ID : MRU_ 432579 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

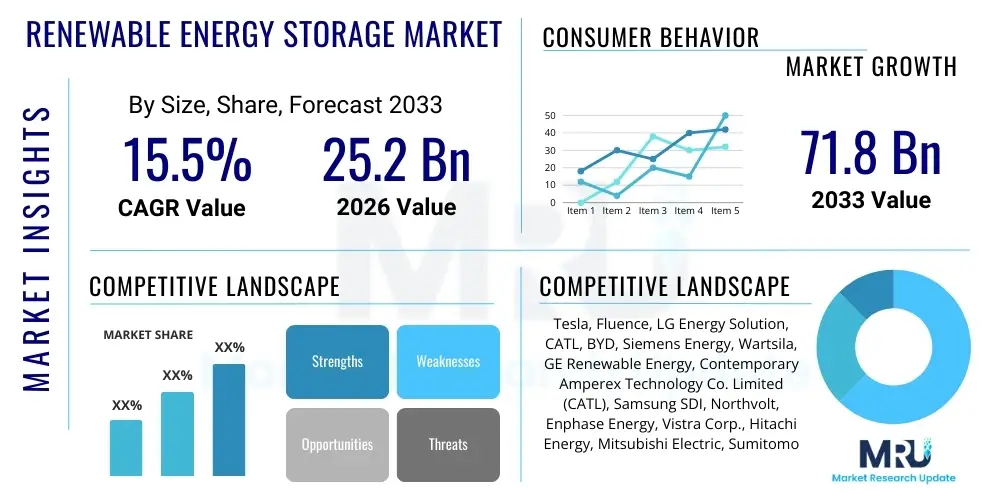

The Renewable Energy Storage Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.5% between 2026 and 2033. The market is estimated at USD 25.2 Billion in 2026 and is projected to reach USD 71.8 Billion by the end of the forecast period in 2033.

The Renewable Energy Storage Market encompasses technologies and systems designed to capture energy generated from intermittent renewable sources, primarily solar and wind power, and release it when needed, thereby ensuring grid stability and reliable energy supply. These systems are crucial components of the global transition towards decarbonization and include diverse technologies such as electrochemical batteries (notably Lithium-ion), pumped hydro storage (PHS), mechanical storage (compressed air energy storage, CAES), and thermal energy storage (TES). The core objective of these products is to decouple renewable generation time from energy demand time, mitigating the inherent variability of solar and wind resources and facilitating higher penetration rates of clean energy into existing power grids.

Major applications for renewable energy storage systems span across the utility sector, commercial and industrial (C&I) installations, and residential use cases. Utility-scale deployment focuses heavily on grid stabilization, frequency regulation, peak shifting, and capacity firming, often involving large lithium-ion battery energy storage systems (BESS). C&I applications leverage storage for demand charge reduction, load management, and enhanced energy resilience, particularly in areas prone to grid outages. The integration of these storage solutions is driven by their multifaceted benefits, which include improving power quality, reducing reliance on fossil fuel peaking plants, and maximizing the financial returns on renewable generation assets, thus supporting a more flexible and efficient electricity infrastructure globally.

The market is experiencing exponential growth propelled by several converging driving factors. Foremost among these are aggressive governmental mandates and regulatory frameworks supporting renewable portfolio standards (RPS) and energy storage deployment targets across North America, Europe, and Asia Pacific. Furthermore, the substantial and continued decline in the cost of lithium-ion battery technology, coupled with breakthroughs in long-duration storage alternatives like flow batteries and green hydrogen storage, makes deployment increasingly economically viable. The necessity for grid modernization and hardening against climate change impacts and cyber threats also accelerates the adoption of resilient, decentralized energy storage solutions, establishing this market as foundational to future energy security.

The Renewable Energy Storage Market is defined by intense technological competition and rapid capacity expansion, primarily driven by utility-scale BESS projects in high-growth regional hubs such as China, the United States, and Germany. Current business trends indicate a significant consolidation among system integrators and increased focus on vertical integration by battery manufacturers aiming to secure supply chains, particularly for critical materials like lithium, cobalt, and nickel. Investment is heavily skewed towards enhancing power density and safety features in Li-ion systems, although strategic attention is shifting towards commercializing non-Li-ion alternatives, specifically long-duration energy storage (LDES) technologies, which promise durations exceeding four hours, addressing a key limitation of current technology.

Regional trends highlight Asia Pacific (APAC) as the dominant market, characterized by immense governmental investment in grid-scale storage to manage vast solar and wind buildouts, particularly in China and India. North America and Europe follow closely, distinguished by sophisticated regulatory structures favoring market mechanisms like frequency response services and capacity markets that incentivize storage deployment. Europe is particularly focused on achieving ambitious net-zero targets, driving investment in coupled renewable generation and storage projects, while North America’s growth is spurred by state-level mandates and federal tax credits designed to reduce reliance on aging thermal generation infrastructure and enhance grid reliability.

