ID : MRU_ 433640 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

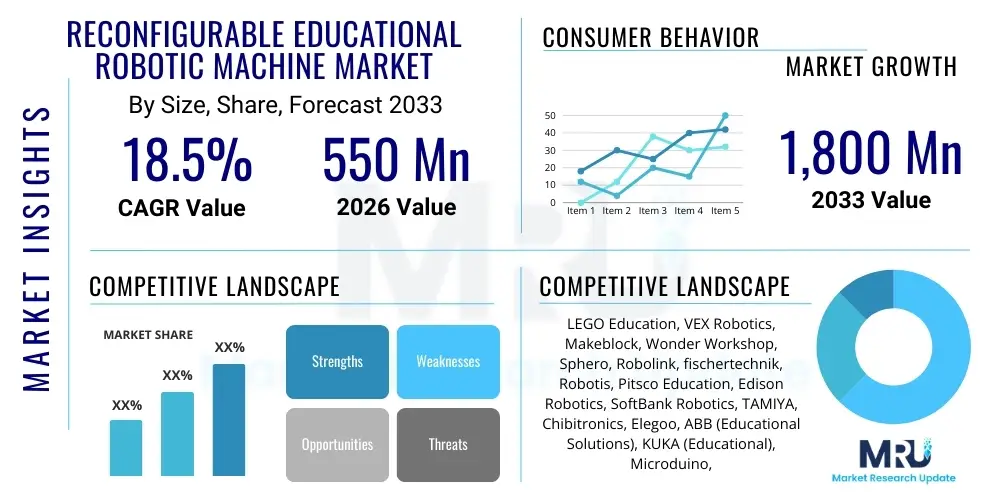

The Reconfigurable Educational Robotic Machine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at USD 550 Million in 2026 and is projected to reach USD 1,800 Million by the end of the forecast period in 2033.

The Reconfigurable Educational Robotic Machine Market encompasses sophisticated modular robotic kits and systems specifically designed to teach Science, Technology, Engineering, and Mathematics (STEM) concepts, computer programming, and computational thinking. These systems distinguish themselves from traditional fixed-design educational robots by offering users the flexibility to rapidly change the robot's physical structure, functionality, and sensory inputs without needing extensive redesign or manufacturing time. This modularity allows students to explore complex mechanical principles, advanced sensor integration, and diverse algorithmic approaches through iterative prototyping, significantly enhancing the learning experience across various educational levels, from primary schools to higher research institutions. The inherent versatility of these machines supports a project-based learning curriculum, enabling educators to address a broader range of topics using a single, adaptable platform, thereby maximizing return on investment for educational institutions.

The primary product offerings in this market segment include modular hardware components such as specialized motors, actuators, advanced microcontrollers, standardized connector interfaces, and a variety of sensors (vision, touch, distance, gyroscope). Coupled with the physical hardware is the robust software ecosystem, which typically involves visual programming languages (like Scratch or block-based interfaces) for beginners, transitioning smoothly to text-based coding environments (such as Python or C++) for advanced learners. Major applications of reconfigurable educational robotic machines span competitive robotics (e.g., FIRST Robotics), personalized learning environments, vocational training for industrial automation, and specialized research in AI and machine learning. The demand is heavily influenced by global educational reform initiatives prioritizing digital literacy and practical STEM application, alongside governmental funding for educational technology procurement.

The core benefit driving the market's expansion is the unparalleled ability of these machines to bridge theoretical knowledge with practical, hands-on application, fostering critical 21st-century skills like problem-solving, teamwork, and systematic debugging. Unlike single-purpose kits, reconfigurable systems allow for the simulation of real-world industrial or research scenarios, preparing students for future careers in advanced manufacturing, robotics engineering, and software development. Key driving factors include the escalating integration of artificial intelligence into learning platforms, the need for cost-effective teaching tools that evolve with the curriculum, and increasing parental awareness regarding the importance of early exposure to advanced technological concepts. Furthermore, the accessibility features and standardized platforms offered by leading vendors lower the entry barrier for schools with limited resources, accelerating global adoption rates.

