ID : MRU_ 431517 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

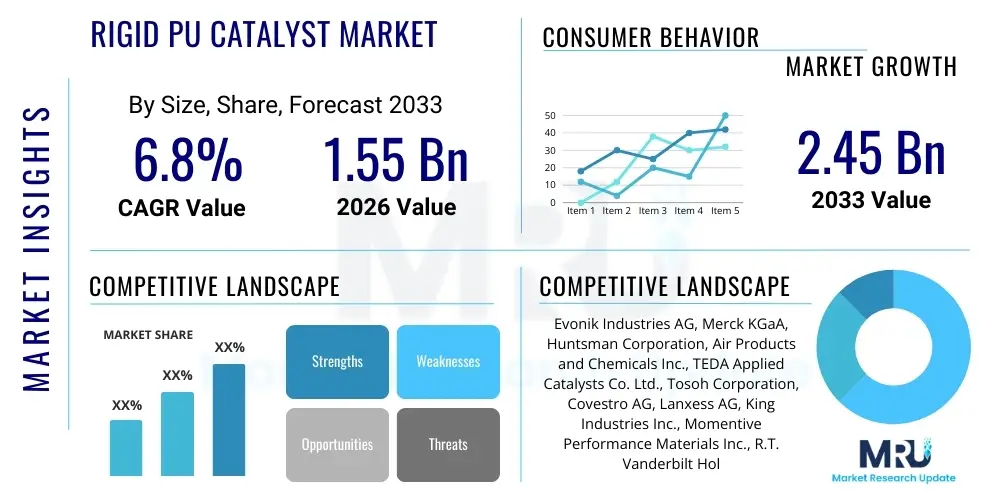

The Rigid PU Catalyst Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 1.55 billion in 2026 and is projected to reach USD 2.45 billion by the end of the forecast period in 2033.

The Rigid PU Catalyst Market encompasses specialty chemical additives crucial for the production of rigid polyurethane (PU) foams. These catalysts, primarily tertiary amines and organometallic compounds, facilitate the precise reaction kinetics necessary for the polymerization of polyols and isocyanates, ensuring the formation of high-quality rigid foam structures characterized by excellent insulation properties and mechanical strength. Rigid PU foams are indispensable in construction (insulation boards, spray foam), refrigeration (appliances and cold chain logistics), and automotive sectors, where energy efficiency and structural integrity are paramount requirements. The market's stability is directly tied to global infrastructure development and the increasing stringency of energy conservation regulations, particularly in developed and rapidly urbanizing economies, which mandates superior thermal efficiency in building materials and appliances.

The primary function of catalysts in rigid PU production is to balance the gelling reaction (chain growth) and the blowing reaction (carbon dioxide formation), which determines the foam’s density, cell structure, and fire performance characteristics. Unlike flexible foams, rigid foams require highly selective catalysts that promote strong cross-linking rapidly, locking in the insulating gas within the closed-cell structure. The shift toward low-global warming potential (GWP) blowing agents, such as hydrofluoroolefins (HFOs), necessitates the continuous development of novel catalyst systems tailored to maintain optimal processing and curing profiles, driving innovation within the market. This technological adaptation ensures that manufacturers can meet both environmental targets and performance demands without compromising production efficiency or final product quality.

Major applications driving the demand for rigid PU catalysts include the burgeoning demand for high-performance insulation in residential and commercial construction, particularly in regions prone to extreme temperatures. Furthermore, the global expansion of the cold chain, spurred by increasing consumption of frozen foods and pharmaceuticals, significantly contributes to catalyst consumption, as rigid PU is the material of choice for freezers, refrigerators, and insulated transport containers. The transition away from older, less efficient insulation materials, coupled with governmental incentives for energy-efficient retrofitting, solidifies the fundamental growth trajectory of the rigid PU catalyst sector, making it a critical enabling market within the broader chemicals industry.

