ID : MRU_ 431933 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

The Regenerative Artificial Skin Market is experiencing robust expansion driven by the increasing global prevalence of burn injuries, chronic wounds such as diabetic ulcers, and a rising demand for advanced wound care solutions that offer functional restoration rather than mere covering. Technological advancements in biomaterials science, tissue engineering, and cell culture techniques have significantly improved the efficacy and biocompatibility of artificial skin products. Furthermore, the growing elderly population, which is highly susceptible to non-healing wounds, provides a substantial demographic impetus for market growth. This scenario necessitates continuous innovation in scaffold design, cellular components, and integration capabilities to facilitate rapid healing and minimal scarring.

The market trajectory is heavily influenced by favorable regulatory approvals for novel bioengineered products and substantial funding from both governmental bodies and private investors aimed at accelerating research and development in regenerative medicine. Emerging economies, particularly in Asia Pacific, are contributing significantly to the market expansion due to improving healthcare infrastructure and increasing awareness regarding advanced wound management practices. However, high product costs and stringent reimbursement policies in certain regions pose minor hurdles. Despite these challenges, the clinical success of currently available products, combined with an expanding pipeline of next-generation regenerative solutions, firmly positions the market for significant value appreciation throughout the forecast period.

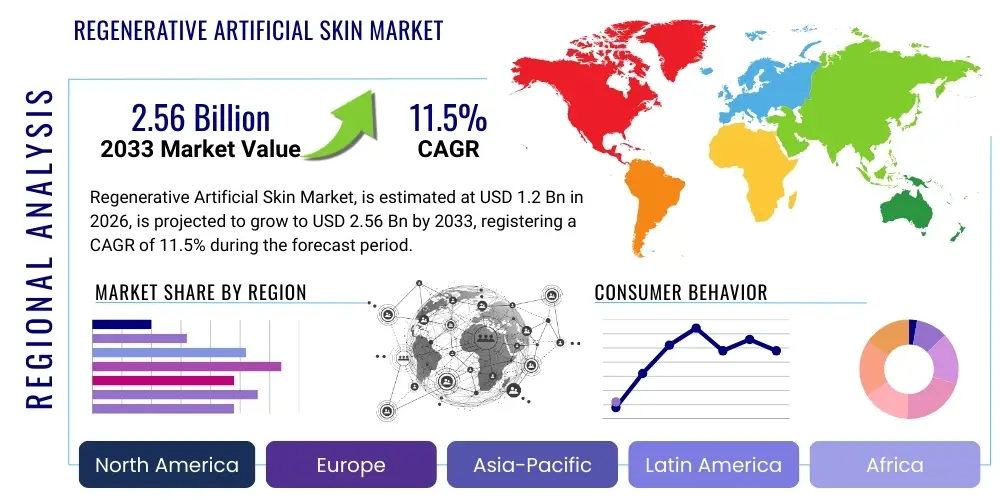

The Regenerative Artificial Skin Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.5% between 2026 and 2033. The market is estimated at $1.2 Billion in 2026 and is projected to reach $2.56 Billion by the end of the forecast period in 2033.

The Regenerative Artificial Skin Market encompasses products designed to mimic the structural and functional properties of natural human skin, serving as advanced biological substitutes for temporary or permanent wound coverage. These sophisticated biomedical devices utilize principles of tissue engineering and regenerative medicine, often incorporating specialized materials like collagen, hyaluronic acid, or biodegradable polymers, sometimes seeded with autologous or allogeneic cells (keratinocytes and fibroblasts). The primary objective of these substitutes is not only to protect the underlying tissue but crucially, to promote the body's intrinsic healing processes and facilitate the regeneration of functional skin layers.

Major applications of regenerative artificial skin include the treatment of severe burns (second- and third-degree), chronic non-healing wounds (venous ulcers, pressure ulcers, and diabetic foot ulcers), and reconstructive procedures following trauma or surgical excisions. The core benefit these products offer is superior therapeutic outcomes compared to traditional grafting techniques, including reduced pain, minimized scarring, decreased risk of infection, and enhanced functional recovery. Furthermore, they address the limitations associated with the availability and morbidity of autologous donor sites, particularly in patients with large surface area burns.

