ID : MRU_ 434310 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

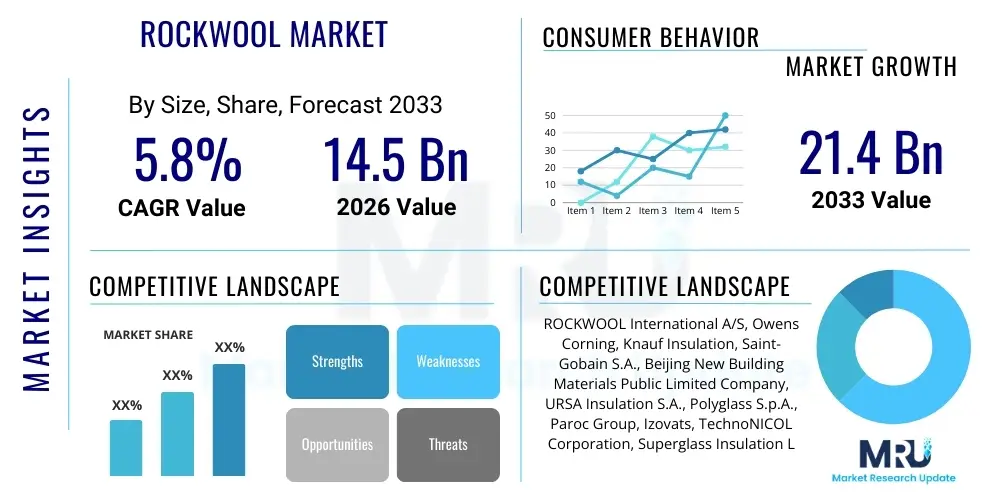

The Rockwool Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2026 and 2033. The market is estimated at USD 14.5 Billion in 2026 and is projected to reach USD 21.4 Billion by the end of the forecast period in 2033.

The Rockwool market, often synonymous with stone wool or mineral wool, encompasses insulation materials derived from natural minerals, predominantly basalt or diabase, melted at extremely high temperatures and spun into fine fibers. This resultant fibrous material is highly valued for its superior thermal, acoustic, and fire protection properties, making it an essential component in modern, energy-efficient construction and industrial applications. Rockwool products are environmentally benign, offering high durability and dimensional stability across a wide temperature range, which positions them favorably against traditional insulation materials like fiberglass or foam polymers. The core product range includes slabs, blankets, pipe sections, and granulated loose fill, customized for specific installation requirements in residential, commercial, and industrial settings. The primary market segments driving demand include building envelope insulation, HVAC systems, industrial process insulation, and increasingly, specialized applications in hydroponic growing media.

The operational mechanism of Rockwool relies on trapping air within its dense, non-combustible fiber structure, which significantly impedes heat transfer and sound transmission. Its inherent resistance to moisture, mold growth, and pests enhances its longevity and performance stability over the building's lifecycle. Major applications span structural insulation for walls, roofs, and floors in new construction projects, retrofitting in existing buildings to meet stringent energy efficiency standards, and industrial insulation where protection against high temperatures is critical, such as in petrochemical plants and power generation facilities. Furthermore, its unique properties lend it to use in passive fire protection systems, acting as a crucial barrier to limit the spread of fire. The versatility and robustness of the material allow it to meet demanding specifications across diverse climate zones and regulatory environments, ensuring its continued relevance in the global push toward sustainable infrastructure development.

Driving factors for the substantial market growth include escalating global focus on energy conservation, underpinned by governmental mandates and building energy codes that demand higher R-values and lower U-factors for structures. The global imperative for decarbonization necessitates the insulation of building stock, thereby increasing demand for high-performance materials like Rockwool. Furthermore, rapid urbanization, particularly in Asia Pacific, coupled with significant investments in infrastructure development (residential, commercial, and industrial), provides a robust foundation for market expansion. The material's exceptional fire safety rating is becoming increasingly important, especially following several high-profile fire incidents globally, pushing regulatory bodies to favor non-combustible insulation solutions, directly benefiting the Rockwool sector. Ongoing product innovation, focusing on enhanced thermal performance and ease of installation, further consolidates its market position.

