ID : MRU_ 437384 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

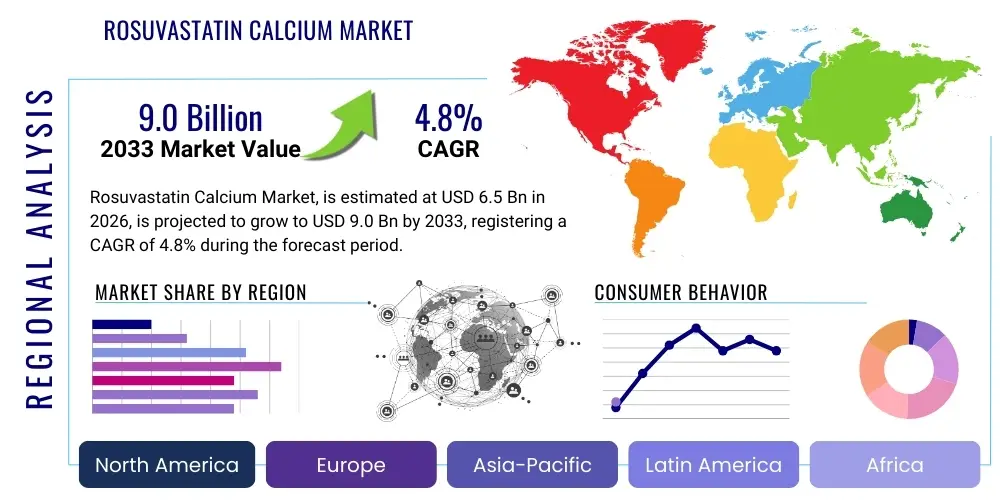

The Rosuvastatin Calcium Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 6.5 Billion in 2026 and is projected to reach USD 9.0 Billion by the end of the forecast period in 2033.

Rosuvastatin calcium is recognized globally as a highly efficacious synthetic inhibitor of 3-hydroxy-3-methylglutaryl coenzyme A (HMG-CoA) reductase, positioning it firmly within the class of drugs commonly known as statins. Its primary therapeutic purpose is the management of primary hypercholesterolemia, mixed dyslipidemia, and homozygous familial hypercholesterolemia. By selectively inhibiting the rate-limiting enzyme in cholesterol biosynthesis within the liver, Rosuvastatin dramatically reduces levels of low-density lipoprotein cholesterol (LDL-C), often referred to as 'bad cholesterol,' which is a crucial risk factor in the pathogenesis of atherosclerotic cardiovascular disease (ASCVD). Furthermore, clinical trials have demonstrated its capability to elevate high-density lipoprotein cholesterol (HDL-C) and modestly reduce triglycerides, thereby offering a comprehensive improvement in overall lipid profiles critical for cardiac health.

The clinical relevance of Rosuvastatin Calcium extends significantly into the realm of preventive cardiology. It is widely prescribed for the primary prevention of major cardiovascular events, such as myocardial infarction and stroke, in individuals who possess multiple ASCVD risk factors but may not yet present with overt coronary artery disease. This application reflects a broader shift in global clinical practice toward aggressive, early intervention to mitigate long-term cardiovascular burden, particularly in high-risk populations including those with Type 2 diabetes mellitus or established peripheral artery disease. The drug’s powerful LDL-C reduction capabilities, which often surpass those of older-generation statins like Simvastatin and Pravastatin, ensure its designation as a preferred therapeutic agent when intensive lipid lowering is required, cementing its role as a fundamental medicine on essential drug lists worldwide. The benefits of Rosuvastatin, encompassing LDL-C lowering, plaque stabilization, and proven long-term safety, underpin its status as a cornerstone in CVD management protocols.

