ID : MRU_ 431385 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

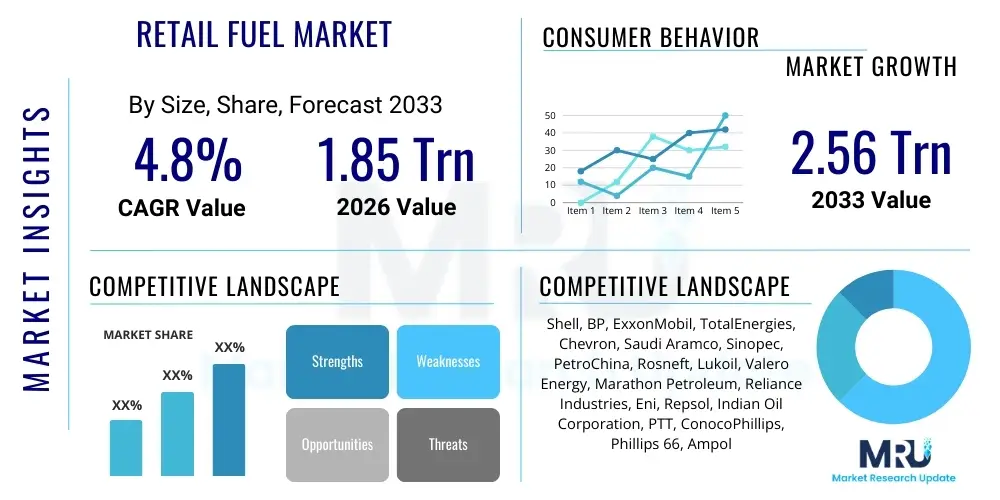

The Retail Fuel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 1.85 Trillion in 2026 and is projected to reach USD 2.56 Trillion by the end of the forecast period in 2033.

The Retail Fuel Market encompasses the extensive network of service stations and refueling points globally responsible for distributing refined petroleum products, compressed natural gas (CNG), liquefied petroleum gas (LPG), and increasingly, alternative fuels such as electricity and hydrogen, directly to end-users. This market serves as the critical final link in the petroleum supply chain, ensuring mobility for road transportation, aviation, and marine sectors. Given the massive scale of global transportation and logistical demands, the retail fuel sector remains foundational to the world economy, despite growing pressures from decarbonization initiatives and the accelerating transition toward electric vehicles (EVs).

The core product offerings traditionally include gasoline (petrol) and diesel, categorized by various octane levels and additive packages tailored for specific engine performance and regulatory compliance. Beyond liquid fuels, modern retail fuel stations have evolved into comprehensive mobility hubs, incorporating non-fuel retail (NFR) services such as convenience stores, food service, and advanced car wash facilities. This diversification is crucial for operators seeking to maintain profitability as fuel margins fluctuate and volumes potentially decrease in developed economies due to energy transition policies.

Major applications of retail fuel span across personal vehicle consumption, commercial fleet operations, and public transit systems. Key benefits provided by this infrastructure include widespread accessibility, operational reliability, and the ability to enable high-capacity long-distance travel, which is still challenging for nascent alternative fuel infrastructures. The market is driven primarily by global population growth, urbanization, and expanding commercial logistics networks, particularly in rapidly developing regions like Asia Pacific and parts of Africa, where conventional Internal Combustion Engine (ICE) vehicles remain dominant.

The Retail Fuel Market is experiencing a pivotal structural transformation, moving away from a volume-driven model towards a service- and convenience-oriented framework. Current business trends indicate a strong focus on margin optimization through non-fuel retail (NFR) offerings, leveraging digital technologies to enhance customer loyalty, and streamlining operational efficiency. Major fuel retailers are actively investing in modernizing their forecourts, integrating advanced payment solutions, and developing loyalty programs that capture detailed consumer data to enable highly personalized marketing strategies. Furthermore, partnerships are increasingly being formed with technology providers and quick-service restaurant (QSR) chains to maximize the utility and revenue per customer visit, mitigating risks associated with volatile oil prices and the long-term decline in traditional fuel consumption.

Regionally, the market exhibits sharp contrasts. Asia Pacific (APAC) stands out as the primary growth engine, fueled by burgeoning vehicle populations, expanding middle classes, and massive infrastructure development in countries like China, India, and Indonesia. These regions necessitate extensive build-out of traditional fueling infrastructure, providing short- to medium-term volume growth. Conversely, North America and Europe, classified as mature markets, are leading the transition toward electrification and alternative fuels. Here, the strategic focus shifts from building new sites to retrofitting existing stations with high-speed EV charging facilities and integrating sustainable practices, often driven by aggressive governmental decarbonization mandates and stringent Euro emission standards.