The Rigid PU Catalyst Market demonstrates robust expansion driven primarily by global energy efficiency mandates and sustained growth in the construction and appliance industries. Business trends indicate a strong focus on sustainable catalyst technologies, specifically those offering reduced volatile organic compound (VOC) emissions and enhanced compatibility with next-generation HFO blowing agents. Manufacturers are concentrating efforts on developing non-fugitive, reactive catalysts that chemically bind into the polymer matrix, thereby minimizing environmental impact and improving the long-term integrity of the foam product. Strategic mergers and acquisitions among key chemical providers are noted, aiming to consolidate market share and leverage combined R&D capabilities to address complex regulatory landscapes and performance requirements across diverse geographies.

Regional trends highlight the Asia Pacific (APAC) region as the fastest-growing market, propelled by massive urbanization, infrastructure projects, and the expanding domestic manufacturing base for refrigeration equipment, particularly in China and India. North America and Europe, while mature, exhibit steady demand driven by strict building codes emphasizing thermal performance and ongoing retrofitting activities aimed at improving the energy footprint of existing structures. Regulatory pressures, especially the phase-down of older fluorinated blowing agents under various international protocols, are forcing rapid material substitution and catalyst reformulation across all major regional markets, creating short-term volatility but long-term opportunities for specialized product lines.

Segmentation trends reveal that amine-based catalysts, specifically tertiary amines, maintain market dominance due to their cost-effectiveness and versatility in promoting both gelling and blowing reactions; however, metal-organic catalysts are gaining traction, especially in applications requiring highly specific curing profiles or where enhanced fire resistance is critical. End-user segmentation shows that the construction sector remains the largest consumer, but the appliance and cold chain segments are registering accelerated growth due to increased global food safety concerns and the need for reliable temperature-controlled transport solutions. Innovation in polyisocyanurate (PIR) foam production, which uses catalysts to impart superior fire resistance, is also a significant trend influencing segment growth dynamics.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Rigid PU Catalyst Market frequently center on its role in accelerating formulation development, optimizing production processes, and predicting material performance under varied environmental conditions. Key themes emerging from these questions include the integration of machine learning (ML) for structure-property relationship analysis of novel catalyst compounds, the utilization of digital twin technology to simulate complex foaming kinetics, and the potential for AI-driven quality control to minimize batch-to-batch variability in polyurethane synthesis. Users express high expectations that AI will significantly reduce the timeline and cost associated with discovering new, environmentally friendly, and highly efficient catalyst combinations, ultimately leading to superior insulation products that meet future regulatory standards more quickly and effectively. There is also substantial interest in how predictive modeling can optimize catalyst loading and reaction parameters in real-time manufacturing environments, thus improving resource utilization and reducing waste.

AI is poised to revolutionize catalyst development by allowing researchers to screen millions of potential chemical structures virtually, far exceeding the speed of traditional laboratory synthesis and testing. Machine Learning algorithms can analyze vast datasets concerning reaction thermodynamics, kinetics, and resulting foam morphology, identifying non-obvious correlations between catalyst molecular structure and final foam properties like compressive strength, thermal conductivity, and aging performance. This predictive capability is critical for optimizing systems compatible with complex modern blowing agents and achieving specific, nuanced foam characteristics required for specialized applications, such as ultra-low lambda (thermal conductivity) rigid insulation panels. The deployment of AI tools shifts the focus from empirical trial-and-error to data-driven rational design, speeding up the commercialization pathway for next-generation catalyst systems.

Furthermore, the integration of AI and data analytics into the manufacturing process (Industry 4.0) enhances operational efficiency for PU foam producers. AI systems monitor real-time sensor data from mixers, metering units, and reaction chambers, allowing for instant adjustments to catalyst flow rates, component temperatures, and pressure levels to ensure consistent foam quality regardless of minor variations in raw material purity or environmental humidity. This predictive maintenance and quality assurance capability not only reduces scrap rates and energy consumption but also ensures compliance with stringent product specifications required in regulated sectors like aerospace and medical cold storage. The ability to model the long-term aging behavior of foam using AI simulations also provides manufacturers with a competitive advantage by offering reliable performance guarantees over the product lifecycle.