Driving factors for this market include the escalating incidence of trauma and burn injuries worldwide, the rising prevalence of diabetes leading to chronic ulcers, and continuous innovations in biomaterials that improve the integration and viability of artificial skin grafts. Government initiatives supporting regenerative medicine research and increasing public health expenditure on wound care further catalyze market growth. The shift towards biological and functional restoration in wound management, moving beyond basic protective dressings, underscores the critical role regenerative artificial skin plays in modern clinical practice.

The Regenerative Artificial Skin Market demonstrates dynamic business trends characterized by intense mergers and acquisitions (M&A) activity among large pharmaceutical and medical device companies aiming to consolidate specialized technology platforms and expand product pipelines. Key strategic partnerships focusing on co-development and distribution are prevalent, particularly between advanced biomaterials manufacturers and clinical research institutions. Companies are heavily investing in personalized medicine approaches, developing constructs tailored to specific patient needs, and utilizing 3D bioprinting techniques to achieve enhanced structural complexity and biological fidelity, thereby positioning themselves for competitive advantage in high-value clinical segments.

Regionally, North America maintains market leadership, driven by high healthcare expenditure, sophisticated regulatory pathways that expedite advanced therapy approvals, and the presence of major industry players and specialized burn centers. However, the Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR), fueled by rapidly expanding healthcare infrastructure, increasing medical tourism for specialized treatments, and a large underserved patient population, particularly in China and India. Europe exhibits steady growth, primarily focusing on government-backed clinical trials and robust academic research collaborations aimed at optimizing next-generation scaffolds and cellular components.

Segment trends reveal that the cellular artificial skin category, despite its higher cost and complexity, is gaining momentum due to superior long-term clinical outcomes and functional integration capabilities compared to acellular matrices. Application-wise, chronic wound treatment represents a high-growth segment, reflecting the pervasive challenge posed by diabetic ulcers globally. Furthermore, the rising adoption of synthetic and composite materials, offering cost-effectiveness and flexibility in manufacturing, is influencing procurement decisions across various healthcare settings, ensuring sustained demand across both hospital and specialized wound care clinic environments.

User queries regarding the impact of Artificial Intelligence (AI) on the Regenerative Artificial Skin Market predominantly center on how AI accelerates research, optimizes manufacturing, and enhances clinical application and patient outcomes. Users frequently ask about AI's role in designing novel biomaterials, predicting graft rejection, and personalizing treatment plans. The core expectations revolve around AI reducing the time-to-market for complex bioengineered products and improving the predictive success rate of skin substitutes. There is significant interest in using machine learning (ML) to analyze large genomic and proteomic datasets derived from wound healing studies to identify key biomarkers, thereby guiding the optimal selection of regenerative products for individual patients.

AI's primary influence is seen in the computational modeling of complex biological interactions, specifically in predicting how different scaffold architectures and cellular components will interact with the host immune system and surrounding tissues. Machine learning algorithms can process vast databases of material properties, cellular viability, and histological outcomes to design optimized matrices with targeted biodegradation rates and enhanced regenerative potential. This predictive capability substantially reduces reliance on expensive and time-consuming physical experimentation, thereby streamlining the preclinical development phase.

Furthermore, AI is crucial in quality control and manufacturing scalability. Computer vision systems integrated into bioprinting platforms ensure precise cell placement and structural integrity during the fabrication of multilayered skin constructs. Clinically, AI algorithms are being developed to analyze real-time patient data—including vascularization, temperature, and microbiological profiles—to predict the success or failure of a skin graft early on, allowing clinicians to intervene proactively. This personalized monitoring capability is expected to significantly improve patient safety and therapeutic efficacy across all major applications.

The market is primarily driven by the escalating global burden of chronic diseases such as diabetes, which leads to millions of cases of non-healing ulcers annually, necessitating advanced regenerative solutions beyond conventional dressings. Coupled with this is the continuous refinement of tissue engineering techniques, leading to the development of highly effective, bio-integrative products that provide superior functional outcomes compared to traditional skin grafting. The supportive regulatory environment in major developed economies, often granting fast-track approvals for genuinely novel regenerative therapies, further accelerates product commercialization and clinical adoption, acting as a powerful catalytic force.

However, significant restraints temper the market growth. The high cost associated with the research, development, and manufacturing of complex cellular or acellular matrices poses a considerable financial barrier for healthcare systems and patients in resource-constrained settings. Furthermore, challenges related to the shelf life, storage, and logistical complexities inherent in handling cryopreserved cellular products limit their widespread adoption, especially in emergency or remote healthcare facilities. Ethical concerns surrounding the use of certain cellular sources and the potential for regulatory fragmentation across various international markets also contribute to market friction.

