ID : MRU_ 433513 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

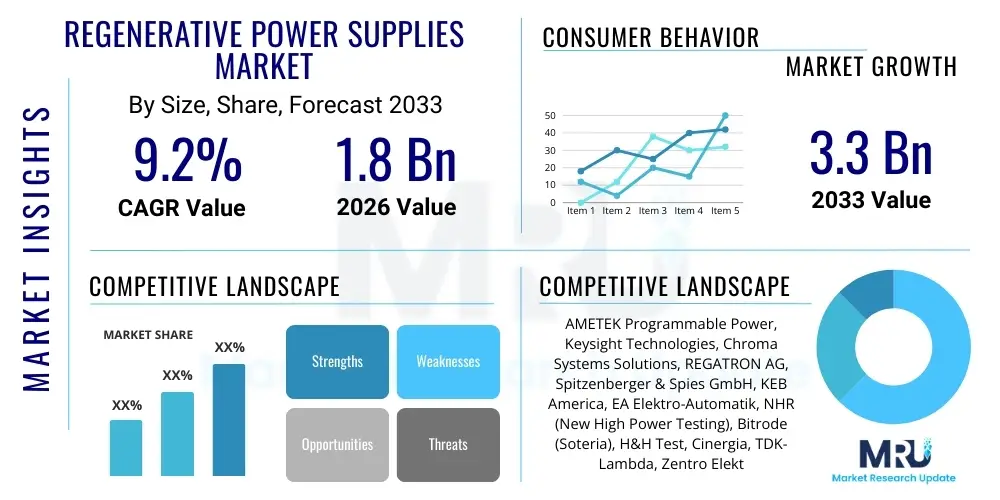

The Regenerative Power Supplies Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.2% between 2026 and 2033. The market is estimated at USD 1.8 Billion in 2026 and is projected to reach USD 3.3 Billion by the end of the forecast period in 2033.

The Regenerative Power Supplies Market encompasses advanced electronic equipment designed not only to source power to a load but also to efficiently sink power back into the utility grid or a dedicated storage system. Unlike traditional power supplies that dissipate excess energy as heat, regenerative units capture and recycle this energy, leading to significant reductions in operational costs, lower heat generation, and improved energy efficiency in testing environments. These systems are critical components in industries requiring precise simulation and testing of energy storage systems, electric vehicle drivetrains, photovoltaic inverters, and sophisticated military hardware. The fundamental technology relies on high-speed bidirectional power converters, often employing insulated-gate bipolar transistors (IGBTs) or silicon carbide (SiC) devices, coupled with sophisticated control algorithms to manage power flow direction, stability, and quality.

Key applications driving market adoption include the burgeoning Electric Vehicle (EV) sector, where regenerative power supplies are essential for battery cycling, drive train simulation, and validating vehicle-to-grid (V2G) capabilities. Furthermore, the expansion of renewable energy infrastructure necessitates these supplies for testing grid-tied inverters and optimizing microgrid stability, ensuring that energy quality standards are rigorously met. The ability to precisely mimic real-world load profiles, including rapid changes in current and voltage, makes regenerative supplies indispensable for reliable product development and quality assurance across high-power electronics domains. The integration of high-fidelity control loops and programming interfaces (such as LXI and GPIB) further enhances their utility in automated test environments.

Major benefits derived from the adoption of regenerative power supplies include substantial energy savings due to energy recovery rates often exceeding 90%, reduced cooling requirements in test facilities, and a smaller environmental footprint compared to resistive load banks. The driving factors are primarily centered around global mandates for energy efficiency, the rapid transition to electric mobility requiring advanced testing solutions, and the increasing complexity of power electronics demanding high-accuracy, high-power bidirectional sourcing and sinking capabilities. The continuous innovation in wide-bandgap semiconductors (GaN and SiC) is accelerating the development of smaller, lighter, and more efficient regenerative units, thereby improving accessibility and application scope across various industrial sectors.

The global Regenerative Power Supplies Market is characterized by robust growth, primarily fueled by the accelerating electrification of transportation and the global push towards smarter, more resilient power grids. Business trends indicate a strong move toward higher power density units and the integration of advanced communication protocols for IoT and Industry 4.0 environments, allowing seamless data logging and remote diagnostics. Key manufacturers are focusing on developing modular systems that allow users to scale power levels easily, optimizing capital expenditure and future-proofing test benches. Furthermore, there is a distinct trend towards software-defined power supplies, offering unparalleled flexibility in waveform generation and fault simulation capabilities necessary for complex testing requirements like battery emulation and transient analysis. Strategic partnerships between power supply manufacturers and EV drivetrain developers are becoming crucial for maintaining market leadership and customizing solutions to meet evolving automotive standards.

