ID : MRU_ 438115 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

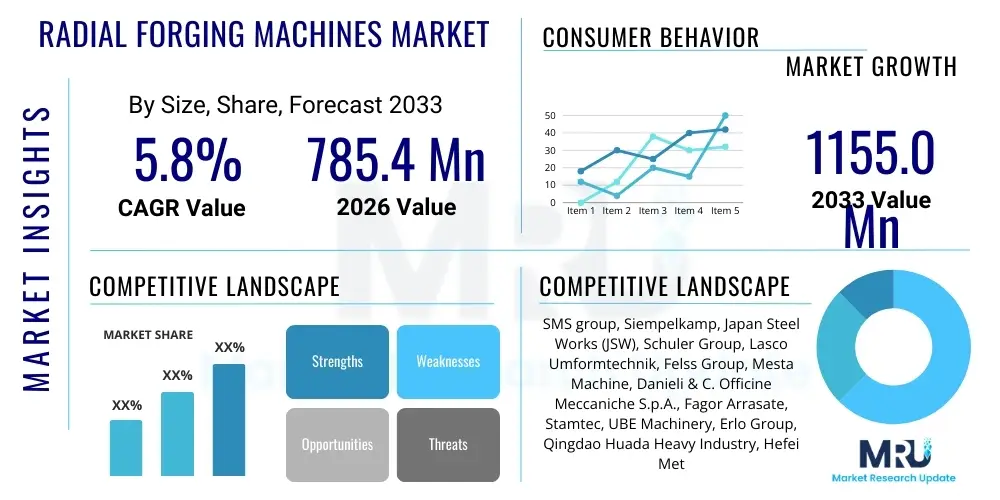

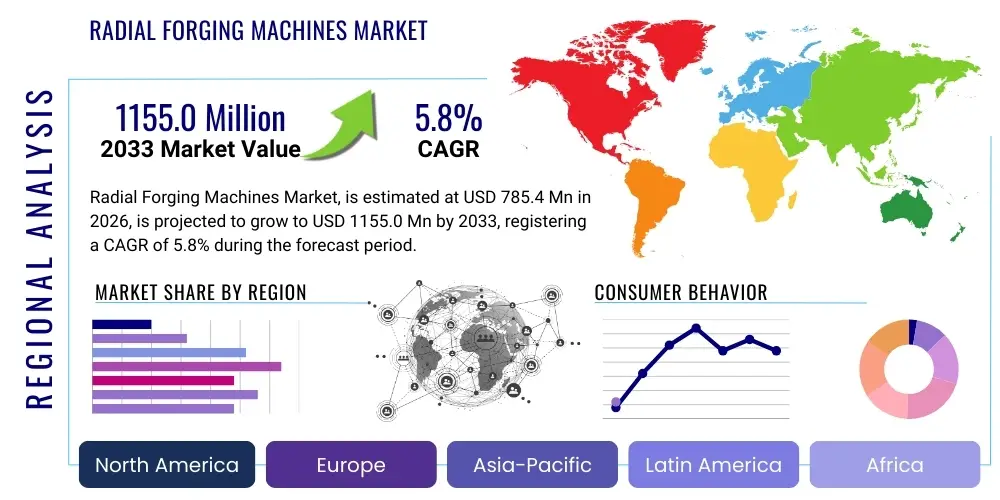

The Radial Forging Machines Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 785.4 Million in 2026 and is projected to reach USD 1155.0 Million by the end of the forecast period in 2033.

The Radial Forging Machines Market encompasses specialized industrial equipment designed for incrementally shaping metal workpieces, typically into long, axisymmetric components such as shafts, tubes, and stepped axles. These machines utilize multiple forging hammers (often two or four) arranged radially around the workpiece, applying high-frequency, synchronized blows to achieve precise dimensional control and superior material microstructures. Radial forging, also known as rotary forging or swaging, is a highly efficient process that minimizes material waste, particularly when working with expensive alloys used in critical applications. The market expansion is intrinsically linked to the robust growth of industries demanding high-performance, structurally sound components, ensuring that the final products possess high fatigue strength and favorable grain flow characteristics essential for safety and longevity.

