ID : MRU_ 434496 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

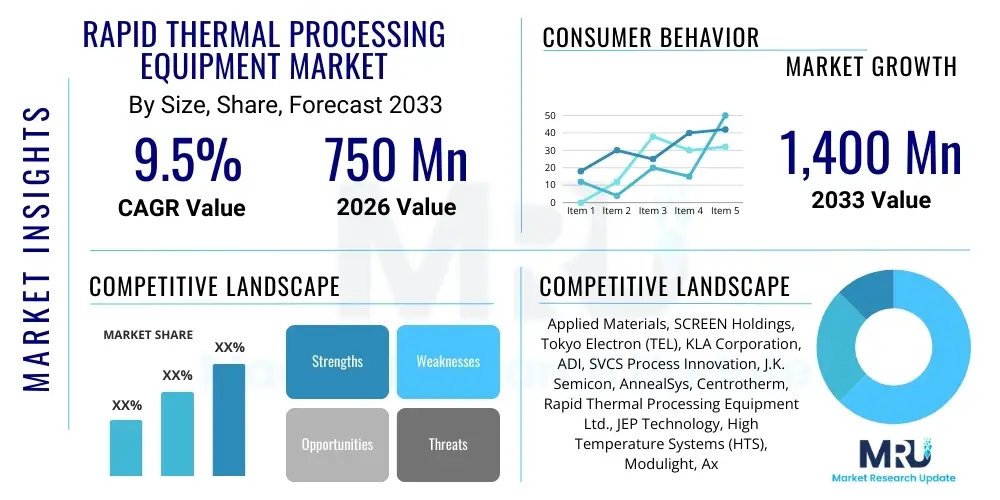

The Rapid Thermal Processing Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2026 and 2033. The market is estimated at $750 Million in 2026 and is projected to reach $1,400 Million by the end of the forecast period in 2033.

The Rapid Thermal Processing (RTP) Equipment Market encompasses advanced systems utilized in semiconductor manufacturing to heat single or multiple wafers to high temperatures for short periods, typically ranging from a few seconds to a few minutes. RTP is a crucial technology replacing traditional furnace annealing processes, offering superior control over the thermal budget, which is essential for manufacturing modern microelectronic devices with shrinking feature sizes and complex material stacks. The primary objective of RTP is to execute critical thermal steps such as dopant activation, silicidation, thin dielectric formation, and reflow processes with minimal diffusion, thereby preserving the sharpness of device junctions and maximizing device performance.

RTP equipment leverages highly controlled heating sources, predominantly halogen lamps, arc lamps, or increasingly, specialized lasers, to ensure extremely rapid temperature ramp-up and cool-down rates. This capability is paramount in advanced manufacturing nodes (14nm and below), where the thermal exposure must be precisely limited to prevent unintended movement of dopant atoms, which would otherwise degrade transistor characteristics. Major applications include the annealing of ion implantation damage following lithography steps, the formation of high-quality silicide layers on source/drain regions to reduce contact resistance, and the activation of complex III-V and other compound semiconductor materials used in high-frequency applications.

The core benefits driving the adoption of RTP include improved process repeatability, reduced contamination risks due to its single-wafer processing nature, and significant enhancement in wafer uniformity compared to batch furnaces. Furthermore, the increasing complexity of semiconductor architectures, particularly the shift towards FinFET and Gate-All-Around (GAA) structures, necessitates the precise thermal control that only RTP can deliver. Key driving factors include the relentless miniaturization trend (Moore's Law), escalating demand for high-performance computing (HPC) and artificial intelligence accelerators, and the global expansion of advanced wafer fabrication capacities, especially in Asia Pacific.

The Rapid Thermal Processing Equipment Market is characterized by intense technological competition focused on achieving tighter temperature uniformity and higher throughput, directly driven by the semiconductor industry's transition to smaller process nodes and complex material integration. Business trends indicate a strategic focus among major equipment manufacturers on developing hybrid RTP systems that combine lamp-based and laser annealing capabilities to address diverse thermal requirements across the wafer processing flow. Furthermore, there is a strong emphasis on integrating advanced sensing and real-time process monitoring tools, often leveraging machine learning algorithms, to optimize recipes and ensure zero-defect manufacturing, particularly crucial for high-volume foundry operations supplying next-generation consumer electronics and automotive components. Strategic collaborations between equipment vendors and leading Integrated Device Manufacturers (IDMs) are defining the technological roadmap, pushing the boundaries of thermal budget control.

