ID : MRU_ 435456 | Date : Dec, 2025 | Pages : 251 | Region : Global | Publisher : MRU

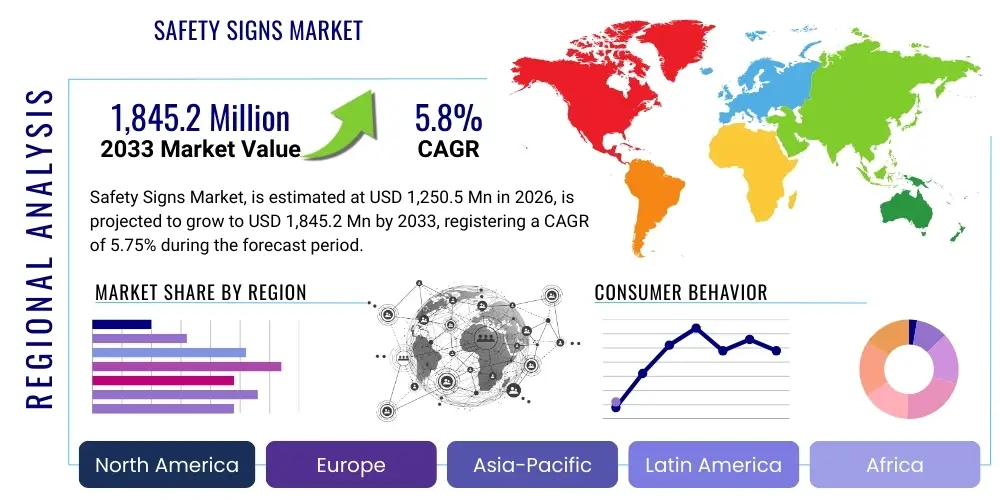

The Safety Signs Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.75% between 2026 and 2033. The market is estimated at USD 1,250.5 Million in 2026 and is projected to reach USD 1,845.2 Million by the end of the forecast period in 2033.

The Safety Signs Market encompasses the production and distribution of visual aids designed to convey critical information regarding hazards, mandatory actions, permitted activities, and emergency procedures in workplaces, public spaces, and industrial environments. These signs are essential tools for maintaining compliance with stringent occupational safety regulations enforced globally by bodies such as OSHA (Occupational Safety and Health Administration) and ISO (International Organization for Standardization). Products range from standard prohibition and warning signs to specialized photoluminescent and electronic signs, utilizing various materials like vinyl, aluminum, polyester, and acrylic to ensure durability and visibility under diverse operational conditions.

Safety signs serve a primary function in risk mitigation by minimizing workplace accidents and ensuring the well-being of personnel. Major applications span high-risk sectors including construction, heavy manufacturing, petrochemicals, transportation infrastructure, and healthcare facilities. The efficacy of these signs is critically dependent on adherence to standardized formats, colors, and pictograms, ensuring universal interpretation irrespective of linguistic barriers. The adoption of advanced materials that offer high durability, weather resistance, and enhanced visibility, such as retroreflective and glow-in-the-dark properties, is steadily increasing across mature markets.

The market growth is fundamentally driven by the escalating implementation of global safety standards, particularly concerning fire safety, chemical handling, and machine guarding. Furthermore, the rapid expansion of industrial infrastructure in developing economies necessitates the installation of comprehensive signage systems to meet modern safety protocols. Key benefits derived from robust safety signage deployment include reduced liability risks for companies, improved operational efficiency due to clear navigation, and a measurable decrease in lost-time incidents, solidifying safety signs as non-negotiable investments for any responsible organization.

The global Safety Signs Market is characterized by steady regulatory push across all major geographies, making compliance the central growth driver. Business trends indicate a shift towards customized, high-specification signage, particularly those integrating smart technology, durable substrates, and multi-lingual formats to serve complex international operations. Furthermore, the integration of digital display boards for dynamic messaging is emerging, though conventional physical signs remain dominant due to reliability and cost-effectiveness. Key players are focused on securing long-term supply agreements with large multinational industrial conglomerates and expanding their product lines to include sustainable, recycled, or low-VOC content materials to appeal to environmentally conscious procurement strategies.