Product descriptions of modern radial forging machines emphasize automation, precision control via CNC systems, and the capacity to handle challenging materials like titanium, nickel-based superalloys, and specialized steel grades. Major applications span several capital-intensive sectors, including aerospace for manufacturing engine shafts and landing gear components, automotive for steering columns and axles, oil and gas for drill pipes and downhole tools, and power generation for turbine rotors and generator shafts. The ability of radial forging to produce components close to net shape reduces subsequent machining time and cost, enhancing overall manufacturing efficiency. These machines are increasingly integrated with advanced monitoring systems that ensure real-time adjustments to forging parameters, contributing to zero-defect manufacturing goals.

The primary driving factors propelling the market include the escalating global demand for fuel-efficient and structurally optimized vehicles, necessitating lightweight forged components in the automotive sector, particularly for electric vehicle (EV) drivetrains. Furthermore, stringent regulatory standards in the aerospace and energy sectors mandate the use of materials processed under highly controlled deformation conditions, which radial forging inherently provides. Benefits derived from utilizing these machines include significant improvement in material strength and ductility, superior surface finish, and substantial energy savings compared to open die or large closed die forging operations. Continued innovation in machine design, focusing on higher tonnage capacity and greater operational flexibility, ensures the sustained relevance and growth trajectory of the Radial Forging Machines Market over the forecast period.

The Radial Forging Machines Market is characterized by steady technological advancements focused on increased automation and integration with Industry 4.0 principles, driving current business trends. Major manufacturers are shifting towards developing hybrid machines capable of performing both cold and hot forging operations, offering end-users greater versatility in material processing. Strategic alliances between forging equipment manufacturers and material suppliers are becoming commonplace to optimize machine parameters for novel high-temperature and refractory alloys. Business growth is strongly correlated with capital expenditure cycles in the aerospace and defense sectors, which rely heavily on high-integrity components produced by these specialized machines, leading to resilient demand even amidst short-term economic fluctuations.

Regionally, Asia Pacific (APAC) dominates the market in terms of volume and is projected to exhibit the highest growth rate, primarily fueled by massive infrastructure development, burgeoning domestic automotive production, and increased investment in advanced manufacturing capabilities in countries such as China, India, and South Korea. North America and Europe, while mature markets, maintain a strong foothold due to high demand from the specialized aerospace and power generation industries, focusing more on high-value, high-precision radial forging systems rather than sheer volume. Regional trends also show a move towards localized maintenance support and faster deployment cycles to reduce downtime, pushing global suppliers to establish stronger local operational footprints and specialized service networks across key geographies.

In terms of segment trends, the market categorized by the number of hammers shows that the four-hammer configuration segment holds the largest market share due to its superior capability in precise dimensional control and rapid processing of complex profiles. Based on application, the automotive and aerospace segments remain the largest consumers, though the oil and gas segment is showing resurgence driven by demand for advanced, corrosion-resistant drill string components requiring excellent internal structure uniformity. Furthermore, the segmentation by machine type indicates a growing preference for hydraulic radial forging machines over mechanical types, owing to the enhanced control over forging force and stroke precision offered by hydraulic systems, which is crucial for modern high-specification component manufacturing.

User queries regarding the intersection of Artificial Intelligence (AI) and the Radial Forging Machines Market commonly revolve around themes of predictive maintenance, process optimization, and quality assurance. Key concerns center on how AI can enhance the accuracy of force prediction during forming, minimize material defects like cracks or non-uniform grain flow, and ultimately reduce the reliance on highly skilled operators. Users are keenly interested in leveraging AI-driven analytics to move from traditional reactive maintenance schedules to proactive, condition-based monitoring, anticipating component failure long before it occurs. Expectations are high that AI will provide real-time feedback loops to CNC controllers, allowing the machine to dynamically adjust parameters such as hammer velocity and feed rate based on material property fluctuations observed during the forging process itself, thereby maximizing yield and component reliability.

The primary technological impact of AI will materialize through the implementation of machine learning algorithms trained on massive datasets covering temperature profiles, strain rates, and resultant microstructure data. This enables the creation of highly accurate digital twins of the forging process, allowing manufacturers to simulate complex material flow and predict final mechanical properties without extensive physical prototyping. Such integration is essential for handling increasingly complex geometries and novel high-strength, low-ductility materials. Furthermore, AI systems are expected to streamline the initial setup and calibration phases, significantly reducing the lead time for new product introduction, especially in high-mix, low-volume production environments typical of aerospace component manufacturing.

