ID : MRU_ 433163 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

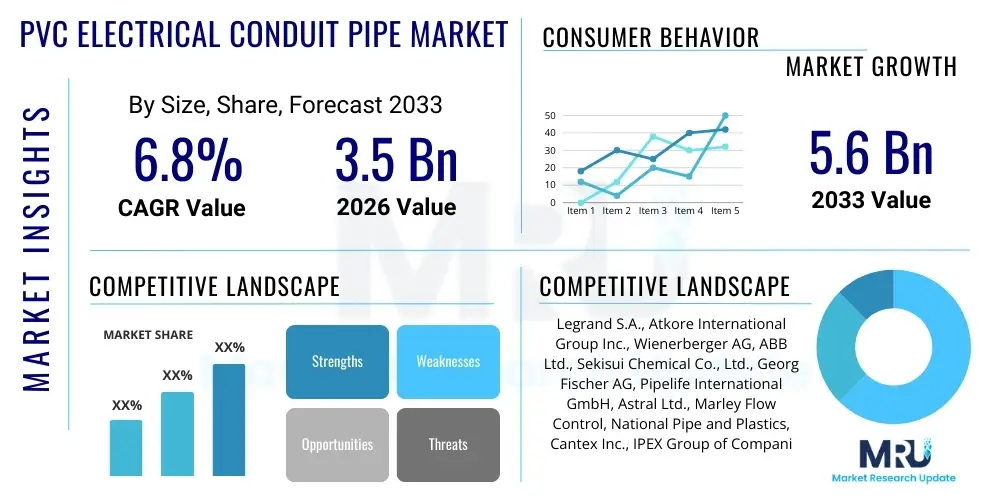

The PVC Electrical Conduit Pipe Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 3.5 Billion in 2026 and is projected to reach USD 5.6 Billion by the end of the forecast period in 2033.

The PVC Electrical Conduit Pipe Market encompasses the manufacturing, distribution, and utilization of polyvinyl chloride (PVC) pipes specifically designed to encase and protect electrical wiring and cables in various structural applications. These conduits are integral components of modern electrical infrastructure, ensuring safety, durability, and ease of maintenance for wiring systems in residential, commercial, and industrial settings. PVC is preferred due to its inherent properties, including corrosion resistance, high dielectric strength, non-conductivity, and self-extinguishing characteristics, which are critical for electrical safety standards worldwide. The market trajectory is heavily influenced by global construction spending and the ongoing need for safer and more efficient electrical installations, particularly in developing economies undergoing rapid urbanization.

PVC conduit pipes are utilized across major applications ranging from infrastructure projects like bridges and tunnels to vertical construction such as high-rise office buildings and data centers. The primary function is to shield conductors from physical impact, moisture, chemical exposure, and temperature fluctuations, thereby extending the lifespan of the electrical system and minimizing fire hazards. The versatility of PVC allows for the production of different types, including rigid conduits (most common) and flexible conduits, catering to diverse installation requirements and environmental conditions. Standardization efforts and stringent building codes continually shape product demand, pushing manufacturers towards enhanced compliance and quality assurance.

Key driving factors supporting market expansion include robust governmental investments in smart city projects and essential infrastructure refurbishment. The continuous replacement cycles of aging metallic conduit systems with lighter, easier-to-install, and cost-effective PVC alternatives further bolster demand. Moreover, the increasing adoption of renewable energy sources, such as solar and wind power, requires extensive new cabling infrastructure, where PVC conduits are essential for managing and protecting power lines connecting generation sites to the grid. The inherent benefits of PVC—low cost, longevity, and resistance to environmental degradation—make it the material of choice for large-scale electrical protective systems.

The PVC Electrical Conduit Pipe market is characterized by stable growth driven primarily by accelerated global construction activities, particularly in the residential and commercial sectors across Asia Pacific and the Middle East. Business trends highlight a strong emphasis on product innovation focusing on fire retardancy, low smoke zero halogen (LSZH) variants, and pre-wired conduit solutions to enhance installation efficiency and meet evolving safety regulations. Manufacturers are increasingly integrating digitalization into their supply chains to optimize production and manage the volatility in PVC resin prices, a key determinant of final product cost. Strategic partnerships between raw material suppliers and large-scale construction firms are emerging as a critical competitive edge.

