ID : MRU_ 435740 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

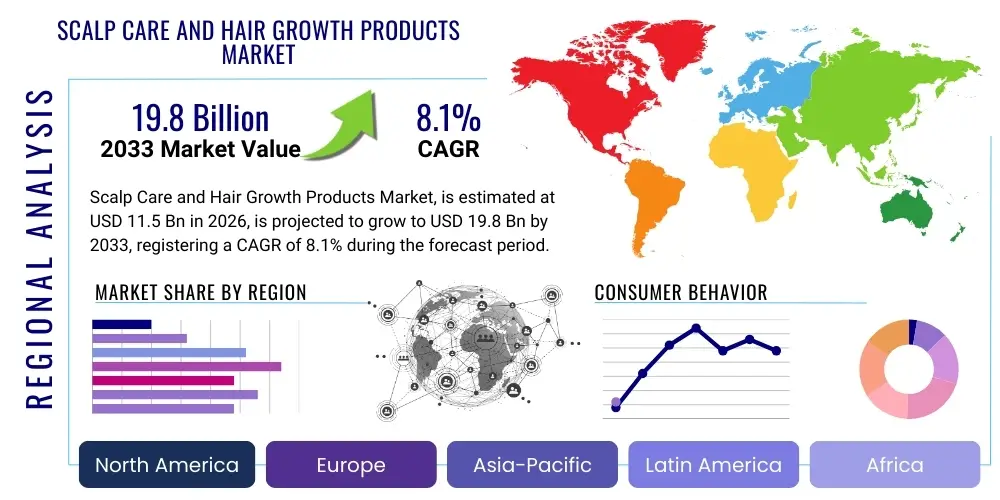

The Scalp Care and Hair Growth Products Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.1% between 2026 and 2033. The market is estimated at $11.5 Billion USD in 2026 and is projected to reach $19.8 Billion USD by the end of the forecast period in 2033.

The Scalp Care and Hair Growth Products Market encompasses a wide array of specialized cosmetic and dermatological preparations designed to maintain scalp health, address common conditions such as dandruff, inflammation, and excessive oiliness, and stimulate hair follicle activity to promote density and growth. These products range from therapeutic shampoos and conditioners to highly concentrated serums, oils, and topical treatments containing active ingredients like minoxidil, peptides, biotin, and various botanical extracts. The growing consumer awareness regarding the crucial role of the scalp in overall hair vitality, coupled with rising instances of stress-induced hair loss (telogen effluvium) and pattern baldness, has significantly fueled product innovation and market expansion across global regions. The industry is currently characterized by a strong shift toward clinical efficacy validation and natural or clean formulations, appealing to a consumer base that prioritizes both results and safety.

Major applications of these products span preventive maintenance, addressing specific chronic scalp disorders, and intensive treatment protocols for hair thinning and loss. Preventive care involves maintaining a balanced scalp microbiome and pH level, typically through specialized cleansers and exfoliating treatments. Therapeutic applications target conditions such as seborrheic dermatitis, psoriasis, and folliculitis, often requiring products formulated with antifungal or anti-inflammatory agents. The segment focused on hair growth is propelled by demographic shifts, including an aging population and younger consumers experiencing premature hair thinning, seeking solutions that offer visible and sustainable improvements in hair density and texture. The market benefits from substantial investment in R&D, leading to the introduction of advanced delivery systems such as microencapsulation and liposomal technology, which enhance the bioavailability and efficacy of active ingredients directly at the follicular unit.

Key benefits derived from these products include improved hair quality, reduced hair fall, mitigation of scalp discomfort (itching, redness), and the restoration of a healthy environment for optimal hair growth cycle function. Driving factors primarily include the increasing aesthetic consciousness globally, aggressive marketing campaigns emphasizing 'scalp-as-skin' care routines, and the accessibility of clinically backed over-the-counter (OTC) treatments. Furthermore, the rising influence of digital platforms and social media in normalizing discussions about hair loss and promoting sophisticated beauty routines contributes substantially to the sustained demand for premium and specialized scalp care products. Regulatory frameworks, particularly in advanced economies, while ensuring product safety, also push manufacturers towards greater transparency regarding ingredient sourcing and scientific substantiation of efficacy claims, thereby bolstering consumer trust in the market offerings.

