ID : MRU_ 432348 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

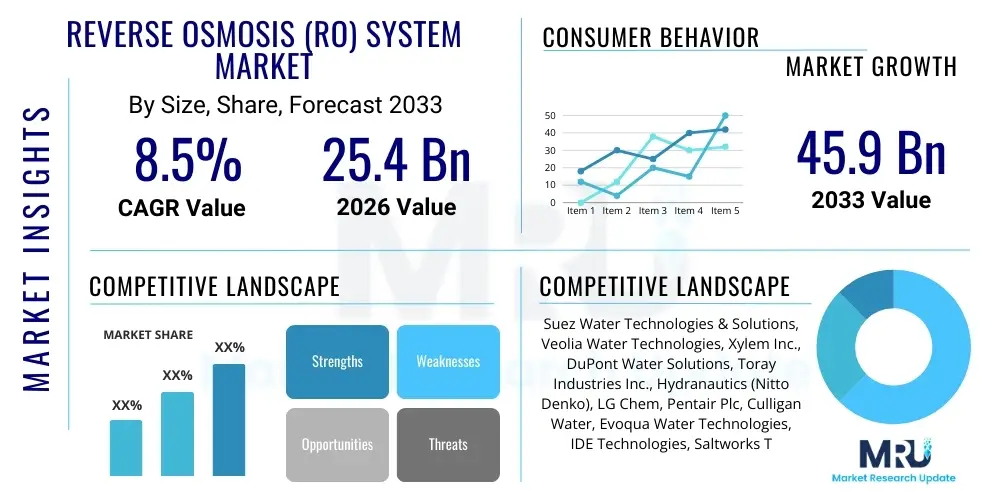

The Reverse Osmosis (RO) System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 25.4 Billion in 2026 and is projected to reach USD 45.9 Billion by the end of the forecast period in 2033.

The Reverse Osmosis (RO) System Market encompasses the design, manufacture, and deployment of semi-permeable membrane technology utilized primarily for water purification, desalination, and contaminant removal. This technology operates by applying pressure to overcome the osmotic pressure, forcing water molecules through the membrane while rejecting dissolved solids, salts, bacteria, and larger particulate matter. The core product offering includes various configurations such as brackish water RO (BWRO), seawater RO (SWRO), and tap water RO (TWRO) systems, catering to diverse needs across municipal, industrial, and commercial sectors. The increasing global scarcity of freshwater resources, coupled with stringent regulatory standards regarding water quality, serves as the fundamental catalyst driving robust adoption rates worldwide.

Major applications of RO systems span essential industries, including pharmaceuticals, food and beverage processing, semiconductor manufacturing, and power generation, where ultra-pure water is a critical input. In the municipal sector, RO is increasingly vital for augmenting existing water supplies through desalination and wastewater reuse projects, providing a resilient solution against drought and population growth pressures. The primary benefits derived from RO adoption include superior water quality, effective removal of emerging contaminants (e.g., PFAS, microplastics), and long-term cost-effectiveness compared to alternative purification methods, particularly in high-salinity environments.

Key driving factors accelerating market expansion include rapid industrialization in developing economies, necessitating high volumes of process water; supportive government initiatives promoting water treatment infrastructure investment; and significant technological advancements focused on improving energy efficiency and reducing membrane fouling. Continuous innovation in membrane materials, such as thin-film nanocomposite (TFN) membranes, is enhancing flux rates and rejection capabilities while simultaneously reducing the overall energy footprint, making RO a more sustainable and economically viable solution across a broader spectrum of applications.

The global Reverse Osmosis (RO) System market demonstrates strong growth momentum, underpinned by increasing environmental awareness and critical needs for potable and industrial-grade water. Business trends indicate a significant shift towards modular, decentralized RO systems, particularly in regions facing infrastructural deficits. Furthermore, manufacturers are focusing heavily on integrating smart monitoring and IoT capabilities to enhance system performance, optimize chemical dosing, and facilitate predictive maintenance, thereby reducing operational expenditure (OpEx) for end-users. Strategic alliances and mergers between membrane manufacturers and system integrators are common, aimed at creating comprehensive, end-to-end water management solutions and capitalizing on large-scale infrastructure projects, especially in the Middle East and Asia Pacific regions.