Segmentation trends reveal Lithium-ion technology maintaining market supremacy due to its proven performance, scalability, and decreasing cost curve, although flow batteries and solid-state batteries are gaining traction for specific commercial and LDES applications, respectively. Application-wise, the Utility-Scale segment holds the largest market share, reflecting the immediate need for transmission and distribution (T&D) infrastructure support and resource adequacy. However, the Commercial & Industrial (C&I) segment is projected to exhibit the fastest growth rate, fueled by favorable regulations allowing businesses to manage peak demand charges and improve operational resilience through localized energy management systems coupled with rooftop solar installations.

Analysis of common user questions regarding the impact of Artificial Intelligence (AI) on the Renewable Energy Storage Market reveals a primary focus on optimization, predictive capabilities, and smart grid integration. Users are keen to understand how AI can improve the efficiency and lifespan of expensive battery assets, specifically addressing concerns about thermal runaway, degradation rates, and optimal charging/discharging cycles. Key themes emerging include the potential for AI-driven energy trading and market participation strategies, maximizing revenue streams, and ensuring seamless coordination between distributed energy resources (DERs) and centralized grid operations. The expectation is that AI will move storage systems beyond simple hardware components into intelligent, autonomous assets capable of complex decision-making in real-time within volatile energy markets.

AI’s transformative influence is most pronounced in battery management systems (BMS), where sophisticated algorithms process vast datasets on cell performance, temperature fluctuations, and usage patterns to optimize operational parameters. This data-driven approach allows operators to precisely predict remaining useful life (RUL) and state of health (SOH), enabling proactive maintenance and scheduling that significantly extends asset longevity and improves safety. Furthermore, AI facilitates highly granular forecasting of renewable generation intermittency and load demand profiles. By achieving superior predictive accuracy, storage operators can participate more effectively in ancillary service markets, maximizing the economic value derived from each cycle of the storage system.

In the context of grid integration, AI serves as the central intelligence orchestrating complex, decentralized energy systems. Advanced AI platforms manage the dispatch of fleets of distributed energy storage systems (DESS) across different locations to balance supply and demand dynamically, achieving true virtual power plant (VPP) functionality. This level of optimization minimizes curtailment of renewable energy, enhances grid resilience during extreme weather events, and reduces congestion in transmission lines. Ultimately, AI accelerates the feasibility of 100% renewable energy grids by providing the necessary software layer to manage the inherent complexity and variability introduced by widespread renewable energy storage deployment.

The dynamics of the Renewable Energy Storage Market are shaped by powerful Drivers and substantial Opportunities that are currently outweighing persistent Restraints, leading to strong market momentum and high impact forces. Key drivers include global decarbonization targets and supportive government policies, specifically tax incentives and feed-in tariffs that make storage deployment financially attractive. The growing necessity for grid resilience, driven by increasing frequency of extreme weather events and grid vulnerability, further compels utilities and consumers to adopt storage solutions. Simultaneously, the continuous cost reduction in battery technologies, particularly lithium-ion, makes energy storage a competitive alternative to traditional peaking power plants, accelerating large-scale deployment.

However, the market faces notable restraints, primarily high upfront capital costs associated with certain emerging technologies, regulatory hurdles related to permitting and interconnection standards, and inherent risks within the supply chain, including geopolitical dependencies for critical materials and price volatility. Another significant restraint is the technological limitation concerning long-duration storage (LDS) solutions, where Li-ion batteries remain cost-prohibitive for storage durations exceeding 8 to 12 hours, slowing down the transition to 24/7 renewable grids. These constraints require strategic mitigation through innovation and diversification of material sourcing.

Opportunities in the market are abundant, centered around the rapid innovation in long-duration energy storage (LDES) technologies such as green hydrogen, flow batteries, and advanced compressed air systems, which promise to unlock multi-day storage capability crucial for grid independence. Furthermore, the integration of energy storage with electric vehicle (EV) infrastructure, enabling vehicle-to-grid (V2G) services, presents a massive untapped resource. The high impact forces resulting from these drivers and opportunities dictate aggressive infrastructure spending, technological maturation, and a rapid shift in regulatory perception, positioning energy storage as a mandatory, rather than optional, component of modern electricity networks.