The Scalp Care and Hair Growth Products Market exhibits robust growth driven by significant shifts in consumer preferences toward specialized, evidence-based cosmetic dermatology and holistic wellness approaches. Business trends indicate a strong move towards premiumization, with consumers willing to invest in high-cost, efficacy-proven serums and medical-grade treatments, often integrating professional salon services with at-home maintenance regimes. Key industry players are focusing on mergers, acquisitions, and strategic partnerships to acquire niche clean beauty brands or gain access to proprietary ingredient technologies, especially those centered around microbiome balancing and stem cell research. Supply chain optimization is also critical, emphasizing sustainable sourcing of raw materials and eco-friendly packaging, aligning with increasing environmental, social, and governance (ESG) considerations affecting consumer purchasing decisions globally. This dynamic competitive landscape necessitates continuous product innovation to secure market share and brand loyalty among diverse consumer demographics.

Regional trends highlight North America and Europe as dominant revenue generators, characterized by high disposable incomes, strong awareness of advanced beauty and wellness trends, and a well-established infrastructure for distribution through pharmacies, luxury retailers, and specialized dermatology clinics. However, the Asia Pacific (APAC) region is projected to register the highest Compound Annual Growth Rate (CAGR) during the forecast period, primarily fueled by rising urbanization, the expanding middle class in countries like China and India, and a deep cultural emphasis on hair appearance and traditional herbal remedies. Manufacturers are tailoring product lines to address specific Asian hair and scalp characteristics, often integrating local botanical ingredients while leveraging mass-market distribution channels to capitalize on the region's vast consumer base. Latin America and the Middle East & Africa (MEA) present nascent but rapidly developing markets, showing significant potential particularly in the premium and clinical segments due to increasing Western influence and accessible e-commerce platforms.

Segmentation trends reveal that the natural/herbal ingredient segment is experiencing rapid acceleration, driven by heightened concerns regarding synthetic chemicals and a desire for 'clean' labels. Within product types, specialized hair growth serums and oils, often utilizing concentrated peptide complexes and plant-derived extracts, command high value due to their perceived efficacy and targeted action, overshadowing traditional shampoos and conditioners in terms of market value growth. Distribution channels are witnessing a substantial shift toward online platforms, enabling direct-to-consumer (DTC) models which offer personalized consultation and subscription services, thereby enhancing customer retention and data collection for targeted marketing strategies. The male segment, traditionally underserved, is increasingly acknowledged through dedicated product lines addressing male pattern baldness and scalp sensitivity, contributing significantly to overall market volume expansion.

Common user questions regarding AI's impact on the Scalp Care and Hair Growth Products Market revolve heavily around personalized treatment efficacy, the accuracy of digital scalp diagnosis, and the future of consumer engagement. Users frequently inquire about how AI algorithms can analyze individual biometric data (e.g., genetic predisposition, lifestyle factors, existing scalp conditions captured via smartphone imaging or diagnostic tools) to recommend the most effective product combinations and regimens, thus moving beyond generic formulations. Key concerns often focus on data privacy when sharing sensitive health and image data, and the reliability of AI-driven diagnostics compared to professional dermatological assessments. Expectations are high regarding AI's potential to revolutionize R&D by simulating ingredient interactions and predicting product performance, leading to faster, more effective, and potentially less expensive product development cycles. The integration of AI into customer service, through virtual scalp analysts and intelligent recommendation engines, is also a highly anticipated area of development.

AI is fundamentally transforming the R&D process in scalp care by enabling massive data aggregation and analysis, allowing researchers to correlate specific genetic markers or environmental exposures with different types of hair loss and scalp dysfunctions. This predictive capability significantly reduces the time and cost associated with identifying novel, highly targeted active compounds. For instance, machine learning models can sift through vast libraries of peptides and botanical extracts to pinpoint candidates most likely to modulate key biological pathways related to hair follicle regeneration or inflammation reduction. This shift towards data-driven formulation allows companies to bring clinically superior, personalized products to market faster, moving away from conventional trial-and-error methodologies.

The primary commercial impact lies in enhanced personalization and consumer diagnostics. AI-powered diagnostic apps utilize image recognition and deep learning to analyze photos of the scalp, identifying issues like density loss, follicle miniaturization, or scaling, and recommending specific product SKUs from a brand's portfolio. Furthermore, AI optimizes the consumer journey through highly sophisticated A/B testing of marketing content, predictive inventory management based on regional trend analysis, and the implementation of intelligent chatbots that offer detailed product usage instructions and troubleshoot common user issues, thereby significantly improving customer satisfaction and loyalty in a highly saturated market. This technological integration is crucial for maintaining competitive edge in the evolving digital commerce ecosystem.

