ID : MRU_ 433105 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

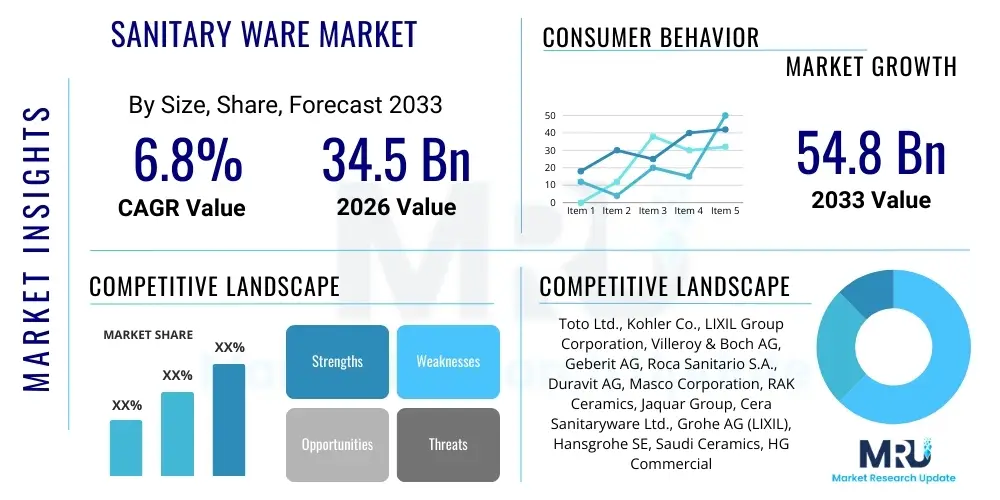

The Sanitary ware Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at USD 34.5 Billion in 2026 and is projected to reach USD 54.8 Billion by the end of the forecast period in 2033. This substantial expansion is fundamentally driven by rapid urbanization across emerging economies, coupled with increasing consumer expenditure on home renovation and infrastructure development projects globally. The shift towards smart, water-efficient, and aesthetically pleasing bathroom fixtures is contributing significantly to the valuation increase, reinforcing the market’s resilience against macroeconomic fluctuations by focusing on long-term sustainability and luxury segments.

The Sanitary ware Market encompasses products crucial for hygiene, sanitation, and aesthetic functionality in both residential and commercial spaces, primarily including wash basins, toilets, cisterns, bathtubs, and associated fittings, manufactured predominantly from ceramics, porcelain, and increasingly, composite materials. Product innovation focuses heavily on maximizing water conservation, integrating smart features like touchless operation and self-cleaning mechanisms, and optimizing ergonomic design to cater to diverse global consumer needs. These products form an essential component of the construction industry, directly impacting public health standards and modern architectural design principles across developing and developed nations alike.

Major applications of sanitary ware span across new construction projects, including high-rise residential complexes, commercial office buildings, hospitality venues (hotels and resorts), and public infrastructure (hospitals and educational institutions), as well as significant replacement and renovation activities in established structures. The increasing penetration of designer sanitary ware, offering premium aesthetics and customized finishes, is capturing the high-end market segment, while demand for durable, affordable, and easy-to-maintain ceramic products remains strong in mass housing initiatives. The integration of advanced glazing technologies ensures enhanced hygiene and longevity, driving replacement cycles based on performance improvements rather than just physical failure.

Key driving factors propelling the market include stringent government regulations mandating water efficiency standards (e.g., use of low-flow toilets and faucets), accelerating infrastructure investments, and a demographic shift towards smaller, highly functional urban living spaces where efficient use of bathroom space is critical. The growing awareness regarding personal hygiene, particularly in post-pandemic environments, has further intensified demand for high-quality, anti-microbial, and easy-to-clean sanitary fittings. Furthermore, the rising disposable income in Asia Pacific and Latin America allows consumers to transition from basic, functional products to advanced, technologically integrated sanitary solutions, supporting sustained market expansion throughout the forecast period.

The global Sanitary ware Market is characterized by robust business trends centered on sustainability, digitalization, and premiumization. Manufacturers are increasingly prioritizing eco-friendly production processes and developing products that meet rigorous global standards for water conservation, often leveraging Internet of Things (IoT) connectivity for personalized usage monitoring and fault detection. Mergers and acquisitions remain a crucial strategy for consolidating market share and gaining access to specialized material science or digital technology, ensuring that market leaders can offer integrated bathroom solutions rather than standalone products. Supply chain resilience, particularly concerning ceramic raw materials and complex electronic components for smart fixtures, is a key operational challenge being addressed through diversified sourcing and localized manufacturing hubs.

