ID : MRU_ 434306 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

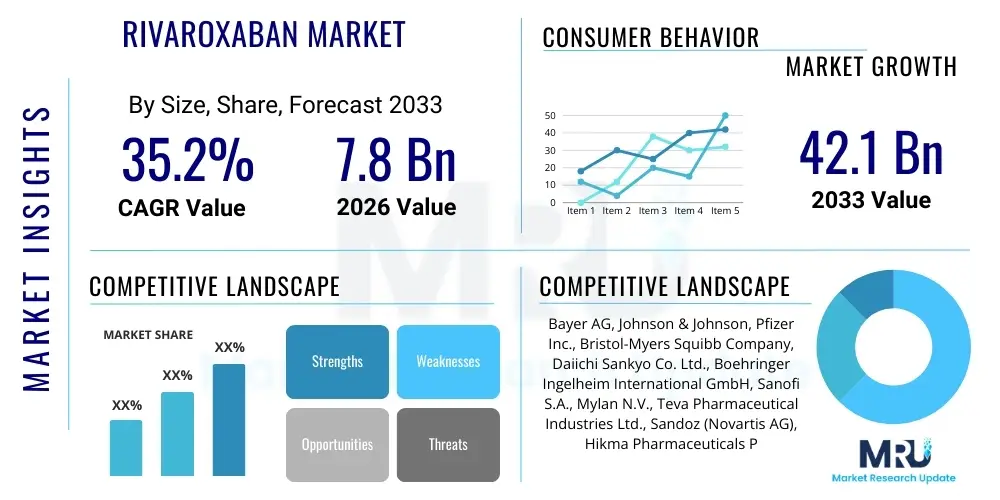

The Rivaroxaban Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 35.2% between 2026 and 2033. The market is estimated at USD 7.8 Billion in 2026 and is projected to reach USD 42.1 Billion by the end of the forecast period in 2033.

Rivaroxaban is a highly effective, orally administered direct factor Xa inhibitor, widely utilized for the prevention and treatment of various thromboembolic disorders. As a key pharmaceutical agent in the Non-Vitamin K Antagonist Oral Anticoagulant (NOAC) class, Rivaroxaban offers significant advantages over traditional anticoagulants, such as warfarin, including predictable pharmacokinetics, fewer drug-drug interactions, and the absence of routine coagulation monitoring. This superior profile has driven its rapid adoption across global healthcare systems, positioning it as a foundational therapy in cardiovascular and orthopedic care. The market is characterized by intense pharmaceutical competition, focusing primarily on expanding indications, improving patient compliance, and managing the evolving patent landscape, particularly concerning generic entry in key geographic regions.

The primary applications of Rivaroxaban span critical medical fields, including the prevention of stroke and systemic embolism in patients with non-valvular atrial fibrillation (NVAF), the treatment of deep vein thrombosis (DVT) and pulmonary embolism (PE), and the reduction of recurrent DVT and PE risk. Furthermore, its use extends to thromboprophylaxis following elective hip or knee replacement surgery. The product description emphasizes its fixed dosing regimen and rapid onset of action, which simplifies patient management and contributes directly to improved clinical outcomes. These therapeutic benefits—superior efficacy in preventing major cardiovascular events and a reduced risk of intracranial hemorrhage compared to traditional therapies—solidify its market position despite the competition from other NOACs.

Market growth is significantly driven by demographic trends, specifically the global aging population, which exhibits a higher incidence of atrial fibrillation and venous thromboembolism (VTE). Concurrently, increasing awareness among healthcare professionals regarding the benefits of NOACs over VKAs, coupled with supportive clinical guidelines from major cardiology societies, acts as a primary catalyst. Technological advancements in diagnostic tools that aid in early identification of patients at high risk of thrombosis further accelerate demand. However, the market structure remains sensitive to pricing pressures, particularly as health systems globally seek cost-effective treatments, necessitating continuous innovation in drug delivery and formulation to maintain competitive advantage.