The market dynamics are fundamentally driven by several powerful and interconnected factors. Firstly, the escalating global epidemic of lifestyle-related diseases, including obesity, hypertension, and sedentary habits, directly feeds the increasing prevalence of dyslipidemia, requiring sustained pharmacological intervention. Secondly, the widespread patent expiration of the original branded product (Crestor) has facilitated the entry of numerous generic manufacturers. This genericization has drastically lowered the cost of therapy, making high-efficacy treatment accessible to large populations across diverse socioeconomic settings, particularly supporting volume growth in emerging markets. Finally, ongoing research continues to reinforce the pleiotropic effects of Rosuvastatin—its anti-inflammatory and plaque-stabilizing properties—which provide therapeutic benefits beyond mere cholesterol reduction, ensuring continued confidence among prescribers despite the introduction of newer drug classes. The synthesis of high-quality, cost-effective API remains a central competitive element for generic companies seeking profitability in this mature yet high-volume pharmaceutical segment, driven by persistent global health needs.

The Rosuvastatin Calcium market analysis reveals a mature generic landscape characterized by high prescription volumes but highly competitive pricing dynamics. Business trends are dominated by aggressive cost optimization strategies employed by major pharmaceutical players to maintain thin margins in the face of widespread commoditization. Companies are increasingly focused on vertical integration, managing the entire supply chain from API synthesis to final formulation, thereby reducing reliance on third-party suppliers and safeguarding quality consistency across their global operations. A critical emerging business trend is the strategic pivot towards fixed-dose combination (FDC) products, which blend Rosuvastatin with antihypertensive, anti-diabetic, or anti-platelet agents. This innovation offers a crucial avenue for value-added differentiation and enhanced patient adherence, offering a modest premium over standard single-entity generic tablets, vital for long-term revenue stability in saturated developed markets.

Regional trends indicate a distinct bifurcation in market performance. Developed markets, encompassing North America and Western Europe, maintain high market volume stability, but exhibit minimal revenue growth due to peak generic penetration and stringent reimbursement policies enforced by national health services and private payers. These regions are focused on optimized utilization within established clinical pathways and tend to favor the lowest-cost generic options. Conversely, the high-growth potential is concentrated in the Asia Pacific (APAC) region, propelled by countries such as China, India, and Southeast Asian nations, which collectively represent the primary engine of volume expansion. This acceleration is linked to demographic transitions, rapidly expanding urbanization leading to a higher burden of non-communicable diseases, and significant investments in public health infrastructure which facilitates wider distribution and prescription of essential medicines. Local manufacturers in APAC are strategically capitalizing on government support for domestic production and large public tender opportunities.

Segmentation insights emphasize the overwhelming dominance of the oral tablet formulation, reflecting its universal acceptance and cost profile, and the primary application in addressing established hypercholesterolemia. However, the fastest-growing sub-segment is the utilization of Rosuvastatin for the primary prevention of ASCVD in intermediate-risk groups, reflecting global clinical guideline shifts towards earlier, aggressive intervention. Distribution channels remain heavily reliant on retail pharmacies and large drug store chains, underscoring the nature of Rosuvastatin as a chronic, outpatient therapy. The competitive environment is intensely oligopolistic among global generic giants who compete fiercely on price and large-scale tender acquisitions. The key strategic imperative for success remains volume maximization through efficient, low-cost API sourcing, regulatory proficiency, and robust supply chain resilience across multiple international jurisdictions.

In analyzing user queries regarding AI’s influence on the Rosuvastatin Calcium market, a recurring interest centers on how machine learning can enhance pharmacovigilance and quality control for generic formulations. With hundreds of generic versions available globally following patent expiry, users and regulators seek assurances regarding bioequivalence, efficacy consistency, and safety profiling across diverse product sources. AI algorithms are highly effective in processing and analyzing vast datasets of real-world patient data (RWD) and electronic health records (EHRs) to detect subtle variations in therapeutic outcomes or adverse event reporting (specifically statin-associated muscle symptoms - SAMS) across different generic manufacturers. This real-time, large-scale surveillance capability helps regulatory bodies and healthcare providers rapidly identify any deviations in quality or performance, ensuring that the mass market adoption of generic Rosuvastatin Calcium remains safe and reliable, which is crucial for maintaining clinical trust in the treatment class and managing public health outcomes effectively.

