ID : MRU_ 434299 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

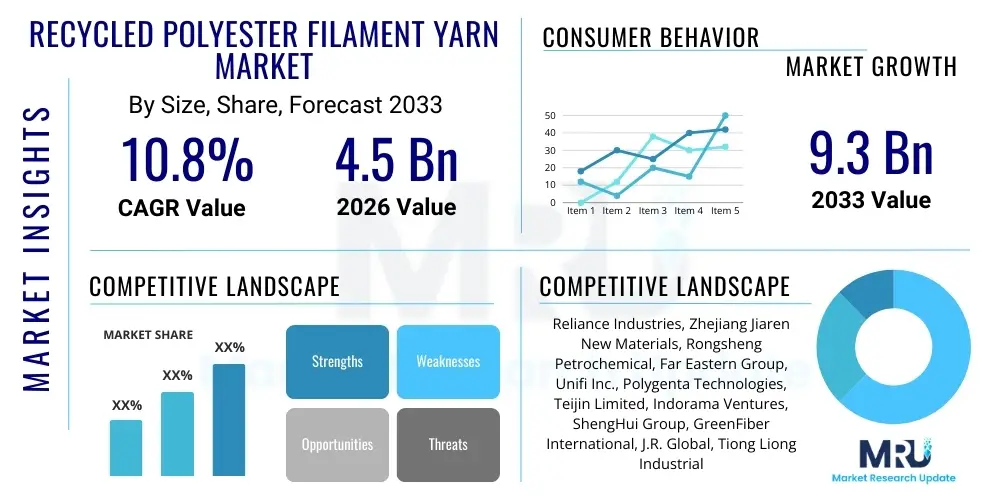

The Recycled Polyester Filament Yarn Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2026 and 2033. The market is estimated at USD 4.5 Billion in 2026 and is projected to reach USD 9.3 Billion by the end of the forecast period in 2033.

The Recycled Polyester Filament Yarn (RPFY) market encompasses the production and distribution of continuous filament yarn derived primarily from post-consumer or post-industrial PET waste, predominantly plastic bottles. This product serves as a sustainable alternative to virgin polyester, offering identical performance characteristics while significantly reducing reliance on fossil fuels and mitigating plastic pollution. RPFY is categorized based on luster (bright, semi-dull, full-dull) and end-use application, including apparel, home textiles, and automotive interiors. The primary driving factors for market expansion include the global push for circular economy models, increasing regulatory pressure on corporate sustainability reporting, and robust consumer demand for eco-friendly textile products. The inherent benefits of RPFY, such as reduced carbon footprint, resource conservation, and high versatility in knitting and weaving processes, solidify its critical role in modern supply chains, particularly within the fast-moving fashion and textile industries that are under intense scrutiny regarding their environmental impact. The technical maturity of mechanical and chemical recycling processes allows manufacturers to produce high-quality RPFY suitable for demanding performance applications, further expanding its market penetration across various industrial sectors.

The Recycled Polyester Filament Yarn (RPFY) market is witnessing accelerated growth, underpinned by significant shifts toward sustainable procurement practices across major industries. Business trends indicate strong capital expenditure in advanced sorting and purification technologies, enabling the production of high-grade, food-contact compliant recycled material, thus expanding RPFY applications beyond conventional textiles into specialized non-woven and technical fabrics. Regionally, Asia Pacific maintains market dominance due to its robust manufacturing base and significant installed capacity for PET recycling, although Europe and North America are exhibiting the highest growth rates, driven by stringent legislative mandates like the EU Green Deal and strong brand commitments to incorporate traceable sustainable materials. Segment trends reveal that the semi-dull category remains highly popular due to its versatility in apparel manufacturing, while the application segment is increasingly diversified, with sportswear and activewear emerging as primary consumers due to the necessity for performance fabrics that also meet sustainability targets. The overall market trajectory confirms a strong positive feedback loop between regulatory incentives, technological advancements in depolymerization, and escalating corporate social responsibility (CSR) initiatives.

