ID : MRU_ 438943 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

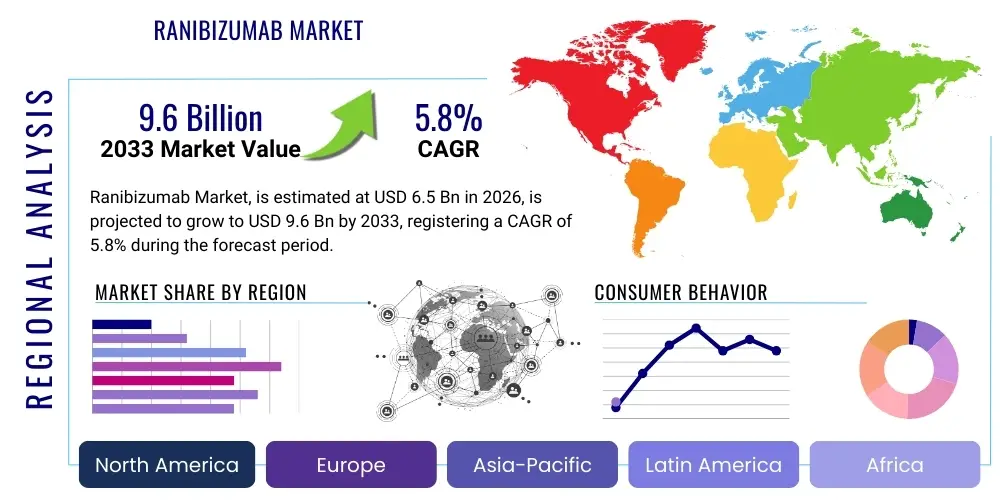

The Ranibizumab Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 6.5 Billion in 2026 and is projected to reach USD 9.6 Billion by the end of the forecast period in 2033. This consistent expansion is primarily fueled by the increasing global prevalence of chronic retinal vascular diseases, notably Age-related Macular Degeneration (AMD) and Diabetic Macular Edema (DME), coupled with the proven efficacy of anti-VEGF therapies like Ranibizumab in preserving vision and improving patient outcomes.

The Ranibizumab market encompasses the global sales and distribution of Ranibizumab, a recombinant humanized monoclonal antibody fragment that binds to and inhibits vascular endothelial growth factor A (VEGF-A). Ranibizumab, marketed under the trade name Lucentis, is administered via intravitreal injection and is a cornerstone therapy in modern ophthalmology, specifically designed to treat vision-threatening retinal conditions caused by abnormal blood vessel leakage and growth. Its mechanism of action targets the core pathological pathway of neovascularization and vascular permeability, offering substantial clinical benefits over older treatment modalities. The product is manufactured using sophisticated bioprocess techniques, ensuring high purity and targeted binding affinity.

Major applications for Ranibizumab include the treatment of Neovascular (Wet) Age-related Macular Degeneration (AMD), Macular Edema secondary to Retinal Vein Occlusion (RVO), Diabetic Macular Edema (DME), and visual impairment due to Choroidal Neovascularization (CNV). The primary benefit of Ranibizumab lies in its ability to halt disease progression, stabilize visual acuity, and, in many cases, lead to significant functional improvement, thereby enhancing the quality of life for patients. Its established efficacy profile and strong clinical data have cemented its position as a gold standard treatment, particularly in regions where healthcare systems prioritize evidence-based medicine for chronic ocular conditions.

Driving factors for market growth include the aging global population, which correlates directly with an increased incidence of AMD; the rising prevalence of diabetes, leading to a higher burden of DME; and continuous advancements in injection techniques and diagnostic imaging (such as Optical Coherence Tomography or OCT) that enable earlier detection and treatment initiation. Furthermore, regulatory approvals extending Ranibizumab’s use to pediatric and emerging indications, alongside ongoing patient education and physician training regarding the optimal use of anti-VEGF agents, are crucial in sustaining market momentum despite competitive pressures from newer, longer-acting biologics and emerging biosimilar entrants.

The Ranibizumab market demonstrates resilient growth, underpinned by a high global disease burden, yet faces significant competitive transformation driven by patent expiry and biosimilar introduction. Current business trends indicate a strategic shift by originator companies toward life cycle management, focusing on optimizing real-world evidence collection and securing advantageous reimbursement pathways, particularly in developed economies. The primary pressure point remains the launch of Ranibizumab biosimilars, which are rapidly altering the pricing landscape and shifting volume utilization towards lower-cost alternatives, especially in European and Asian markets. However, the market size growth projection is maintained by the expanding application scope, specifically in managing complex retinal pathologies and the inherent brand loyalty and established safety profile of the reference product among long-standing clinical practitioners.