The Reconfigurable Educational Robotic Machine Market is poised for substantial growth driven by favorable business trends centered around digital transformation in education and the persistent global shortage of skilled STEM professionals. Business trends indicate a strong shift towards subscription-based software models accompanying hardware sales, offering continuous curriculum updates and access to cloud-based simulation environments, improving vendor profitability and customer retention. Furthermore, strategic partnerships between technology providers and major curriculum developers are becoming crucial for market penetration, ensuring alignment between robotic platform capabilities and pedagogical objectives. Key segments driving revenue include K-12 institutions, which are adopting modular systems to introduce fundamental coding and engineering concepts, and higher education, which utilizes these platforms for advanced research in swarm robotics and dynamic control systems. The competitive landscape is characterized by innovation in connector technology and software usability, with companies focusing on platforms that minimize assembly time and maximize lesson engagement, emphasizing robustness and cross-compatibility with established educational tools.

Regionally, North America maintains market leadership primarily due to high technology adoption rates, significant private and public investment in STEM education initiatives, and the presence of numerous specialized robotics education providers and competitive leagues. However, the Asia Pacific (APAC) region is projected to exhibit the fastest Compound Annual Growth Rate (CAGR), fueled by massive governmental expenditure on modernization of educational infrastructure in economies like China, India, and South Korea, where robotics education is often mandated at the national level. Europe follows closely, driven by initiatives like Horizon Europe focusing on digital skills development and the strong institutional backing for vocational and technical training. Segment trends underscore the increasing preference for modular hardware platforms that offer visual programming interfaces, particularly in elementary and middle schools, while high schools and universities prioritize systems compatible with industrial programming standards and simulation software. Services—including teacher training and technical support—are emerging as a high-growth segment, essential for maximizing the effective deployment and utilization of these complex machines in varied educational settings.

The market faces operational challenges related to the initial cost outlay for institutions and the need for standardized training protocols for educators, which is currently being mitigated through the development of intuitive interfaces and comprehensive support ecosystems. Innovation is rapidly converging on integrating elements of Artificial Intelligence and Machine Learning into the robotic curriculum itself, allowing students to program robots not just to follow instructions, but to learn and adapt to their environment. This trend ensures the long-term relevance of reconfigurable robotic platforms in preparing students for an AI-driven future. Overall, the market outlook is overwhelmingly positive, characterized by expanding geographical reach, increasing product sophistication, and strong foundational support from policy makers and technological advancements aimed at democratizing high-quality STEM education globally.

Common user inquiries regarding AI's influence on the Reconfigurable Educational Robotic Machine Market center on how AI will transform curriculum content, enhance the robotic platforms themselves, and whether these systems can effectively teach advanced concepts like machine learning (ML) and deep learning (DL). Users frequently ask about the necessary computing power and software frameworks required for integrating complex AI algorithms into simple educational robots, and they express concerns regarding data privacy and the ethical implications of teaching AI to young students. Furthermore, educators are keen to understand how AI tutors or adaptive learning algorithms can be embedded within the robotic systems to personalize the educational trajectory for each student. The core theme is the expectation that these machines must evolve rapidly from tools for teaching basic programming to interactive, AI-enabled learning companions capable of demonstrating and teaching autonomous decision-making, predictive analytics, and natural language processing, thus preparing students for the advanced computational challenges of the next decade.

The integration of AI fundamentally redefines the scope of educational robotics, moving the focus from traditional control systems and simple sequential programming to sophisticated intelligent behavior modeling. Reconfigurable educational robots serve as ideal physical platforms for teaching AI because their modular nature allows students to quickly add necessary components like vision sensors, specialized microcontrollers (e.g., those optimized for edge computing), and high-fidelity sensory feedback mechanisms necessary for real-time AI implementation. This capability allows students to run practical experiments involving computer vision, reinforcement learning, and object recognition, providing immediate, tangible results of their algorithmic work. The transition is driving demand for specific sub-segments, including educational kits featuring specialized AI-enabled microprocessors and cloud-based simulation environments that provide access to large datasets necessary for practical ML training, all while mitigating the high computational demands on local institutional hardware.

The primary effect of AI integration is the diversification of market offerings, prompting vendors to develop comprehensive, scaffolded curricula that introduce ML concepts progressively. For instance, beginners might use block-based interfaces to train a robot to categorize simple objects, while advanced users utilize frameworks like TensorFlow Lite or PyTorch to build neural networks that enable autonomous navigation or complex task execution. This shift significantly elevates the perceived value of reconfigurable systems, positioning them not just as engineering tools but as essential platforms for AI literacy. The market growth is increasingly correlated with the sophistication of embedded AI features and the quality of the supporting curriculum, ultimately transforming educational robotics into the foundational layer for future AI practitioners and researchers.