Regionally, Asia Pacific is projected to maintain the highest growth rate, driven by massive urbanization, burgeoning industrial activity—especially in China and India—and acute water stress. North America and Europe, characterized by high adoption of advanced industrial processes, focus on optimizing existing infrastructure through replacement of legacy systems with high-efficiency RO units featuring energy recovery devices (ERDs). The Middle East remains a cornerstone for large-scale seawater desalination projects (SWRO), propelled by governmental mandates to secure water independence, requiring substantial investment in advanced, high-capacity installations. Latin America and Africa represent emerging opportunities, stimulated by improving economic stability and increasing investment in municipal water treatment facilities.

Segment trends highlight the dominance of the municipal application segment due to substantial governmental spending on public waterworks, particularly desalination. By technology, thin-film composite (TFC) membranes remain the standard, but the fastest growth is observed in TFN membranes, which offer improved durability and resistance to fouling. The industrial segment, especially electronics and pharmaceuticals, requires specialized ultra-pure water systems, driving demand for advanced pre-treatment solutions coupled with RO technology. Furthermore, the residential segment continues its steady growth, driven by consumer concerns over tap water quality and contaminants, leading to high adoption rates of point-of-use and point-of-entry home RO filtration units.

Analysis of common user inquiries reveals that key themes concerning AI integration in the RO market revolve around predictive maintenance capabilities, optimization of operational efficiency (especially energy consumption), and autonomous system control for managing variable feed water quality. Users are particularly interested in how AI algorithms can minimize membrane fouling, extend membrane lifespan, and reduce the high energy costs traditionally associated with RO processes. There is a strong expectation that AI will transition RO systems from reactive maintenance schedules to proactive, performance-based operations, ensuring consistently high-quality permeate while minimizing downtime and chemical usage.

The RO System Market is significantly influenced by a confluence of accelerating drivers, critical restraints, and substantial growth opportunities, collectively shaping the market’s trajectory. Key drivers include the global water crisis and the necessity of utilizing non-conventional water sources like seawater and reclaimed wastewater, making high-efficiency RO systems indispensable. Simultaneously, the market faces constraints related to the high initial capital investment required for large-scale facilities and the energy-intensive nature of older RO technologies, which can limit adoption in resource-constrained regions. Opportunities lie primarily in technological breakthroughs, specifically the commercialization of low-energy membranes and the integration of renewable energy sources to power RO plants, transforming the economic feasibility of desalination globally.

Drivers: The fundamental driver is the exacerbating imbalance between freshwater supply and escalating demand, driven by demographic expansion and accelerated industrialization. Regulatory bodies across key geographies are imposing increasingly strict standards on discharged effluent quality and promoting water recycling and reuse, compelling industries to adopt advanced purification methods like RO. Furthermore, the heightened public awareness regarding contaminants in potable water, especially in developed markets, fuels robust demand for residential point-of-use systems. The pharmaceutical and electronics industries, which require extremely high purity water (e.g., ultrapure water for semiconductor fabrication), rely almost exclusively on multi-stage RO processes, ensuring consistent demand regardless of economic cycles.

Restraints: Significant capital expenditure required for installing high-capacity RO plants poses a major barrier, particularly for developing nations and smaller municipalities. Operational restraints center on membrane fouling and scaling, which necessitate frequent cleaning, reduce efficiency, and lead to increased maintenance costs and downtime. The high specific energy consumption, despite recent technological improvements, remains a considerable challenge, particularly for SWRO applications where energy costs account for a substantial portion of the total water production cost. Furthermore, the issue of brine disposal—the highly concentrated waste product—presents environmental compliance hurdles, requiring specialized and often costly management solutions.

Opportunities: Technological advancements represent the most substantial opportunity, particularly the development and scaling of next-generation membranes (e.g., aquaporin membranes, CNT-enabled membranes) that promise significantly reduced operating pressures and enhanced salt rejection. The rising trend of decentralized water treatment solutions, including containerized and modular RO systems, opens up niche markets in remote industrial sites, disaster relief areas, and small communities, minimizing infrastructure investment requirements. The convergence of RO technology with renewable energy solutions, such as solar or wind power, addresses the energy intensity constraint, creating a pathway toward sustainable and cost-competitive clean water production, especially in sun-rich arid regions globally.