The ultimate goal of AI integration is the realization of a fully autonomous radial forging cell. AI systems will manage logistics, scheduling, quality control, and process optimization simultaneously, leading to unprecedented levels of operational efficiency and consistency. While the upfront investment in sensor technology and data infrastructure is substantial, the long-term benefits in terms of reduced material wastage, energy consumption optimization, and extended equipment lifespan position AI as a critical transformative technology for the radial forging sector, enhancing competitiveness and adherence to zero-defect manufacturing standards globally.

The Radial Forging Machines Market is powerfully influenced by a dynamic interplay of Drivers, Restraints, and Opportunities (DRO). A primary driver is the accelerating requirement across the aerospace and defense industries for high-strength, high-integrity components, often manufactured from advanced, difficult-to-forge alloys, where radial forging offers superior material properties compared to conventional methods. The stringent safety regulations in these sectors necessitate manufacturing processes that guarantee material integrity, thus cementing the critical role of radial forging technology. Furthermore, the global shift towards electric and hybrid vehicles stimulates demand for complex, lightweight shafts and rotors, demanding high-precision forming capabilities that these machines excel at providing. The economic efficiency of the process, including reduced material loss and minimized subsequent machining requirements, acts as a strong financial incentive for adoption, particularly among high-volume manufacturers.

However, significant restraints temper the market growth. Radial forging machines represent substantial capital investments, often requiring multimillion-dollar procurement, which poses a significant barrier to entry for smaller or medium-sized forging operations. The specialized nature of the equipment also necessitates highly skilled labor for operation, maintenance, and intricate die design, creating operational challenges in regions facing skilled labor shortages. Additionally, while radial forging is excellent for long, axisymmetric components, its applicability is restricted for components with highly non-uniform geometries, limiting its market penetration compared to versatile, general-purpose forging techniques. Economic volatility, particularly concerning capital expenditure across core end-user industries like oil and gas, can temporarily halt or delay major machine purchases, impacting short-term market stability.

The market presents substantial opportunities, largely stemming from technological innovation and geographical expansion. The growing focus on developing tailor-made alloys for specific industrial requirements, such as heat-resistant materials for additive manufacturing substrates or specialized biomedical implants, creates a niche demand for highly controlled deformation processing. Opportunities also lie in integrating advanced robotics for automated loading and unloading, further enhancing throughput and reducing human error. The increasing industrialization and investment in localized manufacturing capabilities in emerging economies offer fertile ground for new machine installations, particularly as these regions upgrade their manufacturing standards to meet global quality requirements. The shift toward incorporating advanced simulation software and AI for process planning represents a key opportunity for vendors to differentiate their offerings and capture higher value.

The primary impact forces driving the market are technological shifts (advancements in hydraulic systems and CNC control improving precision), economic imperatives (cost reduction through material saving), and regulatory pressure (demands for zero-defect components in critical industries). These forces collectively ensure that despite the high upfront cost, the long-term operational and quality benefits of radial forging technology remain highly compelling, maintaining steady market traction globally.

The Radial Forging Machines Market is segmented based on critical technical and application parameters to provide a detailed view of market dynamics and opportunity areas. Key segmentation criteria include the machine configuration (number of hammers), the forging temperature (hot, cold, or warm forging), the operational mechanism (hydraulic or mechanical), and the specific end-use industry application. This detailed breakdown allows stakeholders to focus on areas experiencing maximum growth, such as high-precision applications requiring multi-hammer hydraulic systems for advanced materials, which currently command a premium market value due to their technological sophistication and performance capabilities.

The value chain for the Radial Forging Machines Market begins with the upstream suppliers who provide specialized components essential for machine construction. This includes high-precision hydraulic systems (pumps, valves, accumulators), high-fidelity CNC controllers, specialized steel alloys for machine structures and tooling (dies, mandrels), and advanced electronic sensors. Upstream activities are characterized by high barriers to entry due to the stringent quality requirements and the necessity for robust, durable components capable of withstanding extreme, repetitive forces and high temperatures. Strategic relationships with niche suppliers of control systems, particularly those offering advanced software integration, are critical for competitive advantage in the machine manufacturing phase, ensuring precision and reliability.

The core of the value chain involves the original equipment manufacturers (OEMs) who design, assemble, and test the complex radial forging systems. This stage requires significant investment in R&D, focusing on optimizing hammer kinetics, developing sophisticated die-changing mechanisms, and integrating safety features. Manufacturers often differentiate themselves through proprietary software for process simulation and control, allowing end-users to maximize material yield and minimize setup time. Downstream activities commence with the installation, commissioning, and exhaustive testing of the machines at the customer site. Post-sales support, encompassing maintenance contracts, spare parts supply, and operator training, forms a crucial, high-margin component of the downstream revenue stream, ensuring machine longevity and optimal performance.