Regionally, the Asia Pacific dominates the market share due to substantial governmental support for infrastructure development and massive urbanization waves in countries like India and China. North America and Europe maintain steady growth, largely spurred by renovation projects, stringent safety regulations necessitating system upgrades, and the increasing complexity of data center infrastructure build-outs requiring specialized conduit systems. Conversely, Latin America and Africa offer high growth potential, driven by rapid industrialization and improving access to reliable electricity, translating to high demand for foundational electrical protection products.

Segmentation trends indicate that the rigid PVC conduit type holds the largest market segment due to its widespread use in standard construction and underground applications requiring high impact resistance. In terms of application, the residential sector remains the largest consumer, although the industrial and commercial segments are witnessing faster expansion due to large-scale facility construction and mandatory safety compliance. The increasing preference for specialized fittings and connectors that reduce installation time and enhance system integrity is also a notable segment trend influencing product development strategies across major market players.

Users frequently inquire about how Artificial Intelligence (AI) and machine learning (ML) are being integrated into the PVC conduit manufacturing process, focusing specifically on optimizing material use, improving quality control, and automating production planning. Key themes center on predictive maintenance for extrusion machinery, smart inventory management to mitigate supply chain disruptions linked to PVC resin volatility, and the potential for AI-driven design optimization to create more efficient and lighter conduit geometries. Concerns often revolve around the initial investment required for AI infrastructure and the need for specialized personnel to manage these advanced systems within traditionally conservative manufacturing environments.

The immediate impact of AI is less visible in the final product itself but profoundly affects operational efficiency. AI algorithms are being deployed to analyze real-time data from extrusion lines, predicting potential equipment failures before they occur, thus minimizing downtime and maximizing throughput. Furthermore, ML models are utilized for complex quality assurance, automatically inspecting conduits for dimensional defects or material irregularities at speeds unattainable by human inspectors. This enhancement in precision and speed ensures higher compliance with international standards and reduces waste, contributing positively to sustainability goals and profit margins.

Over the forecast period, AI is expected to transform logistics within the PVC conduit sector. Predictive analytics can forecast demand fluctuations based on complex macroeconomic indicators and regional construction permits, allowing manufacturers to adjust production schedules dynamically. This capability minimizes overstocking and stockouts, particularly crucial for bulky, low-margin products like conduits. Ultimately, AI serves as an efficiency accelerator, driving down the unit cost of manufacturing and distribution, thereby indirectly stabilizing prices for end-users and reinforcing the competitiveness of PVC conduits against alternative materials.

The market dynamics are governed by a complex interplay of Drivers (D), Restraints (R), and Opportunities (O), which collectively define the Impact Forces influencing market growth. The primary drivers stem from infrastructural development and the inherent cost-effectiveness of PVC. Conversely, fluctuations in the cost of raw PVC resin, coupled with increasing environmental scrutiny regarding plastic usage, present significant restraints. The market is propelled forward by the opportunity for manufacturers to innovate in fire safety standards and penetrate rapidly developing non-residential construction markets.

The core drivers center on the global imperative for electrical safety upgrades and the sustained growth in emerging economies. PVC conduits offer a superior combination of insulation, non-corrosive properties, and ease of installation compared to traditional metal alternatives, making them highly attractive for large-scale, cost-sensitive projects. However, the market faces significant headwinds from the volatility of crude oil prices, which directly impacts PVC resin costs. Furthermore, legislative pressure in mature markets, favoring non-plastic materials or demanding highly specialized, eco-friendly variants (such as bio-based PVC), acts as a constraint, forcing costly research and development investments.

Impact forces are currently leaning toward positive growth, primarily due to the undeniable necessity of electrical protection in urbanization. Opportunities lie in developing high-performance conduits, such as those with antimicrobial or enhanced chemical resistance properties for specialized industrial applications (e.g., healthcare facilities and food processing plants). Furthermore, the push towards pre-fab construction techniques creates a niche for pre-installed, flexible PVC conduit systems, enhancing efficiency on construction sites. Manufacturers strategically addressing sustainability concerns through recycling initiatives and material substitution will capture long-term market leadership.