Regionally, Asia Pacific maintains its dominance, fueled by unprecedented rates of urbanization and massive government investments in smart city projects and public sanitation infrastructure, making it the primary hub for both production and consumption. North America and Europe are distinguished by their high adoption rates of smart bathroom technology and strict adherence to environmental regulations, driving innovation towards highly efficient, minimalist designs. The Middle East and Africa present significant growth opportunities, particularly in the hospitality and luxury real estate sectors, where demand for premium, custom-designed sanitary ware is surging, often influenced by European aesthetic standards and cutting-edge water management systems tailored for arid climates.

In terms of segmentation, the toilet segment (WC) dominates by volume, with significant revenue growth derived from intelligent toilet systems offering advanced features like bidet functions, heated seating, and automated flushing. Material-wise, ceramic and porcelain remain the foundational choices due to their durability and cost-effectiveness, while the fiberglass and composite materials segments are exhibiting the fastest growth, particularly in the bathtub and shower tray categories, appealing to modern design sensibilities emphasizing seamless integration and lightweight properties. The market structure is shifting from retail distribution towards stronger partnerships with architects, interior designers, and major construction contractors, emphasizing B2B channels for sustained, high-volume project procurement.

Common user inquiries regarding the impact of Artificial Intelligence (AI) on the Sanitary ware Market often revolve around how AI can enhance product functionality, improve manufacturing efficiency, and personalize the user experience. Users frequently ask about the role of predictive maintenance in smart toilets, the optimization of water usage through machine learning algorithms, and the potential for AI-driven design tools to create customizable and ergonomic fixtures. Key concerns focus on data privacy related to usage monitoring and the high initial cost barrier associated with integrating complex AI components into traditional bathroom products. Overall, consumers and industry professionals expect AI to revolutionize hygiene standards and operational efficiency, making bathrooms smarter, more sustainable, and seamlessly integrated into the broader smart home ecosystem.

AI is fundamentally transforming the manufacturing landscape through predictive quality control and autonomous system optimization. In production lines, AI vision systems can identify minute defects in ceramic glazing or molding processes far quicker and more consistently than human inspection, drastically reducing waste and improving the overall quality consistency of the final product. Furthermore, AI-powered robotics are enhancing precision in material handling and assembly, particularly for complex smart fixtures that involve integrating electronic components into ceramic bodies. This operational transformation leads to lower production costs and faster time-to-market for new designs.

On the consumer front, AI is the backbone of next-generation smart sanitary ware. Smart toilets utilize AI to monitor usage patterns, allowing for optimized flushing volumes based on actual waste detection, thus maximizing water savings. Personalized wellness features, such as basic bio-feedback monitoring (e.g., temperature, weight variation) integrated into the toilet seat or mirror, utilize AI algorithms to process and present actionable health insights to the user via associated mobile applications. This move transforms sanitary ware from purely functional items into proactive health and lifestyle tools, justifying the premium price points associated with AI-enabled products.

The Sanitary ware Market dynamic is defined by a complex interplay of Drivers, Restraints, and Opportunities (DRO), significantly influenced by governmental policies and consumer trends, which collectively act as pivotal impact forces. The primary drivers include aggressive global construction activities, particularly housing and commercial development in Asia Pacific and the Middle East, coupled with the increasing consumer expectation for high-tech, water-saving fixtures driven by sustainability consciousness. Simultaneously, the market is restrained by the volatile pricing of raw materials, such as ceramic clay and kaolin, reliance on energy-intensive firing processes which increase operational costs, and the inherent durability of existing sanitary products, which extends replacement cycles. However, substantial opportunities arise from the rapid adoption of IoT and smart home technology, enabling premium pricing for sophisticated, connected bathroom solutions, and the untapped potential of retrofitting older buildings with modern, water-efficient systems.

Impact forces stemming from technological advancement exert significant pressure, compelling manufacturers to continuously innovate. The shift from traditional gravity-flush toilets to pressure-assisted or vacuum systems, coupled with touchless activation mechanisms powered by motion sensors, requires substantial investment in R&D but results in higher consumer value propositions. Furthermore, regulatory forces, such as the EPA’s WaterSense program in the U.S. or similar water conservation mandates across Europe and Australia, directly influence product design specifications, pushing the market towards ultra-low flow rates and higher performance standards. Economic forces, including fluctuating interest rates affecting construction financing and general consumer confidence, dictate the volume of large-scale infrastructure projects and subsequent demand for mid-to-high range sanitary ware products, stabilizing the market overall through balanced demand from both new builds and renovation cycles.