Regionally, Asia Pacific maintains its dominance as the primary consumption and manufacturing hub for RTP equipment, spurred by massive investments in semiconductor fabrication plants (fabs) across Taiwan, South Korea, and Mainland China. These regions are capitalizing on government incentives and soaring global demand for memory (DRAM, NAND) and logic chips, necessitating continuous capacity expansion and technology upgrades featuring state-of-the-art RTP tools. North America and Europe, while smaller in volume, represent critical centers for R&D and the manufacturing of niche, high-value components, such as power devices and specialized compound semiconductors, thereby maintaining a steady demand for highly specialized RTP systems capable of handling non-silicon substrates. The intensifying geopolitical landscape is also subtly influencing supply chain resilience, prompting localized production strategies in several key markets.

Segment trends reveal a rapid shift towards specialized Laser Rapid Thermal Processing (LRTP) tools, particularly for critical steps like laser spike annealing (LSA) and millisecond annealing, necessary for 7nm and 5nm nodes to activate dopants while minimizing diffusion. The application segment dominated by ion implantation activation continues to hold the largest market share, but the silicidation and high-K/metal gate formation segments are demonstrating faster growth rates due to the pervasive adoption of new transistor architectures. By end-user, Foundries (pure-play and IDM) remain the largest consumers, demanding high-throughput, highly reliable systems to support multi-client manufacturing environments. The increasing necessity for faultless performance validation is boosting the market for specialized metrology and inspection systems integrated with or adjacent to the RTP equipment.

Common user questions regarding AI's influence on the Rapid Thermal Processing Equipment Market frequently center on how AI can enhance process control, predict equipment failure, and optimize the highly sensitive thermal recipes essential for advanced semiconductor nodes. Users are keenly interested in the integration of predictive maintenance (PdM) algorithms to maximize uptime and the application of machine learning (ML) to analyze complex sensor data (temperature uniformity, lamp status, wafer stress) in real-time. Key themes include the feasibility of achieving ‘self-optimizing’ RTP chambers, concerns over data security and proprietary recipe protection when implementing cloud-based AI solutions, and the tangible economic benefits, such as yield improvement and energy efficiency gains, resulting from AI-driven thermal management. Expectations are high that AI will transform RTP from a manually monitored tool to a highly autonomous system capable of dynamic recipe adjustment based on wafer-to-wafer variations, critical for achieving high yields at sub-10nm fabrication processes.

The market dynamics for Rapid Thermal Processing (RTP) equipment are shaped by a confluence of accelerating drivers related to miniaturization and high-performance demands, stringent restraints concerning capital expenditure and technical complexity, and significant opportunities arising from emerging semiconductor technologies and new application fields. The fundamental driver is the ongoing necessity to achieve tighter thermal control and minimize the thermal budget during critical doping activation and material modification steps, directly corresponding to the shift to sub-10nm geometries where traditional annealing techniques are insufficient. Restraints predominantly involve the extremely high cost of acquiring and maintaining these highly complex, multi-sensor systems, coupled with the necessity for highly skilled personnel to manage and troubleshoot advanced thermal recipes. The primary opportunity lies in the expanding adoption of specialized semiconductor materials, such as SiC (Silicon Carbide) and GaN (Gallium Nitride), crucial for power electronics and 5G/6G applications, which require custom, highly precise thermal annealing profiles that RTP systems are uniquely positioned to deliver.

Impact forces are centered on two major axes: technological obsolescence speed and geopolitical manufacturing shifts. The rapid pace of technological innovation in transistor architecture (e.g., GAA transition) compels equipment manufacturers to continuously invest in R&D, often shortening product lifecycles and requiring significant capital reinvestment from end-users to stay competitive. Geopolitical tensions, particularly regarding semiconductor supply chains, are driving a massive proliferation of localized fabrication capacity, most notably in the U.S. and Europe (CHIPS Act equivalent initiatives), which significantly increases the immediate addressable market for all types of semiconductor processing equipment, including RTP. Furthermore, environmental regulations and the focus on sustainable manufacturing are beginning to exert pressure, demanding RTP systems with lower energy footprints and minimized process gas usage, creating both a challenge and an opportunity for innovation in chamber design and heating mechanisms.

The balancing act between maintaining production efficiency (high throughput) and ensuring stringent process control (low thermal budget) creates a perpetual state of innovation pressure. Equipment providers must constantly optimize hardware reliability while integrating advanced software solutions for real-time monitoring and fault detection. Market forces thus favor established players who can offer integrated solutions that bundle RTP tools with critical metrology and inspection capabilities, ensuring seamless process flow and high yields for the most demanding fabrication processes. The transition to 300mm and eventually 450mm wafer sizes, although slow, also remains a structural force impacting future equipment design and capacity scaling requirements across the industry.