Opportunities abound in leveraging 3D bioprinting technologies to create on-demand, patient-specific skin constructs, which promises to revolutionize personalized wound care. Investment in developing affordable, off-the-shelf, acellular substitutes that require less complex handling offers substantial market penetration opportunities in emerging markets. The primary impact forces are regulatory approval dynamics, dictating speed-to-market, and technological innovation in material science, which directly influences product efficacy and patient outcomes. The growing clinical evidence supporting long-term efficacy enhances confidence among surgeons and reimbursement bodies, serving as a powerful force propelling broader clinical integration.

The Regenerative Artificial Skin Market is meticulously segmented based on product type, material, application, and end-user, providing a granular view of market dynamics and opportunity areas. The segmentation by product type distinguishes between Acellular, Cellular, and Composite skin substitutes, reflecting differences in structural complexity and biological function. Material segmentation highlights the reliance on diverse components such as collagen, silicone, and synthetic polymers, each contributing specific mechanical and biological properties to the construct. Application segmentation details the primary clinical uses, with critical burn care and chronic wound treatment being the most substantial revenue contributors, while end-user segmentation recognizes the critical role played by hospitals, specialized burn centers, and ambulatory surgical centers in product adoption and deployment.

The value chain for the Regenerative Artificial Skin Market is complex and involves specialized processes spanning raw material sourcing, complex manufacturing, and clinical distribution. Upstream analysis focuses heavily on the procurement of highly specialized, medical-grade raw materials, including pharmaceutical-grade collagen sources (bovine, porcine, or recombinant), biocompatible synthetic polymers, and essential growth factors and cell culture media. Research and development activities, often involving partnerships with academia and dedicated biotech firms, are critical upstream components, driving innovation in scaffold design and cellular expansion techniques. Quality assurance processes at this stage must be exceedingly rigorous due to the biological nature and sensitivity of the final product.

Midstream activities involve sophisticated manufacturing processes, including tissue engineering, decellularization, sterilization, and, increasingly, 3D bioprinting. This stage requires specialized cleanroom facilities, highly skilled technical staff, and strict adherence to Current Good Manufacturing Practices (cGMP). The transition from laboratory-scale production to commercial scalability represents a significant challenge and a point of potential bottleneck. Products are often cryopreserved or stored under specific conditions to ensure cellular viability and structural integrity before moving to the distribution phase.

Downstream analysis covers distribution channels and end-user adoption. Due to the high value, specific handling requirements (especially for cellular products), and specialized application of artificial skin, the distribution is often direct or through highly specialized third-party logistics (3PL) providers capable of maintaining cold chain integrity. Direct distribution channels, where manufacturers interface directly with major hospital systems and specialized burn centers, are prevalent. Indirect channels involve authorized distributors focusing on regional clinics and smaller healthcare centers. The final consumption is driven by key opinion leaders (KOLs) in plastic surgery, trauma surgery, and dermatology, making professional education and clinical evidence sharing crucial for market penetration and sustained growth.

The primary customers for regenerative artificial skin are institutions and medical professionals involved in the specialized treatment of severe tissue damage and chronic wounds. These include trauma centers and specialized burn units within tertiary care hospitals, which frequently manage patients requiring immediate and extensive skin replacement due to life-threatening injuries. These centers prioritize products offering rapid coverage, infection control, and optimal functional outcomes, often favoring advanced cellular and composite grafts despite the high cost. Specialized orthopedic and plastic surgery departments also represent core customers, utilizing these products for complex reconstructive procedures.

A rapidly expanding customer base includes specialized wound care clinics and diabetes centers. These facilities focus primarily on treating chronic, non-healing wounds prevalent among the aging and diabetic populations. For these customers, factors such as ease of application, reduced total cost of care (by avoiding repeated procedures), and efficacy in promoting angiogenesis and granulation tissue formation are critical purchasing criteria. The shift towards outpatient treatment models also makes these clinics increasingly important distribution points for acellular matrices and simpler bilayered products.