Distribution channels for these high-value machines are predominantly direct, involving close collaboration between the OEM's technical sales team and the end-user’s engineering department. Given the customized nature and large capital outlay associated with radial forging machines, an indirect distribution model through general industrial distributors is rare, except perhaps for ancillary equipment or spare parts. Direct sales ensure that specialized engineering consultation is provided pre-purchase, helping the buyer select the precise configuration (e.g., tonnage, number of hammers, automation level) tailored to their specific material and application needs. This direct approach mitigates risks associated with complexity and ensures efficient handling of logistical challenges, including transportation and installation of extremely heavy machinery components.

The primary consumers, or potential customers, of radial forging machines are large-scale manufacturers operating in sectors where high-integrity, high-performance metallic components are mandatory. The aerospace and defense sector represents a critical end-user base, utilizing these machines to produce mission-critical components such as engine shafts, structural airframe parts, and missile casings from materials like titanium alloys and Inconel. These buyers prioritize dimensional accuracy, superior fatigue life, and traceability, making advanced radial forging machines an indispensable investment, especially as demand for commercial aircraft rebuilds and next-generation military platforms continues to rise globally.

Another significant segment comprises the automotive industry, specifically Tier 1 and Tier 2 suppliers focused on manufacturing drivetrain components, including axles, gear blanks, and specialized connecting rods. With the automotive industry’s rapid transition towards electrification, there is increasing demand for machines capable of forging lightweight materials and creating highly complex internal structures necessary for high-efficiency electric motors and transmission systems. These customers typically demand high throughput capabilities and robust automation features to maintain cost-competitiveness in mass production environments, preferring four-hammer, hydraulic systems for enhanced efficiency and control.

Furthermore, specialized manufacturing facilities serving the oil and gas and power generation sectors constitute substantial potential customers. Oil and gas companies require robust, corrosion-resistant drilling tools, downhole components, and specialized piping forged to extremely high material standards to withstand harsh operating conditions. Similarly, power generation entities, including those focused on nuclear and thermal energy, require turbine and generator shafts with flawless internal grain structure, making radial forging the preferred method. These customers emphasize machine durability, the capability to handle high tonnage, and adherence to rigorous industry certifications (e.g., API standards) as primary purchasing criteria.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 785.4 Million |

| Market Forecast in 2033 | USD 1155.0 Million |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | SMS group, Siempelkamp, Japan Steel Works (JSW), Schuler Group, Lasco Umformtechnik, Felss Group, Mesta Machine, Danieli & C. Officine Meccaniche S.p.A., Fagor Arrasate, Stamtec, UBE Machinery, Erlo Group, Qingdao Huada Heavy Industry, Hefei Metalforming Machine Tool, VODIA forging machinery |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Radial Forging Machines Market is rapidly evolving, driven primarily by the need for enhanced precision, versatility, and operational efficiency. Central to this evolution is the advancement in hydraulic and electro-hydraulic control systems, which allow for extremely precise control over the forging force, frequency, and ram positioning. Modern machines utilize closed-loop feedback systems integrated with high-speed proportional valves to ensure hammer synchronization within milliseconds, crucial for maintaining geometric tolerances, particularly when forging hollow components using a mandrel. The trend is moving away from purely mechanical linkages toward hydraulic actuation for superior force regulation and stroke variability, enabling the processing of a wider range of materials with diverse flow stresses.

Computer Numerical Control (CNC) technology remains fundamental, but current innovations focus on integrating sophisticated process monitoring and data acquisition tools directly into the CNC interface. This includes the use of load cells, pyrometers, and strain gauges to monitor temperature, force, and deformation rates in real-time. This real-time data is essential for managing the material’s thermal history and ensuring optimal microstructure development. Furthermore, the development of quick-change tooling systems and modular die sets has significantly reduced machine downtime and increased the flexibility of radial forging machines, allowing manufacturers to rapidly switch production between different component types without extensive manual reconfiguration.

