ID : MRU_ 439080 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

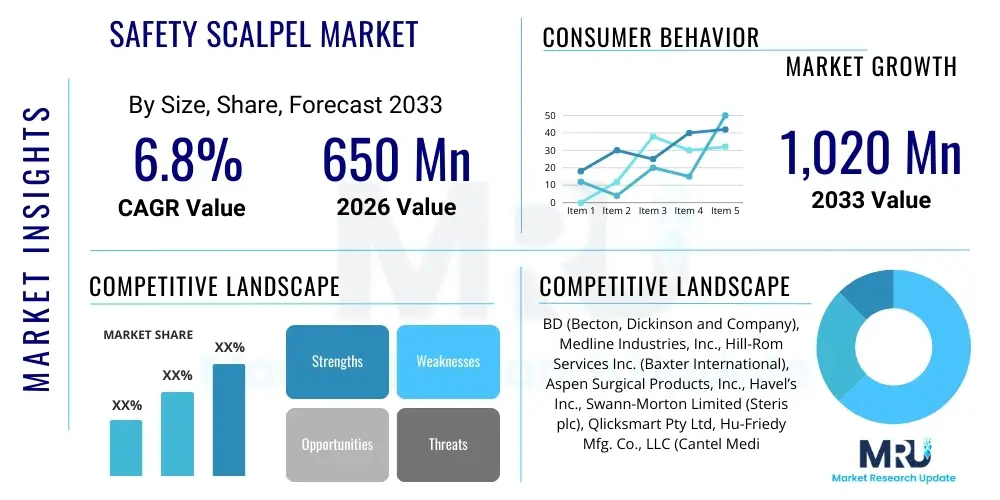

The Safety Scalpel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 650 Million in 2026 and is projected to reach USD 1,020 Million by the end of the forecast period in 2033.

The Safety Scalpel Market encompasses specialized surgical cutting instruments designed with integrated protective mechanisms aimed at minimizing accidental sharps injuries, particularly needlestick and laceration injuries, among healthcare professionals. These devices typically feature protective sheaths, retraction systems, or blunt tips to cover the blade before and after use, adhering strictly to global occupational safety standards. The primary objective is to enhance the safety profile in operating rooms and clinical settings where high volumes of surgical procedures are performed, thus reducing the risk of transmitting bloodborne pathogens such as HIV, Hepatitis B, and Hepatitis C. The design innovation focuses on maintaining the precision and performance of traditional scalpels while incorporating robust safety measures that are intuitive and easily activated single-handedly by the user.

Major applications of safety scalpels span across general surgery, orthopedic surgery, cosmetic procedures, cardiology, and emergency medicine, making them indispensable tools in modern healthcare infrastructure. The increasing volume of complex surgeries worldwide, coupled with the heightened regulatory focus on creating safer clinical environments, consistently drives their adoption. Benefits include substantial reduction in hospital liability costs associated with sharps injuries, improved staff morale, and compliance with stringent international safety guidelines, notably the OSHA Bloodborne Pathogens Standard in the United States and similar directives across Europe and Asia Pacific. These instruments are available in various materials and configurations, catering to specific procedural requirements, ensuring that safety does not compromise surgical efficacy.

Driving factors for this market include the global imperative to reduce healthcare-associated infections (HAIs) and occupational injuries. Mandatory safety legislation imposed by governing bodies significantly accelerates the shift from traditional scalpels to safety-engineered variants. Furthermore, continuous technological advancements in retraction and locking mechanisms are improving device usability and reliability, making the transition seamless for surgeons. The widespread awareness campaigns orchestrated by occupational health organizations, coupled with the rising geriatric population necessitating increased surgical interventions, solidify the sustained growth trajectory of the safety scalpel market throughout the forecast period.

The global Safety Scalpel Market is characterized by robust growth, primarily fueled by strict adherence to occupational safety regulations in developed economies and a burgeoning demand for safer medical consumables in rapidly expanding healthcare markets. Current business trends indicate a strong preference for disposable, single-use safety scalpels, owing to concerns over reprocessing effectiveness and cross-contamination risks. Key manufacturers are concentrating on ergonomic design improvements and developing advanced passive safety features that activate automatically upon use withdrawal, thereby minimizing user intervention error. Strategic mergers, acquisitions, and partnerships focused on distribution network expansion in emerging markets like India, China, and Brazil are shaping the competitive landscape, while continuous patent filings for unique blade retraction systems highlight the focus on intellectual property and differentiation in a safety-critical domain.