Furthermore, AI plays an increasingly vital role in optimizing the utilization and prescribing patterns of Rosuvastatin by moving the therapeutic model towards precision medicine. By integrating complex data inputs including patient characteristics, genomic markers (e.g., polymorphisms in SLCO1B1), metabolic profiles, and existing medication adherence data, AI models can predict a patient’s likely response to standard Rosuvastatin dosing, identifying potential non-responders or those susceptible to muscle-related side effects. This ability allows for the precision adjustment of dosage, initiation of alternative therapies, or tailored risk counseling, thus maximizing the efficacy and safety profile for each patient. This application of AI refines the drug's usage, maximizing its therapeutic window and enhancing patient compliance, thereby reinforcing Rosuvastatin's perceived value in the face of costly, newer non-statin competitors that rely on highly targeted patient selection. AI thus stabilizes Rosuvastatin’s demand by ensuring its appropriate and optimized deployment.

Operationally, within the highly optimized generic manufacturing sector, AI is instrumental in streamlining production logistics and improving quality management. Complex predictive maintenance systems monitor sophisticated API manufacturing equipment, minimizing unexpected shutdowns and maximizing throughput, which directly impacts the ability of generic companies to maintain competitive pricing by increasing operational efficiency. Supply chain optimization, leveraging AI to predict fluctuations in regional demand (e.g., seasonal variations or large government tender awards) and adjusting inventory levels accordingly, reduces carrying costs and prevents costly stockouts. Ultimately, AI transforms Rosuvastatin Calcium from a simple chemical compound into a component within a digitally managed therapeutic ecosystem, enhancing efficiency across its entire lifecycle, from synthesis through to patient adherence monitoring, thereby sustaining its position as the workhorse of cardiovascular prevention.

The Rosuvastatin Calcium market’s trajectory is dictated by a compelling set of market dynamics, where entrenched drivers meet significant restraining forces. The key market driver is the inexorable expansion of the global population afflicted by chronic metabolic disorders, including type 2 diabetes, obesity, and hypercholesterolemia, all of which mandate long-term statin therapy to prevent catastrophic cardiovascular outcomes. This sustained epidemiological pressure is buttressed by clear, globally accepted clinical guidelines that consistently mandate the use of high-intensity statins, such as Rosuvastatin, as the first line of defense. The drug's transition to an affordable generic status acts as an additional powerful driver, enabling mass procurement by public health systems in both mature and emerging markets, significantly increasing total addressable patient volume and consumption units annually.

Conversely, the primary and most acute restraint is the aggressive and sustained price deflation across all major markets following patent expiration. This "race to the bottom" severely erodes revenue per unit, forcing manufacturers to operate on minimal margins and constantly seek greater cost efficiencies, which limits investment in non-essential areas such as new formulation innovation or extensive marketing. Furthermore, the increasing emergence of novel, high-cost non-statin therapies, such as PCSK9 inhibitors and siRNA-based drugs (e.g., inclisiran), poses a moderate long-term threat. While these alternatives currently target niche patient populations (e.g., those with familial hypercholesterolemia or statin intolerance), their expanding indications and potential for less frequent dosing (e.g., bi-annual injections) could eventually chip away at the premium end of the Rosuvastatin market, though they are unlikely to replace it as the foundation therapy due to cost disparities.

Opportunities for sustaining profitability lie predominantly in strategic market maneuvers, specifically focusing on complex fixed-dose combinations (FDCs) and penetrating underdeveloped regions with growing healthcare needs. FDCs offer a mechanism to revitalize perceived product value by improving patient adherence and outcomes, allowing manufacturers to charge a slight premium over standard generics, thus sidestepping pure price competition. Geographically, expanding market penetration across high-population, high-growth rate emerging economies, particularly in Southeast Asia, the Middle East, and parts of Africa, represents a critical growth pathway. These regions are experiencing rapid expansion of private healthcare and government focus on chronic disease management, providing substantial tender opportunities for cost-effective, established cardiovascular treatments like Rosuvastatin. Successfully navigating the complex regulatory filing requirements and establishing robust local supply chains in these diverse jurisdictions is essential for seizing these expansion opportunities and maintaining market relevance.