Segment trends highlight a distinct evolution in the Fuel Type category. While gasoline and diesel maintain dominance by volume, the fastest-growing segments are centered around new energy solutions, particularly Electric Vehicle (EV) charging infrastructure and, to a lesser extent, hydrogen fueling stations (especially for commercial heavy-duty vehicles). In terms of Service Type, self-service stations dominate globally due to lower operating costs, but there is a growing trend towards automated, unmanned stations utilizing advanced surveillance and payment technology. Fleet management and commercial applications remain critical revenue streams, characterized by long-term contracts and dedicated bulk fueling options, which are also beginning to incorporate electric and low-carbon fuel solutions.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Retail Fuel Market commonly center on improving profitability, optimizing complex logistics, and managing the disruptive transition to electric mobility. Key concerns revolve around how AI can enhance dynamic pricing strategies, predict equipment failure (preventive maintenance), and personalize the forecourt experience for increasingly demanding consumers. There is significant user interest in leveraging AI for supply chain resilience, particularly in anticipating demand fluctuations caused by weather events or economic shifts, ensuring that fuel inventory levels are optimally maintained at each station without incurring excessive storage costs or facing stock-outs. Furthermore, users are exploring AI’s role in integrating and managing disparate data streams—from pump sales and convenience store purchases to external traffic patterns—to generate actionable business intelligence.

AI’s influence is profound in optimizing retail operations, fundamentally shifting decision-making from reactive to predictive. Advanced machine learning algorithms are now employed to execute dynamic pricing, adjusting fuel costs minute-by-minute based on competitor pricing, local traffic data, and real-time inventory levels, thereby maximizing margin capture across the retail network. This capability is critical in a high-volume, low-margin business environment. Concurrently, AI supports sophisticated personalization within the non-fuel retail sector; by analyzing past purchasing behavior, AI systems can push tailored promotions and discounts via mobile apps or pump screens, significantly boosting cross-selling opportunities and customer engagement, turning a standard refuel stop into a comprehensive consumer experience.

Moreover, AI is playing a critical role in infrastructure management for alternative fuels. For EV charging, AI algorithms optimize grid load management, predicting charging patterns to stabilize energy supply and dynamically adjusting charging rates based on grid capacity and electricity prices. This ensures efficient utilization of expensive charging assets and minimizes operational costs. For traditional infrastructure, AI-powered predictive maintenance utilizes sensor data from pumps, tanks, and dispensers to forecast component failures, allowing proactive repairs and minimizing costly downtime, which is essential for maintaining a high level of operational reliability across vast, dispersed retail networks.

The Retail Fuel Market is characterized by a complex interplay of Drivers, Restraints, and Opportunities (DRO) that collectively shape its trajectory and influence investment decisions globally. Key drivers bolstering the market include the continued reliance on road transport for global logistics and passenger mobility, particularly in emerging economies where vehicle ownership is soaring and public transport infrastructure lags. The sustained, albeit fluctuating, demand for conventional liquid fuels in hard-to-abate sectors like long-haul trucking and aviation ensures a foundational level of volume stability. Opportunities are primarily centered around diversification into non-fuel retail (NFR), the strategic build-out of next-generation infrastructure (EV charging and hydrogen), and leveraging digital transformation (IoT, cloud services) to create superior customer experiences and enhance operational efficiency.

However, the market faces significant and rapidly intensifying restraints that demand strategic adaptation from retailers. The most critical restraint is the aggressive global push for decarbonization and the subsequent governmental mandates and incentives promoting the adoption of electric vehicles (EVs). As the global EV fleet grows, traditional fuel volume demand will inevitably peak and begin a long-term decline, severely impacting profitability for non-diversified stations. Furthermore, increasing regulatory complexity, including stricter emission standards (e.g., Euro 7) and requirements for incorporating biofuels, adds significant operational and capital expenditure burdens. Geopolitical instability, manifesting in highly volatile crude oil prices and disrupted supply chains, also acts as a powerful external restraint, making long-term financial forecasting extremely challenging.

The cumulative impact forces dictate that survival in the retail fuel sector requires a fundamental shift towards becoming holistic mobility service providers rather than purely fuel distributors. Operators must rapidly accelerate their integration of low-carbon energy sources and significantly expand high-margin NFR offerings to compensate for the anticipated erosion of fuel margins. The transition necessitates substantial upfront investment in technology—both for back-office optimization and for customer-facing digital platforms. Stations that fail to adapt their infrastructure to accommodate both traditional refuelers and electric charging customers, or those that neglect digitalization, face significant risks of obsolescence as consumer preferences pivot toward sustainable and convenient energy solutions.