Regionally, North America and Europe remain the dominant revenue contributors due to well-established healthcare infrastructure, high diagnosis rates, and comprehensive anti-VEGF treatment guidelines. The Asia Pacific region, conversely, is poised for the highest growth rate, fueled by improving healthcare access, increasing disposable income in emerging economies like China and India, and rising awareness campaigns regarding diabetic retinopathy screening. Segment trends show Wet AMD continuing its dominance in terms of overall revenue due to the large patient pool, while the Diabetic Macular Edema (DME) segment exhibits robust growth, mirroring the global diabetes epidemic. Distribution channels are progressively diversifying, with specialized hospital pharmacies and retinal clinics maintaining their primary roles, increasingly supported by robust supply chain logistics necessary for handling high-value, temperature-sensitive biologics.

Looking forward, the market’s stability hinges on innovation in drug delivery systems designed to reduce injection frequency, which is a key driver for patient compliance and preference. While competition from drugs like Aflibercept and novel compounds that target broader anti-angiogenic pathways is intense, Ranibizumab maintains significant market relevance due to its proven track record and the potential for combination therapies. The ongoing challenge for market stakeholders involves balancing the need for cost-effectiveness, mandated by payers and governments, with the continued investment required for clinical research and development necessary to maintain therapeutic superiority in the evolving ophthalmology space.

Common user inquiries concerning the influence of Artificial Intelligence (AI) on the Ranibizumab market frequently center on its capacity to revolutionize diagnostic pathways, optimize treatment decision-making, and streamline clinical trial processes. Key questions include whether AI can accurately predict patient response to Ranibizumab therapy, how AI-driven image analysis (OCT and fundus photography) might enable earlier intervention, and if generative AI models can accelerate the development of next-generation anti-VEGF molecules or delivery systems. Users express both anticipation regarding enhanced diagnostic efficiency and concern about the integration costs and regulatory hurdles associated with deploying sophisticated AI tools in routine clinical ophthalmology practices, particularly concerning data privacy and algorithmic bias in diverse patient populations. The overarching expectation is that AI will function as a powerful assistive technology, improving the efficiency and personalization of Ranibizumab treatment, thereby potentially maximizing treatment success rates and optimizing healthcare resource allocation.

The Ranibizumab market is shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively forming the fundamental Impact Forces guiding its trajectory. Primary drivers include the escalating global burden of retinal diseases, particularly age-related macular degeneration and diabetic retinopathy, coupled with substantial governmental and private payer investment in chronic eye care services. The established clinical safety and efficacy profile of Ranibizumab serve as a foundational driver, ensuring its sustained preference among retinal specialists worldwide. However, the market faces significant restraints, chiefly stemming from the intense pricing competition introduced by biosimilars following patent expiry and the inherent cost and invasiveness associated with frequent intravitreal injections, which can deter patient adherence and strain healthcare budgets.

Opportunities for growth are concentrated in expanding market access within developing nations, utilizing advanced formulation technologies to extend the drug’s duration of action, and exploring combination therapies that target multiple pathways simultaneously. Furthermore, developing less invasive delivery methods, such as sustained-release implants or gene therapies, presents a lucrative long-term opportunity to retain market share against emerging competitor modalities. These internal and external forces continuously interact, determining the therapeutic utility and commercial viability of Ranibizumab in an increasingly competitive environment. The Impact Forces analysis suggests that while external restraints (biosimilar competition) are intensifying, strategic internal maneuvers (expanding indications and improving delivery) are essential to counterbalance these pressures and maintain the drug’s significant market footprint.

The core Impact Forces affecting market dynamism include Technology Advancement, which drives better diagnostics and drug delivery; Regulatory Landscape shifts, particularly concerning biosimilar approvals and interchangeability status; Economic Factors, such as global healthcare spending limitations and reimbursement policies; and Competitive Dynamics, dominated by the rivalry between originator products (Lucentis, Eylea) and newly launched biosimilar alternatives (e.g., Byooviz, Cimerli). These forces collectively pressure stakeholders to innovate on price, convenience, and clinical differentiation to secure future market penetration. The continuous evolution of treatment paradigms from monthly dosing toward more flexible 'Treat-and-Extend' regimens further emphasizes the power of these forces in shaping patient care protocols and subsequent drug utilization patterns.

The Ranibizumab market is comprehensively segmented based on its primary applications, the types of distribution channels utilized for its supply, and the geographical regions where it is commercialized. Analyzing these segments provides critical insights into consumption patterns, regional disparities in disease prevalence and treatment access, and the efficacy of various commercial strategies. Application segmentation reveals where the highest clinical demand resides, with Wet Age-related Macular Degeneration (AMD) traditionally representing the largest revenue stream due to its high incidence in aging populations, although Diabetic Macular Edema (DME) is rapidly gaining share globally. The distribution channel breakdown highlights the crucial role of specialized centers and hospitals in administering this complex injectable therapy, while the increasing role of retail and online pharmacies reflects logistical adaptations in broader market access strategies. This granular segmentation is essential for stakeholders to tailor marketing efforts and optimize supply chain efficiencies in a market increasingly influenced by biosimilar dynamics and strict procurement regulations.