The Rosuvastatin Calcium market is fundamentally segmented based on factors related to product type, therapeutic application, and distribution channel, reflecting the varied needs of both patients and institutional healthcare purchasers globally. The analysis of these segments is crucial for identifying pockets of resilience and future growth within this mature generic space. The formulation segment reveals that conventional oral tablets overwhelmingly dominate volume consumption due to their cost-effectiveness, ease of administration, and standardized clinical dosing protocols. However, a significant growth avenue lies within the Fixed-Dose Combinations (FDCs) segment, which addresses the pervasive issue of patient non-adherence by simplifying complex multi-drug regimens, thereby adding value beyond the basic generic product.

Application segmentation clearly demonstrates that the largest revenue share is derived from treating established hypercholesterolemia and mixed dyslipidemia, where the drug has proven indispensable in achieving strict LDL-C goals. Nevertheless, future growth momentum is anticipated to shift increasingly towards the primary prevention segment. As global health organizations and insurance payers recognize the long-term cost benefits of preventing initial cardiovascular events, clinical guidelines are becoming more aggressive in recommending statin initiation for individuals identified at intermediate risk, based on factors such as age, diabetes status, and elevated inflammatory markers. This focus on prevention significantly broadens the target patient pool. Furthermore, segmentation by dosage strength—from 5 mg up to 40 mg—is critical for market analysis, with 10 mg and 20 mg doses typically accounting for the bulk of prescriptions for maintenance therapy, accurately reflecting standard clinical practice necessary to meet LDL-C goals.

The value chain for Rosuvastatin Calcium commences with the rigorous, capital-intensive manufacturing of the active pharmaceutical ingredient (API). This upstream phase is crucial and is heavily concentrated among a few large, globally recognized API producers, predominantly based in South Asia (India) and China, leveraging geographical cost advantages and advanced chemical synthesis technologies. The process requires complex, multi-step chemical synthesis and purification, adhering strictly to global regulatory standards (e.g., US FDA, EMA GMP). Upstream analysis highlights that competitive success in this phase is defined by process chemistry innovation aimed at increasing yield, optimizing reaction conditions, and ensuring the absolute purity and consistent crystalline polymorphism of the Rosuvastatin calcium salt. This fierce upstream competition sets the baseline cost for the entire market, making strategic API procurement or efficient in-house production a defining competitive feature for generic companies seeking sustainable profitability.

Mid-stream activities focus on formulation and finished product manufacturing (FDF). This phase involves transforming the API into various dosage forms, primarily oral tablets, and ensuring the product meets stability, bioequivalence, and regulatory compliance requirements across diverse international markets. The formulation process requires sophisticated technological processes, especially for moisture-sensitive Rosuvastatin or complex FDCs requiring specialized drug layering and protective coating. Quality control and exhaustive stability testing are non-negotiable requirements here, demanding significant investment in analytical technology. Downstream activities revolve around product distribution and ensuring broad market access. The distribution model is predominantly indirect, utilizing global wholesalers and national distributors who manage vast logistics networks to efficiently move product from manufacturing plants to retail pharmacies and hospital procurement centers across multiple territories. This network management is critical due to the high volume and low-margin nature of the product, necessitating optimized inventory control and fast turnover.

Direct distribution, utilized mainly for securing large government contracts or bulk sales to managed care organizations, simplifies the supply chain and provides manufacturers with better control over realized pricing and delivery schedules, often yielding favorable terms by eliminating intermediary costs. However, indirect channels remain indispensable for maximizing retail market penetration into fragmented global landscapes. The end-users—patients, prescribers, and institutional buyers—exert powerful influence on the value chain. Pharmacy Benefit Managers (PBMs) and national healthcare systems, acting as centralized buyers in developed markets, leverage Rosuvastatin's generic status to dictate pricing and inclusion on essential medicine lists, profoundly impacting the realized profitability at the manufacturer level. Consequently, sustained generic market success depends less on novel drug development and more on vertical integration, superior regulatory expertise for rapid multi-jurisdiction filing, and sheer logistical prowess to dominate high-volume supply tenders globally, ensuring product accessibility and cost minimization across the entire chain.

