ID : MRU_ 434898 | Date : Dec, 2025 | Pages : 253 | Region : Global | Publisher : MRU

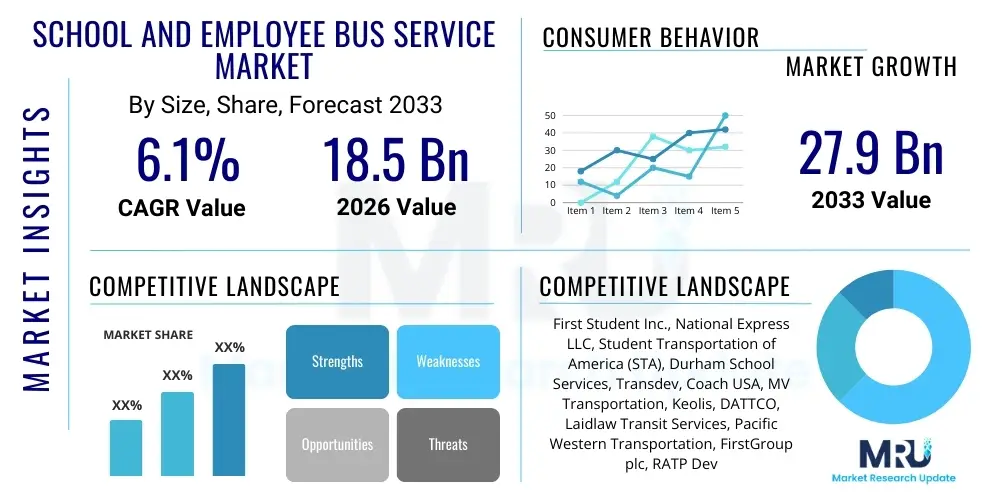

The School and Employee Bus Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.1% between 2026 and 2033. The market is estimated at USD 18.5 Billion in 2026 and is projected to reach USD 27.9 Billion by the end of the forecast period in 2033. This consistent expansion is underpinned by demographic shifts, increasing urbanization, stringent safety regulations imposed by governments globally, and the growing trend of outsourcing fleet management to specialized private operators, allowing educational institutions and corporations to focus on their core competencies.

The stability of this market segment is high, driven by the essential nature of the services provided. School transportation is often mandated by law, ensuring a reliable demand base. Similarly, employee transportation, particularly in large industrial zones, business parks, and IT sectors, is viewed as a crucial employee benefit and operational requirement, enhancing productivity and security. The market valuation reflects not just the volume of vehicles but also the increasing integration of technology, such as advanced routing software and safety systems, which command higher service premiums.

The School and Employee Bus Service Market encompasses specialized transportation services dedicated to the regular, scheduled movement of students to educational institutions and employees to their workplaces. This critical sector ensures safe, reliable, and efficient transit, serving as a vital infrastructural component for both the education system and corporate operational logistics. Key services involve route planning, vehicle maintenance, specialized driver training, and the integration of safety and monitoring technologies. Major applications span K-12 schooling, university commuting, corporate shuttles for large campuses, and specialized transport for construction or manufacturing sites. The primary benefits include enhanced safety compliance, reduced traffic congestion around facilities, guaranteed punctuality, and operational cost savings realized through outsourced fleet management and optimized routing.

The increasing complexity of urban environments and the expansion of metropolitan areas have made dedicated bus services indispensable. For schools, regulatory demands concerning student safety and security protocols are paramount, leading to greater reliance on professional service providers equipped with features like GPS tracking, onboard surveillance, and specialized communication tools. For corporate clients, the focus is often on reliability, comfort, and the environmental impact, driving the adoption of high-capacity and increasingly electrified vehicle fleets to support corporate sustainability mandates (ESG). The market serves as a backbone for daily economic and social activity, demonstrating consistent resilience even amidst economic fluctuations.

Driving factors for sustained growth include expanding educational enrollment worldwide, particularly in emerging economies; the proliferation of centralized corporate office hubs outside city centers, necessitating organized commuter solutions; and the persistent trend of operational outsourcing across public and private sectors. Furthermore, technological advancements like telematics, integrated fleet management solutions, and the shift towards environmentally friendly vehicles (electric and CNG buses) are enhancing service quality and driving modernization investments across the provider landscape, further cementing market expansion and generating higher revenue per vehicle managed.

The global School and Employee Bus Service Market is poised for stable yet significant growth, primarily fueled by urbanization and stricter compliance mandates regarding passenger safety and environmental sustainability. Business trends indicate a strong move toward consolidation among major operators who are leveraging economies of scale and advanced digital platforms to offer integrated, end-to-end transportation solutions. Key competitive differentiators include the rapid adoption of Electric Vehicles (EVs) to meet net-zero commitments, the implementation of sophisticated Artificial Intelligence (AI) for predictive maintenance and dynamic routing, and the enhancement of real-time communication tools for improved parental and employee transparency. Operators are increasingly adopting a service-as-a-product model, bundling fleet provision with software management and specialized safety training.