Common user questions regarding AI's impact on the Recycled Polyester Filament Yarn market primarily revolve around optimizing material sourcing, enhancing quality control consistency, and forecasting demand for recycled materials versus virgin materials. Users are highly interested in how Artificial Intelligence can improve the highly fragmented and complex waste collection logistics, ensuring a stable and contaminant-free feedstock supply (post-consumer PET bottles). Concerns center on the potential capital intensity required for adopting AI-driven sorting systems and the need for standardized data protocols across the recycling value chain. Expectations suggest AI will revolutionize optical sorting mechanisms, enabling higher purity levels of PET flakes crucial for high-quality filament spinning, simultaneously predicting regional waste availability to optimize plant operational capacity. Furthermore, AI tools are expected to play a vital role in supply chain transparency, using machine learning to track recycled content provenance from collection point to final yarn production, thereby substantiating sustainability claims for brand owners and combating greenwashing concerns prevalent in the textile sector, ultimately influencing procurement strategies and pricing models.

The market dynamics for Recycled Polyester Filament Yarn (RPFY) are principally governed by the confluence of legislative drivers favoring circularity and corporate demand for sustainable raw materials, contrasted by inherent logistical and quality constraints. Drivers include increasing global mandates for plastic waste reduction, significant brand commitments to eliminate virgin plastics, and the demonstrable economic and environmental benefits of recycling PET over primary production, which encourages competitive pricing. Restraints primarily involve the volatile availability and pricing of high-quality PET bottle bales, which are susceptible to regional collection efficiencies and economic fluctuations, alongside the necessity for substantial, capital-intensive infrastructure upgrades required to achieve the necessary purity for closed-loop, high-grade filament production. Opportunities are abundant, rooted in the maturation of chemical recycling technologies (depolymerization), which can handle mixed or low-quality waste streams and produce materials identical to virgin inputs, alongside the rapid expansion of RPFY usage in lucrative, specialized markets such as performance apparel, automotive textiles, and geo-synthetics, where premium pricing justifies the sustainability advantage. The combined effect of these impact forces ensures sustained market growth but underscores the importance of supply chain resilience and technological innovation.

The Recycled Polyester Filament Yarn market is segmented primarily based on product characteristics, encompassing luster and technical specifications, and secondly by end-use application, which reflects the diverse industries consuming RPFY. Product segmentation differentiates yarn types by their visual properties, affecting their suitability for various textile finishes, while application segmentation highlights the key consumption sectors, from mass-market apparel to niche industrial uses. The dominant segmentation factor remains the source of the recycled PET (post-consumer versus post-industrial waste), which heavily influences the yarn's purity and inherent cost structure, directly impacting final market price and perceived quality. The granular segmentation allows producers to tailor RPFY characteristics, such as denier per filament (DPF) and tenacity, to meet the specific performance requirements of sophisticated end-users, driving differentiated product offerings and sustaining premiumization within high-demand sustainable niches.

The value chain for Recycled Polyester Filament Yarn (RPFY) is complex, commencing with the upstream collection and sorting of Polyethylene Terephthalate (PET) waste, primarily post-consumer bottles. This upstream stage is highly dependent on municipal waste management infrastructure, bottle deposit schemes, and the efficiency of Material Recovery Facilities (MRFs). Efficient collection is paramount because the purity and consistency of the feedstock directly dictate the quality and cost-effectiveness of the final RPFY product. Key activities in the upstream segment include baling, transportation, and sophisticated washing and flaking, often leveraging optical sorters to minimize contamination from PVC, HDPE, and other plastics. The subsequent middle stage involves the manufacturing process itself: converting PET flakes into recycled chips (rPET), followed by extrusion and spinning into filament yarn. Integration between large recyclers and yarn producers is increasingly common, aiming to secure reliable, high-quality chip supply and optimize the energy-intensive spinning process, which is critical for cost control and maintaining yarn specifications required by downstream converters. This stage also includes quality assurance checks to ensure tenacity, elongation, and dye uptake meet stringent textile industry standards, often requiring specialized additives or purification steps, particularly for continuous filament yarn production used in high-performance applications.

