ID : MRU_ 435477 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

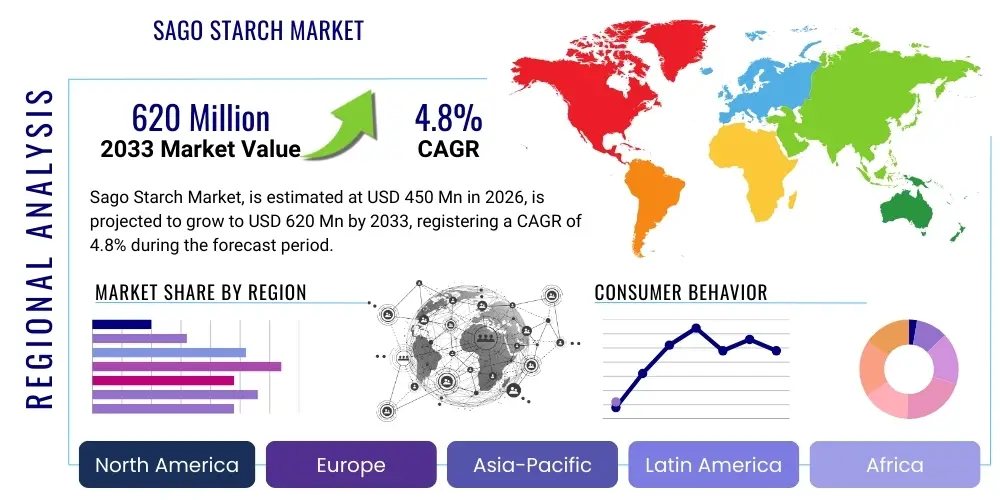

The Sago Starch Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2026 and 2033. The market is estimated at USD 450 Million in 2026 and is projected to reach USD 620 Million by the end of the forecast period in 2033.

Sago starch, derived from the pith of various tropical palm stems, primarily the Metroxylon sagu palm, is a versatile carbohydrate utilized globally across numerous industrial and food applications. As a pure carbohydrate source, it exhibits excellent thickening, binding, and gelling properties, making it an indispensable ingredient in processed foods, including noodles, puddings, baked goods, and specialty snacks. Its natural origin and relative cost-effectiveness compared to alternative starches, such as potato or corn starch, significantly contribute to its expanding market footprint, particularly in regions with high domestic production and processing capabilities.

The product is highly valued for its unique granular structure and ability to form transparent, stable gels, characteristics that are critical in the manufacture of high-quality adhesives, textiles, and bioplastics. Major applications span the food and beverage industry, where it serves as a stabilizer and texturizer; the pharmaceutical sector, where it is used as a binder and disintegrant; and the industrial sector, notably in paper manufacturing and textile sizing. The increasing consumer preference for natural, gluten-free, and plant-derived ingredients further amplifies the demand for sago starch, positioning it favorably against synthetic alternatives and conventional grain-based starches.

Key driving factors propelling market growth include rapid industrialization in Southeast Asia, where sago palms are abundant, coupled with advancements in starch modification technologies that enhance its functional attributes for specific high-performance industrial uses. Furthermore, the rising global consumption of processed and convenience foods, particularly in emerging economies, directly translates into increased requirement for stabilizing and thickening agents like sago starch. The transition toward sustainable and biodegradable materials also opens new avenues for sago starch derivatives in the packaging and biofuels markets, solidifying its role as a strategically important natural resource.

The Sago Starch Market is characterized by robust expansion driven primarily by the escalating demand for natural food additives and industrial binders, coupled with favorable government initiatives supporting sustainable agriculture in major producing regions like Southeast Asia. Business trends indicate a strong focus on optimizing supply chain logistics and investing in advanced processing technologies to yield high-quality modified starches tailored for high-end applications, particularly in pharmaceuticals and advanced food texturization. Strategic collaborations between primary producers and international food conglomerates are becoming common, aimed at standardizing quality metrics and securing consistent supply volumes to meet fluctuating global demand profiles. Furthermore, the market exhibits a clear pivot towards value-added products, moving beyond commodity status to specialized ingredients.

Regionally, the Asia Pacific (APAC) dominates the global market, accounting for the largest share in both production and consumption, mainly led by Indonesia and Malaysia—the world's primary sago palm cultivators. These nations benefit from expansive cultivation areas and established domestic processing infrastructure. However, North America and Europe are demonstrating the fastest growth trajectories, fueled by the rising adoption of sago starch as a gluten-free and allergen-friendly substitute in the sophisticated Western food industries, especially within the clean label movement. This growth is supported by increasing import activities and strategic distribution agreements ensuring timely supply to these lucrative consumer markets. Meanwhile, Latin America and the Middle East and Africa (MEA) are emerging as crucial consumption hubs for industrial applications, leveraging sago starch in textile and paper production.