The market dynamics of Reconfigurable Educational Robotic Machines are fundamentally shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), all acting under the influence of powerful external forces. Key drivers include widespread global recognition of the necessity for STEM skills, resulting in robust governmental mandates and funding allocations for integrating educational robotics from elementary school levels upwards. The inherent flexibility and reusability of these systems provide a compelling economic advantage over fixed-function kits, appealing to institutions facing budget constraints but requiring versatile, long-term technological assets. Concurrently, rapid technological advancements, especially in standardized connector technologies and high-performance, cost-effective microcontrollers, continually improve the accessibility and capability of these educational platforms. The rising popularity of international robotics competitions also serves as a strong market accelerator, encouraging student participation and driving demand for advanced, highly customizable hardware.

Conversely, the primary restraints center on the significant initial capital investment required to equip laboratories and the persistent challenge of teacher training and professional development. Many educators lack the necessary background or confidence to effectively integrate complex robotic curricula into standard lessons, leading to underutilization of expensive resources. Standardization remains an issue; while reconfigurability is a driver, the lack of universally accepted modular standards across different vendors can create vendor lock-in and complicate resource sharing between different school districts. Furthermore, the rapid obsolescence cycle of associated software and computing hardware necessitates frequent updates, imposing ongoing maintenance costs that strain long-term educational budgets, particularly in developing economies.

Opportunities for market expansion are abundant, particularly through strategic geographical penetration into emerging markets in APAC and Latin America, where digital education infrastructure is rapidly expanding. The development of specialized educational content focused on cutting-edge fields like quantum computing, biotechnology, and advanced AI using these platforms presents a lucrative niche. Furthermore, the transition to hybrid learning models post-pandemic has created a demand for sophisticated remote-controlled and simulation-integrated robotic platforms that facilitate hands-on learning outside traditional classroom settings. The major impact forces include technological forces (rapid evolution of AI and sensors), economic forces (fluctuations in educational funding and procurement policies), and socio-cultural forces (increasing parental and societal pressure for digital literacy and high-quality STEM outcomes), all pushing the market towards more integrated, sophisticated, and user-friendly solutions that can quickly adapt to changing pedagogical needs and technological landscapes.

The Reconfigurable Educational Robotic Machine Market is comprehensively segmented based on component type, robot configuration, application area, and the target end-user demographic, allowing for precise market sizing and strategic targeting. This detailed segmentation reveals nuances in purchasing behavior and technological requirements across the educational spectrum. Component segmentation, covering hardware, software, and services, demonstrates that hardware remains the largest revenue generator, but software subscriptions (for coding environments and curriculum access) and professional services (for teacher training) are the fastest-growing segments, signaling a shift toward holistic educational ecosystems rather than just physical products. Robot configuration differentiates between purely modular kits, where components are designed for endless rearrangement, and hybrid systems, which combine standardized base platforms with reconfigurable appendages and sensor arrays, each catering to different levels of educational complexity and budget constraints. The application analysis confirms STEM education and competitive robotics as key drivers, emphasizing the demand for platforms capable of rigorous, performance-based tasks.

The critical segmentation by end-user—ranging from K-12 (primary and secondary education) to higher education (universities and vocational schools)—highlights distinct needs. K-12 requires robust, block-based programming systems with intuitive connectors to ensure accessibility for younger learners and generalist educators, focusing on foundational concepts. Conversely, higher education demands open-source compatibility, high-level programming language support (Python, ROS), and the ability to integrate advanced components suitable for specialized research, such as complex motion planning or vision processing. Understanding these divergent needs is essential for market participants to tailor their product development and distribution strategies. The increasing role of hobbyists and personal learning, often driven by maker spaces and online educational platforms, forms an emerging, yet highly influential, micro-segment that demands affordability and strong community support, often favoring fully open-source hardware designs.

Further segmentation by geographic region provides crucial insight into varied regulatory environments and funding mechanisms. North America and Europe possess mature markets characterized by high per-student technology spending and sophisticated purchasing protocols, while APAC offers immense volume growth potential due to expansive national educational policies and massive student populations. The market structure, therefore, is not monolithic but a mosaic of localized educational needs, technological readiness, and budgetary capacities. Successful market penetration necessitates offering a scalable product portfolio that addresses both the budget-conscious K-12 schools in developing regions and the high-performance research laboratories in established economies, ensuring that the platform’s core reconfigurability remains a central, unifying selling proposition across all segments.