Regionally, Asia Pacific (APAC) stands out as the dominant growth engine, driven largely by massive investments in electric vehicle manufacturing in China, South Korea, and Japan, coupled with extensive renewable energy deployments, particularly solar and wind farms. North America and Europe maintain significant market shares, characterized by early adoption of sophisticated, high-power regenerative systems for aerospace, defense, and premium automotive R&D. European regulatory frameworks emphasizing energy efficiency and carbon neutrality further stimulate demand. Manufacturers in these regions are increasingly prioritizing compliance with stringent safety standards (e.g., UL, CE) and high harmonic reduction requirements, necessitating continuous R&D into advanced active power factor correction (APFC) and filtering technologies to ensure clean energy feedback to the grid.

Segment trends reveal that the DC regenerative power supply segment holds the largest market share, directly attributed to the prevalence of DC-based systems such as batteries, fuel cells, and high-voltage EV buses. However, the AC regenerative segment is projected to exhibit the fastest growth, driven by the increasing need for testing large-scale grid-tied inverters, smart grid equipment, and AC motor drives under highly realistic conditions, including three-phase fault simulation and harmonic injection testing. Power level analysis shows that the high-power segment (above 100 kW) is witnessing significant growth, driven by heavy-duty EV testing (trucks, buses) and utility-scale energy storage integration projects. This shift underscores the market's maturation towards handling higher voltage and current demands efficiently and safely.

Users frequently inquire about how Artificial Intelligence (AI) and Machine Learning (ML) will enhance the efficiency, reliability, and automation of regenerative power supply systems, particularly concerning complex battery testing and grid simulation. Key concerns revolve around AI's ability to optimize energy recycling rates in real-time, predict equipment failures (predictive maintenance), and generate high-fidelity, adaptive test profiles that mimic complex, non-linear real-world usage patterns, thereby accelerating R&D cycles. Users expect AI to move beyond simple automation to facilitate smarter testing environments, reducing manual intervention and maximizing throughput while ensuring the integrity of the power feedback process to the utility or local storage. The core theme is the integration of autonomous decision-making capabilities within the power supply control system.

AI's primary impact involves enhancing the control algorithms used in regenerative power supplies. Machine learning models can analyze vast datasets generated during battery charging/discharging cycles, identifying optimal current profiles that maximize battery life and minimize thermal stress, a capability far superior to traditional, fixed-profile testing. This refinement leads to more accurate and reliable test results for battery management systems (BMS). Furthermore, AI can be utilized to dynamically manage the interaction between the regenerative supply and the electrical grid, optimizing the timing and quality of the recovered energy feedback, which is crucial for compliance with strict grid codes regarding voltage sags and swells, ultimately increasing overall system efficiency and compliance.

In terms of operational efficiency, AI algorithms are being deployed for predictive maintenance within the power supply hardware itself. By continuously monitoring internal component temperatures, current ripple, and switching frequencies, ML models can predict potential failures in critical components like IGBT modules or DC link capacitors long before they occur, scheduling proactive maintenance and dramatically reducing unplanned downtime in expensive, high-power test facilities. This shift from reactive to predictive operations significantly improves the total cost of ownership (TCO) for large-scale users in the automotive and aerospace testing sectors, driving the demand for AI-enabled, self-optimizing regenerative units.

The market dynamics for Regenerative Power Supplies are primarily shaped by robust environmental policies favoring energy efficiency (Drivers) contrasted by high initial procurement and installation costs (Restraints). Opportunities lie in the rapidly expanding electrification ecosystem, including maritime and aerospace applications, while Impact Forces are dominated by the stringent regulatory landscape governing grid interconnection and power quality. The confluence of these factors determines the pace and direction of market growth, necessitating manufacturers to balance high performance with cost-effectiveness.

Driving factors are inherently linked to global megatrends: the explosive growth of the EV market demanding high-power testing infrastructure; the massive increase in renewable energy sources (solar, wind) requiring sophisticated inverter testing and grid synchronization capabilities; and regulatory incentives promoting waste energy recovery in industrial settings. These drivers create a non-negotiable need for regenerative solutions over traditional dissipative load banks, pushing R&D towards higher voltage, higher frequency operation. Furthermore, the inherent safety benefits of regenerative units, which eliminate the massive heat generation associated with dissipative loads, make them the preferred choice in modern, space-constrained testing facilities.

