ID : MRU_ 433111 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

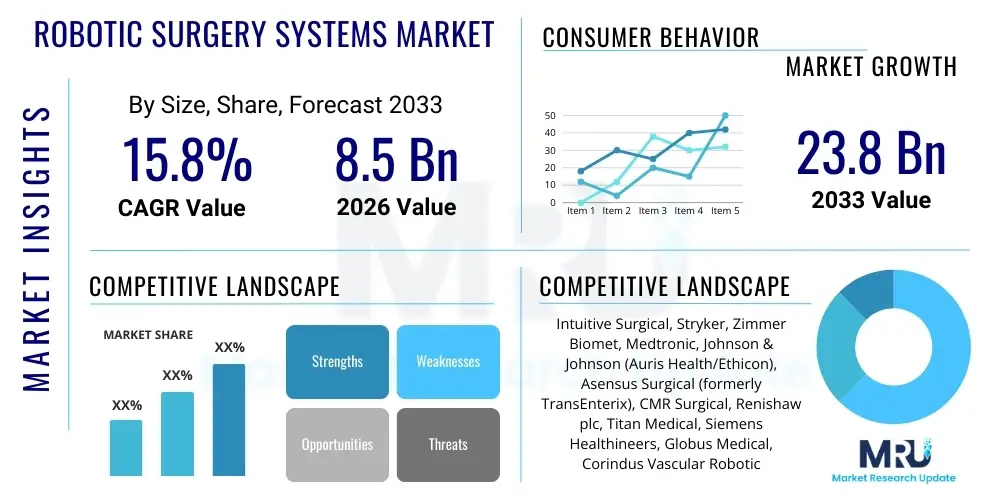

The Robotic Surgery Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2026 and 2033. The market is estimated at USD 8.5 Billion in 2026 and is projected to reach USD 23.8 Billion by the end of the forecast period in 2033.

The Robotic Surgery Systems Market encompasses advanced surgical platforms designed to assist surgeons in performing minimally invasive procedures with enhanced precision, flexibility, and control. These systems typically consist of a surgeon console, a patient-side cart with robotic arms, and a high-definition 3D vision system. Key product offerings include multi-port systems, single-port systems, and dedicated robotic platforms for specific disciplines like orthopedic and neurosurgery. Major applications span across general surgery, urology, gynecology, cardiology, and orthopedics, facilitating complex procedures that reduce patient trauma, decrease hospital stays, and accelerate recovery times. The primary benefits driving market adoption include superior visualization capabilities, tremor filtering, and increased dexterity for surgeons, which collectively improve patient outcomes and procedural efficiency in high-volume surgical centers globally. Furthermore, the persistent demand for minimally invasive techniques coupled with technological advancements in haptics and artificial intelligence integration are the core driving factors propelling market expansion across developed and emerging economies.

The global Robotic Surgery Systems Market is characterized by robust growth, primarily driven by increasing healthcare expenditure in developed nations and the rising geriatric population necessitating complex surgical interventions. Current business trends indicate a strong move toward specialization, with companies developing robotic platforms tailored for specific anatomical sites, moving beyond the traditional general-purpose systems. Furthermore, competitive dynamics are shifting as new entrants challenge the incumbent dominance by offering more cost-effective, modular, and sometimes AI-enhanced alternatives, fostering a competitive pricing environment and accelerating system upgrades in hospitals. Regionally, North America maintains the largest market share due to early adoption, high procedural volume, and established infrastructure, while the Asia Pacific region is poised for the fastest expansion, fueled by increasing medical tourism, improving regulatory frameworks, and government investments aimed at modernizing public health facilities. Segment trends highlight that gynecological and urological applications continue to dominate procedural volumes, but orthopedic and neurosurgical segments are experiencing the most rapid technology adoption rates due to the capability of robotic systems to enhance precision in bone cutting and spinal fixation, promising significant long-term growth.

User inquiries regarding the impact of Artificial intelligence (AI) on robotic surgery frequently center on critical themes such as procedural autonomy, data-driven surgical decision support, and the future role of the human surgeon. Common questions explore how AI-powered computer vision and machine learning algorithms will improve intraoperative guidance, whether AI can accurately predict complications, and the feasibility of achieving fully autonomous tasks, focusing heavily on safety and regulatory hurdles associated with enhanced automation. Another major concern revolves around the massive datasets generated by robotic procedures—users seek to understand how this data is anonymized, analyzed, and leveraged to personalize surgical approaches and train new generations of robotic systems. These themes highlight a strong market expectation that AI will transition robotic systems from sophisticated instruments to intelligent, collaborative surgical partners, thereby standardizing outcomes and expanding the complexity of procedures that can be safely performed minimally invasively.