Regional trends reveal North America maintaining market dominance, driven by early adoption of sophisticated safety standards, favorable reimbursement policies for safety-engineered devices, and a high incidence of chronic diseases requiring surgical intervention. However, the Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR), stimulated by massive investments in public health infrastructure, increasing medical tourism, and the gradual adoption of stringent sharps injury prevention protocols across major developing nations. European markets demonstrate stable growth, heavily influenced by the European Union’s Council Directive concerning the prevention of sharps injuries in the hospital and healthcare sector, pushing mandatory implementation across member states. The Middle East and Africa (MEA) and Latin America show promising potential, albeit constrained by budget limitations and slower regulatory enforcement compared to Western counterparts.

Segmentation trends illustrate that the Retractable Safety Scalpel segment holds a significant market share due to its superior protection mechanism and versatility across various surgical disciplines. Among end-users, Hospitals remain the largest consumer segment, given the volume and complexity of procedures performed. Nevertheless, Ambulatory Surgical Centers (ASCs) are rapidly emerging as a fast-growing segment, propelled by the increasing shift of minor and intermediate surgeries to outpatient settings, demanding efficient, high-volume disposable safety solutions. Manufacturers are increasingly exploring specialized material coatings, such as ceramic blades, for specific procedures requiring enhanced sharpness retention or non-magnetic properties, though stainless steel remains the dominant material due to its cost-effectiveness and proven performance in general surgery.

User inquiries regarding Artificial Intelligence (AI) in the context of the Safety Scalpel Market typically revolve around whether AI will directly integrate into the physical device, how it can optimize safety protocols, and its influence on procurement and supply chain management. The prevailing consensus reflected in user queries is that while the physical scalpel remains a manually operated tool, AI significantly impacts the ecosystem surrounding surgical safety. Key themes include AI's role in predictive risk modeling for sharps injuries, optimizing surgical workflows to reduce human error, and utilizing computer vision and machine learning algorithms for enhanced surgical training and performance monitoring. Users are particularly interested in how data generated from surgical safety logs can be analyzed by AI to mandate targeted safety training and drive evidence-based procurement decisions, prioritizing devices that demonstrably reduce injury rates in specific procedural contexts. This analytical layer adds a crucial dimension of intelligence to the utilization and selection of safety equipment.

The indirect yet powerful impact of AI stems from its capability to revolutionize surgical training and procedural standardization. AI-driven simulation platforms and robotic surgery systems, which often utilize specialized sharp instruments including safety scalpels, rely on machine learning to provide real-time feedback to trainees regarding technique, instrument handling, and tissue interaction. By improving the precision and consistency of surgical actions through intelligent feedback loops, the likelihood of accidental sharps exposure, which often occurs due to fatigue or inexperienced handling, is inherently reduced. AI systems contribute to a safer environment by minimizing variability in procedural execution, ensuring compliance with established protocols, and automating documentation related to equipment usage and disposal.

Furthermore, AI is fundamentally changing the procurement and inventory management landscape for specialized consumables like safety scalpels. Machine learning algorithms analyze historical usage rates, procedural schedules, and vendor performance to predict optimal stock levels, prevent shortages, and ensure the timely availability of the required safety devices. This optimization minimizes wastage and ensures that facilities consistently have the necessary safety-engineered instruments, thereby preventing staff from reverting to cheaper, non-safety alternatives due to supply constraints. AI also assists in regulatory compliance tracking, automatically flagging safety incidents and integrating that data into performance metrics for device selection, offering hospitals data-driven insights into the long-term cost benefits of investing in premium safety scalpels over cheaper conventional options.

The dynamics of the Safety Scalpel Market are significantly influenced by a confluence of powerful drivers, stringent restraints, compelling opportunities, and overriding impact forces that dictate market adoption rates and technological advancement. A primary driver is the global enforcement of occupational safety regulations, notably concerning the prevention of sharps injuries, mandated by organizations like OSHA and European directives, which compels healthcare institutions to adopt safety-engineered devices. The growing awareness regarding the severe risks associated with bloodborne pathogen transmission (e.g., HIV, HBV, HCV) acts as a powerful catalyst, positioning safety scalpels as an essential component of infectious disease control protocols. This regulatory and public health pressure ensures continuous uptake, moving the market away from conventional, unprotected instruments towards universal use of safety variants.

