ID : MRU_ 433421 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

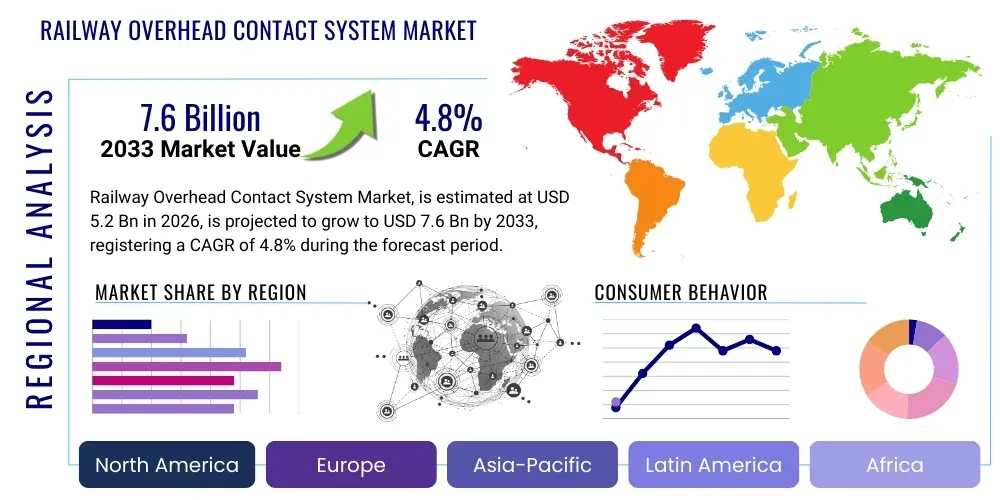

The Railway Overhead Contact System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 5.2 Billion in 2026 and is projected to reach USD 7.6 Billion by the end of the forecast period in 2033.

The Railway Overhead Contact System (OCS), also commonly referred to as the overhead line equipment (OLE) or catenary system, is a critical infrastructure component designed to supply electrical energy to trains, trams, and trolleybuses. These systems ensure uninterrupted current collection by the pantograph, enabling electric propulsion across various railway networks. The OCS comprises intricate components such as contact wire, messenger wire (catenary wire), droppers, insulators, cantilevers, and tensioning devices, all engineered for high reliability and minimizing wear under dynamic operating conditions. The longevity and efficiency of railway operations are heavily dependent on the robust design and maintenance of these electrified systems, particularly in environments facing extreme weather conditions and high operational speeds.

The core product in this market revolves around managing electrical power transmission at various voltages, including 1.5 kV DC, 3 kV DC, and the globally dominant 25 kV AC, single-phase systems. Major applications span high-speed rail networks, where highly dynamic and specialized OCS designs are required to minimize uplift and spark generation; mainline passenger and freight corridors needing durable, low-maintenance solutions; and urban transit systems (metros, light rail) which often utilize rigid overhead conductor rails in tunnels and constrained environments. The primary benefit of an efficient OCS is maximizing network capacity, reducing reliance on fossil fuels, and ensuring rapid, reliable transit.

Driving factors underpinning market growth include massive global investments in high-speed rail expansion, particularly across Asia Pacific and Europe, driven by urbanization and sustainable transport mandates. Furthermore, the mandatory replacement and modernization of aging OCS infrastructure in developed economies, coupled with increased focus on railway safety standards and network digitalization, necessitate continuous investment in advanced materials, monitoring technologies, and smart power management solutions. The push towards standardization and interoperability across international rail networks also contributes significantly to market demand for compatible, high-performance systems.

The Railway Overhead Contact System market is characterized by stable, long-term growth driven primarily by governmental infrastructure spending and the global shift towards electrifying rail transport for carbon reduction goals. Business trends indicate a strong move towards prefabricated OCS components and modular systems to accelerate installation timelines and reduce overall project costs. Strategic collaboration between railway operators and specialized component manufacturers is intensifying, focusing on developing lighter materials, such as copper-magnesium alloys for contact wires, which offer superior conductivity and mechanical strength, thereby enhancing the operational lifespan of the system.

Regional trends highlight Asia Pacific, led by China and India, as the foremost growth engine due to expansive new rail project development, including dedicated freight corridors and high-speed connections. Europe maintains a significant market share, driven primarily by the modernization of existing transnational rail lines, standardization efforts mandated by the European Union, and the integration of smart monitoring solutions. North America, while having extensive freight rail, is seeing targeted growth in passenger rail and commuter lines requiring new or significantly upgraded OCS infrastructure to accommodate higher capacity and speed requirements.