The value chain for the Ranibizumab market is highly regulated and intricate, starting with complex upstream processes involving biomanufacturing and active pharmaceutical ingredient (API) production. Upstream activities require advanced cell culture technology, stringent quality control measures, and substantial capital investment to produce the recombinant humanized antibody fragment. Key activities include cell line development, large-scale fermentation, purification, and sterile formulation. Given the high-tech nature of biologics, integration between research and manufacturing facilities is crucial for maintaining batch consistency and ensuring compliance with global Good Manufacturing Practices (GMP). The upstream segment is dominated by companies possessing proprietary biotechnological expertise and large-scale manufacturing capacity, acting as significant barriers to entry for smaller firms.

Midstream activities involve secondary packaging, serialization, storage, and logistics, focusing heavily on maintaining the cold chain necessary for Ranibizumab’s stability. Distribution channels are highly specialized due to the nature of the administration (intravitreal injection), meaning distribution is often direct from the manufacturer or through specialized third-party logistics (3PL) providers to centralized hospital pharmacies or dedicated retinal clinics. Direct distribution allows manufacturers greater control over the supply chain integrity and temperature monitoring. Indirect channels, primarily involving wholesalers and distributors, are utilized in regions requiring broader geographical coverage, but robust contractual agreements are necessary to ensure proper handling and rapid delivery timelines, crucial given the urgency often associated with retinal treatments.

Downstream activities center on the healthcare provider and the patient. This includes prescribing by retinal specialists, procurement by hospital pharmacies, and the sterile preparation and injection procedure performed in clinical settings. The final delivery of value is the administration of the drug to the end-user (patient) under expert medical supervision. Payers and reimbursement bodies play a critical downstream role, influencing product adoption and volume utilization through formulary inclusion decisions and pricing negotiations. The complexity of the downstream segment is magnified by the introduction of Ranibizumab biosimilars, which necessitates continuous education for payers and providers regarding interchangeability, cost-effectiveness, and real-world efficacy data comparison.

The primary potential customers and end-users of Ranibizumab are patients afflicted with severe, chronic retinal vascular diseases that threaten vision, such as Wet Age-related Macular Degeneration (AMD), Diabetic Macular Edema (DME), and Macular Edema following Retinal Vein Occlusion (RVO). These patient populations are primarily elderly individuals (for AMD) and individuals with poorly controlled or long-standing diabetes (for DME). The clinical decision-makers and immediate purchasers, however, are retinal specialists (ophthalmologists), institutional buyers (hospital procurement departments), and specialized clinics or ambulatory surgical centers (ASCs) that manage the large volume of intravitreal injection procedures. Government health systems and private insurance payers act as crucial financial gatekeepers, as their reimbursement policies fundamentally determine accessibility and affordability for the ultimate patient beneficiaries, making them essential stakeholders in the customer ecosystem.

Beyond individual clinics, large hospital systems and integrated delivery networks (IDNs) represent significant customers, often purchasing in bulk to benefit from volume-based discounts and streamline inventory management across multiple sites. These institutional customers prioritize stability of supply, established safety data, and competitive pricing, especially now with biosimilars available. Emerging markets present a growing customer base, where increasing awareness, better diagnostic technologies, and improving healthcare infrastructure are enabling a transition from limited or non-existent treatment to sophisticated anti-VEGF therapies. Therefore, strategic engagement must target both the medical professionals who make the prescribing decisions and the institutional bodies and governmental agencies that control the funding and procurement processes.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 9.6 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Genentech (Roche), Novartis, Samsung Bioepis, Coherus BioSciences, Sandoz (Novartis), Bio-Thera Solutions, Xbrane Biopharma, Polifarma S.p.A., Biocon Biologics, Regeneron Pharmaceuticals, Pfizer Inc., Amgen, Alcon, Bausch + Lomb, Apellis Pharmaceuticals, Eyevance Pharmaceuticals |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technology underpinning the Ranibizumab market is recombinant DNA technology used in the manufacturing of the anti-VEGF monoclonal antibody fragment. This technology involves highly specialized mammalian cell culture systems (e.g., CHO cells) to produce the therapeutic protein, followed by sophisticated chromatography and purification processes to ensure high biological activity and minimal impurity. Since Ranibizumab is a biologic, maintaining stringent biosafety and quality control standards throughout the production cycle is paramount. This foundational biotechnology determines the drug's effectiveness and manufacturing cost structure, creating a high barrier to entry for potential competitors, excluding those focused specifically on biosimilar development, which leverage existing molecular structure knowledge.