The global Rockwool market is characterized by robust growth, primarily fueled by stringent regulatory frameworks promoting energy efficiency and the rising global demand for non-combustible, sustainable building materials. Current business trends indicate a strong move toward product customization, focusing on high-density Rockwool products for enhanced acoustic insulation in urban environments and specialized solutions for high-temperature industrial processes. Manufacturers are strategically investing in optimizing production processes, specifically through digitalization and automation, to reduce energy consumption during manufacturing and improve yield rates. A key business strategy involves securing stable access to raw materials (basalt and slag) and expanding capacity in fast-growing regional hubs. Sustainability reporting and circular economy initiatives, such as the ability to recycle end-of-life Rockwool products, are increasingly vital competitive differentiators, influencing procurement decisions in major construction projects.

Regional trends highlight the Asia Pacific (APAC) as the fastest-growing market, driven by massive infrastructure spending, rapid urbanization, and the adoption of modern building standards in China, India, and Southeast Asian countries. Although APAC exhibits high growth, Europe maintains the largest market share, predominantly due to long-standing, aggressive energy efficiency directives (such as the Energy Performance of Buildings Directive) and high consumer awareness regarding sustainable construction. North America shows steady growth, particularly in commercial construction and industrial insulation applications, where high-temperature resistance is a premium requirement. Geopolitical stability and fluctuating raw material costs, particularly energy costs required for the melting process, represent significant regional sensitivities that affect operational margins and pricing strategies across continents.

Segmentation analysis reveals that the Building & Construction application segment dominates the market, contributing the largest share of revenue, driven by residential and commercial building insulation needs. Within the product type segment, boards/slabs maintain market leadership due to their versatility and ease of installation in structural applications (walls and roofs). However, specialized segments like pipe insulation and loose fill are showing accelerated growth due to increased industrial activity and the demand for efficient retrofitting solutions. Manufacturers are focusing R&D efforts on enhancing the water repellency and compressive strength of Rockwool products, ensuring their suitability for demanding applications like flat roofs and green roofs, diversifying the portfolio beyond standard thermal insulation. This targeted innovation confirms a market trajectory emphasizing performance and multifunctionality.

Common user questions regarding AI's influence on the Rockwool market typically revolve around operational efficiency, product development speed, and supply chain resilience. Key concerns include how AI can optimize the highly energy-intensive melting process to reduce carbon footprint and operating costs, and whether predictive maintenance can significantly lower equipment downtime in manufacturing facilities. Users also inquire about AI's role in optimizing the complex logistics of delivering bulky insulation products and improving quality control (QC) through automated visual inspection of fiber structure and density. The consensus expectation is that AI will not fundamentally alter the product itself but will revolutionize the manufacturing process, supply chain management, and material formulation optimization, leading to higher efficiency, lower waste, and ultimately, more competitively priced and sustainably produced Rockwool insulation. AI is seen as a crucial tool for aligning production with the stringent environmental, social, and governance (ESG) standards demanded by institutional buyers and regulatory bodies, particularly concerning energy consumption monitoring and emissions reduction strategies.

The Rockwool market is fundamentally driven by tightening global energy regulations and the intrinsic benefits of the material, particularly its non-combustible nature. Primary drivers include governmental mandates for thermal efficiency in buildings, significant growth in global construction activities, and increasing consumer awareness regarding sustainable building materials. However, the market faces significant restraints, chiefly the high initial capital investment required for establishing manufacturing facilities (due to the high-temperature requirements) and intense competition from alternative, often cheaper, insulation materials like expanded polystyrene (EPS) or polyurethane (PUR) foams in certain cost-sensitive applications. The volatility of energy prices, which heavily influences manufacturing costs, also acts as a constraint. Opportunities primarily lie in expanding industrial insulation applications, developing highly specialized hydrophobic variants for wet environments, and capitalizing on the hydroponics segment where Rockwool acts as an effective inert growth medium. Impact forces highlight the critical role of regulatory bodies in setting safety and performance standards, the influence of raw material scarcity (slag vs. basalt sourcing), and the pervasive pressure from environmental organizations to minimize the industry's manufacturing carbon footprint, thereby forcing innovation in furnace technology and material input composition.