The Rosuvastatin Calcium market is characterized by a high volume of potential customers spanning both clinical and institutional segments. The primary consumer is the patient population, specifically adults over the age of 45, globally, who have been diagnosed with primary hypercholesterolemia, mixed dyslipidemia, or established cardiovascular disease. This demographic typically requires lifelong, chronic therapy, ensuring stable, sustained demand for maintenance doses. A secondary, yet increasingly critical patient cohort includes individuals who are asymptomatic but identified through risk screening (e.g., high Framingham risk scores or elevated C-reactive protein) as candidates for primary prevention of major cardiac events. As preventative medicine gains traction globally, this cohort represents significant future growth in prescription volume, particularly in regions where health screening is becoming more prevalent.

Beyond the individual patient, critical institutional buyers significantly influence market procurement and pricing. These include Government Health Systems and national public health agencies (such as those in Europe, India, and China), which engage in massive annual procurement tenders, purchasing bulk volumes of generic Rosuvastatin based almost exclusively on the lowest achievable cost per unit and proven regulatory compliance. Similarly, Pharmacy Benefit Managers (PBMs) in the US and large regional managed care organizations act as powerful, consolidated customers. They control formulary inclusion and reimbursement status, effectively acting as gatekeepers to the mass market. These institutional customers prioritize robust supply assurance, impeccable regulatory history, and maximal cost savings, viewing Rosuvastatin as a cost-effective commodity essential for managing population health, thus dictating the intense competition among generic suppliers focused on delivering value and volume efficiency.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 9.0 Billion |

| Growth Rate | 4.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Teva Pharmaceutical Industries, Mylan (Viatris), Sun Pharmaceutical Industries, Hikma Pharmaceuticals, Aurobindo Pharma, Dr. Reddy's Laboratories, Pfizer Inc., AstraZeneca PLC (Generic/API involvement), Cipla Ltd., Lupin Ltd., Sandoz (Novartis), Apotex Inc., Zydus Cadila, Alkem Laboratories,Torrent Pharmaceuticals, Amneal Pharmaceuticals, Glenmark Pharmaceuticals, Intas Pharmaceuticals, Cadila Pharmaceuticals, Daiichi Sankyo Company, Limited, Hetero Drugs Ltd., Granules India Ltd., Unichem Laboratories, Natco Pharma Limited, Shandong Xinhua Pharmaceutical Co., Ltd., Hubei Tianrui Chemical Co., Ltd., Changzhou Pharmaceutical Factory. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape surrounding the Rosuvastatin Calcium market is predominantly focused on advanced pharmaceutical engineering and digitalization aimed at maximizing efficiency and product stability in a hyper-competitive generic environment, rather than molecular drug innovation. A critical area of technological focus is the deployment of highly sophisticated continuous manufacturing processes for API synthesis. This technology moves beyond traditional batch processing, allowing for uninterrupted production, reduced cycle times, and enhanced quality monitoring through sophisticated Process Analytical Technology (PAT) systems. The shift toward continuous flow chemistry for Rosuvastatin production grants leading manufacturers significant cost advantages by reducing labor, minimizing waste, and accelerating throughput, essential competitive edges when selling a high-volume, low-margin generic product into global markets. Furthermore, precise control over crystallization technology is paramount to ensure consistent crystalline structure (polymorphism) and guaranteed bioequivalence across all generic batches, a non-negotiable regulatory standard.