The dynamics of the Scalp Care and Hair Growth Products Market are shaped by a complex interplay of Drivers, Restraints, and Opportunities (DRO), collectively forming the Impact Forces that dictate market direction and growth trajectory. Key drivers include the global aging population, which increases the prevalence of age-related hair thinning, and the simultaneous rise in psychological and environmental stressors leading to premature hair loss among younger demographics. Significant restraints revolve around the high cost associated with clinically proven ingredients and advanced formulations, which limit accessibility in price-sensitive markets, alongside consumer skepticism stemming from historical instances of ineffective or poorly regulated products. Opportunities are abundant, particularly in the realm of biotech advancements, such as stem cell technology and gene therapy approaches to hair regeneration, coupled with the unmet demand for highly efficacious, non-pharmaceutical, and natural topical solutions. These forces exert high impact, pushing manufacturers toward continuous scientific validation and transparent labeling practices to sustain consumer trust and navigate regulatory hurdles.

The primary drivers powering market expansion are multifaceted. The pervasive influence of social media and beauty influencers has dramatically raised awareness regarding scalp health as a fundamental component of cosmetic routines, moving it from a niche concern to a mainstream wellness category. This trend encourages consumers to adopt multi-step scalp care routines utilizing multiple specialized products (e.g., exfoliators, pre-wash treatments, tonics). Furthermore, regulatory approval of over-the-counter drugs like minoxidil, alongside the strong acceptance of FDA-approved low-level laser therapy (LLLT) devices which complement topical treatments, expands the options available to consumers, solidifying market growth. The increasing prevalence of lifestyle-related conditions such as stress, poor nutrition, and pollution exposure further exacerbates hair loss issues, thereby creating an inherent, expanding demand base for protective and reparative scalp solutions.

Despite significant growth potential, the market faces notable restraints. The development cycle for innovative, clinically proven ingredients is long and capital-intensive, leading to high retail prices that can deter mass market adoption. Regulatory stringency, particularly in jurisdictions like the EU and the US, imposes strict requirements on efficacy claims and ingredient safety, demanding extensive clinical trials which increases R&D expenditure and time-to-market. Moreover, the market is frequently challenged by the proliferation of counterfeit products and misleading marketing, which erodes consumer confidence in the category overall. Successfully capitalizing on opportunities requires navigating these restraints through robust scientific validation, strategic intellectual property protection, and leveraging digital technologies to educate consumers effectively about the science and expected outcomes associated with premium scalp care formulations.

The Scalp Care and Hair Growth Products Market is highly segmented based on product type, ingredient type, distribution channel, and end-user, reflecting the diverse nature of scalp health concerns and consumer purchasing behavior globally. This granular segmentation allows manufacturers to tailor their marketing strategies and product portfolios to specific demographic and therapeutic needs, maximizing market penetration. The complexity arises from the overlap between general cosmetic care and specialized therapeutic treatment, requiring clear categorization to ensure consumers select the appropriate product for their specific condition, ranging from simple dryness to advanced pattern hair loss. Understanding these segments is crucial for identifying high-growth pockets and adapting distribution strategies effectively.

Segmentation by Product Type is vital, as it differentiates high-volume, lower-cost items (like shampoos and conditioners) from high-margin, specialized treatment products (like serums, oils, and masks). Treatment serums and tonics, which typically contain the highest concentration of active growth factors or proprietary peptides, are driving revenue growth, especially in the premium and clinical segments. Meanwhile, Ingredient Type segmentation highlights the massive shift toward natural, organic, and plant-derived extracts (e.g., caffeine, rosemary oil, essential fatty acids), contrasting with chemically synthesized ingredients (like Minoxidil or Finasteride derivatives). This divergence is driven by consumer desire for 'clean beauty' solutions and concerns over long-term chemical side effects.