Regionally, North America and Europe currently dominate the market, primarily due to well-established, strictly enforced safety legislation and high levels of awareness regarding occupational hazards. However, the Asia Pacific (APAC) region is projected to register the highest growth rate during the forecast period, fueled by rapid industrialization, large-scale infrastructural projects, and the increasing adoption of Western safety standards by local governments and international corporations operating within countries like China, India, and Southeast Asia. The standardization efforts in APAC are creating substantial demand for compliant and robust safety identification products.

Segmentation trends reveal that the Warning Signs category holds the largest market share, essential for communicating immediate hazards. Simultaneously, the demand for specialized materials, particularly photoluminescent (glow-in-the-dark) signs, is witnessing above-average growth, driven by requirements for emergency egress marking in low-light or power-failure scenarios within public buildings and tunnels. The Manufacturing and Construction sectors remain the primary end-users, consistently requiring replacements and new installations corresponding to project expansions and regulatory updates. E-commerce platforms are increasingly critical distribution channels, enabling smaller businesses and regional procurement managers access to a wide variety of specialized safety products quickly and efficiently.

User queries regarding the impact of Artificial Intelligence (AI) on the Safety Signs Market frequently revolve around the potential for 'smart' or adaptive signage systems, the role of computer vision in auditing sign compliance, and whether digital screens powered by AI algorithms could eventually replace traditional static signs. Users are keenly interested in how AI can enhance the effectiveness of safety communication, specifically asking about real-time hazard detection linked to immediate, localized warnings, and the optimization of sign placement based on dynamic environmental and personnel flow data. Concerns also include the security implications and reliability of digital systems compared to passive signage.

AI is influencing the Safety Signs Market primarily through optimization and enforcement mechanisms rather than fundamentally altering the signs themselves. AI-powered computer vision systems are being deployed to monitor workplaces, automatically identifying instances where mandatory protective equipment is missing or where unauthorized personnel enter restricted areas. In such scenarios, AI acts as a compliance auditor, flagging non-conformity, which in turn drives demand for compliant physical signage when deficiencies are found. Furthermore, AI analytics can process accident data and operational patterns to strategically recommend the necessity and placement of specific warning or prohibition signs, ensuring maximum visibility and relevance where human risk is highest.

The development of 'smart signage,' though nascent, involves integrating sensors and connectivity into traditional safety identifiers. These systems, powered by machine learning algorithms, can dynamically change the message displayed (on digital screens or sophisticated e-paper) based on real-time inputs, such as the detection of a gas leak or machinery failure. This transition from passive communication to active, context-aware warnings represents a significant technological leap. However, the regulatory requirement for static, reliable backup signage means that physical safety signs will remain indispensable, with AI acting as an overlay technology to improve monitoring, compliance, and dynamic communication strategies.

The dynamics of the Safety Signs Market are shaped by powerful regulatory drivers mandating workplace safety, counterbalanced by cost-sensitivity and the challenges associated with standardizing multilingual requirements. Strict governmental enforcement and escalating penalties for non-compliance constitute the primary drivers, compelling industries across the globe to invest continuously in robust and certified safety identification systems. However, the standardization challenges, especially concerning international operations requiring adherence to multiple local and global standards (like ISO 7010), can restrain rapid adoption. Opportunities are substantial in integrating IoT technology for smart, connected signage and expanding into high-growth sectors like renewable energy infrastructure, which has specific, complex safety requirements.

The key impact forces center on regulatory pressure and technological evolution. Regulatory bodies continually update standards (e.g., GHS for chemical labeling), requiring companies to frequently update and replace existing signage inventories, ensuring a baseline demand stream. Technological forces, including advancements in durable materials (UV resistance, enhanced photoluminescence) and digital printing, enable faster customization and higher quality products, driving product differentiation among manufacturers. Furthermore, the macroeconomic force of increasing urbanization and the resulting expansion of public infrastructure projects (transportation hubs, residential complexes) mandates comprehensive public safety signage, providing broad market resilience.