Despite strong drivers, the market faces restraints, primarily related to the relatively higher acquisition cost of safety scalpels compared to traditional blades. Budgetary constraints, particularly in low-resource settings and emerging economies, often lead procurement departments to prioritize cost savings over immediate safety improvements, slowing widespread adoption. Furthermore, resistance to change among some experienced surgeons, who may express concerns about potential changes in device feel, ergonomics, or slight compromises in precision (though often unfounded in modern designs), presents a psychological barrier. The complexity of integrating various retraction and locking mechanisms into existing surgical workflows also necessitates additional training and standardization efforts, posing logistical challenges for large healthcare systems.

Significant opportunities exist in technological innovation focused on developing fully passive safety mechanisms that require minimal or no user action for activation, thereby maximizing inherent safety. The expansion into high-growth, underserved markets in Asia Pacific and Latin America, driven by massive healthcare infrastructure modernization projects, provides ample scope for market penetration. Furthermore, strategic partnerships with Group Purchasing Organizations (GPOs) and major hospital chains allow manufacturers to secure long-term, high-volume contracts. The increasing shift towards specialized surgical centers and office-based surgical settings also creates demand for cost-effective, high-quality disposable safety instruments that cater specifically to high turnover, outpatient environments. The combined impact forces include escalating liability costs associated with sharps injuries, compelling hospitals to invest prophylactically, and the continuous pressure from healthcare worker unions demanding safer working conditions.

The Safety Scalpel Market is extensively segmented based on key structural attributes, including the mechanism of the blade, the primary end-user facility, and the material composition of the blade. This segmentation allows for targeted market analysis and enables manufacturers to tailor product offerings to specific operational requirements and cost sensitivities across different healthcare sectors. Understanding these segments is crucial for strategic planning, as adoption rates and feature preferences vary significantly between high-volume surgical hospitals and smaller specialty clinics. The Disposable segment, for example, heavily dominates the market due to regulatory preferences for single-use items to mitigate reprocessing risks, contrasting with specialized segments where reusability might still be considered in non-safety-critical components.

The value chain for the Safety Scalpel Market begins with the upstream procurement of specialized materials, including high-grade stainless steel or carbon steel for blades, specialized plastics (polymers) for the handle and safety mechanism components, and specific alloys for retraction springs. Key upstream activities involve maintaining strict quality control over raw material sourcing to ensure blade sharpness, durability, and corrosion resistance, which are critical for surgical performance. Material suppliers must comply with rigorous medical-grade specifications (e.g., ISO standards) as dictated by the scalpel manufacturers. Cost management in the upstream phase is critical, as the increased complexity of the safety mechanism inherently raises manufacturing costs compared to conventional scalpels, requiring efficient material utilization and inventory management.

The core manufacturing stage involves precision engineering, including stamping, grinding, assembly, sterilization, and packaging. This stage is highly regulated, necessitating compliance with GMP (Good Manufacturing Practices) and specific sterilization standards (e.g., ethylene oxide or gamma radiation). Scalpel companies invest heavily in automated assembly lines, particularly for complex retractable models, to ensure the reliable functioning of the safety features. Differentiation often occurs here through proprietary ergonomic handle designs and patented safety retraction mechanisms, creating barriers to entry for new competitors. Quality assurance (QA) protocols are stringent, ensuring that every safety scalpel performs reliably and that the protective mechanism is robust enough to prevent accidental activation during or after surgery.

Downstream activities center on distribution and end-user engagement. Distribution channels are predominantly indirect, relying on large medical device distributors (national and regional) who manage warehousing, logistics, and sales to hospitals, ASCs, and clinics. Direct sales models are often employed for strategic accounts or specialized product lines. The final step involves the end-user hospitals and surgical centers, where training and adoption are paramount. Effective post-market surveillance, including tracking sharps injury incidents related to the device, provides crucial feedback to manufacturers for continuous improvement. The strong reliance on GPOs in developed markets simplifies procurement for large institutions but intensifies price negotiation pressure on manufacturers, necessitating efficient supply chain logistics and strong contractual relationships.

