ID : MRU_ 437693 | Date : Dec, 2025 | Pages : 249 | Region : Global | Publisher : MRU

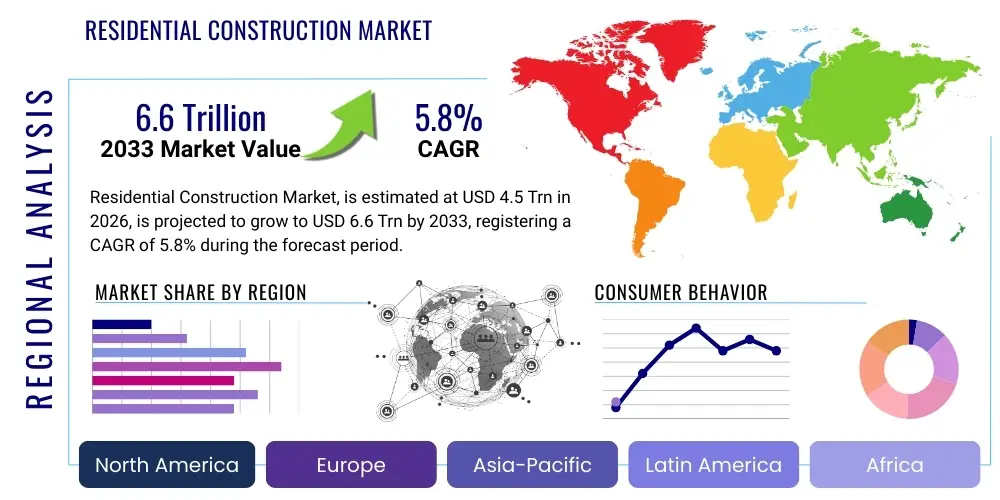

The Residential Construction Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at $4.5 Trillion USD in 2026 and is projected to reach $6.6 Trillion USD by the end of the forecast period in 2033. This robust growth trajectory is underpinned by persistent global urbanization trends, shifting demographic patterns favoring smaller household sizes, and significant infrastructural investments in emerging economies aimed at alleviating housing shortages. The market expansion reflects a consistent demand for new housing units, driven by first-time homeowners, migratory trends, and the necessity for modern, energy-efficient residential structures that comply with increasingly stringent environmental regulations.

The Residential Construction Market encompasses the entire scope of building and renovation activities related to housing units, ranging from single-family homes and detached dwellings to multi-family structures such as apartments, condominiums, and townhouses. The primary product involves the physical structure and associated site development necessary to create habitable living spaces. Major applications include new build projects (which account for the largest market share), repair and remodeling, and specialized adaptive reuse of non-residential buildings into residential units. Key benefits derived from this sector include job creation, economic stability through investment multipliers, and the provision of essential societal infrastructure. The market is fundamentally driven by population growth, sustained economic prosperity facilitating mortgage availability, favorable government policies promoting homeownership, and the imperative to replace aging housing stock with resilient and technologically integrated modern structures.

Global business trends in the Residential Construction Market are heavily centered on innovation in construction methodology, specifically the adoption of Modular and Prefabricated Construction (P&MC) to combat labor shortages and increase construction speed while reducing waste. Sustainable building practices, including the widespread use of green materials and Net-Zero Energy (NZE) home design, are rapidly moving from niche requirements to mainstream standards, particularly in developed economies. Regionally, the Asia Pacific (APAC) market maintains its dominance, fueled by rapid urbanization in China, India, and Southeast Asian nations, demanding massive-scale housing solutions. North America and Europe, while slower in growth rate, lead in technological integration, focusing heavily on smart home systems and efficient project management solutions. Segment trends show a significant pivot towards multi-family units in dense urban centers due to land scarcity and affordability challenges, while the single-family segment remains strong in suburban expansion areas, catering to luxury and spacious living demands. The overall market resilience is tied to government fiscal stimuli designed to stabilize housing markets post-economic volatility.

User queries regarding the impact of Artificial Intelligence (AI) on the Residential Construction Market frequently revolve around optimizing project timelines, managing supply chain unpredictability, enhancing safety protocols, and automating design processes. Key concerns center on the potential displacement of skilled manual labor and the high initial investment required for sophisticated AI deployment. Users are highly interested in how AI can streamline pre-construction phases, specifically regarding generative design capabilities that can quickly test thousands of viable architectural layouts based on budget, regulatory, and environmental constraints. Furthermore, there is a strong expectation that AI will revolutionize risk management by analyzing vast datasets concerning material price volatility, weather patterns, and subcontractor performance, leading to more accurate project bidding and scheduling.

