameters in real-time, drastically reducing scrap rates and ensuring consistency across large production volumes. The deployment of advanced analytical tools, often coupled with AI, for measuring molecular weight distribution and residual solvent levels provides unprecedented control over the final film properties. This technological push is moving the industry away from traditional batch processing toward continuous, highly automated manufacturing, securing better material traceability and enhancing compliance with the stringent quality standards required by global regulators and premium end-users.

The PVB Film Market exhibits distinct regional dynamics, with Asia Pacific (APAC) maintaining its position as the largest and fastest-growing region globally. This dominance is primarily attributed to rapid urbanization, massive infrastructural investments, and burgeoning automotive production, particularly in China and India. Government initiatives promoting green building certifications and increasing construction safety standards in densely populated cities necessitate the widespread adoption of laminated safety glass. Moreover, APAC is a key manufacturing hub for solar panels, driving significant demand for PVB as an encapsulant material. Local manufacturers are expanding production capacities to meet this regional demand, often focusing on high-volume, cost-effective standard-grade films, though demand for high-performance acoustic PVB is also escalating in urban centers.

Europe represents a highly mature and technologically advanced market, characterized by stringent environmental and safety regulations, such as mandatory use of safety glass in public buildings and a strong focus on energy efficiency (NZEB directives). The European market is a major consumer of specialized PVB films, particularly those offering superior acoustic and thermal performance to comply with regulations aimed at reducing building energy consumption and noise pollution. The automotive sector here drives innovation, focusing on thin, lightweight films essential for reducing the overall mass of premium vehicles and complying with CO2 emission targets, resulting in higher average selling prices for PVB products compared to the global average.

North America is characterized by robust demand stemming from the strong recovery in the residential construction market and the continued high safety standards mandated for all types of vehicles and buildings. The region faces unique demand drivers, notably the need for impact-resistant laminated glass in areas prone to severe weather events, such as hurricanes and tornadoes, boosting the demand for specialized heavy-duty PVB films. While the US and Canada have established manufacturing bases, the market is highly competitive, dominated by global majors who invest heavily in R&D to cater to specialized demands from the high-end architectural sector and the rapidly evolving electric vehicle manufacturing segment.

The primary applications driving demand are the Automotive industry, requiring PVB for safety windshields and acoustic side windows, and the Construction sector, utilizing laminated glass extensively in architectural glazing, safety barriers, and skylights for enhanced security and energy efficiency.

Price volatility in feedstocks like polyvinyl alcohol and butyraldehyde, which are petrochemical derivatives, significantly increases the operational costs for PVB manufacturers, potentially leading to fluctuating film prices and margin pressure across the entire value chain.

The Asia Pacific (APAC) region currently holds the largest market share, fueled by rapid urbanization, substantial growth in both automotive manufacturing and construction activities, and strong demand from the solar encapsulation industry, particularly in China.

Standard PVB film focuses on basic safety and adhesion, while high-performance PVB films are specialized variants engineered with additives or multilayer structures to provide superior functional attributes, such as enhanced acoustic damping, thermal insulation, or increased ballistic resistance.

While PVB remains the dominant interlayer material, materials like ethylene vinyl acetate (EVA) and specialized ionoplast interlayers (e.g., SentryGlas) are emerging as alternatives, particularly in applications requiring extreme structural rigidity or higher resistance to moisture and temperature extremes.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.