ID : MRU_ 431609 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

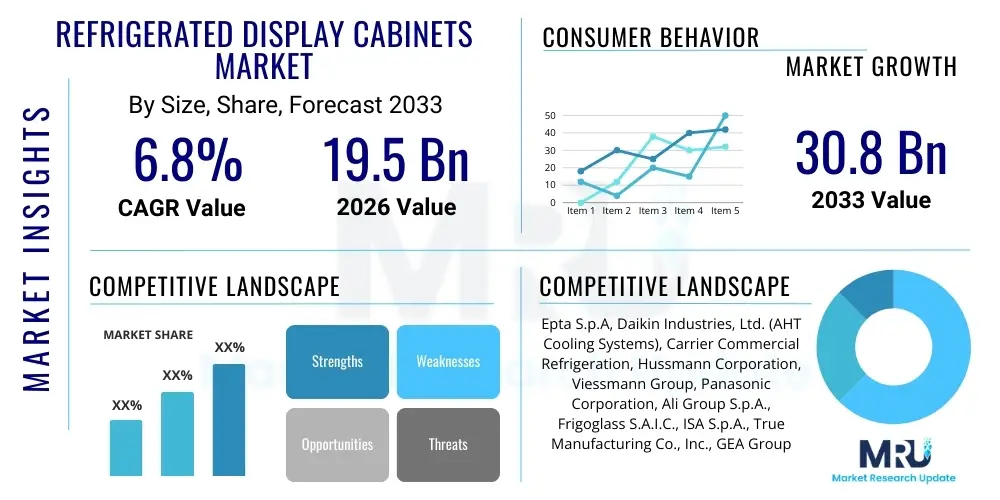

The Refrigerated Display Cabinets Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 19.5 Billion in 2026 and is projected to reach USD 30.8 Billion by the end of the forecast period in 2033.

The Refrigerated Display Cabinets (RDCs) Market encompasses specialized commercial refrigeration equipment designed primarily for storing, preserving, and visually merchandising perishable food and beverage products within retail environments. These cabinets are foundational to modern food retail, ranging from small-format convenience stores to large hypermarkets, providing critical temperature control necessary for maintaining product quality and extending shelf life. The core function of RDCs is to balance optimal preservation parameters with consumer accessibility and aesthetic presentation, utilizing technologies such as advanced insulation materials, high-efficiency compressors, and integrated lighting systems.

The product portfolio includes a diverse range of units such as multideck cabinets, serve-over counters, island freezers, and glass-door merchandisers, categorized mainly into plug-in (self-contained) and remote systems. Major applications span across grocery stores, supermarkets, convenience stores, quick-service restaurants, and specialized food outlets like bakeries and butcher shops. The principal benefits derived from the adoption of modern RDCs include significant reductions in energy consumption, enhanced food safety compliance through precise temperature monitoring, and improved product visibility which directly correlates with impulse purchases and sales growth in the retail sector.

Key driving factors currently propelling market expansion include the global proliferation of organized retail formats, the escalating consumer demand for ready-to-eat and frozen foods requiring stringent cold chain logistics, and increasingly rigorous governmental regulations mandating the transition toward environmentally sustainable refrigerants (e.g., natural refrigerants like CO2, hydrocarbons). Furthermore, technological advancements centered on smart refrigeration and connectivity, enabling remote diagnostics and predictive maintenance, are fundamentally reshaping the operational efficiency and total cost of ownership of these essential retail assets.

The global Refrigerated Display Cabinets (RDC) Market is experiencing robust expansion driven by structural shifts in the retail landscape and heightened focus on sustainability and energy efficiency. Business trends are dominated by the push towards natural refrigerant systems, particularly those utilizing CO2 and propane, positioning compliance and environmental stewardship as non-negotiable competitive advantages. Manufacturers are heavily investing in smart refrigeration technologies, integrating IoT sensors, and cloud-based monitoring platforms to provide retailers with real-time operational insights, optimizing energy usage and reducing food spoilage, thereby delivering a compelling return on investment.

Regional trends indicate that the Asia Pacific (APAC) region is projected to register the fastest growth, fueled by rapid urbanization, increasing disposable incomes, and the widespread establishment of Western-style supermarket chains and convenience store networks, particularly in developing economies like China and India. While North America and Europe remain mature markets, growth there is sustained primarily by replacement cycles driven by strict energy performance standards and the retrofit requirement for ozone-depleting refrigerants. Europe, specifically, is leading innovation in CO2 booster systems due to proactive regulatory initiatives such as the F-Gas Regulation.