The End-User split between Male and Female segments is increasingly significant. While historically women were the primary target, dedicated lines for men addressing male pattern baldness, sensitivity, and oil control are emerging as rapid growth categories. Distribution Channel analysis confirms the dominance of Offline sales (pharmacies, professional salons, department stores) for established brands and prescription-strength products, yet Online channels (e-commerce sites, brand websites, and specialized beauty platforms) are showing superior growth rates, facilitating geographic reach and personalized digital marketing campaigns. This robust segmentation framework is indispensable for accurate market forecasting and strategic investment planning.

The value chain for the Scalp Care and Hair Growth Products Market commences with raw material sourcing and research and development (R&D), where significant scientific investment is made to discover and validate active ingredients, ranging from specialized plant extracts and peptides to pharmaceutical-grade compounds. The upstream analysis focuses heavily on securing sustainable, high-quality, and traceable ingredients, crucial for maintaining product efficacy and aligning with 'clean beauty' claims. Key activities in this stage include clinical testing, formulation refinement, and ensuring compliance with international cosmetic ingredient regulations (e.g., INCI labeling). Strategic alliances with biotech companies and specialized ingredient suppliers are critical for maintaining a competitive advantage in the upstream segment, ensuring a consistent supply of novel, patented actives that deliver verifiable results to the end-user.

The midstream involves manufacturing, packaging, and quality control. Scalp care products, particularly high-efficacy serums, often require specialized, sterile manufacturing environments to maintain the stability and potency of sensitive active ingredients. Packaging plays a dual role: protection of the formulation (e.g., UV-protected glass vials for unstable vitamins) and consumer engagement, with premium and sustainable packaging enhancing brand perception and marketability. Quality assurance, including stability testing and microbial analysis, is non-negotiable, given the direct application of these products to the skin. Efficiency in manufacturing and scaling production while adhering to stringent Good Manufacturing Practices (GMP) is essential for optimizing cost structure before distribution.

The downstream analysis covers distribution and marketing. Products reach the end-user through a diverse network of distribution channels, encompassing direct-to-consumer (DTC) digital platforms, specialized beauty retailers, professional salon chains, and regulated pharmacies. Direct and indirect sales strategies are both critical; DTC channels offer higher margins and direct consumer data access, facilitating personalized marketing and subscription models. Indirect channels, particularly pharmacies and dermatologists, lend credibility and trust to therapeutic and clinical-grade products. Effective marketing, leveraging digital content, influencer partnerships, and educational materials regarding proper usage and expected outcomes, completes the value chain, driving final sales and brand loyalty.

Potential customers for the Scalp Care and Hair Growth Products Market are broadly classified into three primary categories: individuals seeking prophylactic and routine maintenance, patients suffering from specific dermatological scalp conditions, and consumers experiencing symptomatic hair thinning or loss due to age, genetics, or environmental factors. The largest segment, driven by routine maintenance, includes both male and female consumers aged 25-45 who are highly engaged in holistic wellness and preventive anti-aging routines, viewing scalp health as synonymous with overall hair aesthetic quality. These consumers prioritize products offering detoxification, balancing the scalp microbiome, and preventing premature aging of hair follicles, often favoring natural and premium organic formulations promoted through social media and specialty beauty retailers.

The second major group consists of consumers seeking solutions for clinical conditions such as chronic dandruff (seborrheic dermatitis), psoriasis, and contact dermatitis. These buyers are typically guided by recommendations from dermatologists, trichologists, or pharmacists and rely on medicated, often physician-strength, formulations containing ingredients like ketoconazole, coal tar, or corticosteroids (though OTC products focus on non-prescription alternatives). This segment highly values scientific evidence, clinical validation, and the product's ability to provide long-term symptomatic relief and control, purchasing primarily through professional channels and certified pharmacies.

The third, and often highest-value, customer group comprises individuals actively experiencing moderate to severe hair loss (androgenetic alopecia, telogen effluvium). This segment spans all ages and genders and exhibits a high willingness to pay for treatments proven to stimulate growth, prevent further miniaturization, or thicken existing hair. These customers purchase a combination of pharmaceutical treatments (like Minoxidil), high-concentration peptide serums, and supporting devices (like laser combs). They are motivated by visible results and are heavily influenced by clinical efficacy data, case studies, and credible testimonials, making them prime targets for professional salon brands, clinical lines, and subscription-based targeted treatment regimens.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $11.5 Billion USD |