Segment trends reveal that the Catenary System segment, particularly the compound catenary variant, holds the largest market share due to its suitability for mainline and high-speed applications requiring high reliability and performance under tension. Simultaneously, the Urban Transit segment is showing accelerated growth, fueled by the adoption of rigid overhead conductor bars for metro systems, offering compact, low-maintenance power delivery in tunnels. Furthermore, the voltage segment specializing in 25 kV AC is dominant, reflecting its status as the international standard for new high-performance mainline electrification projects, while the demand for advanced insulators and remote monitoring components is seeing high technological innovation and adoption rates.

User queries regarding the impact of Artificial Intelligence (AI) on the Railway Overhead Contact System market predominantly revolve around predictive maintenance capabilities, anomaly detection, and optimization of power consumption. Stakeholders are keen to understand how AI-driven analytics, utilizing data from sensor arrays integrated into OCS components, can transition maintenance practices from reactive or time-based schedules to condition-based and predictive interventions. Key concerns focus on the cost-effectiveness of implementing complex AI models, the security of large volumes of operational data, and the need for standardized data formats across diverse OCS architectures to ensure successful deployment of advanced diagnostic tools.

AI is fundamentally transforming the lifecycle management of OCS assets. By deploying machine learning algorithms on high-frequency data streams—including temperature, vibration, sag, and visual inspections captured by drone or train-mounted cameras—operators can accurately predict component failures, such as contact wire wear or insulator degradation, long before they lead to service disruption. This predictive capability significantly minimizes unplanned downtime, optimizes maintenance resource allocation, and extends the effective operational life of the infrastructure. Moreover, AI models are increasingly used to analyze complex environmental factors (like wind load or ice buildup) and adjust system tension settings remotely for optimal performance.

The introduction of AI-powered digital twins allows railway engineers to simulate various operational scenarios, test the resilience of new OCS designs under simulated loads, and optimize the energy flow across the network in real-time. This optimization, particularly critical in large, interconnected high-speed networks, ensures power consumption is minimized while maintaining consistent voltage levels for train operation. The integration of AI tools is becoming a prerequisite for next-generation OCS modernization projects, moving the industry towards highly automated, self-regulating, and exceptionally reliable electric railway systems.

The market dynamics are governed by a complex interplay of Drivers, Restraints, and Opportunities (DRO), amplified by various Impact Forces stemming from regulatory, technological, and economic factors. The primary driver is the accelerating global imperative for sustainable transportation, necessitating widespread rail electrification to meet climate targets. However, the high initial capital expenditure associated with new OCS installation, coupled with extended project timelines and dependence on governmental funding cycles, acts as a significant restraint. Opportunities lie chiefly in the realm of smart infrastructure and advanced materials, allowing for lighter, more durable, and digitally monitored systems that appeal to cost-conscious operators seeking long-term operational efficiency.

The impact forces influencing the market are multifaceted. Technological innovation, particularly in composite materials for insulators and the application of superconducting technologies in feeder lines, pushes the efficiency and reliability envelope. Regulatory forces, such as stringent European Union standards for interoperability (TSI) and increasing safety requirements globally, necessitate continuous upgrades and adoption of standardized OCS products, thereby stabilizing demand. Economic impact forces are crucial; while high commodity prices (especially copper) can increase input costs, the lower operational and environmental costs of electric rail compared to diesel provide a robust long-term justification for investment, mitigating short-term financial pressures.

Furthermore, demographic impact forces, particularly increasing urbanization and commuter density, necessitate higher-capacity, high-frequency transit systems, which demand more robust and reliable OCS infrastructure. Competitive impact forces are high, with established large engineering firms vying for large infrastructure contracts, leading to intense pricing pressures but also fostering rapid technological iteration, such especially concerning modular components and rapid deployment solutions. These forces collectively steer the market towards advanced solutions that promise maximum throughput with minimal lifetime maintenance costs.

The Railway Overhead Contact System market is segmented based on the fundamental characteristics of the infrastructure, the components utilized, the operating voltage, and the end-use application. This segmentation provides a granular view of demand patterns, enabling manufacturers to tailor products to specific operational requirements, whether for ultra-high-speed passenger services or heavy-haul freight lines. The market is primarily bifurcated into dynamic catenary systems used predominantly outdoors, and rigid overhead conductor rails favored in restricted environments like tunnels and depots. Understanding these segments is crucial as technological evolution is often segment-specific, driven by unique performance criteria such as maximizing speed versus minimizing maintenance requirements.