Restraints primarily concern the substantial capital investment required for high-power regenerative systems compared to conventional unidirectional power supplies or simple load banks. The complexity involved in grid synchronization and managing power feedback requires specialized expertise for installation and maintenance, sometimes leading to slower adoption rates in smaller enterprises. Opportunities are abundant, specifically in emerging technologies like hydrogen fuel cells, where regenerative units are essential for testing the high-power density conversion systems, and in developing vehicle-to-everything (V2X) infrastructure, which requires seamless bidirectional power flow testing. The primary impact force remains the necessity of adherence to international grid codes (e.g., IEEE 1547, IEC 61000 standards), which dictates the complexity and cost of the control electronics within the power supply unit.

The Regenerative Power Supplies Market is comprehensively segmented based on the type of power (AC or DC), the magnitude of the power output (Low, Medium, High), and the primary end-use application (Automotive, Grid, Industrial). This segmentation allows for precise market sizing and strategic targeting by manufacturers. The differentiation between AC and DC supplies is fundamental, reflecting the inherent needs of the component being tested—DC supplies are crucial for battery testing and charging, while AC supplies are indispensable for grid-tied inverters, motor drives, and aeronautical systems simulation. The evolution of high-voltage DC systems, especially in utility-scale battery storage, is blurring the lines, driving demand for hybrid or modular AC/DC regenerative solutions.

Further breakdown by power level illustrates the distinct requirements across industries. Low-power units (typically below 10 kW) serve laboratory research and small-scale component validation. Medium-power units (10 kW to 100 kW) are standard for passenger EV component testing and small industrial applications. The High-power segment (above 100 kW) is reserved for heavy-duty EV powertrain testing, aerospace equipment, and utility-scale renewable energy integration points, representing the most capital-intensive segment but also offering the fastest growth potential due to expanding commercial electrification projects globally. The application segment analysis reveals that the Automotive sector consistently holds the largest share due to the global regulatory push for electrification and the corresponding need for high-throughput, energy-efficient testing benches. This continuous demand ensures that segmentation remains a critical tool for strategic market positioning.

The value chain for the Regenerative Power Supplies Market begins with upstream suppliers providing critical components such as high-power semiconductors (SiC, IGBTs), magnetic components (transformers, inductors), and advanced control microprocessors. The quality and cost of these raw materials significantly influence the final product efficiency and pricing. Manufacturers, positioned centrally, engage in complex R&D to integrate these components into highly efficient, grid-compliant systems, focusing intensely on firmware development for bidirectional power flow control and safety features. This integration stage is where intellectual property and technological differentiation are established, especially concerning power density and waveform accuracy.

The downstream analysis focuses on distribution and integration. Regenerative power supplies are often sold through specialized, high-service distributors who possess technical expertise in system integration, especially for complex automotive or aerospace testing facilities. Direct sales channels are frequently employed for high-value, customized, or utility-scale projects where direct communication between the manufacturer and the end-user is necessary for custom specification definition. System integrators play a vital role, combining the power supply unit with other test equipment (e.g., climatic chambers, dynamometers, battery cyclers) to deliver a complete, turn-key testing solution to the end customer. The after-sales service, including calibration, repair, and software updates, constitutes a crucial part of the downstream value proposition due to the precision required by these systems.

The distribution channel emphasizes a blend of direct and indirect engagement. Large OEMs, particularly in the automotive sector, prefer direct procurement due to the scale and complexity of their requirements, ensuring customized software integration and long-term support agreements. Smaller R&D labs and educational institutions typically utilize indirect channels, relying on distributors for accessibility, localized support, and integration expertise. The efficiency of this value chain is increasingly reliant on supply chain resilience, given the current global constraints on advanced semiconductor components, making strategic sourcing and component redundancy a key competitive advantage for power supply manufacturers.

Potential customers for Regenerative Power Supplies span several high-technology and infrastructure sectors where energy efficiency and precision power testing are paramount. The dominant customer base includes Original Equipment Manufacturers (OEMs) in the automotive industry, specifically those designing and manufacturing Electric Vehicles (EVs), Hybrid Electric Vehicles (HEVs), and their associated powertrain components like batteries, motors, and inverters. These buyers require robust, high-channel-count regenerative systems for extensive durability testing and performance validation under simulated real-world conditions, including highly dynamic charging and discharging cycles.