| Market Forecast in 2033 | $19.8 Billion USD |

| Growth Rate | 8.1% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | L'Oréal S.A., Procter & Gamble Co., Unilever PLC, Beiersdorf AG, Shiseido Company, Kao Corporation, Estée Lauder Companies Inc., Natura & Co Holding S.A., Henkel AG & Co. KGaA, Johnson & Johnson, Revlon Inc., Amorepacific Corporation, P&G Prestige, Sephora (LVMH), The Body Shop International Limited, Kerastase (L'Oréal), Olaplex, Aveda (Estée Lauder), Virtue Labs, Philip Kingsley |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape in the Scalp Care and Hair Growth Products market is characterized by a strong focus on enhancing ingredient penetration, leveraging advanced biotechnology for new active discovery, and integrating digital tools for consumer diagnostics and personalization. In formulation technology, the shift is towards microencapsulation and liposomal delivery systems. These systems protect sensitive bio-actives (like growth factors or retinoids) from degradation and ensure their targeted delivery deep into the follicular unit, significantly enhancing efficacy compared to traditional topical applications. Furthermore, advancements in microbiome technology, utilizing prebiotics, probiotics, and postbiotics, are essential for restoring the scalp's ecological balance, addressing issues like inflammation and dandruff from a foundational perspective. These sophisticated delivery and foundational biological technologies represent a high barrier to entry for smaller manufacturers and drive the premium pricing of high-performance products.

Biotechnology innovation plays a critical role in identifying the next generation of hair growth stimulants. Research is increasingly focused on mimicking natural biological processes, utilizing synthetic peptides, plant stem cell extracts, and patented growth factor mimetics that specifically target the Dermal Papilla cells responsible for hair cycle initiation. Genomic and proteomic research assists in tailoring these ingredients to common genetic predispositions for hair loss. Parallel to formulation technology, diagnostic technology is rapidly evolving. Handheld and smartphone-attachable microscopic devices, combined with AI software, allow trichologists and consumers alike to accurately assess hair density, follicle health, and scalp inflammation levels in real-time. This democratization of clinical-grade diagnosis is pivotal for driving personalized treatment uptake and validating product effectiveness for the end-user.

The integration of IoT (Internet of Things) devices and digital platforms further solidifies the technological landscape. Smart devices, such as connected laser caps or low-level light therapy (LLLT) helmets, offer tracking and adherence features, ensuring optimal usage protocols are followed and monitored, often synching data with specialized companion apps. Furthermore, blockchain technology is being explored to ensure the traceability and authenticity of high-value raw materials and finished products, combating the pervasive issue of counterfeiting in the luxury and therapeutic segments. The successful interplay between advanced chemistry, biotechnology, and digital consumer-facing tools is defining the competitive advantage and future growth trajectory of the specialized scalp care market.

The primary growth factors include increased consumer awareness regarding the link between scalp health and hair quality, rising global prevalence of stress-induced hair loss (telogen effluvium), and the strong industry shift towards incorporating advanced biotechnological ingredients like peptides and plant stem cells for enhanced efficacy. The expansion of professional trichology services also fuels demand for specialized products.

The Natural and Herbal segment is projected to exhibit a faster Compound Annual Growth Rate (CAGR) due to heightened consumer preference for 'clean label' products, concerns over long-term chemical exposure, and the successful integration of traditional botanicals with modern scientific validation. However, synthetic ingredients like Minoxidil maintain strong market value in the clinical treatment sub-segment due to regulatory approval and proven efficacy in addressing pattern baldness.

AI is crucial for market advancement by enabling hyper-personalization through digital diagnostics, where machine learning algorithms analyze individual scalp images and biometric data to recommend tailored product regimens. Furthermore, AI accelerates R&D by simulating ingredient interactions and predicting optimal formulation stability and clinical performance, shortening the time-to-market for novel treatments.

The Online distribution channel, encompassing direct-to-consumer (DTC) brand websites and major e-commerce platforms, is currently experiencing the fastest expansion. This growth is driven by the ability to offer targeted advertising, seamless subscription models, personalized digital consultations, and broader geographic accessibility, particularly for innovative or niche premium brands.

Future growth will be dominated by advancements in cellular technology, specifically the development of stem cell therapies and highly targeted gene-editing techniques focused on reactivating dormant hair follicles. In topical treatments, the widespread implementation of advanced delivery systems (liposomes, nanoparticles) to ensure deep follicular penetration of active pharmaceutical ingredients (APIs) will define efficacy standards.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.