The market also faces restraining impact forces related to potential user complacency or misinterpretation of signage, necessitating ongoing education and clear graphical standards. Additionally, smaller businesses often view safety signage as a necessary expenditure rather than a preventative investment, leading to price sensitivity and preference for lower-cost, potentially non-compliant, alternatives. The critical balance between regulatory stringency (driving demand) and cost-optimization (restraining premium material adoption) defines the competitive landscape and market growth trajectory, making compliance consultation services an increasingly vital component of the overall market offering.

The Safety Signs Market is extensively segmented based on the function of the sign (product type), the material used for manufacturing, the specific industry requiring the signs (end-use), and the method through which the product is distributed. Analyzing these segments provides strategic insights into demand patterns, technological preferences, and the major revenue streams within the industry. The diversity of safety requirements across sectors, ranging from complex chemical warning labels in pharmaceutical plants to large-scale traffic management signs in construction sites, necessitates this detailed segmentation approach, ensuring tailored product development and targeted marketing strategies by vendors.

The value chain for the Safety Signs Market begins with upstream activities involving the sourcing and processing of raw materials. This stage is crucial and focuses on acquiring specialized substrates such as high-grade aluminum, industrial-strength polymers (vinyl, acrylic), and specialized chemicals for photoluminescent and retroreflective coatings. Manufacturers must ensure that these materials meet stringent performance criteria regarding durability, UV resistance, and adherence to required safety specifications, often involving specialized suppliers that provide compliant inks and adhesives necessary for regulatory adherence.

The core manufacturing process involves high-precision digital printing, screen printing, or engraving, followed by lamination and finishing to enhance weather and chemical resistance. This stage adds significant value through compliance certification (e.g., ISO, ANSI, OSHA standards) and customization capabilities, allowing manufacturers to cater to specific client needs such as unique pictograms or language requirements. Distribution forms the midstream component, which often relies on a mix of direct sales channels, particularly for large industrial clients requiring consultation and installation services, and a robust network of industrial safety equipment distributors and wholesalers who maintain regional inventory.

Downstream activities focus on the end-user deployment and ongoing replacement cycle. The complexity of the installation environment (e.g., extreme temperatures, corrosive atmospheres) influences the choice of sign material and mounting hardware. Direct engagement with large end-users (e.g., major construction firms or petrochemical companies) allows for large volume, customized orders. Indirect channels, primarily E-commerce platforms and specialized online safety stores, are increasingly important for small to medium-sized enterprises (SMEs) seeking quick, standardized purchases, optimizing accessibility and reducing logistical overhead for vendors in this crucial final stage of the value chain.

Potential customers for safety signs are widespread across nearly every economic sector, driven universally by the need for regulatory compliance and operational safety. The primary end-users are large organizations operating in high-hazard environments, including multi-site industrial manufacturers, large-scale construction and infrastructure development companies, and energy producers (oil, gas, and renewable). These entities require bulk orders of standardized, durable, and highly visible signs for production floors, construction sites, pipelines, and equipment warnings, often seeking vendors capable of providing full compliance audits and inventory management.

A second major customer segment includes institutional and public service sectors such as healthcare facilities (hospitals, clinics), educational institutions (universities, schools), and transportation authorities (airports, railway systems, ports). These customers prioritize emergency and wayfinding signage, particularly those utilizing photoluminescent technology for critical egress routes. Demand here is characterized by the need for aesthetic yet compliant solutions suitable for high-traffic public areas, emphasizing non-toxic materials and long-term durability in indoor environments.