The Rivaroxaban market currently operates under the influence of complex business trends characterized by patent expiration dynamics and strategic maneuvering by major pharmaceutical corporations. Original innovators are strategically extending market exclusivity through new formulations, combination therapies, and expanding indication approvals, while generic manufacturers are aggressively preparing for launches following primary patent lapses in key developed markets. This interplay results in dual market dynamics: robust revenue generation driven by high-volume prescriptions in regulated markets, juxtaposed with anticipated pricing erosion upon generic market entry. Furthermore, strategic alliances focused on distribution in emerging economies and investments in real-world evidence studies to validate long-term safety and efficacy are defining competitive business strategies, ensuring sustained market relevance despite looming competitive threats.

Regional trends indicate a continued dominance of North America and Europe in terms of revenue, primarily due to well-established healthcare infrastructure, high diagnosis rates of cardiovascular diseases, and high adoption of premium pharmaceutical therapies. However, the Asia Pacific region is demonstrating the highest growth trajectory, fueled by rapidly improving healthcare access, increasing prevalence of lifestyle-related chronic diseases leading to VTE and NVAF, and growing government initiatives focused on non-communicable disease management. While regulatory hurdles and lower per capita spending constrain immediate market size in some emerging markets, the sheer volume of potential patients positions these areas as crucial long-term growth frontiers. Market players are tailoring commercial strategies to address regional prescribing habits, reimbursement policies, and varying levels of patient compliance across diverse geographies.

Segmentation trends highlight the Oral Tablet segment maintaining the largest market share due to patient convenience and established formulation protocols. Simultaneously, the application segment focused on Atrial Fibrillation (AF) remains the revenue cornerstone, driven by the significant burden of AF-related stroke risk globally. However, the application segment for Deep Vein Thrombosis (DVT) and Pulmonary Embolism (PE) treatment and prophylaxis is exhibiting accelerated growth, largely attributed to increasing hospital recognition of VTE risk and improved diagnostic capabilities. Future segment growth is expected to be influenced by advancements in personalized medicine, allowing for tailored dosing based on individual patient risk factors, potentially driving demand for specialized formulations or combination therapies designed to mitigate bleeding risk while maximizing anticoagulant efficacy.

User queries regarding the impact of Artificial Intelligence (AI) on the Rivaroxaban market frequently center on two main themes: enhancing prescription safety and optimizing drug discovery for next-generation anticoagulants. Users are keenly interested in how AI can move beyond general risk stratification to provide personalized bleeding and thrombosis risk assessments, enabling more precise dosing of Rivaroxaban, which traditionally uses standardized regimens. A significant concern revolves around the potential for AI-driven diagnostic tools to better identify patients who might benefit most from NOACs versus those who require alternative therapies, thereby improving treatment effectiveness while reducing adverse events like major hemorrhage. The anticipation is high that AI could transform adherence monitoring and patient education, making complex anticoagulation management simpler for both providers and patients.

In the near term, AI implementation is revolutionizing pharmacovigilance and real-world evidence generation. Machine learning algorithms are now capable of rapidly analyzing vast datasets—including electronic health records, insurance claims, and spontaneous adverse event reports—to detect subtle signals regarding drug safety, particularly concerning rare complications associated with Rivaroxaban use in heterogeneous patient populations. This robust analytical capacity provides pharmaceutical companies and regulatory bodies with deeper insights into the drug's performance outside of controlled clinical trials, helping refine clinical guidelines and improve overall risk management strategies. The ability of AI to integrate genomic data is also beginning to inform patient selection, offering the possibility of predicting individual patient responses to Rivaroxaban based on genetic predispositions related to metabolism and clotting factors.

Looking ahead, the long-term impact of AI is poised to fundamentally alter the competitive landscape through accelerated research and development. AI-driven platforms are being used to simulate molecular interactions, potentially leading to the discovery of novel anticoagulants with highly targeted action profiles that minimize systemic bleeding risk—the primary limitation of current therapies like Rivaroxaban. Furthermore, AI is crucial in optimizing clinical trial design for new indications or pediatric applications of existing NOACs, identifying optimal patient cohorts, and accelerating data analysis, thereby reducing the time and cost associated with bringing innovative treatments to market. The seamless integration of AI into clinical decision support systems is expected to make Rivaroxaban prescribing safer and more efficient, maintaining its market leadership until next-generation treatments emerge.