Segmentation trends highlight the increasing demand for remote refrigerated display cabinets in large retail settings, owing to their superior energy efficiency and heat rejection capabilities compared to self-contained units. The multideck and vertical cabinets segments are witnessing rapid adoption due to their efficient use of floor space and enhanced visual merchandising appeal for packaged goods. Concurrently, the rise of discount retail and hard-discounters is driving demand for cost-effective, high-volume refrigerated island cases and chest freezers, focusing on frozen and bulk commodities.

Common user questions regarding AI’s impact on RDCs frequently center on optimizing energy consumption, enhancing predictive maintenance capabilities, and improving inventory accuracy. Users are keen to understand how AI algorithms can process vast amounts of data—including ambient temperature, door openings, compressor performance, and sales data—to dynamically adjust cooling cycles, thus minimizing energy waste and maximizing equipment longevity. Concerns often revolve around the initial investment required for AI integration, data privacy, and the complexity of integrating advanced algorithms into existing legacy infrastructure. Users expect AI to move RDC management from reactive repair to proactive, condition-based monitoring, ultimately reducing downtime and operating costs significantly. The summarization of these queries points toward a strong expectation that AI will transform RDCs from passive storage units into intelligent, energy-saving assets central to the digital retail ecosystem.

The integration of Artificial Intelligence (AI) and Machine Learning (ML) into Refrigerated Display Cabinets is rapidly transitioning from conceptual development to commercial application, primarily focusing on operational efficiency and predictive analytics. AI models analyze complex refrigeration system parameters, allowing for highly granular control over variables such as defrost schedules, fan speeds, and compressor modulation based on real-time factors like store traffic patterns, external weather conditions, and precise internal temperature load fluctuations. This dynamic optimization ensures that the cabinet operates only at the necessary intensity, leading to substantial energy savings—often cited as up to 20% compared to traditional controls—and extending the lifespan of critical components by reducing unnecessary strain.

Furthermore, AI algorithms are playing a pivotal role in optimizing inventory management and merchandising within RDCs. By integrating with point-of-sale (POS) systems and image recognition technology, AI can monitor stock levels, identify potential out-of-stock events, and even analyze shopper interaction patterns (e.g., dwell time near a cabinet) to inform product placement and pricing strategies. This convergence of operational efficiency and retail strategy positions AI-enabled RDCs as crucial tools not only for preservation but also for maximizing profitability per square foot of refrigerated space, providing retailers with actionable insights previously unattainable through conventional monitoring systems.

The Refrigerated Display Cabinets (RDCs) market dynamics are powerfully shaped by a confluence of regulatory mandates, technological innovations, and evolving consumer habits, summarized by its key Drivers, Restraints, and Opportunities (DRO). The primary impact forces currently driving the market include stringent global environmental regulations, particularly the phase-down of hydrofluorocarbon (HFC) refrigerants under initiatives like the Kigali Amendment, which forces manufacturers and retailers to invest in new, compliant equipment utilizing natural refrigerants (Drivers). Conversely, the significant upfront investment required for these technologically advanced and sustainable cabinets, coupled with the complexity of retrofitting existing infrastructure, acts as a major Restraint, particularly for smaller independent retailers with limited capital expenditure budgets. The greatest Opportunity lies in the rapid growth of modern, organized retail in emerging economies, coupled with the ongoing shift toward e-commerce and subsequent demand for small, high-efficiency RDCs for hyperlocal distribution hubs and dark stores, creating new demand channels beyond traditional supermarkets.

Specific market drivers contributing to accelerated growth include the rising consumer awareness regarding food safety and quality, which necessitates reliable and consistent temperature control across the supply chain, translating directly into demand for high-performance RDCs with advanced monitoring capabilities. Furthermore, the pervasive trend of retail modernization, where competitive pressures necessitate aesthetically appealing and energy-efficient display solutions to enhance the in-store shopping experience and reduce operational costs, continuously fuels the replacement market. The mandatory transition to refrigerants like CO2 and R290, while initially costly, serves as a powerful long-term driver by ensuring regulatory compliance and achieving corporate sustainability goals, often supported by government incentives or carbon taxation mechanisms.

However, the market faces significant restraints related to supply chain volatility, fluctuating raw material costs (especially metals and components like compressors), and the scarcity of skilled technicians capable of installing and maintaining complex natural refrigerant systems, particularly CO2-based booster systems. These restraints increase the operational complexity and raise the Total Cost of Ownership (TCO), particularly for initial adopters. Opportunities are abundant in areas such as remote monitoring and IoT integration, which allow service providers to offer value-added services like condition monitoring and preventative maintenance contracts, securing long-term revenue streams and mitigating retailer concerns regarding system complexity. Developing modular, scalable RDC solutions that simplify installation and maintenance remains a strategic opportunity for manufacturers aiming to penetrate fragmented markets effectively.