The Sanitary ware Market is comprehensively segmented based on product type, material, application (end-user), and distribution channel, providing a granular view of market dynamics and consumer preferences across different tiers. Product segmentation highlights the dominance of basic yet essential items like toilets and wash basins, while showcasing the rapid growth of specialized products such as cisterns, pedestals, and increasingly complex smart systems. Material segmentation is vital, reflecting both cost considerations and aesthetic requirements, with the traditional ceramics segment holding the largest share, although innovative composite materials are gaining traction in the luxury bath fixture market due to design flexibility and reduced weight. Understanding these segmentations is critical for manufacturers tailoring their product portfolios to specific regional regulations and evolving consumer tastes, especially the demand for integrated bathroom concepts.

The value chain for the Sanitary ware Market is characterized by a high degree of integration between raw material extraction and the final distribution to end-users, requiring meticulous coordination to manage costs and quality. Upstream analysis highlights the critical role of mining and processing of essential raw materials such, as specialized clays (kaolin, ball clay), feldspar, and silica sand, which account for a significant portion of the initial production cost and require consistent quality control to prevent firing defects. The energy-intensive nature of firing processes in kilns necessitates strategic energy procurement and investment in efficient technologies to maintain competitive pricing, making raw material sourcing and primary processing a bottleneck for smaller manufacturers.

Midstream activities involve core manufacturing, including slurry preparation, molding (casting), glazing application, and the high-temperature firing of products. This stage is where technological differentiators such as pressure casting, robotic glazing, and advanced firing profiles (fast-firing techniques) offer substantial competitive advantages, improving product density, reducing water absorption, and enhancing surface finish durability. For smart sanitary ware, the midstream also includes the integration of electronic components, sensors, and actuators, often sourced from specialized electronics OEMs, requiring strict quality assurance protocols to ensure compatibility and long-term performance in humid environments.

Downstream analysis focuses on distribution channels, which are segmented into direct sales to large construction companies and indirect sales through a network of wholesalers, specialized plumbing distributors, and large retail showrooms. Direct channels allow manufacturers greater control over branding and pricing in major construction projects, while indirect channels provide wider geographical reach and cater to the renovation market and smaller contractors. E-commerce is rapidly gaining prominence, particularly for replacement parts and easily shippable accessories, requiring manufacturers to optimize packaging and logistics for damage minimization.

Distribution complexity varies by product type; high-volume, standardized ceramic pieces often utilize mass distribution methods, whereas bespoke or luxury items rely heavily on high-touch showroom experiences and specialized architectural design partnerships. The overall efficiency of the value chain is determined by minimizing material waste during production and optimizing logistics costs, as sanitary ware products are typically bulky and prone to breakage, necessitating specialized handling and warehousing solutions.

Potential customers for the Sanitary ware Market are broadly categorized into three major segments: the residential sector, driven by new housing starts and home improvement projects; the commercial sector, focused on hospitality, office, and retail development; and the institutional sector, encompassing government-funded projects like healthcare facilities and educational campuses. Residential buyers are highly sensitive to aesthetics, brand reputation, water efficiency ratings, and price, with growing demand for premium, comfortable fixtures in newly affluent urban centers. This segment often purchases through retail channels and relies on the advice of plumbers and interior designers for brand selection and installation guidance.

The commercial segment, particularly the hotel and high-end office development industry, represents a vital customer base characterized by demand for highly durable, low-maintenance, and aesthetically consistent products suitable for high-traffic use. These customers prioritize bulk purchasing efficiency, longevity, and adherence to specific design specifications laid out by architectural firms. The increasing emphasis on sustainability certification (e.g., LEED standards) makes water efficiency an absolute prerequisite for commercial buyers, often leading them to choose high-performance smart or sensor-activated fixtures to minimize operational costs and enhance user experience.

Institutional customers, including public hospitals and educational bodies, prioritize cost-effectiveness, extreme durability, anti-vandalism features, and easy compliance with stringent public health and accessibility standards (e.g., ADA compliance). Purchasing decisions in this segment are often driven by centralized procurement policies, focusing on long-term value and reliability rather than luxury aesthetics, typically procuring through large-scale tenders and specialized B2G distributors. The need for specialized infection control features, such as touchless fixtures and specialized materials, is also a growing requirement in the healthcare subset of this customer group.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 34.5 Billion |

| Market Forecast in 2033 | USD 54.8 Billion |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Toto Ltd., Kohler Co., LIXIL Group Corporation, Villeroy & Boch AG, Geberit AG, Roca Sanitario S.A., Duravit AG, Masco Corporation, RAK Ceramics, Jaquar Group, Cera Sanitaryware Ltd., Grohe AG (LIXIL), Hansgrohe SE, Saudi Ceramics, HG Commercial Ptd Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The Sanitary ware Market is undergoing a rapid technological evolution, moving beyond basic ceramic production towards sophisticated integration of sensor technology, advanced materials, and connectivity features, collectively forming the smart bathroom ecosystem. Key technological advancements are centered on optimizing water conservation, enhancing surface hygiene, and improving the operational convenience of the fixtures. For instance, the use of specialized anti-microbial glazes and hydrophobic nano-coatings is a foundational technological development ensuring easier cleaning and significantly reducing the proliferation of bacteria and molds, addressing mounting public health concerns and aligning with sustainability goals by minimizing the need for harsh chemical cleaners.