The primary potential customers and end-users of safety scalpels are institutions where surgical procedures and invasive medical treatments are routinely performed, requiring sterile, precise cutting tools while maintaining high occupational safety standards. Hospitals, particularly large tertiary care and university teaching hospitals, represent the most significant customer segment due to the sheer volume and complexity of the surgeries they handle across all specialties, including trauma, orthopedic, cardiovascular, and general surgery. Their procurement decisions are often influenced by institutional safety mandates, compliance with national accreditation bodies, and the need to manage substantial workforce injury liability costs. These facilities typically purchase in bulk through centralized procurement systems or GPO contracts, favoring vendors who offer a comprehensive portfolio of blade sizes and retraction mechanisms.

Ambulatory Surgical Centers (ASCs) and outpatient specialty clinics constitute the fastest-growing customer segment. ASCs focus primarily on less invasive, high-turnover procedures (e.g., ophthalmology, orthopedics, gastroenterology), demanding highly reliable, disposable, and cost-effective safety scalpels that fit streamlined operational budgets. Their procurement strategies prioritize convenience, ease of use, and quick disposal protocols. As procedures increasingly shift from inpatient hospital settings to ASCs to reduce overall healthcare costs, the demand for safety instruments tailored to outpatient environments continues to rise substantially. Physicians' offices, particularly those performing minor skin procedures or biopsies, also form a critical customer base, favoring user-friendly, non-retractable sheath-based safety devices.

Furthermore, research laboratories, pathology centers, and veterinary clinics represent niche but important potential customers. These institutions utilize scalpels for dissection, tissue preparation, and various biological procedures, often involving infectious materials. For these end-users, safety scalpels are essential not just for occupational safety but also for maintaining laboratory compliance and biohazard control protocols. The driving factor for these specialized segments is stringent laboratory safety regulations and the absolute necessity of preventing exposure to biological samples, thus making the safety features of the scalpel a non-negotiable requirement in their purchasing criteria.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 650 Million |

| Market Forecast in 2033 | USD 1,020 Million |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | BD (Becton, Dickinson and Company), Medline Industries, Inc., Hill-Rom Services Inc. (Baxter International), Aspen Surgical Products, Inc., Havel’s Inc., Swann-Morton Limited (Steris plc), Qlicksmart Pty Ltd, Hu-Friedy Mfg. Co., LLC (Cantel Medical), Kai Corporation, Mani, Inc., Angiotech Pharmaceuticals, Inc. (Medical Devices Business), Tidi Products, LLC, Feather Safety Razor Co., Ltd., JMI Laboratories, Cincinnati Surgical Company, LLC, Mortone Surgical, Inc., SecuritSharp, Inc., Suture Safe, DeRoyal Industries, Inc., Myco Medical, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Safety Scalpel Market is defined by continuous innovation focused on enhancing both user safety and surgical performance while simplifying the activation of the protective mechanism. The primary technological advancements center around retraction and locking mechanisms. Modern designs increasingly utilize spring-loaded, single-hand activated retraction systems that provide audible and tactile confirmation of the blade being securely locked in the safe position post-use, preventing inadvertent exposure. Passive safety features, which automatically sheath the blade upon withdrawal from the incision or after a predetermined number of uses, are gaining traction as they eliminate the element of human error inherent in manual activation systems. Material science advancements also play a critical role, involving specialized coatings on blades to maintain sharpness longer and reduce friction, improving the cutting edge precision which is crucial for microsurgery and specialized procedures.

Ergonomics and design optimization represent another significant technological focus. Manufacturers are developing handles that mimic the weight, balance, and feel of traditional scalpels to facilitate seamless adoption by surgeons. These handles often incorporate textured grips and optimized weight distribution to reduce hand fatigue and enhance control, ensuring that the safety mechanism does not compromise the surgical tactile experience. Furthermore, the integration of radio-frequency identification (RFID) technology into high-value or specialized safety scalpels is an emerging trend. While not widely adopted, this technology aims to improve inventory tracking, prevent misplaced instruments (a critical safety issue), and ensure accurate disposal logging, thereby enhancing accountability and optimizing supply chain logistics within hospital settings, particularly for complex operative environments.

