ID : MRU_ 436500 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

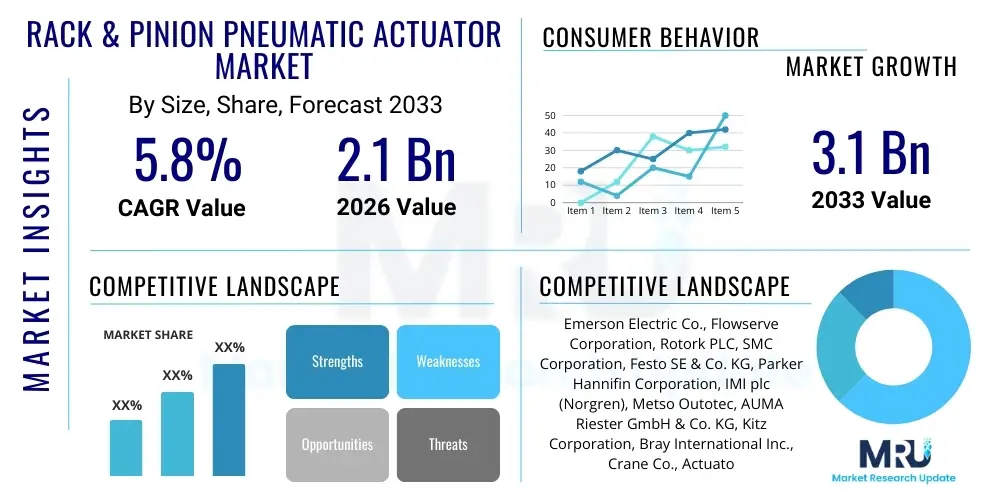

The Rack & Pinion Pneumatic Actuator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 2.1 Billion in 2026 and is projected to reach USD 3.1 Billion by the end of the forecast period in 2033.

The Rack & Pinion Pneumatic Actuator Market encompasses devices that use compressed air (pneumatic energy) to convert linear motion (the rack and piston) into rotary motion (the pinion gear) for operating industrial valves, such as ball, butterfly, and plug valves, or dampers. These actuators are foundational components in fluid control systems across nearly all industrial sectors due to their inherent simplicity, high torque-to-weight ratio, and robust operational capabilities, especially in hazardous or explosive environments where electric devices pose risks. The primary function of these actuators is to provide precise and rapid control over fluid flow, pressure, and temperature within complex process pipelines.

The core product offering is defined by its mechanism: air pressure drives pistons, which move racks engaging a central pinion, resulting in 90-degree or 180-degree rotation. Key product variations include Double Acting actuators, which require air pressure for both opening and closing strokes, and Spring Return (Single Acting) actuators, which use compressed air for one stroke and springs for the default fail-safe position. Major applications are concentrated in critical infrastructure and process industries where reliability and speed are paramount. Benefits such as low cost, ease of maintenance, and intrinsic safety continue to drive their adoption, particularly in large-scale chemical processing and oil and gas transportation.

Market growth is predominantly fueled by the global acceleration of industrial automation, coupled with significant infrastructural investments in water treatment and power generation facilities, particularly across developing economies in Asia Pacific. Furthermore, the mandatory upgrade and replacement cycles in mature markets like North America and Europe, driven by stringent safety regulations and the need for enhanced energy efficiency, support sustained demand. The integration of advanced materials to improve operational lifespan and the modular design allowing for easy integration with positioners and limit switches are also critical driving factors influencing market expansion and technological innovation.

The global Rack & Pinion Pneumatic Actuator Market is currently undergoing a strategic transformation characterized by increasing demand for highly reliable, robust, and smart pneumatic systems capable of integrating seamlessly into Industry 4.0 architectures. Business trends indicate a strong focus on modular designs and standardization, allowing manufacturers to serve diverse industrial applications with fewer components, thereby reducing production costs and enhancing supply chain resilience. Regionally, the Asia Pacific market is emerging as the dominant growth engine, driven by massive expansions in the chemical, pharmaceutical, and construction sectors, necessitating extensive new pipeline infrastructure and associated flow control components. Conversely, established markets in North America and Europe are witnessing steady demand primarily due to maintenance, repair, and overhaul (MRO) activities and the replacement of older, less efficient units to comply with stricter environmental and safety standards.