The Rivaroxaban market is propelled by significant intrinsic and extrinsic drivers that underscore its sustained expansion. A major driver is the global epidemiological shift towards an older population base, which correlates directly with an increased incidence of age-related cardiovascular conditions such as Atrial Fibrillation (AF) and Venous Thromboembolism (VTE). The demonstrated superior efficacy and safety profile of Rivaroxaban, particularly its fixed-dose regimen without the need for routine monitoring, further acts as a powerful adoption catalyst among both prescribers and patients, minimizing healthcare resource utilization compared to Vitamin K Antagonists (VKAs). Furthermore, widespread clinical guideline endorsements from influential medical bodies strongly advocate for the use of NOACs like Rivaroxaban as the first-line treatment for several thromboembolic conditions, cementing its position in standard clinical practice protocols.

However, the market faces significant restraints that temper its growth trajectory. The primary restraint is the high cost associated with proprietary NOACs, including Rivaroxaban, which imposes substantial burden on healthcare systems, particularly in cost-sensitive markets where reimbursement challenges persist. A major safety concern, despite its relative improvement over warfarin, remains the risk of major bleeding events; although reversal agents exist, the necessity for rapid response protocols and the associated healthcare costs pose a barrier. Crucially, the looming threat of patent expiration in major markets like the U.S. and Europe, enabling the introduction of lower-cost generic versions, represents a near-term restraint on the revenue growth of the originator brand, fundamentally shifting competitive focus from efficacy to cost containment.

Opportunities for growth are concentrated in expanding the therapeutic indications of Rivaroxaban and enhancing its geographical reach. There is substantial potential in pediatric VTE treatment, anti-platelet combination therapies for acute coronary syndrome (ACS), and specialized applications in patients with cancer-associated thrombosis, where Rivaroxaban demonstrates favorable data. Geographically, untapped markets in Asia Pacific and Latin America present significant expansion avenues, provided that local regulatory hurdles are navigated successfully and affordable access strategies are implemented. The impact forces acting on the market structure—comprising competitive intensity from other NOACs (such as Apixaban and Dabigatran), regulatory stringency regarding safety and manufacturing standards, and the increasing influence of health technology assessment (HTA) bodies on formulary placement—dictate that market players must balance premium pricing with demonstrating superior long-term, real-world cost-effectiveness data.

The Rivaroxaban market segmentation provides a granular view of demand distribution based on formulation type, application area, and distribution channels, enabling targeted commercial strategies. The market is primarily segmented by Formulation into Tablet and Oral Suspension, reflecting the standard delivery methods designed for varying patient populations, including those unable to swallow solid dosage forms. Application segmentation, which defines the therapeutic areas, is crucial for market sizing, with segments like Atrial Fibrillation, Deep Vein Thrombosis (DVT), Pulmonary Embolism (PE), and orthopedic prophylaxis dominating utilization. This application-based analysis reveals where the highest clinical need and reimbursement coverage converge, providing strategic direction for marketing and R&D investment. Furthermore, understanding the nuances of segmentation allows companies to anticipate shifts in prescribing patterns influenced by evolving clinical guidelines and competitor product launches within specific indications.

Analyzing the segmentation by Distribution Channel reveals the critical pathways through which Rivaroxaban reaches the end-user. Hospital Pharmacies maintain a vital role, especially for initial VTE treatment and post-surgical prophylaxis, where immediate access and administration are necessary. Conversely, Retail Pharmacies and Online Pharmacies drive long-term maintenance therapy, particularly for conditions like Atrial Fibrillation requiring chronic management. The increasing influence of specialty pharmacies, which offer enhanced adherence programs and patient support services for high-cost or complex medications, is reshaping the distribution landscape, ensuring better patient outcomes and minimizing dispensing errors. This multichannel approach is essential for achieving broad market penetration and maximizing patient compliance across different points of care.