Detailed analysis of the component segment highlights where the highest value resides, with contact wire being the most frequently replaced consumable, driving recurrent revenue for suppliers. Conversely, components like tensioning devices and cantilevers require high initial engineering investment but offer longer service lives. The application segmentation clearly delineates distinct market requirements; for example, high-speed rail demands complex, compensated catenary systems, while mainline and freight applications prioritize robustness and resistance to heavy loads and adverse environmental conditions. This structure allows for precise forecasting based on regional infrastructure investment plans.

The value chain for the Railway Overhead Contact System market starts with upstream activities involving the sourcing and processing of raw materials, predominantly high-purity copper and copper alloys (e.g., CuMg, CuCd) for contact wires, high-strength steel or aluminum for support structures, and advanced polymers or ceramics for insulators. Critical upstream suppliers include specialized non-ferrous metal producers and cable manufacturers. The quality and availability of these materials directly impact the final product's performance specifications, such as conductivity, tensile strength, and abrasion resistance. Efficiency in this stage relies heavily on optimizing manufacturing processes to meet strict railway safety and performance standards.

Midstream activities involve the core manufacturing and integration of OCS components. This stage is dominated by specialized engineering firms and large multinational conglomerates who possess the complex intellectual property required for designing high-performance catenary systems, specifically the geometry needed for high-speed operation. Key processes include precision extrusion of contact wires, fabrication of cantilevers, and assembly of complex tensioning equipment. Distribution channels are typically direct, involving long-term contracts between system integrators or Tier 1 suppliers and the end-user (Railway Operators or Governmental Railway Authorities). Indirect channels are less common but involve distributors or local agents for smaller component sales or specific regional projects.

Downstream analysis focuses on installation, commissioning, and long-term maintenance. Installation is highly specialized, requiring specific railway engineering expertise and often involving highly automated equipment for wire stringing and tensioning. The downstream market provides significant opportunity for service revenue through maintenance, inspection, and replacement of consumable components like contact wires and droppers. Direct engagement ensures quality control and adherence to project specifications, while the specialized nature of the infrastructure minimizes indirect influence on major project execution.

The primary customer base for the Railway Overhead Contact System market comprises governmental and private entities responsible for the planning, financing, and operation of electric railway networks globally. The largest volume buyers are National Railway Operators, such as Deutsche Bahn, SNCF, Indian Railways, and China Railways, which manage extensive mainline and high-speed infrastructure and possess significant budgetary authority for electrification and replacement programs. These operators prioritize long-term reliability, low total cost of ownership (TCO), and compliance with stringent national and international standards, often dictating the technical specifications for components.

A second major customer segment includes Urban Transit Authorities and Metropolitan Transport Agencies, which manage metro, subway, and light rail systems. These buyers typically focus on rigid OCS solutions or specific compact catenary systems tailored for confined urban environments. Their purchasing criteria often emphasize robustness, minimal maintenance requirements, and quick installation within densely populated or operational areas. Projects in this segment are often driven by city-level infrastructure expansion plans aimed at reducing road congestion and improving urban mobility.

Furthermore, specialized rail project consortiums, often comprising public-private partnerships (PPPs) formed for large-scale, greenfield high-speed rail development, represent significant, albeit episodic, customer demand. These consortiums act as temporary buyers, procuring comprehensive, integrated OCS solutions from Tier 1 suppliers. Finally, large industrial operations, particularly in mining or ports utilizing captive electric rail networks for heavy-haul transport, also constitute a niche customer base, requiring highly durable, heavy-duty OCS equipment designed for continuous, severe operating conditions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 5.2 Billion |

| Market Forecast in 2033 | USD 7.6 Billion |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Siemens AG, Alstom SA, Hitachi Ltd., ABB Ltd., TE Connectivity, Kummler + Matter AG, Furrer + Frey AG, NKT A/S, L.B. Foster Company, CRRC Corporation Limited, Arteche Group, Nexans S.A., Pfisterer Holding AG, Progress Rail (Caterpillar), TATA Projects Ltd., Eland Cables, Arthur Flury AG, Cembre S.p.A., K&M Engineering, Bombardier Inc. (acquired by Alstom). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape in the Railway Overhead Contact System market is shifting from traditional, heavy copper-based systems towards lightweight, smart, and durable solutions designed for higher speeds and reduced maintenance intervals. One pivotal technological trend is the increasing adoption of copper-magnesium (CuMg) and copper-silver alloys for contact wires, which offer superior tensile strength and resistance to abrasive wear compared to pure copper, allowing for higher tensioning and greater operational speeds without compromising safety or conductivity. Furthermore, the push towards standardized modular components, such as pre-assembled cantilever assemblies and standardized dropper lengths, is streamlining installation processes and reducing project costs significantly.