Segment trends reveal that the Spring Return actuator configuration holds substantial market share due to its inherent fail-safe functionality, which is mandatory in numerous safety-critical applications across the oil and gas and power generation industries. However, the Double Acting segment is projected to experience slightly faster growth, largely driven by applications requiring precise bidirectional control and higher operating speeds, such as complex mixing and batch processes in the chemical sector. Furthermore, the end-user segmentation highlights the continuous prominence of the Chemical and Oil & Gas industries as the largest consumers, though the Water & Wastewater segment is showing accelerated adoption rates fueled by global urbanization and the resultant need for sophisticated municipal treatment facilities.

From a competitive standpoint, market players are increasingly investing in proprietary coating technologies and composite materials to enhance actuator performance in highly corrosive or high-temperature environments, extending mean time between failures (MTBF). Strategic partnerships aimed at integrating advanced position sensing and diagnostic capabilities into standard pneumatic packages are key to capturing market share. The move towards digitalization means that while the core mechanism remains pneumatic, the control interface is becoming increasingly electronic and networked, ensuring data transparency and enabling predictive maintenance strategies, ultimately shaping the competitive landscape over the forecast period.

User queries regarding the impact of Artificial Intelligence (AI) on the Rack & Pinion Pneumatic Actuator Market frequently revolve around two main areas: how AI can enhance the operational efficiency and predictive maintenance capabilities of these traditionally mechanical components, and whether AI-driven systems could lead to the displacement of pneumatic technology by advanced electric actuators. Analysis reveals that users are primarily interested in applying machine learning algorithms to analyze compressed air consumption patterns, valve positioning data, and actuator performance metrics (such as cycle time and torque output). The central concern is leveraging AI to transition from scheduled maintenance to condition-based and predictive maintenance, thereby minimizing costly downtime and optimizing energy usage. Expectations center on AI facilitating the identification of subtle mechanical degradation or air leakage well before catastrophic failure occurs, thereby maximizing the lifespan and reliability of the pneumatic system without fundamentally altering the robust mechanical architecture of the rack & pinion design itself.

The Rack & Pinion Pneumatic Actuator Market is shaped by a robust interplay of Drivers (D), Restraints (R), Opportunities (O), and potent Impact Forces. Key drivers include the pervasive adoption of automation in processing industries globally, particularly driven by Industry 4.0 initiatives which require reliable, fast-acting flow control devices. The inherent safety features of pneumatic systems—being spark-free and explosion-proof—make them indispensable in hazardous environments, such as chemical plants and offshore platforms, providing continuous demand irrespective of economic fluctuations. Furthermore, increasing investment in large-scale infrastructure projects, specifically in municipal water treatment and new power generation facilities (including gas and hydrogen), mandates the deployment of thousands of control valves, directly fueling actuator sales. The low initial cost and relatively simple installation procedures compared to complex electric servo systems also act as a significant market accelerant.

However, the market faces notable restraints, most prominently the competition from advanced electric actuators, which offer superior precision, higher energy efficiency, and easier integration into digital control networks without requiring extensive compressed air infrastructure. Another significant constraint is the necessity of constant maintenance associated with pneumatic systems, particularly dealing with air leaks, which results in energy wastage and higher long-term operational costs. Furthermore, limitations in achieving highly accurate, continuous modulation required in highly specialized control loops often favor electro-hydraulic or electric servo solutions over standard pneumatic actuators, restricting the growth potential in highly specialized niche applications.

Opportunities for growth are concentrated in the development of "smart pneumatics," incorporating integrated sensors and IO-Link capabilities to provide real-time performance diagnostics and seamless communication with central control systems (DCS/SCADA). The market also benefits substantially from the rising adoption of specialized materials (e.g., polymer-based components and sophisticated coatings) designed to withstand increasingly harsh process media, extending the life cycle of actuators in corrosive environments. Geographically, emerging economies offer vast untapped potential for both new installations and modernization projects. The primary impact forces driving competition include rapid technological convergence between pneumatic control and digital intelligence, shifting buyer preference towards total cost of ownership (TCO) rather than just initial purchasing price, and stringent industry regulations demanding faster, more reliable fail-safe mechanisms.