The Rockwool market is comprehensively segmented based on product type, application, and end-use, allowing for detailed market targeting and strategic development. The product segmentation typically distinguishes between blankets/rolls, boards/slabs, pipe insulation, and loose fill, reflecting different forms tailored for specific installation methods and R-value requirements. Application segmentation focuses on the primary use case, separating thermal insulation, acoustic insulation, fire protection, and other uses like horticulture. The end-use segments delineate the final consumer industries, primarily Building & Construction (further split into residential and commercial sectors) and Industrial, which includes HVAC, marine, automotive, and power generation insulation requirements. Understanding these segments is crucial as market growth rates and competitive dynamics vary significantly between the high-volume, low-margin construction segment and the high-performance, high-margin industrial applications, necessitating differentiated manufacturing and marketing strategies.

The Rockwool value chain begins with the sourcing of primary raw materials, predominantly basalt (a natural igneous rock) and often recycled materials such as steel slag and mineral waste, which serve as crucial input materials. The upstream segment involves mining, crushing, and preparation of these materials, alongside the supply of auxiliary chemicals like binders and water repellents. Energy inputs, particularly natural gas or electricity for the high-temperature melting process (often exceeding 1,500 °C), represent a substantial cost component and a critical bottleneck in the upstream supply chain. Efficiency in this raw material and energy sourcing phase directly dictates the final product cost and environmental footprint. Strategic relationships with mining operations and efficient logistics for bulky raw materials are paramount for maintaining competitive manufacturing costs.

The midstream of the value chain is dominated by manufacturing—the controlled melting, fiberization (spinning the molten material), curing (adding binders and hydrophobic agents), and cutting/packaging processes. This stage is capital-intensive and requires high technical expertise for quality control, ensuring density uniformity, fiber length, and thermal performance standards are met. Major manufacturers operate integrated facilities globally, striving for continuous process improvement through automation and heat recovery systems. Downstream activities involve distribution and end-user application. Rockwool products, being bulky, require specialized logistics, often involving regional warehouses and efficient freight planning to minimize transportation costs, which can significantly impact the final price to the consumer. Key distribution channels include direct sales to large construction companies, industrial contractors, and indirect sales through specialized distributors and large retail home improvement chains, catering to smaller contractors and DIY markets.

The effectiveness of the distribution channel is highly dependent on market maturity. In established European markets, certified insulation installers and specialist distributors play a central role, ensuring compliance with complex building codes. In contrast, emerging markets often rely more heavily on direct manufacturer-to-contractor relationships. Direct channels facilitate technical support and project customization for large industrial projects, whereas indirect channels ensure broad market penetration for standard building products. The after-sales service and technical consultation provided at the distribution level are crucial, as correct installation is essential for achieving the advertised thermal and acoustic performance of Rockwool products. Furthermore, the increasing focus on the circular economy necessitates establishing effective reverse logistics for collecting and recycling construction and demolition waste containing Rockwool, closing the loop within the value chain.

The potential customer base for Rockwool is highly diversified, spanning both industrial and commercial/residential sectors, driven by the universal need for thermal management, acoustic dampening, and passive fire safety. The largest segment of buyers consists of large-scale construction companies and general contractors specializing in commercial real estate (office buildings, hospitals, schools) and multi-family residential housing, where high safety standards and long-term energy performance are mandatory requirements. These customers prioritize certified products that comply with local and international building codes (e.g., European standards like Euroclass A1 for non-combustibility).

Another significant group comprises industrial engineering, procurement, and construction (EPC) firms that procure large volumes of specialized Rockwool (such as high-density pipe sections and blankets) for high-temperature applications. These end-users include operators in the oil and gas industry, petrochemical processing plants, power generation facilities (both fossil fuel and nuclear), and marine vessel constructors. For this segment, the primary buying criteria are resistance to extreme temperatures, chemical inertness, and durability under harsh operating conditions, often involving specialized technical specifications that exceed standard building insulation requirements. Finally, a growing segment is the agricultural sector, particularly commercial hydroponic and greenhouse operations, where Rockwool slabs are utilized as an inert, high-performance medium for plant growth, valued for its optimal water retention and aeration properties.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 14.5 Billion |