Another major technological advancement is the integration of advanced sensing and monitoring systems, transitioning OCS into smart infrastructure. These systems utilize fiber optic cables (integrated into the catenary) and strategically placed current, temperature, and vibration sensors to provide real-time data on wire sag, icing conditions, pantograph-OCS interaction quality, and insulator performance. This data is fed into centralized monitoring platforms, often utilizing IoT architecture, enabling condition monitoring and facilitating the aforementioned predictive maintenance strategies. This digitalization improves reliability and minimizes the substantial costs associated with manual inspections and reactive repairs.

In urban applications, the rigid overhead conductor rail (ROCR) technology is rapidly maturing. ROCR systems, typically aluminum profiles with a copper contact strip, are favored for metro tunnels and enclosed spaces due to their compact size, minimal maintenance requirements, and ability to handle high currents at low voltage (DC). These systems offer greater stability and safety compared to flexible catenary in tight clearances. Furthermore, new developments in lightweight composite insulators are replacing traditional ceramic ones, offering better resistance to vandalism, pollution, and mechanical shock while simplifying installation procedures.

Regional dynamics significantly influence the trajectory of the Railway Overhead Contact System Market, with spending concentrated in areas undergoing massive infrastructure expansion or compulsory system renewal. Asia Pacific (APAC) dominates the market share and is expected to exhibit the highest growth rate during the forecast period. This growth is directly attributable to extensive government initiatives, particularly in China, India, and Southeast Asia, aimed at building vast new high-speed railway networks and electrifying existing conventional lines to handle increasing passenger and freight volumes efficiently. India’s ambitious 100% electrification target for its broad gauge network is a key factor driving sustained high demand for OCS components and complete systems.

Europe represents a mature but technologically advanced market. Growth here is primarily driven by necessary replacement and modernization programs focused on upgrading legacy systems to meet European Rail Traffic Management System (ERTMS) and Technical Specifications for Interoperability (TSI) standards. Countries like Germany, France, and the UK are heavily investing in digitalizing their OCS infrastructure, focusing on advanced monitoring and predictive analytics to optimize highly utilized transnational corridors. The integration of high-speed lines and cross-border connectivity mandates investments in OCS systems capable of handling multiple voltage inputs and exhibiting high resilience.

North America maintains a specialized market focus. While passenger rail electrification, particularly in urban corridor projects (e.g., California High-Speed Rail), generates significant demand, the region's vast heavy-haul freight networks are slowly exploring electrification where feasible, although diesel remains dominant. The Middle East and Africa (MEA) region shows promising, project-specific growth, driven by ambitious projects such as the Gulf Cooperation Council (GCC) Railway and similar greenfield high-speed projects in Saudi Arabia and the UAE, requiring complete, advanced OCS installations from scratch. Latin America, though facing economic challenges, shows consistent demand stemming from urban transit development in major metropolitan areas like São Paulo and Mexico City.

The primary factor is the global mandate for sustainable transportation, specifically the widespread governmental initiatives and investments aimed at electrifying existing diesel rail networks and constructing new high-speed electric corridors to achieve significant carbon emission reductions.

Predictive Maintenance, enabled by AI and sensor technology, dramatically improves cost-effectiveness by shifting maintenance from scheduled or reactive repairs to condition-based interventions. This minimizes unplanned service disruptions, extends component lifespan, and reduces labor costs associated with unnecessary inspections.

Catenary systems are flexible, utilizing messenger and contact wires tensioned over long spans, making them ideal for high-speed and mainline outdoor applications. ROCS are rigid aluminum profiles with a contact strip, preferred for confined spaces like tunnels, depots, and metro lines due to their compact size and low maintenance needs.

The Asia Pacific (APAC) region currently leads the market for new OCS installation projects, driven primarily by continuous, large-scale railway electrification and high-speed rail network expansion programs in economic powerhouses such as China and India.

Modern OCS contact wires increasingly utilize high-strength copper alloys, predominantly Copper-Magnesium (CuMg) or Copper-Silver alloys. These materials offer superior mechanical strength and abrasion resistance compared to pure copper, enabling higher tensioning and reliable operation at high train speeds.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.