Segment dynamics are continuously influenced by clinical trial outcomes and regulatory endorsements. For instance, the expansion of Rivaroxaban's use into secondary prevention of cardiovascular events in patients with coronary artery disease (CAD) and peripheral artery disease (PAD) has created a significant new sub-segment within the application category, driving growth independent of the core AF market. Geographically, segmentation is critical for pricing strategy, as developed nations with strong reimbursement mechanisms support premium tablet formulations, while emerging markets often require lower-cost or subsidized access programs to drive volume adoption. The overall market resilience is therefore tied to the successful management and expansion of these diverse segments, leveraging global clinical data to demonstrate value across all therapeutic areas.

The value chain for Rivaroxaban begins with complex upstream activities centered on the rigorous procurement and synthesis of highly specific active pharmaceutical ingredients (APIs) and excipients. This stage involves stringent quality control protocols, specialized chemical synthesis processes, and managing a geographically diverse supply chain to ensure purity and consistency of the factor Xa inhibitor molecule. Key upstream challenges include maintaining compliance with global Good Manufacturing Practices (GMP) and managing the intellectual property surrounding the proprietary synthetic routes. Successful upstream management is crucial for cost optimization and mitigating supply disruptions, particularly given the specialized nature of the API manufacturing, often controlled by a limited number of high-quality contract manufacturing organizations (CMOs) operating under license or strategic partnerships with the originator company.

Midstream activities encompass the formulation, tablet manufacturing, and primary and secondary packaging of the finished drug product. This phase requires sophisticated equipment for blending, compression, and coating, ensuring precise dose uniformity and stability. Quality assurance and regulatory approval processes are integrated at every step to guarantee the final product meets the specifications required by global health authorities such as the FDA and EMA. The efficiency of the midstream process directly impacts production capacity and cost per unit, which are pivotal competitive factors ahead of anticipated generic competition. Innovation in this stage focuses on developing advanced formulations, such as the oral suspension, to broaden the therapeutic reach to patient groups with specific swallowing difficulties.

Downstream activities involve the complex distribution channel network, encompassing both direct and indirect sales strategies. Direct sales are often utilized for high-volume hospital contracts and institutional purchases, requiring specialized pharmaceutical sales forces to engage key opinion leaders and hospital formularies. Indirect distribution relies heavily on established networks of pharmaceutical wholesalers, major retail pharmacy chains, and specialized pharmacy networks, ensuring widespread availability across geographical regions. The distribution channel must manage cold chain logistics (though Rivaroxaban typically does not require it, general supply chain efficiency is key), inventory management, and strict compliance monitoring to prevent counterfeiting and parallel trade. The selection of distribution partners and the negotiation of favorable reimbursement status are critical determinants of final market access and commercial success.

The primary end-users and buyers of Rivaroxaban are diverse, encompassing both institutional healthcare providers and individual patients requiring long-term anticoagulation therapy. Institutional buyers include major hospitals, specialized cardiology and orthopedic clinics, emergency departments, and governmental health procurement agencies. These institutions are concerned with evidence-based medicine, cost-effectiveness analyses, formulary inclusion, and the availability of safety protocols (including reversal agents). Their purchasing decisions are heavily influenced by clinical trial data demonstrating superior outcomes in specific patient populations, making comprehensive real-world evidence and pharmacoeconomic studies essential marketing tools targeting procurement committees and clinical guideline developers.

Individual end-users primarily comprise patients diagnosed with non-valvular atrial fibrillation (NVAF), individuals undergoing major orthopedic surgery (hip or knee replacement), and those suffering from or at risk of recurrent deep vein thrombosis (DVT) or pulmonary embolism (PE). Patient choice, while guided by physician recommendation, is heavily influenced by factors such as convenience (fixed dosing), perception of safety, reduced need for blood monitoring, and out-of-pocket cost. The shift towards consumer-centric healthcare means that patient support programs, education materials, and adherence tools become important factors in maintaining high compliance rates, particularly for a chronic medication where non-adherence can lead to catastrophic events like stroke or fatal embolism.