The Rack & Pinion Pneumatic Actuator Market is extensively segmented based on key structural and application parameters, providing a granular view of market dynamics and adoption patterns across diverse industrial landscapes. The primary structural segmentation relies on the operating principle—Double Acting versus Spring Return—reflecting the operational requirements regarding energy usage and fail-safe protocols. Further segmentation based on application highlights the critical role these actuators play in flow control within sectors ranging from highly sensitive pharmaceutical manufacturing to robust, large-scale crude oil processing. Analyzing these segments is essential for manufacturers to tailor product specifications, focusing on torque output, operating pressure capacity, and material compatibility to meet specific industry demands.

The value chain for the Rack & Pinion Pneumatic Actuator Market begins with crucial upstream activities centered on the procurement and processing of raw materials. This includes high-grade aluminum alloys for housing and bodies due to their lightweight and corrosion resistance, specialized synthetic polymers for seals and bearings to ensure smooth operation and durability, and precision steel for the rack and pinion gears. Suppliers of these materials and components—such as metal foundries, plastic injection molders, and specialized spring manufacturers—form the backbone of the upstream segment. Quality control and standardization of material inputs are paramount at this stage, as they directly influence the actuator's performance lifespan and compliance with industry standards like ATEX or SIL ratings.

The core manufacturing process involves precision machining, assembly, testing, and certification. Manufacturers convert raw materials into finished actuators, incorporating advanced surface treatments (like anodizing) to enhance corrosion resistance, especially for actuators destined for marine or chemical environments. This phase often involves significant capital expenditure in automated CNC machining centers and clean-room assembly lines. The distribution channel is bifurcated: Direct sales are common for large volume, customized orders involving major EPC (Engineering, Procurement, and Construction) firms or major oil and gas operators. Indirect distribution relies heavily on a network of specialized industrial distributors, system integrators, and local representatives who provide localized inventory, technical support, and value-added services such as valve-actuator coupling, servicing the vast Maintenance, Repair, and Overhaul (MRO) market.

The downstream segment concludes with the end-users and installation services. System integrators play a critical role, selecting the appropriate actuator size and torque for specific valves and installing them within the larger plant control system (DCS). Post-sales service, including commissioning, scheduled maintenance, and spare parts supply, completes the value circle. The efficiency and reliability of the indirect distribution network are critical for market penetration, as regional distributors often possess the necessary expertise to troubleshoot and maintain complex fluid control systems, creating a barrier to entry for smaller manufacturers who lack this expansive service infrastructure.

Potential customers for the Rack & Pinion Pneumatic Actuator Market are diverse yet concentrated primarily within heavy process industries where fluid management is essential to operations. The largest and most consistent buyers are Original Equipment Manufacturers (OEMs) of industrial valves (ball, butterfly, plug valves) and dampers, who integrate these actuators as a component of their final flow control package. This includes companies supplying control systems to power plants, water utilities, and large-scale manufacturing facilities. Their purchasing decisions are driven by standardization, robust performance specifications, and competitive pricing for high volumes, often leading to long-term supply agreements with actuator manufacturers.

The next major customer base comprises large end-users, specifically plant owners and operators in the Oil & Gas, Chemical, and Petrochemical sectors. These companies utilize actuators in mission-critical applications where failure is costly and hazardous. Their demand is split between new construction projects (capex) and MRO activities (opex), focusing heavily on products with high safety integrity level (SIL) ratings and materials designed for extreme operating conditions (high temperature, corrosive media). Reliability, compliance with global safety standards, and ease of field maintenance are paramount considerations for this customer group.