The Reverse Osmosis System Market is comprehensively segmented based on technology type, application, and end-user, providing a granular view of market dynamics and adoption patterns across various sectors. Technology segmentation highlights the distinction between different membrane materials and configurations crucial for diverse water sources, ranging from high-salinity seawater to low-salinity tap water. Application segmentation focuses on the intended use of the purified water, which dictates the system size, complexity, and purity requirements. End-user segmentation delineates the primary consumer categories, illustrating the distinct purchasing behaviors and regulatory environments governing municipal versus industrial use.

The segmentation structure is fundamental for strategic planning, as it illuminates high-growth areas. For instance, the industrial segment, specifically power generation and pharmaceuticals, demands specialized configurations that handle complex water chemistry, leading to higher average selling prices for units in this category. Conversely, the municipal segment drives sheer volume, particularly through large infrastructure bids for seawater desalination plants. Continuous innovation in materials science directly impacts the technology segment, pushing TFN and advanced polymer membranes to the forefront, challenging the dominance of traditional TFC structures.

The Value Chain for the RO System Market begins with the upstream procurement of specialized raw materials, primarily polymers for membrane manufacturing (e.g., polyamide, cellulose acetate), specialized pumping components, and structural metals for pressure vessels and skids. The upstream segment is dominated by highly specialized chemical and materials companies that dictate membrane quality and cost. This is followed by the core manufacturing and integration phase where membrane elements are fabricated and then incorporated into complete RO systems, often requiring sophisticated engineering tailored to specific application requirements such as salinity handling or flow rate capacity. Efficiency and performance are largely determined at this stage, focusing on minimizing energy usage through high-efficiency pumps and energy recovery devices (ERDs).

The downstream activities involve distribution, installation, and comprehensive after-sales service. Distribution channels are highly varied; large, complex municipal and industrial projects typically utilize direct sales and specialized engineering procurement and construction (EPC) firms that manage installation and commissioning. Conversely, residential and light commercial units are generally sold through indirect channels, including dedicated dealers, plumbing suppliers, and increasingly, e-commerce platforms. The profitability of system providers is often heavily reliant on the high-margin aftermarket services, which include regular membrane replacement, chemical supply, and preventative maintenance contracts.

Direct sales are prevalent for bespoke, high-value industrial and municipal projects where intricate technical consultation is mandatory. Indirect channels ensure broader market penetration for standardized, lower-capacity systems. Optimization of the value chain is increasingly focusing on reducing logistical complexity and improving the speed of system deployment, especially for modular solutions. Control over the membrane supply—the critical technology component—provides significant competitive advantage, leading many system manufacturers to vertically integrate or secure long-term contracts with key membrane suppliers to ensure consistent quality and cost control.

Potential customers for Reverse Osmosis systems represent a broad spectrum of entities requiring consistent access to water purified beyond standard municipal limits, ranging from large public utilities managing water scarcity to small homeowners concerned about local water quality. The municipal sector is a primary purchaser, specifically for large-scale SWRO and BWRO plants designed to create new potable water sources or treat wastewater for reuse. These buyers are highly sensitive to lifecycle costs, focusing intensely on energy efficiency, reliability, and guaranteed permeate quality over decades of operation, driven by strict public health and environmental regulations.

The industrial sector constitutes another major customer base, segmented by the required water purity level. The power generation industry requires ultra-pure boiler feed water to prevent scaling and corrosion in critical turbine components, making RO and subsequent deionization necessary. Similarly, the electronics and pharmaceutical industries demand water of the highest purity standards (UPW and WFI, respectively), requiring advanced multi-stage RO systems. These industrial buyers prioritize continuous uptime and system reliability, as interruptions can lead to massive production losses, often leading them to invest in robust redundancy and advanced monitoring systems.