A burgeoning potential customer segment includes long-term care facilities and home healthcare providers, who manage a rapidly growing population of elderly and chronically ill patients often requiring VTE prophylaxis or stroke prevention. These facilities prioritize ease of administration, minimum interaction risk with other medications, and predictable therapeutic effects to minimize the need for acute interventions. Furthermore, the expansion of indications into preventative care for patients with high-risk cardiovascular conditions (CAD/PAD) broadens the customer base significantly, targeting a population that previously utilized less efficacious or higher-risk antiplatelet monotherapies. Tapping into these varied customer segments requires tailored messaging and robust support for healthcare practitioners across all levels of care.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 7.8 Billion |

| Market Forecast in 2033 | USD 42.1 Billion |

| Growth Rate | 35.2% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Bayer AG, Johnson & Johnson, Pfizer Inc., Bristol-Myers Squibb Company, Daiichi Sankyo Co. Ltd., Boehringer Ingelheim International GmbH, Sanofi S.A., Mylan N.V., Teva Pharmaceutical Industries Ltd., Sandoz (Novartis AG), Hikma Pharmaceuticals PLC, Cipla Ltd., Dr. Reddy's Laboratories Ltd., Sun Pharmaceutical Industries Ltd., Aurobindo Pharma, Hetero Labs Limited, Zydus Cadila, Alkem Laboratories Ltd., Torrent Pharmaceuticals Ltd., Lupin Limited. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape surrounding the Rivaroxaban market is characterized by advancements focused on formulation stability, enhanced bioavailability, and the integration of digital health solutions to optimize patient management. In manufacturing, continuous processing technologies, replacing traditional batch manufacturing, are increasingly adopted to improve production efficiency, reduce costs, and ensure highly consistent drug product quality, which is crucial for a blockbuster medication requiring massive scale production. Furthermore, sophisticated analytical techniques, including high-performance liquid chromatography (HPLC) and mass spectrometry, are utilized in quality control to monitor impurity levels and ensure the precise structural integrity of the complex API molecule, meeting the stringent regulatory requirements across developed nations. These manufacturing technologies provide a key competitive advantage, particularly in preparation for generic erosion, where scale and cost efficiency are paramount.

Beyond core manufacturing, drug delivery technology plays a vital role in enhancing patient compliance and therapeutic efficacy. The development of the oral suspension formulation, achieved through specialized particle engineering and taste-masking technologies, ensures that patients, particularly pediatric and geriatric individuals who struggle with swallowing tablets (dysphagia), can still receive accurate dosing. This formulation innovation broadens the addressable market and aligns with the growing focus on patient-centric care. Current research also explores advanced pharmaceutical technologies such as nanocrystal formulations or amorphous solid dispersions (ASDs) to potentially further enhance the bioavailability and dissolution rate of Rivaroxaban, though the existing tablet formulation already exhibits high efficacy.

The most transformative technological shift lies in integrating Rivaroxaban therapy with digital health tools. This includes the proliferation of smart blister packs, medication adherence apps, and electronic health record (EHR) integration platforms that enable real-time monitoring of patient compliance and potential drug-drug interactions. Telemedicine platforms are increasingly leveraged to facilitate remote patient consultations and monitoring for individuals on chronic anticoagulation therapy, reducing the burden of frequent clinic visits. Looking forward, the application of predictive diagnostics using biomarker technology is expected to become standard, allowing physicians to precisely identify patients at the greatest risk of bleeding complications from Rivaroxaban, thereby tailoring dosing or therapeutic selection based on individual physiological response profiles and genetic markers, marking a significant step toward personalized anticoagulation management.

The global Rivaroxaban market exhibits distinct dynamics across major geographical regions, influenced by healthcare spending, disease prevalence, regulatory maturity, and patent status. North America, encompassing the United States and Canada, remains the largest revenue contributor, characterized by high per capita healthcare expenditures, widespread adoption of innovative therapies, and comprehensive insurance coverage for NOACs. The market here is driven by high incidence rates of Atrial Fibrillation and robust infrastructure for orthopedic surgeries, ensuring consistent demand for prophylactic use. The forthcoming patent cliffs, however, represent a critical shift, prompting strategic efforts by the originator company to maximize revenue through new indications and combination therapies before the market is flooded by generics, thus defining the immediate competitive environment.