Segment trends reveal that the food and beverage application segment remains the largest revenue generator, leveraging the starch’s exceptional textural properties in various culinary preparations. Within the product segment, modified sago starch is anticipated to register the highest Compound Annual Growth Rate (CAGR). This acceleration is attributed to the enhanced functional capabilities of modified variants—such as increased stability, solubility, and resistance to high temperatures—making them ideal for complex industrial processes. Packaging, driven by the shift towards biodegradable films and sustainable materials, represents another rapidly growing segment, underscoring the shift in consumption patterns favoring environmentally conscious inputs.

Common user questions regarding AI's impact on the Sago Starch Market frequently revolve around optimizing palm yields, improving processing efficiency, and forecasting volatile raw material prices. Users are primarily concerned about how machine learning can be deployed to predict disease outbreaks in sago plantations, automate quality control during starch extraction, and refine complex supply chain logistics between remote farms and large processing hubs. The consensus expectation is that AI will primarily serve to stabilize production costs, enhance ingredient traceability, and accelerate the development of novel sago starch derivatives through predictive modeling of chemical interactions, ensuring the industry maintains competitiveness against other major starch sources.

The market trajectory for sago starch is fundamentally shaped by a complex interplay of growth drivers, structural restraints, emerging opportunities, and competitive impact forces. The primary drivers stem from the global increase in demand for clean label food ingredients and the versatility of sago starch in providing gluten-free alternatives, which are crucial factors in the modern consumer packaged goods landscape. Coupled with this is the robust, institutional support from governments in key producing nations that view sago cultivation as an economically viable, sustainable land-use practice, fostering continued investment in large-scale cultivation and processing infrastructure. However, the market faces significant hurdles, notably the vulnerability of sago palms to climate change-induced weather variability and the logistical challenges associated with transporting bulky raw materials from often remote, tropical cultivation sites to centralized processing centers. These factors create operational complexities that challenge market stability and efficiency.

Opportunities in the sago starch sector are extensive and largely revolve around expanding its utility beyond traditional food and industrial applications. Significant potential lies in the bioplastics and biodegradable packaging industry, where sago starch’s rapid biodegradability makes it an attractive substitute for petroleum-based polymers, aligning with global sustainability mandates. Furthermore, ongoing research into high-purity pharmaceutical-grade sago starch, for use as an excipient in tablets and capsules, represents a high-value niche market that promises superior profit margins and diversification avenues for major producers. Technological advancements in enzymatic modification are also creating opportunities to tailor sago starch properties precisely for highly specialized industrial applications, enhancing its functional performance.

The impact forces influencing the market dynamics are highly concentrated around price competitiveness and the substitution threat posed by abundant alternatives like corn, tapioca, and potato starches. Sago starch must consistently maintain a competitive edge on price, or offer demonstrably superior functionality, to sustain its market share. Regulatory impact forces, particularly those relating to international food safety and labeling standards, also exert considerable pressure, compelling processors to adhere to stringent quality assurance protocols. Furthermore, environmental impact forces, specifically concerning responsible sourcing and deforestation prevention, are increasingly critical, necessitating transparent and sustainable supply chain certifications to maintain access to environmentally conscious global consumer bases, especially in developed Western markets.

The Sago Starch Market is comprehensively segmented based on its derivation, product form, application, and end-user industry, providing a granular view of market dynamics and revenue generation streams. The primary segmentation distinguishes between the two main categories of starch available: native sago starch, which is minimally processed and retains its natural structure, and modified sago starch, which undergoes chemical, physical, or enzymatic treatment to enhance specific functional attributes such as thermal stability or viscosity. Application-based segmentation highlights the versatility of the product, with the food and beverage sector dominating consumption, followed closely by robust industrial applications like paper, textile, and adhesive manufacturing, reflecting the broad utility profile of this unique palm derivative.

Further analysis of segmentation reveals crucial insights into growth pockets. The modified starch sub-segment is poised for the most rapid expansion, driven by the increasing complexity of modern food formulations and the requirement for highly stable ingredients in automated industrial processes. Within the end-user landscape, the growing trend of utilizing sago starch in gluten-free bakery items and infant nutrition products is fueling higher demand from specialized food manufacturing units. Geographically, while Asia Pacific remains the bedrock of production and high-volume consumption, the accelerated adoption rates in North America and Europe, driven by health and wellness trends, underscore the shift towards premiumization and specialty imports in these regions.