The Refrigerated Display Cabinets market is segmented based on several critical factors, including product type, configuration, type of refrigerant used, and the primary end-user application. Segmentation by product type primarily differentiates between vertical (multideck, usually open or with glass doors) and horizontal cabinets (island freezers, chest coolers), reflecting their suitability for specific product categories—vertical for beverages and prepared foods, and horizontal for frozen goods. Configuration segmentation, detailing whether the unit is plug-in (self-contained with an integrated condensing unit) or remote (connected to an external centralized refrigeration plant), is vital as it directly impacts energy consumption, noise levels, and store layout flexibility. The refrigerant type is increasingly important, distinguishing between traditional HFCs (being phased out) and natural alternatives (CO2, R290, R600a), reflecting compliance and environmental strategies.

The end-user segmentation is crucial, identifying the specific requirements of large retail formats (supermarkets, hypermarkets), which prioritize remote systems and energy efficiency, versus small retail formats (convenience stores, petrol stations), which typically rely on flexible, plug-in units. Furthermore, the segmentation analysis confirms that multideck RDCs and serve-over cabinets collectively dominate the market revenue share due to their widespread use in fresh food presentation, while the fastest growth is observed in glass-door vertical cabinets, favored for their superior energy efficiency over traditional open multideck designs. This evolving landscape necessitates manufacturers to offer a highly diversified portfolio capable of meeting the varied aesthetic, efficiency, and regulatory needs across the disparate retail spectrum.

The Value Chain for the Refrigerated Display Cabinets Market commences with the upstream activities, involving the sourcing of specialized raw materials and critical components. Upstream analysis focuses heavily on the procurement of highly efficient compressors (often variable speed drives), advanced heat exchangers, specialized insulation materials (e.g., polyurethane foam for minimized thermal leakage), tempered glass (for optimal visibility and reduced condensation), and sophisticated electronic controls. Fluctuations in the prices of key metals like copper and aluminum, necessary for refrigeration coils, directly influence manufacturing costs. Efficiency gains at this stage often involve strategic partnerships with component suppliers to integrate cutting-edge, energy-saving technologies early in the design cycle, specifically related to R290 or CO2 components which require higher pressure ratings and specialized safety standards.

The manufacturing and assembly stage involves high-precision sheet metal fabrication, welding, insulating, and integrating the complex refrigeration circuit, adhering strictly to global food safety and energy efficiency standards (like Energy Star or Ecodesign directives). Downstream analysis focuses on logistics, distribution channels, and installation. Due to the size and fragility of RDCs, specialized logistics are required. Distribution channels are highly segmented: large global retailers often deal directly with top-tier Original Equipment Manufacturers (OEMs), while smaller retailers typically purchase through a network of authorized distributors, wholesalers, or specialized refrigeration contractors who also provide essential installation and commissioning services.

The post-sale phase, which includes maintenance, servicing, and end-of-life management (including refrigerant recovery), constitutes a critical part of the downstream value chain. Direct sales are common for high-volume, standardized units, but indirect channels through distributors and contractors dominate regional markets, providing localized support and technical expertise necessary for complex remote systems, especially those using natural refrigerants. The shift toward servitization, where manufacturers offer RDCs as part of a temperature-as-a-service model, including remote monitoring and predictive maintenance contracts, is increasingly strengthening the downstream value capture for key market players.

The primary consumers and end-users of Refrigerated Display Cabinets are organizations operating within the modern food retail, grocery, and food service sectors that require controlled cold storage coupled with effective product merchandising. The largest segment of potential customers comprises large format retail chains, including multinational supermarket giants and regional hypermarket operators. These entities are consistently replacing older equipment to comply with evolving environmental regulations and pursue significant reductions in electricity consumption, focusing heavily on remote multi-deck systems and high-efficiency island freezers to manage vast quantities of perishable and frozen inventory effectively.

The rapidly expanding second tier of customers includes convenience stores, petrol station forecourts, and small, independent urban grocers. This segment primarily drives demand for plug-in, self-contained RDCs, valuing ease of installation, mobility, and aesthetically pleasing designs that encourage impulse purchases. The growth in urbanization and the proliferation of smaller retail footprints dedicated to fresh and ready-to-eat foods makes this segment highly attractive, demanding versatile cabinets optimized for quick turnover and minimal floor space utilization.