The Retail Fuel Market is structurally segmented across key parameters including the type of fuel dispensed, the primary application or end-user, and the service model employed at the station. This segmentation highlights the dynamic evolution of the market, where traditional fuel dominance is gradually yielding ground to alternative energies, particularly within the 'Fuel Type' segment. Analysis of these segments is vital for stakeholders to understand shifting consumer behavior, target specific regulatory environments, and strategically allocate capital towards high-growth or high-margin areas, such as developing premium fuel blends or installing high-power EV charging infrastructure in key urban corridors.

The Retail Fuel Market value chain is deeply integrated and extends from the initial upstream extraction of crude oil and natural gas through the complex midstream refining and logistics processes, culminating in the downstream retail distribution and customer interaction. Upstream analysis focuses on securing the crude supply, which dictates feedstock quality and pricing volatility for the entire chain. Midstream operations involve the complex refining process where crude oil is converted into usable products (gasoline, diesel, jet fuel) and the massive logistical effort required for storage, pipeline transport, and tanker distribution to regional terminals and bulk storage facilities. Efficiency at this stage is crucial, as transportation costs and storage losses significantly impact final retail margins.

The downstream segment, which constitutes the retail fuel market itself, involves the operation of service stations, which act as the direct interface with the consumer. Key activities here include inventory management, quality control, pricing strategy implementation, and the vital integration of non-fuel retail operations. Effective downstream management is essential for margin preservation, as competition is fierce and pricing decisions must be precise and localized. The shift towards multi-energy retail—handling liquid fuels, charging electricity, and potentially hydrogen—adds substantial complexity to the storage, dispensing, and safety protocols required at the station level, demanding significant capital expenditure and technological upgrades.

Distribution channels in the retail fuel market are predominantly structured around either direct operations (company-owned, company-operated or COCO) or indirect models (dealer-owned, dealer-operated or DODO). The COCO model offers operators maximum control over brand standards, pricing, and NFR strategy but demands higher capital investment and operational overhead. Conversely, the DODO model, while providing rapid network expansion and shared capital burden, requires careful management of quality control and adherence to branding guidelines. Successful market players often employ a hybrid strategy, using COCO sites in high-traffic urban areas to test new concepts and leverage DODO partnerships for broader regional coverage, ensuring optimal reach and operational flexibility across diverse geographic markets.

The customer base for the Retail Fuel Market is diverse, encompassing both B2C (individual consumers) and B2B (commercial enterprises and fleet operators) segments, each with distinct consumption patterns and purchasing criteria. Individual consumers represent the largest volume segment and prioritize convenience, competitive pricing, brand loyalty programs, and high-quality, efficient non-fuel retail offerings. As the energy transition accelerates, this segment is increasingly split between traditional ICE drivers and EV owners, requiring retailers to develop hybrid forecourts capable of serving both groups seamlessly, often focusing on high-speed charging and comfortable waiting amenities for EV users.

The B2B segment, comprising commercial fleets (long-haul logistics, delivery services, construction), public transportation authorities, and governmental agencies, represents a highly valuable revenue stream characterized by high-volume contracts and stringent operational requirements. These customers prioritize fuel quality consistency, reliable network coverage, specialized bulk fueling infrastructure (e.g., dedicated truck stops), and advanced fleet management services, including centralized billing and usage tracking. For this segment, the shift toward alternative fuels is driven less by individual preference and more by regulatory pressure and the need for operational cost reduction through adoption of lower-emission fuels like renewable diesel, CNG, or dedicated electric fleets.

Beyond traditional road users, the market also serves industrial clients requiring specialized fuels and lubricants, and, in a broader context, the aviation and marine industries, though the latter often use dedicated bunkering facilities rather than standard retail stations. The evolving nature of mobility means that retailers are now viewing electric vehicle owners not just as charging customers, but as potential high-value non-fuel retail consumers. Consequently, the focus is shifting to capturing the ‘dwell time’—the 20-40 minutes an EV owner spends charging—by providing premium food, beverages, connectivity, and clean, comfortable facilities, transforming the fuel station into a destination for various services.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.85 Trillion |

| Market Forecast in 2033 | USD 2.56 Trillion |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Shell, BP, ExxonMobil, TotalEnergies, Chevron, Saudi Aramco, Sinopec, PetroChina, Rosneft, Lukoil, Valero Energy, Marathon Petroleum, Reliance Industries, Eni, Repsol, Indian Oil Corporation, PTT, ConocoPhillips, Phillips 66, Ampol |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Retail Fuel Market is undergoing a significant technological renaissance driven by the necessity for operational efficiency, enhanced security, and the integration of new energy dispensing methods. Digitalization forms the bedrock of this transformation, with cloud-based Point-of-Sale (POS) systems replacing legacy hardware, enabling real-time inventory tracking, centralized pricing control across vast networks, and seamless integration with loyalty programs and mobile payment solutions. The implementation of Internet of Things (IoT) sensors within underground storage tanks and dispensing pumps provides continuous data on fuel levels, quality, and potential leaks, dramatically improving environmental compliance and inventory accuracy, minimizing ‘shrinkage,’ and facilitating predictive maintenance based on machine health data.