In terms of dosage formulation, specialized coating and tablet-pressing technologies are crucial. Rosuvastatin is inherently sensitive to moisture and light, necessitating the use of advanced polymer film coatings and optimized excipient blends to maintain chemical stability and prolong shelf life, particularly for products destined for high-humidity regions in APAC and LATAM. Furthermore, the development and regulatory filing of Fixed-Dose Combinations (FDCs) utilize complex multi-layer tablet technology or specialized matrix systems. These require sophisticated pharmaceutical engineering to ensure that chemically incompatible drugs (like Rosuvastatin and certain anti-hypertensives) can be combined into one unit dose while maintaining precise release kinetics, stability, and therapeutic efficacy for all combined compounds, effectively improving complex patient management.

Indirect technological influences include the integration of digital health and supply chain management systems utilizing big data analytics and artificial intelligence. Digital twin technology is increasingly adopted in pharmaceutical operations, allowing engineers to simulate and optimize complex manufacturing parameters—such as material flow and temperature control—without physical disruption, thereby drastically reducing production variability and time-to-market. Additionally, the adoption of smart packaging and adherence monitoring systems tracks whether patients are taking their Rosuvastatin as prescribed. This data integration into telehealth platforms and Electronic Health Records (EHRs) ensures consistent adherence, maximizes the real-world therapeutic effect, and further reinforces the stability of prescription volumes, ensuring that Rosuvastatin remains a highly utilized chronic medication managed through advanced digital platforms.

Market consumption and growth patterns for Rosuvastatin Calcium demonstrate high sensitivity to regional healthcare policies, economic development, and epidemiological profiles, creating varied market dynamics across the globe.

The primary factor driving demand is the escalating global prevalence of cardiovascular diseases (CVD), hypercholesterolemia, and related metabolic syndromes, coupled with the established efficacy and cost-effectiveness of generic Rosuvastatin as a first-line treatment in clinical guidelines worldwide. Its inclusion in essential medicine lists ensures high utilization.

Generic availability has severely constrained overall market revenue growth due to intense price erosion and margin compression. However, it has dramatically increased prescription volume and patient accessibility, shifting market dynamics from branded revenue to generic volume maximization and efficient supply chain operation.

The Asia Pacific (APAC) region, specifically emerging economies like China and India, is projected to experience the fastest market growth. This is driven by rapid increases in disease incidence linked to urbanization, improving healthcare infrastructure, and expanding public health initiatives promoting essential chronic disease medications.

Yes, FDCs are a key strategic trend. They offer enhanced patient adherence and therapeutic convenience by combining Rosuvastatin with other cardiovascular drugs (e.g., anti-hypertensives). This strategy allows manufacturers to revitalize product value and achieve differentiation in the highly commoditized core generic market.

The main restraints are intense price competition among generic manufacturers, high bargaining power of institutional buyers (PBMs, governments) who negotiate massive volume discounts, and the moderate, long-term threat posed by newer, high-cost non-statin lipid-lowering therapies.

AI contributes by enabling precision medicine, utilizing machine learning algorithms to analyze genetic and clinical patient data to predict optimal Rosuvastatin dosing, thereby improving efficacy, minimizing adverse effects, and supporting healthcare providers in adhering to personalized treatment protocols.

Upstream API technology is critical for competitive advantage. The adoption of advanced chemical engineering and continuous manufacturing processes allows leading companies to maximize production yield, ensure high purity, and significantly reduce the cost of goods sold, which is essential for winning large generic volume tenders.

Advanced formulation requires specialized coating technologies to protect the moisture-sensitive Rosuvastatin molecule and enhance stability, alongside complex multi-layer tablet technology essential for developing stable and effective fixed-dose combination products.

The application segment dedicated to the primary prevention of atherosclerotic cardiovascular disease (ASCVD) in intermediate-risk patients is expected to drive future volume growth, following increasingly aggressive clinical guidelines recommending early statin initiation.

PBMs exert significant control by managing formularies and negotiating prices on behalf of health plans. They leverage the abundant generic supply to demand deep discounts, often favoring the lowest-cost manufacturer to ensure Rosuvastatin remains affordable and accessible within their covered drug lists, pressuring manufacturer margins.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.