The Rapid Thermal Processing Equipment Market is fundamentally segmented based on the technology utilized for heating (Type), the specific step in the fabrication process where it is deployed (Application), and the primary facility where the equipment operates (End-User). The complexity of semiconductor manufacturing necessitates diverse RTP solutions; consequently, the segmentation reflects the varying thermal requirements—from ultra-fast millisecond annealing needed for junction activation in advanced logic chips to longer, more controlled processes required for dielectric film formation. Analyzing these segments provides a clear view of where capital expenditures are being directed and which technological advancements are gaining traction, particularly the ongoing transition from traditional lamp-based systems toward more precise laser-based and hybrid technologies designed specifically for thermal budget minimization and handling novel substrate materials.

The value chain for Rapid Thermal Processing Equipment is intricate, beginning with highly specialized upstream suppliers providing critical components such as high-intensity halogen lamps, sophisticated pyrometry systems, vacuum pumps, and advanced quartzware. Upstream activities are dominated by specialized component manufacturers who must maintain rigorous quality control, as the performance and longevity of the RTP system rely heavily on the reliability of the heating source and temperature sensing accuracy. This segment is characterized by high barriers to entry due to stringent performance specifications and intellectual property surrounding thermal engineering. Major equipment manufacturers then integrate these components, adding proprietary software for recipe control, automated wafer handling systems, and advanced metrology integration, transforming components into high-value, complex capital equipment systems. The core value addition at this stage is the system integration and software intellectual property that ensures precise, repeatable thermal processing tailored to specific semiconductor nodes.

Downstream activities involve the distribution, installation, and extensive post-sales support required by the end-users—primarily large semiconductor fabrication facilities (fabs). Distribution channels are typically direct, leveraging the equipment manufacturers' highly trained field service engineers and sales teams due to the specialized nature and immense cost of the systems. Direct sales ensure that the manufacturer maintains control over the system setup and can provide immediate technical support crucial for minimizing fab downtime. Indirect channels, involving local agents or specialized distributors, are sometimes utilized for smaller regional markets or for supplying refurbishment services, but the core capital equipment procurement remains direct. The downstream phase is critical for long-term customer relationships, relying heavily on maintenance contracts, software upgrades, and process consultation services to optimize throughput and yield in the client’s facility.

Crucially, the high complexity of RTP tools mandates that service and maintenance form a significant part of the overall value capture post-sale. The rapid evolution of semiconductor processes requires frequent software updates and, occasionally, hardware modifications (e.g., transitioning from one generation of heating lamps to the next) to accommodate new thermal recipes. This continuous engagement ensures a sustained revenue stream for the original equipment manufacturers (OEMs). The direct interaction between OEMs and end-users (Foundries and IDMs) also facilitates a rapid feedback loop, allowing equipment design to be quickly iterated based on real-world yield data and advanced process development needs, effectively blurring the line between equipment supply and co-development of manufacturing processes.

The primary customers for Rapid Thermal Processing equipment are organizations heavily involved in the front-end fabrication of semiconductor devices, where precise thermal management is non-negotiable for producing high-functioning microchips. The core buying entities are Integrated Device Manufacturers (IDMs) such as Intel, Samsung, and Micron, who design and manufacture their own chips, requiring RTP tools for critical steps like memory cell formation and complex logic transistor creation. Secondly, pure-play Foundries, exemplified by TSMC and GlobalFoundries, represent the largest volume buyers, as they cater to hundreds of fabless design companies and require the most advanced, high-throughput RTP systems to maintain competitiveness across various technology nodes, from mature processes to bleeding-edge 3nm and beyond.

A rapidly growing segment of potential customers includes specialized manufacturers focusing on emerging materials and applications, particularly in the fields of power electronics, photonics, and compound semiconductors. These include companies manufacturing SiC or GaN devices for electric vehicles (EVs) and 5G infrastructure, which demand highly stable and customized RTP tools for high-temperature activation and defect repair. Finally, research and development institutions, including universities and national laboratories specializing in material science and nanotechnology, constitute a steady customer base, albeit for lower-volume, more flexible RTP systems used for prototyping and process discovery before commercial scaling. These diverse end-users share the common requirement for extreme temperature accuracy and wafer uniformity control.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $750 Million |