The Rigid PU Catalyst Market is fundamentally shaped by a dynamic interplay of Drivers, Restraints, and Opportunities, which collectively constitute the Impact Forces influencing market growth and strategic direction. A major driver is the global imperative for energy efficiency, stemming from governmental regulations and consumer demand for low-energy buildings and appliances, which mandates the use of highly efficient insulation materials like rigid PU foam. This sustained demand is countered by significant restraints, primarily the volatile pricing and supply chain complexities associated with key raw materials (isocyanates and specialty amines), alongside increasing regulatory scrutiny regarding VOC emissions and potential toxicity of traditional catalyst types. Opportunities lie in the technological advancement toward non-fugitive, reactive catalysts and the expanding penetration into niche applications such as insulation for liquefied natural gas (LNG) transport and advanced composite materials, positioning the market for sustained innovation and value creation despite existing headwinds.

Drivers are primarily regulatory and application-driven. The adoption of stricter building codes, particularly in Europe and North America (e.g., Passive House standards and updated energy directives), compels the construction industry to utilize superior thermal barriers, increasing the demand for Rigid PU and PIR foams. Furthermore, the rapid expansion of the global cold chain logistics network, essential for food safety and vaccine distribution, relies heavily on high-performance rigid insulation, ensuring steady catalyst consumption. This is complemented by continuous innovation in product performance, suchas the development of ultra-low thermal conductivity foams, which requires specialized catalyst packages to achieve the desired tight, closed-cell structures necessary for maximal thermal resistance. These drivers provide a stable, long-term foundation for market expansion across industrialized and developing economies alike.

Restraints largely revolve around raw material cost fluctuations and environmental compliance. The petrochemical nature of many catalyst precursors makes the market sensitive to crude oil price volatility, impacting production costs and profitability margins for catalyst manufacturers. Moreover, regulatory bodies are increasingly limiting the use of certain tertiary amine catalysts due to their contribution to foam VOC emissions and potential impact on indoor air quality, compelling producers to invest heavily in developing cleaner, lower-emission alternatives. This need for replacement catalysts represents a significant R&D cost barrier. Opportunities arise from this regulatory pressure, specifically the shift toward reactive amine catalysts and tin-free organometallics, which chemically react into the foam matrix, eliminating fugitivity. The emerging market for vacuum insulated panels (VIPs) using PU foam cores and the application of rigid PU in structural insulated panels (SIPs) further present high-value market entry points for advanced catalyst suppliers.

The Rigid PU Catalyst Market is segmented primarily based on catalyst type, which dictates chemical mechanism and performance profile; by application, reflecting the end-use industry; and by region, indicating geographical consumption patterns and regulatory influences. Analyzing these segments provides a clear map of market dynamics and identifies high-growth niches. The segmentation by catalyst type—encompassing tertiary amines (aliphatic and heterocyclic), organometallic compounds (tin, bismuth, potassium salts), and other specialties—is critical, as different foam formulations and blowing agents necessitate tailored catalytic packages to achieve optimal reaction control and physical properties. This detailed categorization assists manufacturers in aligning their product development strategies with specific industry requirements, such as low-VOC emission standards or enhanced fire performance.

The application segmentation is dominated by the construction and appliance sectors. Construction utilizes rigid PU for insulation purposes in walls, roofs, and flooring (e.g., insulation boards and spray foams), driven by energy efficiency standards. The appliance sector relies on rigid PU for thermal insulation in domestic and commercial refrigeration units, where the efficiency of the foam directly translates into appliance energy ratings. Growth in the specialized segments, such such as pipe insulation, automotive components (lightweighting initiatives), and refrigerated transport (cold chain), often requires high-performance catalysts capable of rapid cure times and extreme thermal stability, offering higher margins and emphasizing the importance of differentiated product offerings within the broader market structure.