The value chain for the Reconfigurable Educational Robotic Machine Market begins with upstream activities focused on the design and sourcing of specialized components. Upstream analysis involves the procurement of high-quality, standardized electronic components (microcontrollers, motors, batteries) and the manufacturing of proprietary modular structural elements, often utilizing advanced materials like specialized polymers or lightweight metals to ensure durability and ease of assembly. Key upstream challenges include maintaining component standardization to ensure interoperability and managing the rapid obsolescence of semiconductor technology. Suppliers of microprocessors optimized for educational applications and manufacturers specializing in highly durable, child-safe structural plastics hold significant bargaining power in this phase. Innovation in quick-connect mechanisms and sensor fusion techniques is crucial here, aiming to reduce manufacturing complexity and increase product robustness in demanding educational environments.

The middle stage of the value chain encompasses assembly, software development, and intellectual property creation. Vendors invest heavily in developing proprietary educational software—covering both block-based and text-based programming environments—and creating comprehensive, age-appropriate curriculum content that maximizes the utility of the reconfigurable hardware. This stage is characterized by intense intellectual property competition regarding user interface design, adaptive learning algorithms, and the integration of third-party educational tools. Direct distribution channels, such as selling directly to institutional procurement offices, allow vendors greater control over the messaging and installation process, providing higher margins and facilitating direct feedback for product iteration. Indirect channels, primarily relying on educational distributors, specialized resellers, and e-commerce platforms, are essential for widespread geographical reach, particularly to smaller schools and individual consumers/hobbyists, requiring strong partnership management to ensure consistent quality of pre-sales consultation and after-sales support.

Downstream analysis focuses on deployment, educator professional development, and continued ecosystem support, which significantly influences the total cost of ownership and long-term customer satisfaction. Effective deployment involves not only the physical delivery of hardware but also the technical setup and integration within existing school IT infrastructures. The services segment (teacher training) is a crucial downstream activity, as successful market adoption relies entirely on the educators’ confidence and ability to deliver the curriculum effectively. Ongoing content updates and technical support ensure the platform remains relevant as educational standards and technology evolve. The performance of downstream partners—namely certified trainers and technical support teams—is a key determinant of market success, ensuring institutions maximize their investment in these sophisticated educational tools.

The primary customer base for Reconfigurable Educational Robotic Machines is highly segmented across institutional and individual buyers, unified by the objective of enhancing STEM and digital literacy. The largest segment comprises K-12 educational institutions, which includes public, private, and charter schools globally. These customers are typically driven by curriculum mandates, seeking scalable and affordable systems that can cater to large student groups and integrate seamlessly into existing curricula, with purchase decisions often influenced by governmental funding cycles and district-wide technology initiatives. Specific needs for K-12 include ruggedized designs, intuitive block-based programming interfaces, and comprehensive teacher training packages, viewing the robotic systems as long-term foundational teaching assets.

A secondary, yet highly influential, customer segment is Higher Education and Vocational Training Centers. Universities and technical colleges purchase these machines for specialized engineering programs, robotics research, and advanced prototyping laboratories. Their procurement criteria emphasize open-source compatibility, support for industrial-standard programming languages (like ROS), high-fidelity sensing capabilities, and the capacity for integrating custom components, often prioritizing technical sophistication and research potential over sheer simplicity. This segment frequently demands specialized, high-throughput systems capable of simulating complex real-world scenarios, such as autonomous vehicles or industrial automation processes, often purchasing smaller quantities of higher-value, technically complex platforms.