| Market Forecast in 2033 | $1,400 Million |

| Growth Rate | 9.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Applied Materials, SCREEN Holdings, Tokyo Electron (TEL), KLA Corporation, ADI, SVCS Process Innovation, J.K. Semicon, AnnealSys, Centrotherm, Rapid Thermal Processing Equipment Ltd., JEP Technology, High Temperature Systems (HTS), Modulight, Axcelis Technologies, Semco Engineering, ULVAC, AIXTRON, Advanced Semiconductor Equipment Corporation (ASE), ASM International, Daewoo Semiconductor Equipment. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Rapid Thermal Processing (RTP) market is defined by continuous innovation focused on achieving ultrafast heating rates and exceptional temperature uniformity across larger wafers (300mm). The dominant technology remains Lamp-based RTP, utilizing high-intensity halogen or arc lamps, which provide rapid ramp rates (up to 200°C per second) and are cost-effective for general annealing applications like dopant activation at mature nodes. However, for leading-edge nodes (7nm and below), the requirement for millisecond thermal exposure to prevent junction broadening necessitates the increasing adoption of Laser Rapid Thermal Processing (LRTP), including Laser Spike Annealing (LSA) and Flash Lamp Annealing (FLA). LSA focuses a laser line across the wafer surface, allowing for extremely localized, rapid heating and cooling cycles, which is indispensable for maintaining the integrity of highly constrained FinFET and GAA structures. This dual technological approach—optimized lamp systems for throughput and laser systems for precision—drives market innovation.

A critical technical challenge facing all RTP technologies is accurate, non-contact temperature measurement, which is primarily achieved through advanced pyrometry. Modern systems utilize multi-wavelength pyrometers combined with sophisticated calibration techniques to precisely map the wafer's thermal profile in real-time, compensating for emissivity changes caused by varying thin films on the wafer surface. Furthermore, the development of specialized chambers and advanced gas flow management systems is essential to ensure atmospheric control, often employing ultra-high vacuum or specific inert gas environments to prevent oxidation and contamination during high-temperature processing. Integration with advanced process control (APC) software, leveraging complex algorithms to manage lamp zones and power feedback, is now a standard feature, moving RTP from a passive heating step to an active, intelligence-driven thermal management process.

Emerging technologies include microwave annealing, which offers selective heating of certain materials, and the development of specialized hybrid RTP systems that combine the bulk heating efficiency of lamps with the precision of localized laser heating to achieve optimized thermal budgets for complex 3D stacking processes. As the industry moves towards 3D integration (e.g., stacking logic on memory), the necessity to anneal lower layers without degrading previously formed metallic interconnects demands extremely selective and low-temperature thermal processing, which these hybrid and advanced laser techniques are specifically designed to address. The technology landscape is thus characterized by high complexity, intellectual property concentration, and a dependency on materials science breakthroughs related to heating sources and chamber materials that can withstand extreme thermal cycling.

RTP equipment is designed to rapidly heat semiconductor wafers to high temperatures (up to 1300°C) for short, controlled durations, typically a few seconds. Its primary function is to perform critical thermal steps such as activating implanted dopants, forming low-resistance silicide contacts (salicidation), or growing thin dielectric layers, all while meticulously controlling the thermal budget to prevent excessive diffusion and maintain the performance integrity of nanoscale devices.

Lamp-based RTP uses high-intensity halogen or arc lamps for bulk, large-area heating, suitable for general annealing processes. LRTP, including techniques like Laser Spike Annealing (LSA), uses a focused laser beam to heat the wafer surface in milliseconds. This extremely short thermal exposure time is critical for advanced nodes (7nm and below) to activate dopants without allowing them to diffuse, thereby preserving the sharpness of ultra-shallow device junctions, which is impossible with conventional lamp-based systems due to their longer ramp-down times.

Asia Pacific (APAC), particularly Taiwan, South Korea, and Mainland China, drives the highest volumetric demand due to massive investments in foundry and memory fabrication capacity (300mm wafer production). However, technological innovation, especially regarding advanced laser annealing systems and novel material processing (SiC/GaN), is frequently pioneered by research institutions and leading equipment manufacturers predominantly based in North America and Japan.

AI is increasingly integrated into RTP systems to enhance process robustness and efficiency. AI algorithms are used for real-time Advanced Process Control (APC) by analyzing sensor data to dynamically adjust heating zones and ensure exceptional temperature uniformity. Furthermore, AI drives Predictive Maintenance (PdM) programs, forecasting component failures (e.g., lamp burnout) to maximize equipment uptime and overall manufacturing yield.

The main challenges are the extremely high capital expenditure required for purchasing state-of-the-art LRTP and hybrid systems, coupled with the inherent technical complexity. These tools require highly specialized maintenance, continuous calibration, and sophisticated process development expertise to manage the sensitive thermal recipes necessary for advanced semiconductor device fabrication, posing barriers for smaller or less experienced manufacturing facilities.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.