Furthermore, specialized food service operations and institutional buyers represent a growing niche. This includes gourmet bakeries, professional butcher shops, catering operations, and specialized beverage outlets. These customers require bespoke serve-over counter solutions and display units tailored for specific temperature zones and specialized product presentation (e.g., high humidity control for fresh meat). The emergent segment of dark stores and food delivery fulfillment centers, supporting online grocery platforms, also constitutes a significant future customer base, demanding robust, high-capacity, non-aesthetic RDCs focused purely on storage efficiency and rapid retrieval for cold chain logistics.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 19.5 Billion |

| Market Forecast in 2033 | USD 30.8 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Epta S.p.A, Daikin Industries, Ltd. (AHT Cooling Systems), Carrier Commercial Refrigeration, Hussmann Corporation, Viessmann Group, Panasonic Corporation, Ali Group S.p.A., Frigoglass S.A.I.C., ISA S.p.A., True Manufacturing Co., Inc., GEA Group Aktiengesellschaft, SandenVendo America, Koxka S.A., Lennox International Inc., Fogel Company, ILSA S.p.A., Foster Refrigerator (ITW Food Equipment Group), Metalfrio Solutions S.A., Norpe (Viessmann Group), Imbera Commercial Refrigeration |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Refrigerated Display Cabinets market is characterized by a definitive shift towards holistic energy management, driven primarily by the global mandate for climate-friendly refrigeration. The most significant technological disruption involves the widespread adoption of natural refrigerant technologies, predominantly Carbon Dioxide (CO2 or R744) systems and hydrocarbon refrigerants like Propane (R290) and Isobutane (R600a). CO2 systems, particularly in large supermarkets, utilize transcritical booster technology which offers a significantly lower Global Warming Potential (GWP) compared to phased-out HFCs, although their application requires complex system designs and specialized heat recovery integration to maximize efficiency in warmer climates. Conversely, R290 is favored for plug-in cabinets due to its excellent thermodynamic properties and ease of integration into smaller, self-contained units, meeting strict safety standards for flammability.

Beyond refrigerant type, key innovation centers around enhancing operational efficiency and intelligence. This includes the development of Variable Speed Drive (VSD) compressors and Electronically Commutated (EC) fan motors, which modulate cooling output precisely to match the thermal load, reducing cycling and overall energy consumption by up to 30%. Furthermore, advanced insulation techniques, such as vacuum-insulated panels (VIPs), are being incorporated into cabinet walls to minimize heat ingress and maintain temperature stability with less energy input. These insulation technologies are crucial for meeting increasingly aggressive minimum energy performance standards (MEPS) established by regulatory bodies worldwide.

The digitalization of RDCs represents another major technological pillar. The integration of Internet of Things (IoT) sensors, cloud computing platforms, and advanced control electronics enables real-time remote monitoring of temperature, humidity, pressure, and energy usage. This facilitates sophisticated data analytics, enabling features like predictive maintenance, automated compliance reporting, and optimized product presentation through integrated LED lighting that minimizes heat generation. The development of anti-condensation technologies, often relying on smart heated glass or airflow management systems, further contributes to visual merchandising effectiveness while simultaneously saving energy compared to constantly heated door frames.

The primary driver is stringent global environmental regulations, such as the Kigali Amendment and regional F-Gas regulations, which mandate the phase-down of high-Global Warming Potential (GWP) HFC refrigerants, forcing retailers to invest in compliant natural refrigerant-based systems (like CO2 and R290).

Plug-in (self-contained) cabinets have integrated condensing units and are flexible for small stores, generating heat directly into the retail space. Remote cabinets connect to a central external refrigeration plant, offering superior energy efficiency, higher capacity, and reduced noise/heat inside the store, favored by large supermarkets.

AI significantly enhances operational efficiency by enabling predictive maintenance, automatically adjusting cooling cycles based on real-time load and ambient conditions (Dynamic Energy Optimization), and optimizing defrost schedules, leading to substantial energy savings and reduced equipment downtime.

The Asia Pacific (APAC) region is projected to exhibit the fastest growth, fueled by rapid urbanization, substantial investment in cold chain infrastructure, and the aggressive expansion of modern supermarket and convenience store chains across developing economies like India and China.

The key challenges include the high initial capital investment required for transcritical CO2 booster systems, the need for specialized design and installation to handle high operating pressures, and the scarcity of technicians trained for complex CO2 system maintenance and repair, especially in regions with high ambient temperatures.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.