In the functional realm, technological integration is dominated by the development and refinement of smart toilets and touchless fixtures. Smart toilets incorporate technologies such as automated flushing mechanisms, integrated bidet functionality with temperature control, heated seats, and sophisticated deodorizing systems, all managed through digital interfaces or remote controls. Touchless technology, utilizing radar or infrared sensors for faucets and flushes, is witnessing accelerated adoption in both commercial and high-end residential settings, driven primarily by the heightened focus on minimizing physical contact and cross-contamination in shared spaces. These systems are becoming increasingly efficient, reducing false activations while maintaining reliability under varying environmental conditions.

Furthermore, innovations in manufacturing technology, such as robotics in high-pressure casting and automated glazing lines, are crucial for maintaining the stringent quality standards required for modern thin-edge and complex geometric designs favored by contemporary architecture. Digitalization extends to the consumer experience through augmented reality (AR) tools allowing customers to visualize fixtures in their own bathroom spaces before purchase, reducing returns and enhancing customer satisfaction. Overall, the market's technological landscape is characterized by the convergence of material science, fluid dynamics engineering, and advanced electronics, transforming traditional pottery into highly functional, connected health appliances.

The global Sanitary ware Market exhibits significant regional variations in terms of consumption patterns, manufacturing capabilities, and regulatory environments, dictating localized growth trajectories. Asia Pacific stands out as the dominant and fastest-growing region, primarily due to immense infrastructural development, massive government investment in affordable housing, and the rapid expansion of middle-class populations in countries like China, India, and Southeast Asian nations. These countries are not only massive consumers but also major global production hubs, benefiting from lower operational costs and established supply chains, although they are increasingly pressured to adopt stricter environmental standards for wastewater management and energy efficiency in production.

North America and Europe represent mature markets characterized by replacement demand, renovation activities, and high penetration of smart and luxury sanitary ware products. Growth in these regions is driven less by sheer volume and more by value derived from technological upgrades, such as premium smart toilets, high-efficiency flushing systems (HETs), and designer fixtures emphasizing sustainable manufacturing practices and minimalist aesthetics. European markets, led by Germany, France, and the UK, enforce some of the world's strictest water usage regulations, forcing continuous innovation in ultra-low-flow technology and material traceability.

The Middle East and Africa (MEA) region, particularly the GCC countries, shows robust growth, largely fueled by mega-projects in hospitality, tourism, and luxury residential real estate, demanding high-end, imported sanitary ware that meets global luxury standards. Water scarcity challenges in the MEA region make water-saving technology a critical priority, accelerating the adoption of technologically superior fixtures despite the higher cost. Latin America, meanwhile, presents a high-potential but fragmented market, where economic volatility can impact major construction cycles, yet underlying demand for improved sanitation infrastructure offers long-term growth prospects, particularly in Brazil and Mexico.

The primary factor driving market growth is the accelerating global rate of urbanization, particularly in Asia Pacific, coupled with substantial government and private sector investments in residential and commercial infrastructure projects. Additionally, rising consumer demand for water-efficient and aesthetically advanced sanitary fixtures significantly contributes to market value expansion.

Environmental regulations, particularly mandates concerning water conservation (such as HET standards), are profoundly impacting product design. Manufacturers are compelled to innovate ultra-low-flow toilets, water-saving faucets, and intelligent flushing systems to ensure regulatory compliance, thereby accelerating the shift toward highly efficient and sustainable sanitary ware solutions across developed markets.

Technology drives premiumization by integrating features like IoT connectivity, AI-powered usage optimization, touchless operation, and advanced hygienic functions (e.g., automated cleaning, anti-microbial coatings). These sophisticated additions enhance user comfort, health, and operational efficiency, allowing manufacturers to command higher price points for smart sanitary ware products.

While ceramic and porcelain remain dominant by volume, the composites and fiberglass segment, particularly for bathtubs, shower trays, and customized counter surfaces, is anticipated to show the highest growth rate. This growth is fueled by design flexibility, lighter weight, and improved durability offered by composite materials, aligning with modern architectural trends.

Key challenges include managing the high volatility and increasing cost of essential raw materials (clays and minerals), mitigating the substantial energy consumption required for firing processes, and addressing logistical complexities arising from the bulkiness and fragility of finished goods, all of which pressure profit margins and necessitate constant operational efficiency improvements.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.