Geographically, the market segmentation highlights pronounced differences in maturity and growth trajectory. APAC leads in growth due to massive new construction activity and increasing appliance manufacturing output. Conversely, North America and Europe emphasize catalyst technology that supports sustainable practices, focusing on HFO compatibility and non-fugitive characteristics to meet stringent environmental regulations. Understanding these regional nuances—including varying building codes, accepted blowing agents, and regulatory frameworks (like REACH in Europe or specific US state regulations)—is fundamental for global market players to tailor their distribution channels, product formulations, and compliance strategies effectively, ensuring market access and competitive success across diverse operating environments.

The value chain of the Rigid PU Catalyst Market begins with the upstream procurement of specialty petrochemical intermediates, such as various alcohols, amines, and metals, which are essential precursors for manufacturing both tertiary amine and organometallic catalysts. Upstream analysis involves assessing the supply stability and pricing volatility of raw materials, which are often subject to the global crude oil market and geopolitical influences. Key upstream challenges include maintaining purity and securing reliable supply sources for niche chemical building blocks required for complex, high-performance reactive catalysts. Efficiency at this stage directly impacts the final production cost and margin structure of catalyst manufacturers, necessitating strong supplier relationship management and robust inventory strategies to mitigate supply chain disruptions and unexpected price spikes in commodity chemicals.

The midstream segment involves the core manufacturing, formulation, and quality control processes undertaken by major chemical companies specializing in PU additives. Catalyst manufacturers formulate customized blends designed to optimize reaction profiles for specific end-use applications (e.g., faster demold times in appliance production or enhanced flowability for spray foam applications). These companies invest heavily in R&D to develop non-fugitive, low-VOC catalysts compatible with new blowing agents, adding significant value through intellectual property and specialized technical support. The differentiation in the midstream is achieved not just through the chemical product itself, but also through comprehensive application expertise and technical service provided to PU system house customers, helping them navigate complex foam formulation challenges and meet regulatory compliance.

The downstream segment focuses on distribution and final consumption. Catalysts are typically sold directly or indirectly through specialized distributors to PU system houses, which blend the polyols, isocyanates, and additives into ready-to-use systems. These systems are then supplied to ultimate end-users, such as construction companies, appliance manufacturers, and industrial pipe insulators. Distribution channels are highly specialized; direct sales often target large multinational system houses needing custom formulations, while indirect channels (local chemical distributors) serve smaller, regional foam producers. The effectiveness of the downstream channel relies on fast logistics and specialized chemical handling capabilities to ensure safe and timely delivery to the diverse geographical locations where rigid PU foam production takes place.

The primary potential customers for Rigid PU Catalysts are enterprises engaged in the production of polyurethane systems and final foam products, which predominantly fall within the construction, appliance, and transportation sectors. These customers, categorized mainly as Polyurethane System Houses, Foam Manufacturers, and Original Equipment Manufacturers (OEMs), require catalysts as essential ingredients to control the exothermic polymerization reaction and ensure the final product meets stringent performance specifications, such as R-value (thermal resistance), compressive strength, and dimensional stability. System houses are particularly crucial customers, as they purchase catalysts in large volumes, formulate proprietary blends of polyols, additives, and catalysts, and then market these complete systems to foam applicators, thus acting as the central purchasing hub in the value chain.

Within the construction industry, potential buyers include large-scale insulation board manufacturers, who produce materials used for continuous insulation in commercial and residential buildings, and spray foam contractors/suppliers, who require fast-curing, robust catalyst systems that perform reliably in varying on-site conditions. These customers are highly sensitive to catalyst performance metrics, particularly the initiation time, gel time, and cure speed, as these factors directly impact production throughput and installation efficiency. Furthermore, manufacturers focusing on specialized products like Structural Insulated Panels (SIPs) and advanced panelized construction materials represent high-value customers seeking catalyst solutions that enhance the structural integrity and long-term durability of the foam core, ensuring compliance with high-load bearing architectural requirements.