Europe, including key markets such as Germany, France, and the United Kingdom, represents the second major market, distinguished by complex national reimbursement systems and stringent health technology assessment (HTA) processes. European growth is sustained by strong clinical acceptance and clear clinical guidelines favoring NOACs. However, market access and pricing negotiations are highly decentralized and often result in significant price differences across member states. The focus in Europe is heavily skewed towards real-world data collection to justify the cost-effectiveness of Rivaroxaban compared to generics and established VKAs, maintaining its formulary position in systems highly sensitive to pharmaceutical expenditure. Regulatory harmonization through the European Medicines Agency (EMA) facilitates swift uptake once approval is secured, but national procurement policies dictate commercial success.

The Asia Pacific (APAC) region is projected to register the fastest growth rate throughout the forecast period. This acceleration is attributed to rapidly expanding healthcare infrastructure, increasing disposable incomes, and the massive, underserved patient population suffering from cardiovascular diseases, particularly in China and India. Government investments in healthcare modernization and rising public awareness of stroke prevention are catalyzing NOAC adoption. While pricing remains a major barrier in this region, pharmaceutical companies are employing volume-based strategies, localized clinical trials, and strategic partnerships with regional distributors to navigate diverse regulatory landscapes and drive penetration, ensuring long-term growth potential far surpassing that of mature Western markets.

The primary factor driving market growth is the global demographic shift towards an aging population, which significantly increases the prevalence of conditions requiring chronic anticoagulation therapy, such as Atrial Fibrillation (AF) and Venous Thromboembolism (VTE). Additionally, the superior clinical profile and convenience of Rivaroxaban compared to older anticoagulants (like warfarin) fuel physician and patient preference.

Patent expiration, expected in key regions in the mid-to-late forecast period, is anticipated to cause significant market share erosion for the branded product due to the entry of low-cost generic versions. This competition will lead to substantial price depression, necessitating the brand owner to focus on volume maintenance, new combination therapies, and geographical expansion outside patent-lapsed regions to sustain revenue.

The Asia Pacific (APAC) region, particularly emerging economies like China and India, offers the highest growth potential. This is attributed to rapidly improving healthcare access, increasing diagnosis rates of cardiovascular diseases, and a vast, largely untreated patient population, driving significant volume adoption despite initial pricing sensitivity.

The key restraints include the high proprietary cost of Rivaroxaban compared to generic traditional anticoagulants, leading to challenges in securing favorable reimbursement in cost-conscious healthcare systems. Furthermore, despite its improved safety profile, the risk of major bleeding and the necessity for a specific reversal agent in emergency situations continue to pose clinical and economic challenges.

AI is influencing Rivaroxaban usage by enabling highly personalized risk assessment models that predict individual patient susceptibility to both thrombosis and bleeding, thereby optimizing precise dosing strategies. AI also streamlines pharmacovigilance and adherence monitoring through digital health tools, enhancing overall safety and efficacy management of the medication in real-world settings.

Specialized pharmacies are increasingly vital as they manage complex, high-cost medications requiring extensive patient counseling and adherence programs. For Rivaroxaban, these pharmacies ensure appropriate patient education on dosing schedules, identify potential drug interactions, and provide structured support to maximize compliance for chronic conditions like Atrial Fibrillation, playing a critical role in long-term therapy success.

Emerging therapeutic applications include the chronic, low-dose use in combination with antiplatelet therapy for secondary prevention in patients with stable coronary artery disease (CAD) or peripheral artery disease (PAD). Additionally, its growing utilization for the treatment and prevention of cancer-associated thrombosis (CAT) represents a significant new market segment based on recent compelling clinical data.

The different dose strengths cater to varied clinical indications and renal function requirements. For example, 20mg is typically used for stroke prevention in non-valvular AF; 15mg is used for AF patients with moderate renal impairment; and 10mg is frequently used for initial VTE prophylaxis post-orthopedic surgery or as maintenance therapy for PE/DVT, allowing for highly individualized treatment regimens.