Another major segment comprises utility companies and large-scale renewable energy project developers. These customers utilize regenerative AC and DC supplies to test grid interface components, such as solar photovoltaic (PV) inverters and large battery energy storage systems (BESS), ensuring compliance with strict regional and international grid connection standards. The ability to simulate grid faults, voltage fluctuations, and harmonic distortion accurately is a non-negotiable requirement for ensuring grid stability and reliable renewable energy integration. Furthermore, government and private research institutions focusing on advanced materials science and next-generation energy storage technologies form a steady customer segment.

Beyond energy-focused sectors, aerospace and defense contractors are significant buyers. They require regenerative power systems to simulate complex onboard power networks, test high-reliability avionics, and validate directed energy systems under severe load transient conditions, where power quality and response speed are critical. Lastly, independent testing houses and certification laboratories serve as crucial intermediate customers, purchasing regenerative supplies to offer third-party compliance testing services to smaller component manufacturers who cannot afford their own high-end testing infrastructure. The sophistication of the equipment dictates that the buyers are typically highly specialized engineering or procurement teams.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 3.3 Billion |

| Growth Rate | CAGR 9.2% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | AMETEK Programmable Power, Keysight Technologies, Chroma Systems Solutions, REGATRON AG, Spitzenberger & Spies GmbH, KEB America, EA Elektro-Automatik, NHR (New High Power Testing), Bitrode (Soteria), H&H Test, Cinergia, TDK-Lambda, Zentro Elektrik, Advanced Energy, Magna-Power Electronics, GW Instek, NH Research, ZES ZIMMER, Suzhou Power Supply Co., Dynaload. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Regenerative Power Supplies Market is heavily defined by advancements in power electronics and digital control systems. The core technology relies on fully controlled, insulated-gate bipolar transistor (IGBT) and increasingly, Silicon Carbide (SiC) based inverter topologies. SiC technology is a primary disruptor, enabling higher switching frequencies, resulting in smaller filter components, faster transient response times, and significantly higher power density (kW/liter). This shift is critical for automotive testing labs where floor space is often limited and test speeds must be maximized. Modern units leverage sophisticated Pulse Width Modulation (PWM) techniques and active power factor correction (APFC) to ensure minimal harmonic injection back into the utility grid, maintaining power quality compliance.

Furthermore, digital signal processing (DSP) and field-programmable gate arrays (FPGAs) are essential for executing the complex, high-speed control loops required for regenerative operation. These processors manage the seamless transition between sourcing and sinking power, ensure instantaneous response to load changes, and facilitate the high-fidelity simulation of complex battery and grid characteristics. The software layer is equally important, offering advanced graphical user interfaces (GUIs), integrated scripting languages, and support for industry-standard communication protocols like Ethernet/LXI, CAN, and EtherCAT, facilitating integration into automated test environments (ATEs) and Hardware-in-the-Loop (HIL) simulations.

A notable trend involves the development of modular and stackable architectures. Manufacturers are producing smaller, standardized power blocks (e.g., 30 kW or 50 kW modules) that can be seamlessly paralleled to achieve multi-megawatt capabilities. This modularity not only offers scalability and redundancy but also simplifies maintenance. Coupled with highly advanced thermal management systems—often employing liquid cooling in high-power applications—these technological innovations ensure the reliability and longevity required for continuous operation in demanding industrial and research environments, cementing the market’s reliance on advanced semiconductor and digital control platforms.

The primary benefit is energy efficiency and cost reduction, as regenerative power supplies capture excess energy dissipated by the load and feed it back into the utility grid or local system, achieving energy recovery rates often exceeding 90%, thereby minimizing wasted energy and cooling requirements in test facilities.

Regenerative supplies are essential for EV testing by accurately simulating battery charging/discharging cycles, emulating complex battery chemistries, and performing high-power drivetrain testing, ensuring precise and energy-efficient validation of motor controllers and vehicle-to-grid (V2G) communication.

Silicon Carbide (SiC) semiconductor technology is significantly driving efficiency and power density by allowing higher switching frequencies than traditional IGBTs. This results in smaller, lighter power units with improved transient response and reduced energy loss.

The main challenge is adherence to stringent utility grid codes and standards, such as IEEE 1547 and IEC 61000, which govern power quality, harmonic distortion limits, and anti-islanding protection when feeding recovered energy back into the grid.

The High Power Output segment (above 100 kW) is projected for the fastest growth due to the increasing size and voltage requirements of heavy-duty EV batteries (trucks, buses) and the scale of utility-level renewable energy storage and grid integration projects globally.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.