| Market Forecast in 2033 | USD 21.4 Billion |

| Growth Rate | 5.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | ROCKWOOL International A/S, Owens Corning, Knauf Insulation, Saint-Gobain S.A., Beijing New Building Materials Public Limited Company, URSA Insulation S.A., Polyglass S.p.A., Paroc Group, Izovats, TechnoNICOL Corporation, Superglass Insulation Ltd., Rock-T-Wool, CSR Limited (Bradford), GAF Materials Corporation, Johns Manville, Termoizol, Afico, Thermafiber (part of Owens Corning), Vithal, KCC Corporation. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Rockwool market relies on sophisticated manufacturing technology centered around the controlled high-temperature melting and fiber spinning process. The core technology involves highly advanced cupola furnaces or electric melting furnaces, which must sustain temperatures exceeding 1,500 °C to homogenize the mineral mixture (basalt and slag). Crucial technological innovations are focused on improving the energy efficiency of these furnaces, such as implementing oxy-fuel combustion or advanced heat recovery systems (e.g., regenerative burners) to reduce the substantial energy input required, which is a key cost driver and environmental concern for the industry. Furthermore, advanced robotics and automation are utilized in handling and packaging, improving process precision and reducing manual intervention in high-heat environments. The shift toward electrification of the melting process, though capital intensive, is gaining traction as manufacturers seek to utilize renewable electricity sources to achieve long-term decarbonization goals.

Fiberization technology is another critical area, typically employing high-speed spinning machines (four-roller cascade spinners) to create uniform, fine fibers, which are crucial for achieving optimal thermal performance (low thermal conductivity). The binder technology represents a secondary but increasingly important landscape. Historically, formaldehyde-based binders were common; however, regulatory pressures and environmental concerns have spurred significant innovation toward bio-based, low-VOC (Volatile Organic Compound) or formaldehyde-free binders. These newer generation binders enhance the sustainability profile of the product without compromising its mechanical strength or thermal resistance. Ongoing research focuses on nano-structure enhancement within the fiber matrix to further reduce thermal conductivity, allowing for thinner insulation layers with superior R-values, particularly appealing for space-constrained urban construction projects.

In terms of application technologies, the industry is leveraging digital tools to streamline installation and specification. Building Information Modeling (BIM) integration allows architects and engineers to seamlessly incorporate Rockwool specifications into digital models, optimizing insulation placement and material quantity, thereby reducing waste. Specialized manufacturing techniques are also employed for creating tailored products, such as hydrophobic treatments applied during the curing stage to enhance water repellency for use in roofing and external wall systems, or the development of higher density products specifically engineered for impact sound reduction in floor applications. The continuous pursuit of technical standards compliance (e.g., CE marking in Europe, ASTM standards in North America) drives technological adherence and investment in sophisticated testing and quality assurance equipment throughout the manufacturing lifecycle.

The global Rockwool market demonstrates distinct growth profiles and maturity levels across different geographical regions, heavily influenced by local building codes, energy prices, and construction activity.

The primary drivers are stringent global energy efficiency regulations (requiring better building insulation), the inherent non-combustibility of Rockwool providing superior fire safety, and increasing demand from the massive global construction sector for high-performance, sustainable materials.

While Rockwool products contribute significantly to energy savings during a building's operation phase, the manufacturing process is energy-intensive due to the high-temperature melting required. Manufacturers are mitigating this through the use of recycled slag, implementing heat recovery systems, and transitioning towards renewable energy sources for furnaces.

The Building and Construction sector, specifically for thermal insulation in residential and commercial buildings, holds the largest market share, driven by mandatory thermal performance requirements in roofing, walls, and flooring applications globally.

Rockwool (stone wool) is typically denser and offers superior resistance to fire (non-combustible) and better acoustic dampening compared to standard fiberglass. Both are mineral wools, but Rockwool's basalt base allows it to withstand significantly higher temperatures, making it the material of choice for fire safety applications.

The Rockwool market is moderately consolidated, dominated by a few large multinational players, such as ROCKWOOL International and Owens Corning, who possess global manufacturing capabilities. However, regional markets feature numerous local competitors, particularly in Asia, leading to fragmentation in specific segments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.