The integration of AI is fundamentally transforming the capabilities of robotic surgery platforms, moving beyond simple automation to genuine cognitive assistance. AI algorithms are now being utilized to process real-time imaging data, enhancing visualization by automatically identifying critical anatomical structures such as nerves and vascular boundaries that might be obscured during traditional minimally invasive surgery. Furthermore, machine learning models are applied to analyze pre-operative patient data, including imaging and medical history, to create highly detailed patient-specific surgical roadmaps. This level of predictive analytics allows surgeons to anticipate potential challenges before they arise, significantly reducing procedural variability and enhancing the safety profile of complex operations, driving greater confidence in robotic adoption.

Future iterations of robotic surgery systems, heavily influenced by AI, are expected to introduce sophisticated tools for surgical efficiency assessment and automated quality control. AI can analyze the surgeon's movements (instrument path length, force applied, time taken for critical steps) and provide objective, quantitative feedback both during and after the procedure, crucial for training junior surgeons and benchmarking performance across various institutions. This integration of AI not only optimizes the performance of the machine but also serves as a perpetual learning loop, where every surgery contributes to the refinement of algorithms, ultimately paving the way for adaptive robotics that can adjust instrument force or trajectory based on real-time tissue properties, further minimizing error potential and advancing the standard of care.

The Robotic Surgery Systems Market growth is driven primarily by the escalating demand for minimally invasive surgeries, coupled with technological advancements resulting in higher precision and reduced recovery times for patients. Restraints chiefly revolve around the substantial capital investment required for purchasing and maintaining these sophisticated systems, alongside the rigorous training necessary for surgical staff, which often limits adoption in budget-constrained healthcare settings or emerging markets. Opportunities are abundant in the development of specialized, low-cost robotic platforms, the integration of 5G connectivity for telesurgery, and expansion into non-traditional surgical fields like dental and cosmetic procedures. The major impact forces include the increasing global acceptance of robotic technology among patients and providers, stringent regulatory landscapes governing new system approvals, and the intense competitive pressure among key players to reduce costs and introduce differentiated features like haptics feedback and augmented reality overlays.

The Robotic Surgery Systems Market is comprehensively segmented across several dimensions, including component type (systems, accessories, and services), application area (urology, gynecology, general surgery, etc.), and end-user facilities (hospitals, ambulatory surgical centers). The dominant segmentation remains the application segment, largely dictated by the specific clinical requirements and procedural volume associated with various surgical disciplines. Accessories and consumables, such as surgical instruments, trocars, and specialized drapes, constitute a significant and continuously growing revenue stream, driven by the increasing number of procedures performed per installed system globally. Understanding these segment dynamics is crucial for strategic planning, as market players often target high-growth niches, such as neurosurgery or orthopedics, where high precision requirements justify the premium cost of dedicated robotic platforms.

The value chain for the Robotic Surgery Systems Market begins with upstream activities focused on complex research and development (R&D) concerning advanced robotics, precise engineering, and sophisticated software integration, often involving collaborations with academic institutions and specialized technology providers. Midstream activities involve the highly controlled manufacturing and assembly of robotic systems, instruments, and consumables, emphasizing quality control and compliance with stringent medical device regulations (e.g., FDA, CE mark). Downstream activities primarily encompass distribution, installation, comprehensive training programs for surgical teams, and robust post-sale maintenance services. The distribution channel is often a hybrid model; direct sales are common for high-value capital equipment (the systems themselves), ensuring direct customer support and relationship management, while indirect channels utilizing specialized distributors are frequently employed for the recurring sale of accessories and consumables, especially in geographically dispersed or emerging markets.

The primary end-users and potential buyers of robotic surgery systems are large, multi-specialty hospitals and specialized surgical centers that possess the financial capacity to invest in high-cost capital equipment and maintain a high throughput of procedures to ensure a viable return on investment. Academic medical centers and teaching hospitals are also significant customers, driven by the need to offer state-of-the-art training and participate in clinical research utilizing the latest technology. Increasingly, potential customers include large private hospital chains expanding their geographical footprint, aiming to standardize surgical outcomes across all their facilities. Furthermore, the rising trend of performing less complex procedures in Ambulatory Surgical Centers (ASCs) is opening a new customer base, often preferring smaller, more modular, or application-specific robotic systems that align better with lower overhead and streamlined procedural environments.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 23.8 Billion |