Rivaroxaban maintains a strong competitive position due to its once-daily dosing regimen for many indications, appealing to patients who prioritize convenience. While Apixaban often shows favorable bleeding rates in certain high-risk cohorts and uses a twice-daily regimen, Rivaroxaban excels in applications requiring high efficacy and fixed dosing, such as orthopedic prophylaxis and VTE treatment, differentiating it within the competitive NOAC class.

Manufacturers have focused heavily on developing and ensuring the availability of specific reversal agents, such as Andexanet Alfa, which rapidly reverses the factor Xa inhibition effects of Rivaroxaban in acute bleeding scenarios. Furthermore, efforts are directed toward refining guidelines and developing risk scoring tools to identify patients pre-emptively who are at exceptionally high risk for hemorrhage, allowing for modified dosing or alternative therapies.

DVT treatment is crucial because Rivaroxaban offers the advantage of initiating oral therapy immediately, bypassing the need for initial parenteral bridging therapy (like heparin), simplifying hospital protocols and enabling earlier discharge. This streamlined approach makes it highly attractive to healthcare providers focused on efficient management and cost reduction for acute thromboembolic events.

The synthesis of the Rivaroxaban API involves specialized, multi-step chemical processes requiring stringent adherence to Good Manufacturing Practices (GMP). Value chain management focuses on securing long-term contracts with specialized Contract Manufacturing Organizations (CMOs) that can guarantee high purity, scalability, and intellectual property compliance, essential for maintaining global supply consistency and cost-effectiveness.

Real-world evidence is highly significant as it validates the safety and efficacy observed in controlled clinical trials across a broader, more heterogeneous patient population, often encompassing complex comorbidities. RWE is essential for securing and maintaining favorable reimbursement status, particularly in Europe where HTA bodies rely heavily on post-marketing data to determine long-term value and comparative effectiveness against alternatives.

Advanced tablet manufacturing technologies, particularly continuous manufacturing systems, contribute significantly to quality by ensuring highly consistent blending and compression, leading to precise dose uniformity across massive production volumes. Specialized coating techniques are also employed to enhance stability and control dissolution profiles, guaranteeing optimal drug release in the gastrointestinal tract.

Regulatory stringency requires extensive and well-designed clinical trials, such as the COMPASS trial for cardiovascular risk reduction, to demonstrate clear benefit-risk profiles for new indications. This process is complex and costly, requiring global pharmaceutical companies to invest heavily in large-scale studies and detailed submission dossiers to secure approvals from agencies like the FDA and EMA for expanded use.

Patient adherence is critical because Rivaroxaban is used to prevent life-threatening events like stroke and fatal embolism. Non-adherence directly compromises therapeutic efficacy, leading to poor clinical outcomes, increased healthcare costs from hospitalizations, and negatively impacting the drug's overall perceived effectiveness and market reputation. Hence, adherence support is a core component of commercial strategy.

Educational initiatives are essential for increasing awareness among both prescribers and patients regarding the optimal use of NOACs, emphasizing the advantages over warfarin, appropriate dosing protocols, and recognizing signs of bleeding. These initiatives, often run by manufacturers or medical societies, address lingering hesitancy and promote confident, compliant utilization of Rivaroxaban in clinical practice.

Yes, adoption rates differ; hospitalized settings drive high initial utilization, especially for DVT/PE treatment and post-surgical prophylaxis, benefiting from immediate administration. Outpatient settings, however, drive long-term maintenance therapy for chronic conditions like AF, requiring robust distribution channels and patient support systems to ensure continuous medication supply and adherence over many years.

Generic drug companies exert substantial downward pressure on innovator pricing. Innovator companies often pre-emptively lower prices, offer rebates, or shift focus to patented complementary products (like combination therapies) ahead of generic launch. This competitive threat forces a strategic pivot away from maximizing price per unit towards maximizing total volume and market access before revenue erosion takes hold.

While the pediatric segment is small in volume, it is strategically important. Gaining approval for pediatric VTE treatment broadens the drug’s labeling and demonstrates commitment to comprehensive care across all ages, potentially extending patent life through exclusivity incentives and further solidifying Rivaroxaban’s image as a versatile, gold-standard anticoagulant.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.