The Renewable Energy Storage Market is comprehensively segmented based on technology, application, and deployment scale, reflecting the diverse requirements of the energy ecosystem. Segmentation by technology is crucial, as it dictates performance characteristics such as energy density, cycle life, response time, and duration, influencing suitability for specific uses, whether it be short-duration frequency response or long-duration energy shifting. Application segmentation delineates the end-use sectors, including utility-scale projects focused on transmission and distribution assets, Commercial & Industrial entities utilizing storage for operational efficiency and resiliency, and residential consumers focused on self-consumption optimization and backup power.

The dominance of lithium-ion battery technology, particularly its various chemistries like NMC (Nickel Manganese Cobalt) and LFP (Lithium Iron Phosphate), defines the current competitive landscape in the short-to-medium duration segment (up to 4 hours). However, the market is structurally diversifying, with mechanical storage (Pumped Hydro and CAES) remaining significant for large, established infrastructure, and flow batteries (e.g., Vanadium redox) gaining commercial traction due to their enhanced scalability, longer lifespan, and inherent safety advantages, positioning them competitively for medium-to-long duration requirements in demanding operational environments. This diversification ensures that a fit-for-purpose storage solution is available across the entire spectrum of grid needs.

Deployment scale segmentation—utility, residential, and C&I—allows for tailored market strategies. Utility-scale projects are characterized by large capital investments, adherence to stringent grid codes, and long-term contracts, primarily focusing on capacity firming and ancillary services. Conversely, the C&I and residential segments are driven by consumer economics, focusing on maximizing self-consumption of renewable generation, managing peak demand charges, and providing reliable backup power during outages, typically involving smaller, modular, and highly integrated systems often paired with photovoltaic solar installations. Understanding these distinct segment characteristics is essential for stakeholders developing business strategies across the decentralized and centralized energy infrastructure spectrum.

The Renewable Energy Storage value chain is complex and highly interdependent, beginning with upstream analysis focused on raw material extraction and processing. This stage is dominated by the mining and refining of critical minerals, particularly lithium, cobalt, nickel, and manganese, which are essential for electrochemical storage manufacturing. Geopolitical concentration risks are high at this stage, requiring manufacturers to prioritize long-term supply agreements and investigate recycling pathways to ensure material security. The subsequent manufacturing phase involves cell production, module assembly, and integration into full battery racks, where companies like CATL, LG Energy Solution, and Samsung SDI wield significant market influence due to their technological expertise and economies of scale in gigafactories.

Midstream analysis primarily covers the system integration and distribution channels. System integrators, such as Fluence and Wartsila, specialize in combining battery hardware, power conversion systems (PCS), and sophisticated battery management systems (BMS) into functional, reliable BESS units tailored to specific grid requirements. The distribution channel is bifurcated into direct sales to large utilities and Independent Power Producers (IPPs) for utility-scale projects, and indirect sales through installers, developers, and energy service companies (ESCOs) for the distributed residential and C&I markets. The effectiveness of the indirect channel is highly dependent on streamlined regulatory processes and efficient installer training programs to maintain product quality and safety across widespread deployments.

Downstream analysis focuses on deployment, operations, and end-of-life management. Deployment involves site preparation, installation, and grid interconnection, often requiring extensive regulatory approvals and specialized engineering procurement and construction (EPC) services. Operations are increasingly reliant on digital services, utilizing AI and advanced analytics for performance monitoring, predictive maintenance, and optimizing revenue stacking (participating in multiple markets simultaneously). Finally, end-of-life management, including battery recycling and repurposing (second life applications), is becoming a critical segment, driven by environmental mandates and the necessity to close the material loop and minimize waste generation from large battery installations.

The Renewable Energy Storage Market serves a diverse base of potential customers, segmented predominantly by their objectives concerning energy reliability, cost management, and regulatory compliance. The largest end-user segment is Utility Companies and Transmission System Operators (TSOs). These customers purchase large-scale storage solutions for fundamental grid purposes: stabilizing fluctuating renewable generation, providing fast-acting ancillary services (like frequency response), deferring costly transmission upgrades, and ensuring resource adequacy to meet peak demand reliably. Their procurement decisions are characterized by large volume, long-term contracts, and high requirements for technical specifications and safety certifications, often driven by government mandates and regulatory oversight.

The second major customer group encompasses Commercial and Industrial (C&I) entities, including factories, data centers, retail chains, and large campuses. These buyers primarily seek energy storage to reduce operational expenditures, specifically minimizing high demand charges imposed during peak load periods, and achieving greater energy independence. For critical operations like data centers and healthcare facilities, storage serves as essential backup power, providing crucial resilience against grid failures. C&I customers often prioritize systems that integrate seamlessly with existing building energy management systems (BEMS) and renewable generation assets, focusing on rapid return on investment (ROI) through sophisticated load shifting strategies.