Understanding these segments is vital for stakeholders, allowing them to tailor investment strategies towards the most lucrative product categories and end-user markets. For instance, companies focused on sustainability are increasingly targeting the packaging segment, developing sago-based bioplastics. Conversely, those focused on operational efficiency prioritize the native starch segment, capitalizing on high-volume, low-cost applications in basic industrial binding and sizing processes. This multifaceted segmentation framework provides the necessary clarity for detailed market forecasting and strategic planning.

The Sago Starch value chain commences with upstream activities centered on the cultivation and harvesting of sago palms, which are predominantly grown in tropical regions of Southeast Asia. Upstream analysis involves land preparation, sustainable palm management practices, and the labor-intensive process of felling mature palms and extracting the raw pith. Efficiency at this stage is highly dependent on climate stability, farm labor availability, and robust agricultural logistics for transporting the highly perishable sago logs to processing mills. Investments in sustainable cultivation techniques and early disease detection are crucial for maintaining the quality and volume of raw material supply, which directly influences downstream costs.

The midstream section focuses on processing, where the raw pith undergoes crushing, washing, filtration, and drying to extract the final starch product. This stage is capital-intensive, requiring specialized machinery for high-efficiency extraction and quality control measures, particularly for producing modified starches which involve additional chemical or enzymatic treatments. Major processing centers are typically located in Indonesia, Malaysia, and Papua New Guinea, benefitting from economies of scale. The quality specifications achieved during processing determine the suitability of the starch for high-value applications like pharmaceuticals or specialized food texturizing, impacting profit margins significantly.

The downstream flow involves the distribution channel, which utilizes both direct and indirect networks to reach end-users. Direct channels involve large producers supplying bulk starch directly to major industrial consumers, such as multinational food and beverage corporations or large textile mills, often secured through long-term supply contracts. Indirect distribution relies heavily on regional traders, specialized starch distributors, and global import-export agents who manage inventory, repackaging, and delivery to smaller manufacturers or regional markets. Effective cold chain management, though less critical than for fresh produce, is necessary to prevent spoilage and maintain product integrity, while seamless international logistics are vital for market penetration into North America and Europe.

Potential customers for sago starch span a diverse array of industries, primarily centering around manufacturing sectors that require high-performance, natural, and cost-effective binding, thickening, or gelling agents. The largest segment of end-users consists of food and beverage manufacturers, including major producers of instant noodles, sauces, soups, bakery mixes (especially those focusing on gluten-free lines), and confectionery items, who rely on sago starch for texture modification and stability enhancement. These customers prioritize high purity and consistent viscosity characteristics to ensure uniform product quality across mass production batches.

The industrial sector represents the next significant cohort of buyers, specifically textile manufacturers utilizing sago starch for sizing yarns to improve weaving efficiency, and paper and pulp companies that use it as a wet-end additive to enhance paper strength and stiffness. These industrial customers are price-sensitive but require large, consistent volumes of native starch. Additionally, the emerging segment of bioplastics and sustainable packaging companies represents a high-growth customer base, seeking sago starch and its derivatives as primary biodegradable polymers for manufacturing films, cutlery, and compostable packaging solutions, driven by corporate sustainability mandates.

Finally, the pharmaceutical industry and specialized chemical companies serve as high-value, albeit smaller volume, buyers. Pharmaceutical companies use sago starch as an excipient in tablet formulation, requiring extremely high purity and specific dissolution properties. Chemical manufacturers use native sago starch as a raw material for fermentation processes to produce organic acids or ethanol. For these high-specification buyers, adherence to stringent international quality certifications (like ISO and GMP standards) and guaranteed batch consistency are non-negotiable prerequisites for long-term purchasing agreements, making them critical targets for premium modified starch producers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 450 Million |

| Market Forecast in 2033 | USD 620 Million |

| Growth Rate | CAGR 4.8% |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Tate & Lyle PLC, Cargill, Incorporated, Ingredion Incorporated, PT Austindo Nusantara Jaya Tbk, Sinarmas Cepasa Ltd, Sago Starch Vietnam, Premium Sago Starch, KAO (M) Sdn Bhd, Kuralon Starch Industries, Budi Starch & Sweetener, Chemfix Technologies Sdn Bhd, Universal BioGen, BMT Food Ingredients, Eco Starches, Asia Starch. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Sago Starch Market is characterized by a drive towards higher efficiency in raw material extraction and advanced functional modification of the final product. Key technological advancements in the upstream segment focus on automated harvesting and efficient pith extraction machinery that minimizes mechanical damage and maximizes yield per log, crucial for maintaining processing cost competitiveness. Modern extraction facilities utilize advanced closed-loop water systems and energy-efficient centrifuges to improve starch separation and reduce environmental impact, moving away from traditional, less efficient manual processing methods prevalent in smaller, localized operations.