Regional trends highlight divergent growth profiles. North America and Europe, representing mature markets, are focusing heavily on fleet electrification and advanced regulatory compliance, driving incremental revenue through premium, technologically upgraded services. Conversely, the Asia Pacific (APAC) region is demonstrating explosive volume growth, propelled by massive student enrollment increases and the rapid establishment of corporate and industrial corridors in developing nations, leading to high demand for foundational bus services. The Middle East and Africa (MEA) and Latin America (LATAM) regions are capitalizing on infrastructure development projects and governmental initiatives aimed at formalizing public and private transit systems, offering significant opportunities for international providers to enter and scale operations.

Segmentation trends reveal that the 'Contracted Services' model dominates the market, preferred by both schools and large corporations for its fixed cost structure and risk transfer benefits. The 'Vehicle Type' segment shows increasing traction for medium and large-capacity buses, especially in congested urban areas. In terms of technology, services incorporating telematics and advanced safety features are experiencing the fastest adoption rates, indicating a prioritization of security and efficiency by end-users. This collective shift towards outsourced, technologically enabled, and environmentally conscious transportation solutions underscores the robust future trajectory of the School and Employee Bus Service Market.

Common user questions regarding AI in this sector frequently revolve around how artificial intelligence can demonstrably improve operational efficiency, minimize safety risks, and reduce fuel or energy consumption. Users are highly concerned about the tangible return on investment (ROI) derived from AI implementation, focusing specifically on applications such as predictive maintenance schedules for maximum fleet uptime, dynamic routing algorithms that adjust to real-time traffic conditions, and AI-powered driver behavior monitoring systems designed to proactively prevent accidents. There is also significant interest in how AI can optimize the complex logistics of managing decentralized fleets and personalized pickup/drop-off schedules, particularly in high-density urban environments or large corporate campuses, ensuring both punctuality and resource optimization.

The integration of AI is fundamentally transforming the operational paradigm of the School and Employee Bus Service Market, moving operations from reactive scheduling to predictive and prescriptive management. AI algorithms process vast amounts of data—including GPS coordinates, traffic patterns, driver telematics, and vehicle health metrics—to generate optimal routes that minimize travel time and mileage, directly impacting profitability and service reliability. Furthermore, AI-driven solutions are instrumental in enhancing passenger safety. By continuously analyzing data from onboard cameras and sensors, AI identifies high-risk driving behaviors (such as harsh braking or speeding) in real time, triggering alerts and generating actionable feedback for fleet managers, thereby significantly reducing the likelihood of incidents.

Moreover, AI extends its influence into critical maintenance functions. Instead of relying on time-based maintenance schedules, AI models predict component failures based on operational stressors and sensor readings, allowing for highly targeted and timely servicing. This predictive maintenance approach drastically reduces unexpected vehicle breakdowns, maximizes vehicle availability, and lowers overall maintenance costs, ensuring that service providers can meet their rigorous scheduling commitments. The long-term impact of AI is the creation of a hyper-efficient, safer, and highly adaptive transportation network, positioning AI as a core competitive advantage for market leaders.

The market is defined by a robust set of driving forces centered on increasing urbanization and regulatory pressure, countered by significant restraints related to operational costs and labor availability, while opportunities are emerging through technological integration and environmental shifts. Drivers include mandatory safety regulations (especially for school transport), corporate reliance on scheduled commuting for employee retention, and the global trend toward outsourcing non-core logistics. Restraints involve the high capital expenditure required for fleet electrification, fluctuating fuel prices impacting traditional fleets, and a persistent shortage of qualified commercial drivers globally. Opportunities are abundant in adopting sustainable transport solutions (EV buses), expanding service offerings into specialized needs (e.g., last-mile connectivity), and integrating sophisticated telematics and AI software platforms. These forces exert a significant collective impact, pushing the market towards modernization, efficiency improvements, and sustainable operations, simultaneously demanding higher levels of safety compliance and service reliability from all participating entities.

The School and Employee Bus Service Market is comprehensively segmented based on Service Type, End-User, Ownership Model, and Vehicle Type, allowing for targeted analysis of market dynamics and consumer preferences across different operational environments. Understanding these segmentation nuances is crucial for providers seeking to optimize their service portfolios and regional expansion strategies. The dominance of contracted services reflects the industry's desire for operational scalability and financial predictability, while the key end-user division highlights the distinct safety and regulatory requirements governing school transport versus the logistical demands of corporate shuttles. The increasing shift towards specialized and technologically integrated services further defines the competitive landscape within these segments.