The PVC Electrical Conduit Pipe market segmentation provides a comprehensive view of consumption patterns based on product type, diameter, application, and end-user. This layered approach is critical for stakeholders to identify high-growth niches and tailor their product offerings and marketing strategies effectively. The market is primarily segmented based on the rigidity of the pipe, dividing it into rigid and flexible conduits, each serving distinct functional purposes and installation environments. Further refinement by diameter allows manufacturers to address specific current-carrying capacity requirements, ranging from small residential wiring to heavy industrial feeders.

Application-wise, the segmentation distinguishes between above-ground and underground installations, reflecting different regulatory requirements and environmental stresses. For instance, underground conduits require higher compression strength and UV stability. The end-user analysis is perhaps the most crucial segmentation dimension, categorizing demand generated by residential, commercial, and industrial construction. The residential sector typically demands standard, cost-effective solutions, while commercial spaces (e.g., offices, retail) demand enhanced fire safety features, and industrial settings require specialized chemical or heat-resistant properties.

The ongoing trend towards smart buildings and advanced electrical systems is creating sub-segmentation demand for specialized, color-coded conduits used for data transmission and low-voltage applications separate from power wiring. Analyzing these segmented demands allows manufacturers to allocate resources efficiently, focusing on geographic regions or end-user groups exhibiting the highest projected Compound Annual Growth Rates. Understanding these segments is vital for competitive positioning, particularly in regions where governmental standards dictate specific segment adoption, such as mandatory use of fire-retardant conduits in public buildings.

The value chain for the PVC Electrical Conduit Pipe market begins with upstream activities, primarily the sourcing and manufacturing of Polyvinyl Chloride (PVC) resin, which is derived from petrochemical processes (ethylene) and chlorine. This stage is critical as the quality and cost volatility of PVC resin directly impact the profitability of the downstream conduit manufacturers. Key players in the upstream segment include major petrochemical corporations and resin producers. Efficiency in this stage relies heavily on optimizing polymerization processes and maintaining stable pricing amid global oil market fluctuations.

The middle segment involves the transformation process where conduit manufacturers purchase the resin, stabilizers, plasticizers, and flame retardants, and utilize extrusion technology to form the final pipe product. This manufacturing step involves significant capital expenditure on machinery and requires adherence to strict dimensional and safety standards (e.g., UL, CSA, IEC). Distribution channels form the immediate downstream activity, encompassing a complex network of wholesalers, distributors, specialized electrical supply houses, and direct sales to large construction contractors or governmental bodies. The efficiency of this distribution network is crucial for timely delivery and market reach.

Direct channels usually involve large-volume sales to major infrastructure projects or Original Equipment Manufacturers (OEMs), providing better margins but requiring dedicated logistics. Indirect channels, relying on distributors and retailers, ensure pervasive market presence, reaching smaller contractors and repair/maintenance markets. End-users, including electricians, contractors, and builders, represent the final consumption point. The competitiveness of a company is often determined by its ability to manage supply chain risks upstream while maintaining a highly responsive and broad distribution network downstream, optimizing inventory management across the entire chain.

The potential customer base for PVC Electrical Conduit Pipes is diverse, encompassing various sectors fundamentally involved in new construction, renovation, and maintenance of electrical infrastructure. The largest group of customers consists of Electrical Contractors (ECs) and general contractors responsible for executing residential, commercial, and industrial construction projects. These customers prioritize product availability, ease of installation (e.g., lightweight, easy cutting), compliance with local building codes, and overall cost-effectiveness, often procuring materials through established supply house networks.

Another significant segment comprises large-scale Developers and Real Estate Investment Trusts (REITs) engaged in continuous large-scale housing or commercial developments, such as planned communities or corporate campuses. These buyers typically enter into long-term procurement agreements directly with manufacturers or major distributors to secure consistent quality and volume pricing. For them, long-term durability, fire safety ratings, and the standardization of products across multiple sites are paramount considerations, driving demand for premium and certified rigid conduits.