Governmental and military healthcare systems also constitute significant potential customers, often purchasing large volumes of artificial skin for preparedness and treatment of trauma injuries sustained in conflict or disaster scenarios. Procurement decisions in this segment emphasize long shelf life, robust clinical performance, and bulk pricing. Furthermore, research institutions and universities involved in clinical trials and academic studies on regenerative medicine are consistent, albeit smaller, purchasers of these materials for research applications, contributing to future product development and adoption trends.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.2 Billion |

| Market Forecast in 2033 | $2.56 Billion |

| Growth Rate | 11.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Organogenesis Inc., Integra LifeSciences, MiMedx Group, Avita Medical, Stratatech, B. Braun Melsungen AG, Smith & Nephew, Mallinckrodt Pharmaceuticals, Vericel Corporation, Mylan NV, Cynata Therapeutics, Episkin (L’Oreal), Advanced Tissue, Kerecis, AxioBio. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Regenerative Artificial Skin Market is dominated by advancements in tissue engineering, centered around optimizing the scaffold structure and integrating viable cellular components. A pivotal technology is the development of porous, biodegradable matrices, often made of collagen or polyglycolic acid (PGA), designed to provide a temporary, highly bioactive structure that encourages host cell migration, proliferation, and vascularization. Decellularization techniques are essential for creating acellular dermal matrices, which strip away immunogenic cellular material while preserving the native extracellular matrix structure, thereby reducing the risk of rejection and serving as an ideal platform for host tissue ingrowth. The continuous improvement of these scaffold materials focuses on achieving optimal mechanical resilience, controlling degradation rates, and incorporating antimicrobial or pro-angiogenic factors.

Cellular technologies, which involve seeding scaffolds with keratinocytes, fibroblasts, or stem cells (such as Mesenchymal Stem Cells or induced Pluripotent Stem Cells), represent the frontier of functional artificial skin development. Autologous and allogeneic cellular products require advanced cell expansion and culture techniques to ensure high viability and rapid proliferation necessary for clinical scale-up. The challenge lies in creating multilayered constructs that accurately replicate the complex dermo-epidermal junction. Furthermore, closed-system bioreactors are increasingly employed to automate and standardize cell culture processes, ensuring consistent quality and compliance with stringent regulatory standards, which is vital for mass production of cellular therapies.

The newest and most disruptive technology is 3D Bioprinting. This additive manufacturing process allows for precise, layer-by-layer deposition of bio-inks (containing cells and biomaterials) to fabricate anatomically precise, multi-layered skin structures. Bioprinting offers the potential for creating patient-specific, on-demand skin grafts directly tailored to the size and contours of the wound, significantly improving surgical fit and integration. Research is heavily focused on developing bioprinters capable of in-situ printing, potentially allowing surgeons to print skin directly onto a wound bed during an operation. Alongside bioprinting, nanotechnology is being utilized to encapsulate therapeutic agents within the artificial skin to control their release and enhance local regenerative effects, further blurring the line between passive wound coverage and active therapeutic devices.

Acellular skin substitutes consist only of a biological or synthetic matrix (scaffold), relying entirely on the patient's cells to populate and regenerate tissue. Cellular substitutes incorporate viable living cells (e.g., fibroblasts or keratinocytes) within the scaffold, offering immediate biological activity and often superior long-term functional regeneration, though they require complex storage and handling.

The Chronic Wounds segment, specifically addressing diabetic foot ulcers (DFUs), venous leg ulcers, and pressure ulcers, currently drives the highest volume and projected growth. This is due to the rising global prevalence of diabetes and the substantial need for advanced, cost-effective solutions for non-healing wounds that resist traditional treatments.

The main restraints are the high upfront cost of cellular and composite products, which strains hospital budgets and limits patient access, alongside the technical complexity and logistical challenges associated with manufacturing, transportation, and specialized storage required for maintaining cell viability.

3D Bioprinting allows for the precise, automated, and customized fabrication of multi-layered skin constructs tailored to the exact dimensions and cellular needs of a patient's wound. This technology is expected to enhance structural integrity, accelerate functional integration, and potentially enable on-demand clinical printing, reducing current supply chain limitations.

The Asia Pacific (APAC) region, driven primarily by major economies like China and India, is projected to exhibit the highest CAGR. This accelerated growth is supported by rapid improvements in healthcare infrastructure, increasing adoption of Western medical standards, and a vast, increasingly affluent patient demographic seeking advanced regenerative therapies.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.