Beyond the drug itself, the technology landscape is heavily influenced by the drug delivery mechanism—intravitreal injection. Innovations here are crucial for market retention. Pre-filled syringes and auto-injectors, designed to standardize dosing, minimize contamination risk, and simplify the preparation process for clinicians, are increasingly being adopted. Furthermore, cutting-edge research focuses on developing sustained-release technologies, such as microparticles, hydrogels, or subretinal implants, intended to deliver Ranibizumab or its biosimilars over several months. Such advancements aim to dramatically reduce the frequency of injections, thereby improving patient compliance, reducing the risk of injection-related complications, and enhancing the overall treatment experience, directly competing with newer biologics that naturally possess longer half-lives.

Complementary technological advancements in diagnostic imaging are also indispensable to the Ranibizumab market. High-resolution Optical Coherence Tomography (OCT) allows clinicians to precisely visualize retinal fluid and monitor disease activity, guiding the ‘Treat-and-Extend’ dosing regimens. AI integration into OCT analysis represents the next major technological leap, enabling automated segmentation and quantification of macular edema, aiding in earlier and more accurate therapeutic decision-making regarding the continuation or adjustment of Ranibizumab therapy. The synergy between high-precision drug delivery systems and advanced monitoring tools ensures that Ranibizumab remains a highly effective and personalized treatment option in clinical practice.

The global Ranibizumab market exhibits distinct patterns across key geographical regions, driven by varying healthcare spending, regulatory frameworks, demographic profiles, and competitive landscapes, especially concerning biosimilar adoption. North America, specifically the United States, represents the largest revenue share due to high prevalence rates of AMD and DME, well-established treatment protocols, premium pricing strategies for the originator drug, and comprehensive reimbursement coverage through Medicare and private payers. The highly concentrated market access in the US means that even small shifts in formulary status can have profound revenue implications. However, the anticipated full-scale entry and uptake of Ranibizumab biosimilars in the US market are expected to induce significant pricing erosion and volume shifts post-2025.

Europe stands as the second-largest market, characterized by centralized procurement systems and intense price competition, particularly within the EU5 (Germany, France, UK, Italy, Spain). Biosimilars have achieved substantial penetration here, forcing the originator companies to engage in rigorous tendering processes and implement strategic discounting to maintain market presence. The adoption of biosimilars is rapid due to national policies promoting cost-efficiency and therapeutic equivalents. In contrast, the Asia Pacific (APAC) region is projected to experience the highest growth rate. This acceleration is attributed to massive, underserved patient populations (especially for DME in countries like China and India), rapidly improving access to specialized ophthalmic care, increased governmental expenditure on chronic disease management, and a growing middle class capable of affording advanced biotherapies. Regulatory harmonization and localized manufacturing initiatives in APAC are key to unlocking the region's full potential.

Latin America and the Middle East & Africa (MEA) currently hold smaller market shares but offer significant untapped potential. Market growth in these regions is contingent upon overcoming logistical challenges, improving cold chain management, and expanding public health coverage to include expensive specialty drugs. In MEA, high-income Gulf Cooperation Council (GCC) countries display adoption patterns similar to Western Europe, while broader African countries struggle with diagnosis rates and affordability. Manufacturers are increasingly focused on developing differentiated distribution models and local partnerships to navigate diverse regulatory and procurement environments across these high-potential but complex geographies.

The primary driver is the accelerating global prevalence of chronic retinal vascular diseases, specifically Age-related Macular Degeneration (AMD) in aging populations and Diabetic Macular Edema (DME), both of which necessitate effective and established anti-VEGF treatment like Ranibizumab to prevent permanent vision loss. Increased diagnostic capabilities also contribute significantly.

The entry of Ranibizumab biosimilars (such as Byooviz and Cimerli) has intensified pricing pressure, particularly in developed markets like Europe and increasingly in North America. This competitive dynamic is leading to price erosion, shifting market volume towards lower-cost options, and forcing originator companies to focus on clinical differentiation and lifecycle management strategies.

Wet Age-related Macular Degeneration (Wet AMD) currently holds the largest revenue share in the Ranibizumab market globally, attributed to the high incidence rate of this condition among the elderly and the drug's long-standing status as a first-line treatment in this indication across major regions.

Sustained-release drug delivery systems, including various forms of ocular implants or microparticle injections designed to release Ranibizumab continuously over extended periods (e.g., three to six months), are the most critical technological advancement. These innovations aim to reduce the substantial burden of frequent intravitreal injections for patients and healthcare systems.

AI plays a critical role in enhancing diagnostics by automating the analysis of retinal images (OCT), improving the early detection of disease activity, and assisting clinicians in optimizing personalized dosing schedules (Treat-and-Extend protocols) for Ranibizumab, thereby maximizing therapeutic outcomes and resource efficiency.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.