The downstream segment of the RPFY value chain focuses on distribution and final consumption. Distribution channels are highly structured, relying on a global network of yarn agents, traders, and direct sales teams catering to large textile mills and brand owners. Direct relationships between RPFY producers and major apparel or automotive manufacturers are growing in importance, driven by the need for verifiable sustainability claims and secure, long-term supply agreements. The end-users, comprising textile manufacturers, knitters, weavers, and non-woven specialists, convert the RPFY into fabrics and finished goods. Indirect distribution involves smaller regional distributors who cater to decentralized manufacturing hubs, whereas direct distribution, often preferred by Tier 1 automotive suppliers or major global fashion retailers, ensures better control over inventory, quality, and compliance with specific brand protocols, particularly related to recycled content certification. The increasing demand for traceability and compliance with standards like the Global Recycled Standard (GRS) places significant pressure on all value chain actors to maintain robust documentation and certification procedures throughout every stage, adding transactional complexity but ensuring market integrity.

A critical consideration in the distribution channel strategy is the balance between cost optimization and maintaining transparency. While container shipping remains the dominant logistics mode for global distribution, the proximity of recycling facilities to textile manufacturing clusters, particularly in Asia Pacific, minimizes transportation costs and associated environmental impact. Direct distribution channels facilitate quicker feedback loops regarding yarn performance and quality, enabling producers to rapidly adjust manufacturing parameters. Conversely, reliance on indirect channels through intermediaries helps penetrate fragmented regional markets but introduces additional margin stack-ups and potential dilution of traceability information. The continuous evolution toward chemical recycling offers a long-term shift potential, as chemically derived monomers offer superior quality consistency, potentially simplifying the midstream processing but requiring greater capital expenditure and establishing new standards for chemical recycling infrastructure feedstock collection, distinct from traditional mechanical recycling flows.

The primary potential customers for Recycled Polyester Filament Yarn (RPFY) are large-scale textile manufacturers, specifically those specializing in knitting and weaving processes for apparel and home furnishings. Within the apparel sector, the most significant demand originates from activewear, sportswear, and performance textile brands, which leverage the inherent properties of polyester, such as moisture-wicking and durability, combined with the strong sustainability narrative of RPFY. These brands, including major global athletic wear companies, are under intense public and investor pressure to meet ambitious targets for incorporating recycled or sustainable fibers into their product lines, making them high-volume, strategic buyers. The versatility of RPFY allows it to replace virgin polyester seamlessly across various fabric weights and finishes, ensuring that textile mills catering to these high-growth segments represent the core consumer base requiring long-term, stable contracts for certified RPFY supply. The decision-making unit often includes procurement specialists, sustainability officers, and R&D fabric engineers focused equally on cost-per-unit, technical performance specifications, and verifiable GRS certification.

A second major customer segment includes manufacturers serving the home furnishings and interior textile markets, such as producers of curtains, upholstery fabrics, carpets, and bedding materials. While the growth rate in this sector may be slower than in apparel, the volume requirements are substantial, driven by increasing consumer awareness regarding sustainable living and the adoption of green building standards which often favor recycled content. These customers seek RPFY primarily for its durability, resistance to fading, and stable pricing relative to natural fibers, integrating the recycled aspect as a key marketing differentiator. The automotive sector forms another critical, albeit technically demanding, customer base, utilizing RPFY for interior components like seat covers, headliners, and trunk linings. Automotive OEMs mandate extremely high standards for lightfastness, abrasion resistance, and flame retardancy, requiring specialized, often higher-denier, RPFY variants. Penetrating this segment requires suppliers to adhere to rigorous automotive industry quality management systems, necessitating sophisticated production and certification capabilities that often involve partnerships with specialized Tier 1 suppliers who manage the conversion process.

Furthermore, specialized industrial textile producers represent a rapidly expanding customer group. This includes manufacturers of non-woven fabrics, geotextiles used in civil engineering (for soil stabilization and filtration), and various technical textiles such as ropes, conveyor belts, and filtration media. For these industrial applications, the mechanical properties of RPFY—high tenacity and durability—are prioritized over aesthetic appeal. The use of recycled content provides a cost advantage in high-volume, non-consumer facing products while aligning the procuring company with broader industry mandates for resource efficiency. The key characteristic across all these diverse customer segments remains the requirement for verifiable sustainability credentials and performance parity with virgin polyester. Suppliers must therefore focus not just on efficient yarn production but also on maintaining robust traceability systems and achieving internationally recognized sustainability certifications to satisfy the evolving demands of sophisticated global buyers who prioritize environmental, social, and governance (ESG) performance metrics.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 9.3 Billion |