Looking ahead, the integration of Industry 4.0 elements, particularly the Internet of Things (IoT) sensors and cloud-based analytics, is becoming a standard feature. These technologies facilitate remote diagnostics, predictive maintenance scheduling, and global performance benchmarking. The focus on software extends to simulation capabilities, where advanced Finite Element Analysis (FEA) software is used extensively to model the complex thermomechanical process, optimizing initial billet size, forging sequence, and die geometry before any material is consumed. This technological sophistication is necessary to meet the demanding quality standards of the aerospace and nuclear sectors, where zero-defect manufacturing is the ultimate objective.

The global Radial Forging Machines Market exhibits distinct regional consumption patterns dictated by industrial maturity, capital investment capacity, and the presence of dominant end-user sectors, particularly aerospace and automotive manufacturing clusters. These regional dynamics are crucial for understanding market opportunity and vendor strategy.

Asia Pacific (APAC) Dominance and Growth Trajectory: APAC is the fastest-growing region and the largest market in terms of volume consumption, driven primarily by robust industrial expansion in China, India, and Southeast Asian nations. The region benefits from massive domestic automotive production, increasing defense expenditure, and significant infrastructure investments requiring large-scale, high-quality forged steel components. The Chinese market, in particular, showcases rapid adoption of advanced forging technologies as manufacturers strive to meet international quality standards and optimize material utilization. South Korea and Japan continue to be leaders in high-precision equipment manufacturing, contributing strong demand from their established automotive and shipbuilding industries, favoring the adoption of highly automated, four-hammer systems for complex parts.

North America and Europe: High-Value, Advanced Manufacturing Hubs: North America and Europe represent mature markets characterized by high average selling prices for machines, focusing on specialized, high-tonnage equipment tailored for sophisticated material processing. The demand in North America is heavily concentrated within the aerospace and defense sectors, primarily driven by major OEMs and their supply chains requiring machines capable of forging exotic alloys (e.g., titanium and nickel superalloys) for demanding environments. European demand, led by Germany, Italy, and France, is buoyed by their strong presence in high-end automotive, power generation, and specialized machinery manufacturing. These regions are also at the forefront of integrating AI and automated handling systems into their existing forging operations to maximize productivity and maintain a competitive edge through technological sophistication rather than volume output.

Emerging Opportunities in MEA and Latin America: The Middle East and Africa (MEA), alongside Latin America, offer emerging opportunities, particularly linked to the oil and gas sector resurgence and localized manufacturing initiatives. Demand in the MEA region is driven by investments in high-specification oilfield tubular goods and infrastructure projects, favoring machines with proven durability and maintenance simplicity. Brazil and Mexico lead the demand in Latin America, capitalizing on their established automotive manufacturing base and seeking modern equipment to enhance the quality and competitiveness of exported components. However, market adoption in these regions can be volatile, often tied directly to commodity prices and government spending on infrastructure and energy projects.

Radial forging offers superior material utilization, reducing scrap rates significantly, especially when working with expensive alloys. It produces components with enhanced mechanical properties, including improved grain flow, high fatigue strength, and better surface finish. Furthermore, the process yields components closer to net shape, drastically minimizing subsequent machining costs and time, thus increasing overall manufacturing efficiency.

The largest consumers are the aerospace and defense industries, due to their stringent requirements for high-integrity components such as turbine shafts and landing gear. The automotive sector, particularly manufacturers focused on axles, transmission parts, and specialized components for electric vehicles (EVs), also represents a major application segment requiring high throughput and precision forging capabilities.

Four-hammer machines offer superior control over complex cross-sectional geometries and provide better dimensional accuracy and roundness, especially beneficial for creating stepped or hollow components. Two-hammer machines are generally simpler and used for basic reduction forging, whereas four-hammer configurations enable more sophisticated, multi-stage forming operations crucial for high-precision components like engine shafts, maximizing material deformation control.

AI is primarily used to implement predictive maintenance schedules, analyzing real-time machine data to prevent unexpected downtime, thereby maximizing equipment uptime. It is also applied in process optimization, where machine learning algorithms automatically fine-tune forging parameters (force, speed, temperature) to compensate for material variations, ensuring consistent quality and optimizing energy consumption during the forging cycle.

The most significant restraints include the extremely high initial capital expenditure required for purchasing and installing these specialized machines. Additionally, radial forging requires a highly trained workforce for complex setup, programming, and maintenance. Finally, the process is primarily limited to axisymmetric components, restricting its application compared to more versatile, open-die forging techniques.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.