The implementation of AI algorithms is also being viewed as critical for operational efficiency on site. AI-powered computer vision systems are deployed for continuous site monitoring, ensuring adherence to safety standards and construction blueprints, significantly reducing errors that typically lead to costly rework. This proactive quality control and defect detection mechanism is seen as a major value proposition for developers seeking to maintain high building standards. Additionally, AI optimizes resource allocation, predicting equipment maintenance needs and managing logistics for just-in-time delivery of materials, directly addressing persistent issues related to construction delays and material wastage, thereby boosting overall project profitability and sustainability metrics within the residential sector.

The dynamics of the Residential Construction Market are shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), which collectively constitute the primary impact forces. A major driver is the accelerating pace of global urbanization, particularly the movement of populations into metropolitan and peri-urban areas, necessitating substantial investment in housing infrastructure. Additionally, governmental incentives, such as tax credits and subsidies aimed at promoting sustainable building and affordable housing, provide strong market momentum. However, the market faces significant restraints, including severe skilled labor shortages globally, which inflate operational costs and slow project completion rates. Fluctuations in global commodity prices, especially for key materials like lumber, steel, and concrete, introduce high cost unpredictability, further restraining market potential and affecting housing affordability.

Opportunities within the sector are primarily linked to technological adoption and sustainability mandates. The rising demand for Net-Zero Energy (NZE) homes and smart residential buildings offers substantial growth avenues for companies specializing in integration technologies and high-performance materials. Furthermore, the imperative to address the climate crisis is driving innovation in Modular and Off-Site Construction (OSC) techniques, which promise faster, more efficient, and less wasteful construction processes. These innovative methods also help mitigate the impact of on-site labor scarcity. The collective impact forces push the industry toward consolidation and vertical integration, where firms seek to control more of the value chain to manage risks associated with supply chain volatility and ensure adherence to increasingly complex regulatory standards focused on environmental performance and structural resilience.

The Residential Construction Market is rigorously segmented to understand the diverse demands and supply characteristics across various operational dimensions. Primary segmentation is based on the type of dwelling, construction methodology employed, and the geographic location/end-user profile. This analysis is crucial for developers and investors to target specific consumer needs, such as the growing demand for smaller, more sustainable urban apartments versus larger, technology-integrated single-family homes in suburban peripheries. The structural breakdown helps highlight areas where innovation, such as modular building, is gaining traction versus regions where traditional stick-built methods remain dominant due to established supply chains or regulatory inertia.

Further segmentation by construction method reveals a growing shift toward pre-fabricated and modular construction, especially in regions battling severe weather impacts or chronic labor shortages, as these methods ensure standardized quality and accelerated delivery times. Concurrently, the segmentation by end-user location (urban, suburban, rural) demonstrates distinct investment strategies; urban areas focus on high-density multi-family structures for efficiency and land utilization, while suburban markets prioritize horizontal expansion and single-family detached homes that cater to family-oriented demographics seeking space and privacy. Understanding these distinct segments allows for optimized capital deployment and strategic marketing tailored to regional economic conditions and consumer preferences regarding housing density and lifestyle.

The value chain of the Residential Construction Market is characterized by a sequential flow starting from raw material extraction and ending with property sales and management. Upstream activities involve land acquisition, financing, architectural design, and the procurement of bulk materials (cement, lumber, steel, and aggregates). Efficiency in this phase heavily dictates project profitability; delays in permitting or fluctuating material costs directly impact the downstream construction timeline and budget. Key upstream players include specialized financial institutions, land developers, and large industrial material suppliers who operate on a global scale and whose price stability is essential for the contractor ecosystem.

The midstream segment involves the core construction processes: site preparation, foundation laying, structural framing, and the installation of Mechanical, Electrical, and Plumbing (MEP) systems, typically executed by general contractors and a network of specialized subcontractors. Downstream activities focus on finishing work, interior design, marketing, sales, and long-term property management. Distribution channels are complex, involving both direct purchasing from major manufacturers (especially for high-volume items like concrete) and indirect distribution through wholesalers, retailers, and specialized construction supply outlets for smaller, technical components. The trend toward vertical integration sees larger firms acquiring material suppliers or design capabilities to internalize control and capture greater margin along the entire value chain.

The potential customer base for the Residential Construction Market is segmented primarily by purchasing intent and dwelling requirement. The largest segment comprises first-time homeowners, typically young professionals or small families seeking affordable and entry-level housing solutions, often focusing on multi-family units in urban-adjacent areas due to financial constraints and lifestyle preferences. The second major customer group consists of move-up buyers—established homeowners seeking larger, higher-quality properties (often single-family detached homes) in desirable suburban locations, driven by factors like family expansion, increased income, and preference for amenities.