The rapidly growing niche of individual consumers, including parents, homeschooling communities, and participants in the "maker movement," forms the third key customer group. These buyers prioritize affordability, ease of access to online resources and community support, and robust integration with personal computing devices. Their purchasing decisions are often driven by direct educational outcomes for their children or personal interest in robotics, programming, and engineering hobbies. Furthermore, non-traditional educational settings, such as after-school programs, science museums, and competitive robotics organizations (e.g., FIRST, VEX), represent significant bulk buyers who require platforms specifically designed for rapid, complex assembly and rigorous, high-stakes operational performance under competitive pressure.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 550 Million |

| Market Forecast in 2033 | USD 1,800 Million |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | LEGO Education, VEX Robotics, Makeblock, Wonder Workshop, Sphero, Robolink, fischertechnik, Robotis, Pitsco Education, Edison Robotics, SoftBank Robotics, TAMIYA, Chibitronics, Elegoo, ABB (Educational Solutions), KUKA (Educational), Microduino, SAM Labs, Modular Robotics, OWI Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological foundation of the Reconfigurable Educational Robotic Machine market is defined by four core areas: highly modular hardware components, sophisticated programming interfaces, advanced sensor technology, and seamless integration with cloud-based simulation and learning management systems (LMS). The modular hardware relies heavily on standardized, durable, and highly reliable connection mechanisms—such as magnetic connectors, standardized pin layouts, or unique interlocking plastic blocks—to ensure rapid, tool-free reassembly while maintaining electrical integrity. Microcontrollers used in these systems are increasingly powerful, migrating towards 32-bit architectures (like ARM Cortex-M series) capable of running complex real-time operating systems (RTOS) and executing sophisticated algorithms, including initial AI inference tasks directly on the device, significantly enhancing the learning scope beyond simple command execution. Furthermore, the trend toward open-source hardware standards, like those surrounding platforms such as Arduino and Raspberry Pi, provides flexibility and a vast community support ecosystem, lowering barriers to entry for customization and advanced development.

Software technologies are paramount, transitioning from basic drag-and-drop block coding interfaces (essential for K-6 learners) to fully integrated development environments (IDEs) supporting high-level textual languages like Python and JavaScript, often based on Robot Operating System (ROS) frameworks for university-level applications. Key technological innovation is focused on developing 'scaffolded' programming environments that allow learners to progress seamlessly from visual abstraction to complex code syntax within the same project ecosystem. Furthermore, the integration of simulation technology, often cloud-hosted, allows students to test complex code and robotic behaviors in a virtual environment before deployment, minimizing hardware damage and maximizing learning efficiency. These simulation tools are crucial for scenarios involving multiple agents (swarm robotics) or resource-intensive AI algorithms that might exceed the physical robot’s processing capacity, ensuring scalability in curriculum delivery.

Sensor technology and connectivity standards also play a critical role. Modern educational robots incorporate advanced sensor packages, including high-resolution cameras for computer vision, Lidar for mapping and navigation, and force/torque sensors for simulating tactile feedback in gripping tasks. The connectivity landscape is dominated by robust wireless communication protocols, primarily Bluetooth Low Energy (BLE) for local control and Wi-Fi for cloud integration and data logging. Future advancements are expected in incorporating technologies that enable multi-robot communication (crucial for teaching decentralized control and coordination) and better battery management systems that provide longer operational periods. Ultimately, the technology trajectory is focused on maximizing the robot’s instructional fidelity—the degree to which the educational platform accurately mirrors the capabilities and constraints of real-world industrial or research robotics, ensuring students are learning relevant, transferrable skills.

Reconfigurable robots feature modular components, allowing students to rapidly change the robot's physical structure and function (e.g., shifting from a wheeled vehicle to a robotic arm) using the same kit, promoting iterative design and diverse learning outcomes. Traditional robots are typically fixed-design platforms focused on specific, limited tasks.

These machines provide hands-on, project-based learning platforms that introduce complex concepts like engineering design, advanced programming, computational thinking, and physics in an engaging way. Their versatility allows a single investment to cover a wide spectrum of the STEM curriculum, preparing students for future technological careers.

Key trends include the integration of artificial intelligence (AI) and machine learning (ML) capabilities directly into the educational curriculum using these platforms, the adoption of open-source software frameworks like ROS, and the use of cloud-based simulation tools to enable advanced, complex robot programming and testing remotely.

The K-12 education segment (Primary and Secondary Schools) remains the largest volume driver, primarily due to global governmental mandates and funding prioritizing early exposure to digital literacy and foundational engineering concepts. Higher education demands are high in terms of technology sophistication but lower in volume.

The biggest restraint is the significant upfront capital investment required by educational institutions and the ongoing challenge of providing comprehensive, standardized professional development and training for educators who must integrate and teach with these complex, sophisticated technological tools effectively.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.