In the processing stage, the most critical technological developments lie in starch modification. These include sophisticated chemical modifications (like etherification and esterification) and advanced enzymatic modification techniques. Enzymatic methods are gaining traction due to their ability to produce clean label starches with highly customized functional properties—such as specific gelatinization temperatures or improved freeze-thaw stability—without relying on harsh chemicals. High-shear mixing and controlled drying technologies are also essential for producing uniform, high-quality modified starches required by stringent food and pharmaceutical sectors.

Furthermore, technology is being heavily integrated into quality assurance and supply chain management. Near-Infrared (NIR) spectroscopy and advanced rheometers are utilized for real-time quality monitoring, ensuring batch consistency in viscosity and purity. Digital traceability platforms utilizing blockchain technology are emerging to provide end-to-end transparency, tracking the starch from the sago palm farm to the final end-user. This adherence to digital tracking and advanced analytical technology is essential for gaining trust in developed markets that demand high transparency regarding origin and processing standards.

The Sago Starch Market exhibits profound regional variations in terms of production, consumption patterns, and growth potential, fundamentally shaping global trade flows and investment priorities. Asia Pacific (APAC) stands as the undisputed center of the market, driven by the vast native cultivation areas in Indonesia and Malaysia, which collectively account for the majority of global raw material supply and processed starch output. The robust domestic demand within APAC, fueled by high consumption of staples like noodles and the rapidly expanding processed food sector, ensures its dominance. Furthermore, continuous investment in large-scale processing infrastructure by regional giants reinforces the region’s status as a low-cost production hub for native sago starch destined for global industrial applications.

North America and Europe represent premium, high-growth consumer markets characterized by a strong emphasis on health, wellness, and clean label ingredients. While possessing negligible sago cultivation, these regions are significant importers of specialty and modified sago starches. Demand here is driven specifically by the gluten-free trend, where sago starch is favored over grain-based alternatives, and by the pharmaceutical sector’s need for high-purity excipients. The stringent regulatory environment in these regions necessitates suppliers to adhere to rigorous quality standards and possess strong traceability certifications, which often results in higher import prices but offers attractive margins for specialized starch producers.

The Middle East and Africa (MEA) and Latin America are emerging regional markets, primarily driven by industrial applications such as textile and paper manufacturing growth. In MEA, rapid infrastructure development and the increasing sophistication of local manufacturing hubs boost the need for industrial-grade binders and sizing agents. Latin America, particularly Brazil and neighboring countries, offers a dual opportunity: growing domestic demand for processed foods and potential localized processing of sago or similar palm starches as an alternative to existing local sources. Although currently smaller in volume, these regions present significant long-term growth potential due to demographic expansion and ongoing industrialization efforts.

Sago starch offers superior textural properties, acting as an excellent thickener, stabilizer, and gelling agent. It is valued for producing clear, stable gels and is highly sought after as a natural, gluten-free carbohydrate source in bakery products, instant noodles, and specialized gluten-intolerant diets, enhancing mouthfeel and product longevity.

Modified sago starch undergoes treatments (chemical, physical, or enzymatic) to enhance stability against heat, acid, and shearing, making it suitable for industrial processes requiring extreme conditions. Applications include deep-frozen foods, canned goods, specialized textile sizing, and high-performance adhesives, where native starch performance is insufficient.

Asia Pacific (APAC), specifically the countries of Indonesia and Malaysia, dominates the global production and supply of sago starch. These nations possess extensive natural sago palm cultivation areas and established, large-scale processing infrastructure, making them the primary source for global exports.

Major growth drivers include the escalating global consumer demand for gluten-free and clean label food ingredients, the versatility of sago starch in high-performance industrial applications such as bioplastics, and continuous investment in advanced starch modification technologies improving its functional utility.

The primary competitive threats to sago starch come from readily available and globally scaled starches, particularly corn starch, tapioca starch, and potato starch. These alternatives often compete aggressively on price in commodity applications, compelling sago starch producers to focus on high-value, functional specialization.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.