Finally, Residential consumers represent a high-growth segment, driven by the desire for energy bill reduction through solar self-consumption optimization and increasing necessity for home backup power, particularly in regions experiencing frequent power outages due to aging infrastructure or extreme weather. These potential customers prioritize user-friendly interfaces, compact design, warranty terms, and brand reliability. The buying process for residential customers is often facilitated through solar installers and authorized distributors, making efficient channel management and strong consumer trust vital components for market penetration in this decentralized segment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 25.2 Billion |

| Market Forecast in 2033 | USD 71.8 Billion |

| Growth Rate | CAGR 15.5% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Tesla, Fluence, LG Energy Solution, CATL, BYD, Siemens Energy, Wartsila, GE Renewable Energy, Contemporary Amperex Technology Co. Limited (CATL), Samsung SDI, Northvolt, Enphase Energy, Vistra Corp., Hitachi Energy, Mitsubishi Electric, Sumitomo Electric, Eos Energy Enterprises, Energy Vault, NEXTracker, Toshiba |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Renewable Energy Storage Market is dominated by electrochemical storage, primarily Lithium-ion (Li-ion) batteries, which represent the current benchmark for performance due to their high energy density, modularity, and rapid response time, making them ideal for short-to-medium duration applications like frequency regulation and arbitrage. Significant R&D is focused on improving Li-ion safety (e.g., LFP chemistry’s thermal stability), cycle life, and reducing material cost. Furthermore, advancements in solid-state battery technology promise higher energy density and enhanced safety without the use of flammable liquid electrolytes, although their commercial readiness for large-scale grid applications is still maturing. This segment dictates the market's pace of cost reduction and scaling capability globally, underpinned by massive investments in gigafactory production capacity.

Beyond Li-ion, the market is actively pursuing diverse alternatives to address the critical need for Long-Duration Energy Storage (LDES), which requires systems capable of storing energy for 10 hours up to several weeks. Flow Batteries, specifically Vanadium Redox Flow Batteries (VRFBs), offer a compelling solution due to their decoupled power and energy capacities, inherent non-flammability, and minimal degradation over thousands of cycles, making them highly suitable for multi-hour daily cycling. Mechanical storage, including traditional Pumped Hydro Storage (PHS) and modern Compressed Air Energy Storage (CAES), continues to play a vital role, especially PHS, which currently accounts for the vast majority of installed storage capacity worldwide, despite its geographic limitations and high upfront environmental impact.

Emerging technologies, critical for future decarbonization pathways, include Thermal Energy Storage (TES) and the integration of Power-to-Gas solutions, specifically Green Hydrogen. TES utilizes materials like molten salts or packed beds to store heat generated from excess renewable electricity, offering cost-effective LDES, especially when coupled with concentrating solar power plants. Green Hydrogen, produced via electrolysis using renewable electricity, allows energy to be stored chemically and repurposed for power generation, heating, or transportation, serving as the ultimate solution for seasonal storage. The technological landscape is therefore shifting towards a hybrid future where optimal storage portfolios integrate short-duration, high-power batteries with long-duration, high-energy non-battery solutions to meet all facets of grid reliability and flexibility demands.

The primary driving force is the imperative for grid stability and reliability when integrating high penetrations of intermittent renewable energy sources like solar and wind. Storage systems mitigate variability, allowing utilities to accurately forecast and dispatch clean power, thereby reducing reliance on carbon-intensive peaking power plants and meeting aggressive global decarbonization mandates.

The market is addressing LDES through significant investment in non-lithium-ion technologies. This includes the commercialization of flow batteries (e.g., vanadium redox), which offer scalable energy capacity and long cycle life, and advanced mechanical solutions like compressed air and gravity-based storage. Furthermore, the development of green hydrogen production for seasonal and multi-day storage is gaining strategic importance as the long-term solution.

Lithium-ion (Li-ion) batteries, particularly the LFP (Lithium Iron Phosphate) chemistry, currently dominate the market. LFP is favored for grid-scale applications due to its lower cost per kilowatt-hour, enhanced thermal stability (safety), and long cycle life compared to higher energy density chemistries like NMC, making it the most proven and scalable technology for short-to-medium duration grid support.

AI maximizes storage value by enabling sophisticated operational optimization. AI-driven software forecasts renewable generation and load profiles with high accuracy, optimizing charge/discharge cycles for revenue stacking (participating in multiple ancillary markets). Additionally, AI manages predictive maintenance, extending the overall asset lifespan and improving operational safety.

Utility-scale storage focuses on grid services like frequency regulation, capacity firming, and transmission deferral, often involving multi-megawatt installations driven by regulatory mandates. C&I storage focuses on economic value for the business, specifically reducing peak demand charges, optimizing solar self-consumption, and providing resilience against localized power outages, typically involving smaller, customer-owned modular systems.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.