A third critical segment includes institutional investors, real estate funds, and build-to-rent operators, who purchase residential structures, particularly multi-family complexes, for long-term rental income. These customers prioritize operational efficiency, low maintenance costs, and high occupancy rates, driving demand for technologically advanced, durable, and easily managed properties. Finally, niche customers include retirees seeking specialized housing (e.g., senior living communities) and individuals commissioning bespoke, luxury custom homes. Successful engagement with potential customers requires construction firms to align their building solutions with highly specific demographic needs, financial capabilities, and evolving desires for smart home integration and sustainable living environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $4.5 Trillion USD |

| Market Forecast in 2033 | $6.6 Trillion USD |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | DR Horton, Lennar Corporation, PulteGroup, Toll Brothers, KB Home, NVR Inc., Taylor Wimpey, Barratt Developments, Vanke, Country Garden, China Evergrande, Skanska, Balfour Beatty, Laing O'Rourke, Hochtief, ACS Group, Vinci, Bouygues Construction, Shanghai Construction Group, Sekisui House |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Residential Construction Market is undergoing rapid transformation, moving away from traditional manual processes towards digital integration and automation. Key technologies driving this change include Building Information Modeling (BIM), which provides a comprehensive digital representation of the building project, facilitating collaboration, reducing errors, and improving lifecycle management of the asset. BIM adoption is becoming standard practice globally, enabling better clash detection and optimizing material quantities, which directly impacts project cost and environmental footprint. Furthermore, the integration of advanced project management software utilizing cloud platforms ensures real-time communication between site, office, and supply chain partners, enhancing transparency and efficiency.

Robotics and automation are increasingly crucial, particularly in repetitive or hazardous tasks. Automated bricklaying robots, prefabrication facilities utilizing assembly line techniques, and drone-based site monitoring are becoming common. Crucially, Modular and Off-Site Construction (OSC) relies heavily on high-tech manufacturing processes, including CNC machining, to produce standardized, high-quality components rapidly and efficiently, thereby mitigating on-site risks and labor dependency. These industrialized construction techniques are reshaping the supply dynamics, treating building components more like manufactured goods than custom constructions.

Moreover, the adoption of specialized smart home technologies and sustainable building systems represents a significant technological shift focused on the end-user experience and environmental performance. This includes integrated IoT sensors for energy management, predictive maintenance, and security, alongside high-efficiency HVAC systems, solar panels, and smart glazing. The convergence of construction technology (ConTech) and sustainability requirements is forcing contractors to become adept at integrating complex digital and energy systems from the initial design phase, requiring specialized skills and a significant shift in operational mindset.

Regional dynamics play a crucial role in the global Residential Construction Market, reflecting disparities in economic maturity, population growth, and regulatory frameworks. The Asia Pacific (APAC) region stands out as the primary growth engine, largely due to sustained, high-intensity urbanization coupled with massive infrastructure investments in countries like India and Indonesia. China, despite recent economic stabilization efforts, maintains a vast market size driven by large-scale public and private housing projects designed to accommodate internal migration. The sheer volume of new units required in APAC ensures its dominance in terms of physical market size and material consumption.

In North America and Europe, market growth is generally slower but highly focused on quality, sustainability, and technological integration. These regions lead in the adoption of advanced construction technologies such as BIM, modular construction, and sustainable materials, driven by stringent energy efficiency mandates (e.g., the European Union’s Energy Performance of Buildings Directive). Labor scarcity and high wages in these regions further incentivize the deployment of automation and off-site manufacturing processes. The market emphasis shifts from sheer volume to high-value, resilient, and smart residential units.

Latin America and the Middle East & Africa (MEA) present a mixed landscape. MEA, particularly the GCC nations, witnesses robust growth fueled by ambitious national visions (like Saudi Vision 2030) that necessitate rapid urban development and housing provision, often attracting large international contractors. Latin America’s market growth is highly susceptible to macro-economic volatility and interest rate policies, but pockets of significant opportunity exist in addressing informal settlements and upgrading existing housing stock, often supported by government-backed affordable housing programs. These regions are increasingly becoming adopters of prefabricated techniques to speed up housing delivery under challenging logistical and financial conditions.

The Residential Construction Market is projected to exhibit a Compound Annual Growth Rate (CAGR) of 5.8% between the forecast years of 2026 and 2033, driven by persistent housing demand and technological adoption.

The skilled labor shortage significantly restrains market efficiency by inflating operational costs and increasing project timelines. This pressure is accelerating the industry's shift towards industrialized methods like Modular and Off-Site Construction (OSC) and robotics integration.

Modular and Prefabricated Construction (P&MC) is gaining substantial traction because it allows for high-quality, factory-controlled assembly, optimized material use, and easier integration of Net-Zero Energy (NZE) design components compared to traditional on-site methods.

AI plays a critical role in optimizing pre-construction phases through generative design, enhancing project management via predictive scheduling, and improving site safety and quality control through real-time computer vision analysis.

The Asia Pacific (APAC) region currently holds the largest market share, fueled by massive housing demand driven by rapid urbanization and high population density, particularly in emerging economies such as China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.