In the non-construction segment, major OEMs in the appliance industry (refrigerator, freezer, water heater manufacturers) are significant consumers, driven by the global competition to achieve the highest possible energy efficiency ratings (e.g., Energy Star). These OEMs demand catalysts that enable ultra-fine cell structures and minimal thermal bridging. Additionally, companies involved in cold chain logistics, including manufacturers of insulated shipping containers and refrigerated truck bodies (reefers), are rapidly growing customer segments. Their requirements focus on catalysts that provide exceptional foam uniformity and minimal thermal aging, critical for maintaining temperature control and minimizing spoilage of sensitive goods like pharmaceuticals and perishables across long transit routes.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1.55 Billion |

| Market Forecast in 2033 | USD 2.45 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Evonik Industries AG, Merck KGaA, Huntsman Corporation, Air Products and Chemicals Inc., TEDA Applied Catalysts Co. Ltd., Tosoh Corporation, Covestro AG, Lanxess AG, King Industries Inc., Momentive Performance Materials Inc., R.T. Vanderbilt Holding Company Inc., Kao Corporation, Dow Inc., BASF SE, Wanhua Chemical Group Co. Ltd., Gulbrandsen Technologies Inc., PCI Synthesis, Shepherd Chemical Company, Johnson Matthey, Gelest Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Rigid PU Catalyst Market is defined by a relentless drive towards achieving sustainable formulations and superior reaction control necessary for modern, high-performance foam systems. A major technological focus is the development of non-fugitive (reactive) amine catalysts. Traditional tertiary amines can contribute to VOC emissions and potentially migrate out of the foam structure over time, leading to odor and reduced performance. Reactive amine catalysts are chemically designed with hydroxyl groups or other reactive functional groups that allow them to co-react with the isocyanate, permanently embedding the catalyst into the polymer matrix. This technology eliminates emissions, improves foam aging characteristics, and ensures long-term thermal performance, positioning it as the technological standard for stringent environmental regulations, particularly in indoor air quality sensitive applications.

Another critical technological area involves optimizing catalyst systems for compatibility with new, environmentally preferred blowing agents, specifically Hydrofluoroolefins (HFOs). HFOs offer extremely low Global Warming Potential (GWP) compared to phased-out hydrofluorocarbons (HFCs), but their chemical properties often require a change in catalyst kinetics to maintain efficient processing and high-quality foam structure. Catalyst manufacturers are developing synergistic blends of tertiary amines and organometallic compounds (often tin-free alternatives like bismuth or potassium carboxylates) that precisely tune the gelling-to-blowing ratio under HFO conditions. This requires sophisticated formulation expertise to manage the reduced solubility and distinct vapor pressures of the new blowing agents while ensuring rapid curing and a high percentage of closed-cells for optimal insulation value.

Furthermore, there is increasing adoption of metal-free or low-metal catalyst technologies to address growing concerns regarding heavy metal toxicity (e.g., tin) and to facilitate foam recycling at the end of the product lifecycle. Potassium salts and proprietary amine derivatives are emerging as high-performance alternatives, especially for polyisocyanurate (PIR) foam systems which demand catalysts capable of promoting the trimerization of isocyanate groups, crucial for enhanced fire resistance and thermal stability. Technological innovation is also being applied through digitalization; computational chemistry and high-throughput experimentation (HTE) are increasingly used to rapidly screen novel catalyst candidates, leading to shorter development cycles and more predictable, targeted performance enhancements, ultimately driving the shift towards high-value, specialized catalyst packages tailored for specific foam densities and application methods.

Regional dynamics play a crucial role in shaping the Rigid PU Catalyst Market, influenced significantly by local regulatory frameworks, construction activity levels, and industrial manufacturing capacity, particularly for appliances and cold storage. The Asia Pacific (APAC) region stands out as the global growth engine, fueled by extensive infrastructure development, rapid urbanization, and massive government investment in energy-efficient housing and commercial projects, notably in China, India, and Southeast Asian nations. APAC’s dominance is also driven by its status as a major manufacturing hub for white goods and consumer electronics, requiring vast quantities of rigid foam insulation, translating directly into high demand for PU catalysts. This region generally prioritizes high throughput and cost-effectiveness, although environmental pressures are rapidly increasing the demand for cleaner catalyst solutions.