A critical area of technological focus is customer interaction and payment infrastructure. The widespread adoption of mobile payment technologies, contactless payment (NFC), and ‘pay-at-the-pump’ mobile apps has reduced friction at the dispenser, speeding up transactions and improving throughput, especially at high-volume stations. Furthermore, retailers are adopting sophisticated forecourt management systems that utilize camera analytics and AI to optimize traffic flow, monitor safety compliance, and even manage queue times for charging stations. This technological overlay is essential for managing the growing complexity of hybrid forecourts that must safely and efficiently dispense multiple energy types alongside traditional fuels.

The technological landscape also includes significant investments in Electric Vehicle (EV) charging infrastructure and hydrogen dispensing units. For EVs, this involves the deployment of High-Power Charging (HPC) technology, typically requiring complex electrical grid upgrades and advanced battery storage solutions to manage peak load demand. Software platforms are crucial for operating these charging networks, handling billing, reservation systems, and communicating real-time charger status. Simultaneously, advancements in cybersecurity are paramount, as connected stations transmitting sensitive payment and inventory data are increasingly susceptible to cyber threats, requiring robust security protocols and continuous monitoring across the entire retail network.

The global Retail Fuel Market exhibits highly diversified regional dynamics, reflecting varying levels of economic development, regulatory environments, and the pace of the energy transition. Asia Pacific (APAC) dominates the market in terms of volume growth, driven by massive urbanization, the rapid expansion of the middle class, and lagging EV adoption rates in several major economies. Countries such as India and Indonesia continue to see robust growth in conventional vehicle sales, necessitating ongoing investment in traditional fuel infrastructure. However, APAC is also home to pioneering markets like China, which leads globally in both EV adoption and the scale of retail fuel network digitalization, presenting a mixed landscape of conventional growth and rapid technological transition.

North America and Europe represent mature markets characterized by intense consolidation, rigorous environmental regulations, and a mandated shift toward sustainable energy sources. In Europe, the focus is heavily on decommissioning older, less efficient sites while strategically retrofitting high-traffic locations with ultra-fast EV charging and, in commercial corridors, hydrogen fueling pilots. The European market leads in the deployment of stringent biofuel blending mandates, forcing retailers to adapt their supply chains. North America, while slower in national EV adoption compared to Europe, features large commercial truck stops that are beginning to integrate alternative heavy-duty fuels like CNG and renewable natural gas (RNG), alongside nascent electric truck charging infrastructure.

The Middle East and Africa (MEA) region remains crucial due to its deep connection to the upstream oil sector and the rapid development of infrastructure in Gulf Cooperation Council (GCC) countries. While these regions maintain high per capita fuel consumption, there is growing strategic interest in diversifying national energy portfolios, leading some GCC countries to invest heavily in smart city infrastructure that includes EV charging. Africa presents a vast potential market characterized by fragmented distribution networks and rapid growth in vehicle ownership, necessitating significant future investment in formalized retail infrastructure and logistical solutions to meet escalating demand.

The increasing penetration of EVs will lead to a long-term decline in traditional fuel volumes, compressing margins. Retailers are mitigating this by diversifying revenue through high-margin non-fuel retail (NFR) sales, optimizing operational costs, and strategically integrating EV charging hubs to monetize 'dwell time.'

The critical growth strategy involves transforming the service station into a multi-energy mobility hub. This entails heavy investment in digital infrastructure (loyalty programs, mobile payment), expansion of premium food service offerings (NFR), and the rapid deployment of reliable, fast EV charging points.

Key innovations include AI-driven dynamic pricing, which adjusts fuel costs in real-time to optimize margins; IoT sensors for predictive maintenance and inventory management; and mobile payment platforms that enable seamless, contactless transactions at the pump and in the convenience store.

Asia Pacific (APAC), particularly emerging economies like India and Southeast Asia, is projected to drive the highest volume growth due to rapid urbanization, significant increases in vehicle ownership, and slower relative adoption rates of electric vehicles compared to Western markets.

Electric vehicle (EV) charging infrastructure is the dominant emerging alternative fuel segment, witnessing massive private and public investment. Additionally, compressed natural gas (CNG) and liquefied petroleum gas (LPG) maintain stable presence, while hydrogen fueling is being strategically piloted for heavy-duty commercial vehicle applications.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.