| Growth Rate | 10.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Reliance Industries, Zhejiang Jiaren New Materials, Rongsheng Petrochemical, Far Eastern Group, Unifi Inc., Polygenta Technologies, Teijin Limited, Indorama Ventures, ShengHui Group, GreenFiber International, J.R. Global, Tiong Liong Industrial Co., Ltd., Sarla Performance Fibers, Nan Ya Plastics, Sateri, Alok Industries, Xinfengming Group, Hangzhou Huaqing, FENC, Tonak. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape governing the Recycled Polyester Filament Yarn (RPFY) market is centered primarily on two dominant methods for converting PET waste into usable polymer chips: mechanical recycling and chemical recycling. Mechanical recycling, the most mature and widely adopted technology, involves cleaning, sorting, shredding, melting, and repolymerizing post-consumer PET bottles into rPET chips. Advances in mechanical recycling are focused on improving the sorting stage, specifically through high-resolution near-infrared (NIR) and optical sorting technology, often integrated with AI, to remove contaminants more effectively. This technological refinement is crucial for increasing the purity of the rPET chips, enabling them to be spun into fine denier filament yarn suitable for high-end textile applications, a goal previously difficult to achieve due to inherent color variations and reduced intrinsic viscosity (IV) of mechanically recycled PET. Innovations in solid-state polymerization (SSP) processes applied to rPET chips are also vital for boosting the molecular weight and tenacity of the polymer, ensuring the final RPFY possesses performance characteristics that are comparable to virgin polyester.

The emerging frontier in RPFY production is chemical recycling, encompassing technologies like glycolysis, methanolysis, hydrolysis, and ammonolysis (depolymerization). These processes break down the PET polymer chain back into its original monomers (e.g., PTA and MEG), effectively purifying the material to a virgin-equivalent state, regardless of the initial quality or complexity of the waste stream (including difficult-to-recycle textile waste). Chemical recycling addresses the quality ceiling limitations of mechanical processes and opens up the potential for truly closed-loop textile-to-textile recycling, which is a major long-term sustainability goal for the fashion industry. While currently more capital and energy-intensive than mechanical methods, significant investments are being channeled into scaling up these chemical technologies, which promise an inexhaustible supply of high-purity raw material for premium RPFY. The technological focus here is on developing catalysts and reactor designs that lower operational costs and improve the energy efficiency of the depolymerization process, making it commercially viable for large-scale yarn production.

Beyond the core recycling methodologies, advancements in filament spinning technology itself play a crucial role. Modern RPFY plants employ high-speed spinning (HSS) and partially oriented yarn (POY) production lines optimized for handling rPET polymers. These lines feature specialized filtration systems to manage the minor impurities that may remain in the recycled material without disrupting the delicate spinning process. Furthermore, texturing processes, primarily using the Draw Texturing Machine (DTY) process, are being refined to enhance the bulk, stretch, and aesthetic properties of the final yarn, ensuring it meets the soft-hand feel and performance requirements of contemporary apparel. Traceability technology, often involving embedded digital markers, specialized dyes, or blockchain integration, is rapidly becoming a standard technological component. This verifies the percentage of recycled content throughout the supply chain, moving from a niche requirement to an essential technological prerequisite for securing contracts with major global brands that demand audited evidence of their sustainability claims, thus completing the technological ecosystem necessary for a robust RPFY market.

The principal source material is post-consumer polyethylene terephthalate (PET) plastic waste, predominantly discarded beverage bottles, which are mechanically or chemically recycled and processed into polymer chips for filament spinning.

High-grade RPFY, especially that produced using advanced mechanical sorting or chemical recycling methods, exhibits performance characteristics—such as tenacity, elongation, and dye uptake—that are virtually equivalent to virgin polyester, making it suitable for high-performance applications like activewear.

The core advantages include a significantly reduced carbon footprint, lower consumption of non-renewable fossil fuel resources, and diversion of plastic waste from landfills and oceans, supporting circular economy objectives while maintaining product performance.

Asia Pacific, particularly manufacturing hubs in China, India, and Taiwan, dominates the global production and supply of RPFY due to extensive installed textile and recycling capacity and established supply chains for global brands.

Chemical recycling is critical for market expansion as it enables the reprocessing of complex, contaminated, or mixed textile waste back into virgin-quality monomers, overcoming quality limitations of traditional mechanical recycling and supporting true textile-to-textile circularity.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.