Furthermore, commercial establishments, including hospitality, hospitals, and educational institutions, require mid-sized systems to ensure water quality consistency for their operations, ranging from food preparation to laboratory use. The residential market, though characterized by smaller unit sizes, is volumetrically significant, driven by individual consumer concerns over taste, chlorine, lead, and emerging contaminants, favoring compact, easy-to-install under-sink RO units. The decision-making process for residential consumers is heavily influenced by brand trust and ease of maintenance, whereas industrial buyers focus on total cost of ownership (TCO) and compliance with industry-specific quality specifications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 25.4 Billion |

| Market Forecast in 2033 | USD 45.9 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Suez Water Technologies & Solutions, Veolia Water Technologies, Xylem Inc., DuPont Water Solutions, Toray Industries Inc., Hydranautics (Nitto Denko), LG Chem, Pentair Plc, Culligan Water, Evoqua Water Technologies, IDE Technologies, Saltworks Technologies, Lenntech B.V., Pure Aqua Inc., ROPV Membrane, Koch Separation Solutions, F&P Water Treatment, Hatenboer-Neptun, Dow Chemical Company (Part of DuPont), Membrana GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Reverse Osmosis system market is characterized by a rapidly evolving technological landscape focused intensively on enhancing membrane performance, reducing energy consumption, and improving resistance to biofouling. The core technology remains the Thin-Film Composite (TFC) membrane, typically made of polyamide. However, significant innovation is centered on advanced materials such as Thin-Film Nanocomposite (TFN) membranes, which incorporate nanoparticles (like zeolites or carbon nanotubes) into the polyamide layer. This structural enhancement drastically improves water flux while maintaining or even increasing salt rejection rates, allowing systems to operate efficiently at lower pressures. Furthermore, advancements in anti-fouling coatings and specialized pre-treatment chemistries are critical, addressing the most significant operational challenge faced by RO plant operators globally.

Energy recovery devices (ERDs) constitute another crucial technological segment, particularly for high-pressure seawater RO (SWRO) systems. Devices like pressure exchangers (PX) and turbochargers are essential components that capture hydraulic energy from the high-pressure reject brine stream and transfer it back to the feed stream, substantially minimizing the power consumption required by the main high-pressure pumps. The adoption of high-efficiency pumps and variable frequency drives (VFDs) further allows operators to precisely match energy input to system requirements, contributing significantly to lower overall operational costs and making desalination more economically competitive compared to traditional water sourcing methods.

Future technological advancements are trending towards the integration of sophisticated monitoring and control systems, often leveraging IoT and AI (as discussed previously) to achieve truly adaptive and autonomous operations. Research into next-generation membranes includes biomimetic approaches, such as incorporating aquaporin proteins into synthetic membranes, promising revolutionary increases in permeability and selectivity. Furthermore, hybridization of RO with other membrane processes, like ultrafiltration (UF) for advanced pre-treatment or forward osmosis (FO) for specialized applications, is becoming common practice to manage challenging feed waters and optimize overall water recovery rates, solidifying RO’s position as the central purification backbone.

The global distribution of the Reverse Osmosis System Market is highly correlated with regional water scarcity levels, industrial density, and governmental investment in water infrastructure resilience. Each major geographical region presents a unique set of drivers and application requirements, influencing technology adoption rates and market maturity.

The primary driver is the accelerating global freshwater scarcity coupled with increasingly stringent environmental regulations mandating the treatment and reuse of wastewater and the necessity of utilizing alternative sources like seawater, thereby increasing demand for high-efficiency desalination technology.

AI significantly improves efficiency by enabling predictive maintenance, which reduces unplanned downtime, and by optimizing specific energy consumption (SEC) through dynamic adjustments to pump pressure and flow rates based on real-time feed water quality and operational needs.

The Asia Pacific (APAC) region exhibits the largest growth potential, driven by rapid industrialization, massive urbanization, and extensive government investments in water infrastructure to combat acute water stress, particularly in developing economies like China and India.

The main technical challenges include mitigating membrane fouling and scaling, reducing the high specific energy consumption required to overcome osmotic pressure, and managing the environmental impact and safe disposal of highly concentrated brine effluent.

The most promising technological advancement is the development of Thin-Film Nanocomposite (TFN) membranes, which incorporate nanomaterials to enhance permeability and rejection rates, allowing systems to operate effectively at lower pressures and thus achieve greater energy efficiency.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.