North America and Europe represent mature markets characterized by stringent environmental regulations and a focus on high-performance, sustainable building practices. In Europe, directives emphasizing near-zero energy buildings and the comprehensive implementation of REACH legislation drive the demand for sophisticated, reactive, and low-VOC catalysts that comply with strict health and safety standards. Retrofitting old buildings for improved energy efficiency is a significant market activity in both regions, necessitating specialized spray foam catalysts. North America, influenced by state-level regulations and federal standards like the SNAP program (Significant New Alternatives Policy) regarding blowing agents, shows robust demand for catalysts optimized for HFO-based systems, ensuring compliance and maximizing thermal performance in high-quality insulation materials.

Latin America (LATAM) and the Middle East & Africa (MEA) are emerging markets exhibiting accelerated growth. LATAM’s demand is spurred by expanding industrialization and commercial refrigeration requirements, particularly in Brazil and Mexico. The MEA region, particularly the Gulf Cooperation Council (GCC) countries, showcases significant construction booms related to mega-projects and the need for insulation that performs reliably under extreme desert temperatures. This unique requirement drives demand for catalysts that enable foams with exceptional thermal stability and durability. While these regions may lag in immediate adoption of the most complex, high-cost sustainable catalysts, their trajectory strongly indicates increasing future investment in advanced PU chemistry to meet rising standards of living and necessary climate control requirements.

The primary types are tertiary amine catalysts and organometallic compounds. Tertiary amines (e.g., DABCO derivatives) primarily catalyze the blowing (isocyanate-water) and gelling (isocyanate-polyol) reactions simultaneously, dictating cure speed and foam structure. Organometallics (often tin or bismuth salts) usually selectively promote the gelling reaction. For rigid foams, blends are used to achieve the precise balance needed for optimal cross-linking, thermal performance, and rapid demold times, crucial for high-volume production in construction and appliances. Modern catalyst research is focused on reactive amines that chemically bond into the polymer matrix.

Environmental regulations, particularly the phase-down of high Global Warming Potential (GWP) blowing agents like HFCs in favor of ultra-low GWP Hydrofluoroolefins (HFOs), profoundly impact catalyst demand. HFOs have different chemical compatibility and processing characteristics than traditional agents. This necessitates the reformulation of catalyst systems to ensure efficient mixing, optimal solubility, and balanced reaction kinetics. Manufacturers require highly specialized catalyst packages that maintain superior foam insulation properties (low lambda value) and production efficiency under the new HFO systems, driving innovation towards specific synergistic catalyst blends.

Non-fugitive (reactive) catalysts are essential for meeting stringent indoor air quality standards and achieving long-term foam performance reliability. Traditional catalysts can slowly migrate out of the foam (fugitivity), contributing to VOC emissions, odor, and potentially causing dimensional instability or corrosion in appliance applications. Reactive catalysts possess functional groups that co-react with isocyanates, permanently embedding themselves within the PU polymer structure. This technology eliminates emissions, ensures compliance with environmental regulations like the US EPA's requirements, and safeguards the foam's thermal integrity over its service life.

The Construction industry segment, encompassing applications such as insulation boards, spray foam insulation, and structural insulated panels (SIPs), currently drives the highest volume demand for rigid PU catalysts. This robust demand is fundamentally linked to global energy efficiency mandates and continuous construction activities, especially in the rapidly urbanizing Asia Pacific region and retrofitting initiatives in mature European and North American markets. Rigid PU foam is critical for achieving high R-values and thermal envelopes mandated by modern building codes, solidifying construction's leading position as the primary consumer segment.

Raw material price volatility significantly affects profitability, as many catalyst precursors (specialty amines, alcohols, and metals) are petrochemical derivatives highly sensitive to crude oil fluctuations and global supply chain stability. Manufacturers must employ sophisticated risk management strategies, including long-term supply contracts and hedged purchasing, to stabilize costs. Moreover, sustained high raw material costs often compel catalyst producers to focus R&D efforts on developing high-value, low-loading catalysts or more efficient, cost-optimized blends that reduce the total required weight of the active ingredient while maintaining high performance, thereby mitigating margin compression.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.