| Growth Rate | 15.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Intuitive Surgical, Stryker, Zimmer Biomet, Medtronic, Johnson & Johnson (Auris Health/Ethicon), Asensus Surgical (formerly TransEnterix), CMR Surgical, Renishaw plc, Titan Medical, Siemens Healthineers, Globus Medical, Corindus Vascular Robotics (a Siemens Healthineers Company), Mako Surgical (Stryker subsidiary), Tianjin MicroPort Endoscopic Medical Co., Ltd., NuVasive, Vicarious Surgical, Stereotaxis, Quantum Surgical, Think Surgical. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The core technology landscape of the Robotic Surgery Systems Market revolves around precision engineering, advanced imaging, and seamless software integration. Key technologies include high-resolution 3D vision systems that provide surgeons with depth perception and magnified views, haptic feedback mechanisms that allow the surgeon to physically sense tissue resistance, and sophisticated articulated instruments (endowrist technology) that mimic the full range of motion of the human hand but on a smaller scale. Recent innovations are heavily focused on leveraging Artificial Intelligence (AI) and Machine Learning (ML) for intraoperative image processing and autonomous task execution. Furthermore, the utilization of dedicated platforms for orthopedic surgery involves advanced navigated robotics that assist in highly accurate bone preparation and implant placement, demonstrating a shift toward application-specific technological solutions that enhance procedural outcome predictability and standardization across various surgical disciplines.

North America currently holds the largest share of the global Robotic Surgery Systems Market, driven by high adoption rates in the United States and Canada. This dominance is attributable to several factors, including extensive healthcare infrastructure, substantial hospital budgets allowing for significant capital investment, and the high prevalence of chronic diseases requiring advanced surgical intervention. Furthermore, the region benefits from a high concentration of market leaders and technology innovators who consistently push the boundaries of robotic capabilities, alongside favorable reimbursement policies that support the utilization of advanced robotic procedures. The robust competitive environment also drives continuous innovation, ensuring that healthcare providers have access to the latest generation of multi-port, single-port, and specialized robotic platforms, cementing North America's position as a mature but rapidly evolving market.

Europe represents the second-largest market, characterized by varying adoption rates influenced by the diversity of national healthcare systems and budgetary constraints within the European Union. Western European countries like Germany, France, and the UK are major adopters, propelled by aging populations and state initiatives promoting minimally invasive techniques to reduce overall healthcare burden through faster patient recovery. However, procurement processes in Europe are often slower and more centralized compared to the US, necessitating detailed long-term cost-benefit analyses for widespread adoption. Growth in this region is increasingly focused on orthopedic and general surgery applications, with a noticeable trend toward incorporating local manufacturing and supply chains to improve system accessibility and reduce logistical overheads.

The Asia Pacific (APAC) region is projected to register the fastest growth rate during the forecast period. This rapid expansion is primarily driven by significant government investments in healthcare modernization, particularly in populous nations like China, India, Japan, and South Korea, coupled with a booming medical tourism sector seeking high-quality, state-of-the-art surgical care. Rising economic affluence and increasing patient awareness regarding the benefits of robotic surgery are contributing factors. While the cost of systems remains a barrier in several lower-income nations within APAC, the market is addressing this through the introduction of local, lower-cost robotic platforms and innovative financing models. The critical need to manage high volumes of surgical procedures efficiently makes robotic systems highly attractive to large urban hospitals in this region, particularly for urology and gynecology applications.

Latin America and the Middle East & Africa (MEA) represent nascent but promising markets. Latin America, particularly Brazil and Mexico, shows potential driven by increasing private healthcare spending and the expansion of modern hospital networks, although currency volatility and import duties present significant challenges to technology penetration. In the MEA region, countries like Saudi Arabia and the UAE are rapidly adopting robotic systems as part of their drive to establish world-class healthcare hubs, utilizing substantial oil revenues to fund infrastructure upgrades. The primary driver in MEA is the demand for technological prestige and specialized care, often served initially by high-volume, tertiary care centers. Future growth across both regions hinges critically on the expansion of local surgical training programs and the establishment of reliable service and maintenance networks to support the complex technology.

The high cost of robotic surgery systems stems primarily from intensive Research and Development (R&D) investments, the complex precision engineering required for advanced kinematics and instrumentation, and the continuous recurring expense associated with specialized disposable instruments and annual maintenance contracts necessary for regulatory compliance and optimal performance.

The market is increasingly bifurcating: while multi-port, general-purpose systems remain dominant, there is significant growth in highly specialized, smaller-footprint robots specifically designed for orthopedics (e.g., bone cutting), neurosurgery, or single-port access, offering optimized precision and efficiency for niche procedures, thereby increasing market accessibility.

5G technology is crucial for advancing telesurgery and remote proctoring. Its low latency and high bandwidth capabilities ensure reliable, real-time data transmission between the surgeon console and the patient-side cart, enabling surgeons to operate remotely or guide less experienced surgeons across vast geographical distances safely and effectively.

While urology and gynecology applications currently hold high procedure volumes, general surgery—including colorectal, hernia repair, and bariatric procedures—is projected to show the highest absolute growth in procedural volume, driven by the increasing standardization of minimally invasive techniques for common abdominal surgeries globally.

The most significant restraint remains the high barrier to entry represented by the substantial capital expenditure required (system procurement and installation), which poses a financial burden, particularly on smaller hospitals or healthcare systems in emerging economies, alongside the critical need for comprehensive and certified surgeon training programs.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.