The market also sees technological advancement in blade material diversification. While stainless steel remains standard, high-performance ceramic blades are increasingly used in procedures requiring non-magnetic properties (e.g., MRI-guided surgery) or extreme sharpness retention over prolonged use. Similarly, advancements in sterilization technology ensure the integrity of the plastic components used in the safety mechanism. Disposable safety scalpel designs focus on using cost-effective, bio-compatible polymers that can withstand harsh sterilization processes without degrading, guaranteeing device reliability right up to the point of use. The convergence of these technologies – enhanced mechanics, smart tracking, and superior materials – is driving the premium segment of the safety scalpel market and raising the overall safety benchmark for surgical consumables globally.

North America is anticipated to maintain its dominant position in the Safety Scalpel Market throughout the forecast period. This leadership is underpinned by exceptionally stringent occupational safety regulations, particularly those enforced by the Occupational Safety and Health Administration (OSHA) in the U.S., which mandate the use of safety-engineered devices to minimize sharps injuries. The region benefits from a high level of healthcare expenditure, sophisticated infrastructure, and rapid adoption of advanced surgical technologies, supported by favorable reimbursement policies that incentivize hospitals to invest in premium safety instruments. The high prevalence of chronic conditions requiring surgical management and strong advocacy from healthcare worker unions further solidify North America's market stature.

Europe represents a mature market characterized by steady growth, primarily influenced by the European Union’s Council Directive (2010/32/EU) which requires all member states to implement measures to prevent sharps injuries. Countries such as Germany, the UK, and France show high adoption rates, driven by national healthcare systems prioritizing staff safety and minimizing litigation risks. The European market exhibits a strong preference for high-quality, reusable handle systems coupled with disposable blades, balancing safety needs with environmental considerations and standardized surgical practices. Regulatory harmonization and collective safety protocols across the European Economic Area ensure a consistent demand structure for compliant safety scalpel designs.

The Asia Pacific (APAC) region is projected to be the fastest-growing market globally, presenting immense potential due to rapidly expanding healthcare infrastructure, rising disposable incomes, and increasing awareness regarding occupational safety. Major contributors to this growth include China, India, and Japan. While Japan and Australia demonstrate regulatory environments similar to Western standards, countries like China and India are undergoing massive transitions, upgrading public hospitals and gradually implementing national sharps injury prevention guidelines. The market in APAC is price-sensitive but shows accelerating demand for high-volume, disposable safety scalpels as procedural volumes soar and governments increase spending on public health initiatives and modernizing medical facilities.

Latin America (LATAM) and the Middle East & Africa (MEA) are emerging markets with moderate, but accelerating, growth prospects. In LATAM, regulatory environments are gradually tightening, pushing hospitals toward safer device procurement, though high import duties and economic instability can sometimes restrain market growth. Brazil and Mexico are key markets in this region. The MEA region, particularly the Gulf Cooperation Council (GCC) countries (Saudi Arabia, UAE), is witnessing significant investment in high-end medical tourism facilities, leading to the adoption of international safety standards and premium safety scalpels. However, political instability and uneven healthcare penetration in certain African countries moderate the overall regional growth rate, making procurement often reliant on international aid organizations and private investment.

The Safety Scalpel Market is projected to exhibit a steady Compound Annual Growth Rate (CAGR) of 6.8% between the forecast years 2026 and 2033, driven primarily by increasing global regulatory mandates and growing awareness of sharps injury prevention.

Safety scalpels utilize integrated protective mechanisms, such as retractable blades or protective sheaths, which are designed to cover the sharp edge immediately after use, preventing accidental contact and thus significantly reducing the transmission risk of bloodborne pathogens.

Based on blade type, the Retractable Safety Scalpel segment holds a dominant market share due to its advanced, robust mechanism that ensures the blade is permanently and securely locked within the handle post-use, offering superior protection and compliance with stringent safety protocols.

Yes, the higher initial acquisition cost of safety-engineered scalpels, often due to complex manufacturing and material requirements, acts as a primary restraint, particularly in price-sensitive emerging markets where budget limitations impact procurement decisions for medical consumables.

The Asia Pacific (APAC) region is anticipated to record the highest growth rate, fueled by substantial government investment in healthcare infrastructure, the expansion of medical tourism, and the accelerated adoption of international occupational health and safety standards in key economies like China and India.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.