Furthermore, municipal and private entities involved in Water and Wastewater Treatment represent a rapidly growing customer segment. As global urbanization stresses existing infrastructure, new treatment plants and pipeline networks require thousands of quarter-turn actuators for controlling flow and mixing chemicals. These buyers prioritize durability, corrosion resistance (especially in chlorine and ozone environments), and low energy consumption. System Integrators and Engineering, Procurement, and Construction (EPC) firms act as key intermediaries, specifying and procuring actuators on behalf of these ultimate end-users, requiring manufacturers to maintain rigorous quality control and comprehensive documentation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 2.1 Billion |

| Market Forecast in 2033 | USD 3.1 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Emerson Electric Co., Flowserve Corporation, Rotork PLC, SMC Corporation, Festo SE & Co. KG, Parker Hannifin Corporation, IMI plc (Norgren), Metso Outotec, AUMA Riester GmbH & Co. KG, Kitz Corporation, Bray International Inc., Crane Co., Actuators & Controls S.r.l., Habonim Industrial Valves & Actuators, Swagelok Company, Burkert Fluid Control Systems, Pentair plc, Assured Automation, Valbia S.r.l., Bonomi Group. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Rack & Pinion Pneumatic Actuator Market is characterized not by radical changes to the core mechanical principle, but by significant advancements in material science, digitalization, and modular integration. Modern actuator manufacturers are heavily focused on developing high-performance surface coatings, such as specialized epoxy paints or polytetrafluoroethylene (PTFE) linings, which significantly improve resistance to harsh external environments, extending the operational life in corrosive environments like coastal regions or chemical processing plants. Furthermore, the use of advanced polymer seals and bearings replaces traditional components, reducing internal friction, improving air efficiency, and decreasing the requirement for lubrication, moving towards 'fit and forget' designs and minimizing maintenance complexity.

Digitalization represents the most transformative technological shift. While the actuator remains pneumatic, its control interface is rapidly evolving. The integration of high-resolution sensors and IO-Link communication protocols allows these mechanical devices to function as smart assets within the Industrial Internet of Things (IIoT). These integrated sensors monitor key performance indicators (KPIs) such as cycle count, ambient temperature, air supply pressure fluctuations, and precise valve position (using advanced proximity or magnetic sensors). This rich, real-time data output enables plant operators to implement sophisticated predictive maintenance routines, maximizing uptime and overall equipment effectiveness (OEE).

Another crucial trend is modularity and standardization. Manufacturers are moving towards designing actuator lines that use common platforms and interchangeable internal components. This approach simplifies inventory management for both the manufacturer and the end-user, reduces manufacturing complexity, and allows for rapid customization for specific torque requirements or operational pressures. The development of quick-exhaust valves and advanced solenoid interfaces that improve switching speeds is also crucial, enabling the use of pneumatic actuators in applications previously dominated by faster but more complex solenoid-operated valves, particularly in high-speed bottling and packaging industries, thereby broadening the market application base for the rack & pinion design.

The global demand for Rack & Pinion Pneumatic Actuators exhibits distinct regional consumption patterns dictated by industrial maturity, regulatory frameworks, and infrastructural investment cycles.

The primary driver is the intrinsic safety advantage of pneumatic actuators, which are inherently spark-free and explosion-proof, making them mandatory for use in hazardous, high-risk environments common in the oil, gas, and chemical processing industries where electric motors pose ignition risks.

The chief maintenance challenge is managing compressed air infrastructure, specifically addressing air leakage, which leads to significant energy waste and requires regular inspection of seals, fittings, and air preparation units (filters, regulators, lubricators).

The Asia Pacific (APAC) region is projected to exhibit the highest CAGR, primarily fueled by massive infrastructural build-out, rapid industrial expansion, and high-volume demand from new chemical, pharmaceutical, and water treatment facility construction projects.

Integration is achieved through the adoption of "smart pneumatics," which includes incorporating integrated sensors and IO-Link communication modules to enable real-time condition monitoring, precise position feedback, and data transmission for predictive maintenance systems.

Double Acting actuators are used when precise, high-speed bidirectional control is needed. Spring Return (Single Acting) actuators are deployed in critical applications requiring a guaranteed fail-safe position (either fail-open or fail-close) in the event of an air pressure or power loss.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.