Furthermore, Utility Companies and Government Agencies constitute a highly strategic customer group, especially those involved in public infrastructure projects like road lighting, underground power distribution, telecommunication network expansion, and municipal facility upgrades. These entities demand products meeting the highest levels of durability, resistance to chemical and environmental stress, and compliance with national standards (e.g., burial grade conduits). Finally, specialized industrial end-users, such as data center operators, chemical processing plants, and manufacturing facilities, represent a niche segment demanding high-performance conduits with enhanced specifications like anti-static or extreme temperature resistance.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 5.6 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Legrand S.A., Atkore International Group Inc., Wienerberger AG, ABB Ltd., Sekisui Chemical Co., Ltd., Georg Fischer AG, Pipelife International GmbH, Astral Ltd., Marley Flow Control, National Pipe and Plastics, Cantex Inc., IPEX Group of Companies, Prime Conduit, Allied Tube & Conduit (Atkore), Diamond Plastics, JM Eagle, Zekelman Industries, Precision Pipes & Profiles Co. (PPPC), Mexichem (Orbia), Polypipe Group plc |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The manufacturing technology landscape for PVC electrical conduits is primarily dominated by advanced extrusion processes. Modern extrusion lines incorporate sophisticated automation and precision temperature control systems to ensure consistent wall thickness, high impact resistance, and precise internal diameters, which are critical for smooth wire pulling. Multi-layer co-extrusion technology is increasingly being adopted to produce conduits with specialized inner or outer layers, such as low-friction linings to aid installation or UV-resistant outer coatings for prolonged outdoor exposure, enhancing product performance beyond standard PVC offerings.

A key technological focus area is compound formulation. Manufacturers are heavily investing in proprietary blends and additives to meet stringent safety standards, particularly concerning fire resistance. The development and integration of Low Smoke Zero Halogen (LSZH) compounds represent a significant technological advancement. While traditional PVC can release toxic fumes during a fire, LSZH conduits are designed to produce minimal smoke and no toxic halogens, addressing the rising safety mandates in enclosed spaces like tunnels, hospitals, and high-rise buildings. This requires specialized mixing and processing equipment to handle these higher-end polymeric compounds effectively.

Furthermore, integration technologies are gaining traction, including automated bundling, specialized coupling design (e.g., solvent-cement systems and push-fit connections), and pre-wired conduit systems. Push-fit technology reduces reliance on chemical bonding agents and speeds up installation time significantly, appealing directly to labor-intensive construction markets. Digitalization, including the integration of sensors and AI monitoring on the factory floor, represents the continuous technological evolution, focusing less on the product material itself and more on optimizing manufacturing consistency, quality control, and overall operational efficiency.

The global PVC Electrical Conduit Pipe market exhibits significant regional disparities in growth rate, maturity, and regulatory environments, influencing material specifications and demand patterns.

The PVC Electrical Conduit Pipe Market is projected to exhibit a steady Compound Annual Growth Rate (CAGR) of 6.8% between the years 2026 and 2033, driven largely by sustained global construction activities and infrastructure investment, particularly in developing economies.

Rigid PVC conduits are used for straight runs and exposed wiring protection requiring high impact resistance, common in underground and commercial fixed installations. Flexible PVC conduits are used where wiring requires movement, frequent bending, or complex routing, such as connecting fixed equipment to a junction box.

The Asia Pacific (APAC) region currently dominates the global market share. This dominance is attributed to rapid urbanization, massive government investment in utility and residential infrastructure, and the high volume of new construction projects across countries like China and India.

The market is highly sensitive to the price of PVC resin, which is a petrochemical derivative. Volatility in crude oil prices directly impacts resin costs, leading to pressure on profit margins for manufacturers and potential price instability for end-users, affecting project budgeting.

Yes, key innovations include the shift toward Low Smoke Zero Halogen (LSZH) compounds to enhance fire safety and reduce toxic emissions. Additionally, manufacturers are investing in PVC recycling programs and research into bio-based PVC formulations to address growing environmental concerns and regulatory mandates.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.