Finally, the growing segment of Small and Medium-sized Enterprises (SMEs) and independent commercial facilities (retail stores, offices) forms a crucial customer base, typically procuring standardized safety signs through distributors or online channels. Although their individual order volumes are smaller, the collective volume is significant. This group often seeks cost-effective, readily available solutions for basic safety requirements, fire extinguisher locations, and general warnings, making online retail channels highly relevant for market penetration.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 1,250.5 Million |

| Market Forecast in 2033 | USD 1,845.2 Million |

| Growth Rate | 5.75% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | 3M Company, Brady Corporation, Accuform, Seton, National Marker Company, Clarion Safety Systems, MSA Safety, Graphic Products, Lem Products, Custom Safety Products, Almetek Industries, Sign Manufacturing, Jalite PLC, D&G Signs, Safety Sign UK, ZING Green Products, Northern Safety & Industrial, Safetysigns4less, VOSS SIGNS, Signarama |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape in the Safety Signs Market is increasingly driven by material science innovation and digital manufacturing techniques, aimed at maximizing visibility, durability, and compliance. Digital printing technologies, particularly large-format UV inkjet printing, have revolutionized the industry by enabling high-resolution graphics, vivid colors that strictly adhere to safety standards (e.g., RAL color codes), and rapid customization capabilities. This shift minimizes setup time for unique or low-volume orders, supporting compliance with complex GHS and multi-language requirements. Furthermore, materials development focuses heavily on improving the longevity of signs in harsh industrial environments, utilizing advanced anti-graffiti coatings and substrates resistant to extreme temperatures and corrosive chemicals.

A major area of technological focus is enhanced passive safety features, specifically photoluminescence and retroreflection. Photoluminescent materials—which absorb ambient light and emit a glow in darkness—are critical for emergency egress systems, replacing older, less effective methods. Modern photoluminescent signs offer significantly longer glowing duration and higher intensity (luminance) than previous generations, meeting stringent requirements for critical life safety applications. Similarly, highly reflective sheeting is essential for roadway and construction signs, utilizing microprismatic technology to maximize light return to the source, crucial for visibility during nighttime operations.

The emerging technological frontier involves the integration of connectivity and smart components, moving the market toward the realm of IoT safety solutions. This includes battery-powered or solar-charged LED-enhanced signs that flash warnings under specific conditions, and signs embedded with RFID or NFC tags. These tags allow maintenance personnel to quickly scan and track the inspection, installation date, and compliance status of the physical sign using a mobile device, streamlining auditing processes and ensuring proactive replacement when signs become degraded or obsolete. While full digital signage adoption is slow in high-risk areas due to power dependency, these hybrid solutions represent the cutting edge of safety communication technology.

Regional dynamics within the Safety Signs Market are strongly correlated with local regulatory frameworks, industrial activity levels, and governmental investment in public infrastructure. The following highlights detail the market relevance and primary drivers for key geographical areas.

The primary growth driver is the ongoing global enforcement of stringent occupational safety regulations (like OSHA and ISO 7010). Regulatory mandates require businesses to maintain up-to-date, compliant signage, fueling consistent replacement and new installation demand, particularly in rapidly industrializing regions and large-scale construction projects.

Photoluminescent materials offer superior performance in low-light or power-failure emergencies. These signs absorb and store ambient light, emitting a visible glow in darkness for extended periods, making them essential for marking critical egress routes, firefighting equipment, and mandatory safety exits.

Technology primarily impacts the market through improved durability, visibility, and compliance tracking. Advancements include high-resolution digital printing for complex graphics, specialized coatings for chemical resistance, and the integration of RFID/NFC tags for streamlined compliance auditing and asset management, enhancing the effectiveness of static signs.

The Manufacturing sector (including heavy industry and automotive) and the Construction industry are the largest consumers. These sectors require extensive signage for hazard warnings, machine operation instructions, personal protective equipment (PPE) mandates, and site safety management due to the inherent risks associated with their operations.

While North America currently holds the largest market share, the Asia Pacific (APAC) region is projected to exhibit the highest CAGR during the forecast period. Rapid industrialization, substantial infrastructure investment, and the increasing adoption of international safety standards in APAC are converging to create the largest potential growth trajectory.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.