The value chain for the School and Employee Bus Service Market begins with upstream activities focused on vehicle procurement and maintenance planning. Upstream analysis involves strategic relationships with Original Equipment Manufacturers (OEMs) for bus acquisition, focusing on specialized vehicles that meet stringent safety and environmental standards (e.g., compliant school bus specifications or low-emission corporate shuttles). It also encompasses the sourcing of crucial components like advanced safety systems (cameras, sensors) and fleet management software (telematics). Procurement efficiency and securing favorable financing terms for large fleet purchases are critical determinants of competitive cost structure at this initial stage, often involving negotiations with chassis manufacturers and specialized body builders.

Downstream analysis focuses heavily on service delivery and end-user satisfaction. The distribution channel is predominantly characterized by direct service contracts established between the bus service providers (operators) and the end-users (schools or corporations). Direct channels ensure tailored route planning, real-time communication, and customized safety protocols specific to the client’s environment. Indirect channels might involve partnerships with third-party logistics (3PL) providers in some corporate environments, though this is less common for school transport due to regulatory demands. Key downstream activities include sophisticated route optimization, driver management and training, operational scheduling, and customer support for managing inquiries, changes, and emergency response protocols, all of which directly contribute to the perceived quality and reliability of the service.

The efficiency of the entire value chain is increasingly reliant on technology integration. Successful operators leverage integrated software platforms that link maintenance schedules (upstream) with real-time operational performance and driver behavior monitoring (downstream). This full integration minimizes dead mileage, improves vehicle uptime, and ensures maximum regulatory compliance. The shift towards contracted services emphasizes the service provider's role as the central hub managing all aspects—from capital investment and maintenance liability to daily operational execution—thereby centralizing risk and specialized knowledge, and creating significant barriers to entry for new competitors lacking comprehensive technological infrastructure.

Potential customers, or end-users, of the School and Employee Bus Service Market are highly diversified, but broadly fall into institutional and corporate categories, each presenting unique service requirements and procurement processes. The primary institutional buyers are educational bodies, ranging from local public school districts (K-12) mandated to provide transport, to large private schools and universities requiring daily commuter services for thousands of students across extended geographical areas. These customers prioritize adherence to stringent child safety regulations, reliability, and cost-efficiency, often selecting long-term contracts through competitive bidding processes that heavily weigh compliance records and fleet modernity.

Corporate customers form the second major segment, including large technology companies with sprawling campus environments, manufacturing firms located in industrial parks far from residential centers, and governmental agencies requiring secure, reliable transit for employees. For corporate buyers, service priorities center on punctuality, employee comfort, flexibility in route adjustments, and increasingly, alignment with their Environmental, Social, and Governance (ESG) targets through the use of low-emission or electric vehicles. The decision-makers are typically facilities managers, HR departments focused on benefits packages, or procurement teams managing comprehensive logistics portfolios, looking for bundled services that integrate easily with existing internal systems.

Furthermore, emerging customer segments include specialized event organizers, large-scale medical facilities (hospitals), and residential developers in planned communities who require shuttle services to local transportation hubs. These buyers seek scalable, high-quality, and reliable service solutions that enhance the overall user experience of their constituents or residents. The common thread across all potential customers is the desire to outsource the complexity and capital burden associated with fleet ownership and management, opting instead for professional, compliant, and technology-enabled third-party services.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 27.9 Billion |

| Growth Rate | 6.1% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | First Student Inc., National Express LLC, Student Transportation of America (STA), Durham School Services, Transdev, Coach USA, MV Transportation, Keolis, DATTCO, Laidlaw Transit Services, Pacific Western Transportation, FirstGroup plc, RATP Dev, ComfortDelGro Corporation Limited, Stagecoach Group, Thames Travel, LogiBus, Zūm, Kura, Bus.com |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the School and Employee Bus Service Market is undergoing rapid transformation, driven primarily by the need for enhanced safety, operational efficiency, and environmental compliance. The core technologies currently dominating this sector are advanced telematics and IoT devices, which provide real-time data on vehicle location, speed, maintenance requirements, and driver behavior. These systems are critical for service transparency, enabling parents and employers to track vehicles, and for operational managers to ensure route adherence and performance metrics are met. Furthermore, sophisticated proprietary software platforms are utilized for managing complex scheduling, integrating vehicle availability with student or employee ridership data, and dynamically adjusting routes based on traffic flows, moving beyond static, pre-planned itineraries.

A second major technological pillar involves the integration of Advanced Driver Assistance Systems (ADAS) and high-definition onboard surveillance. ADAS features, such as collision mitigation, lane departure warnings, and pedestrian detection systems, significantly elevate the safety profile of the fleet, a non-negotiable requirement, especially in school transport. Coupled with internal camera systems and biometric authentication for drivers, these technologies minimize human error and provide comprehensive records for incident analysis, thereby reducing liability and insurance costs. The implementation of AI-powered video analytics is increasingly being used to monitor student behavior or employee interactions, ensuring a safe and secure environment inside the vehicle cabin throughout the transit duration.

Finally, the long-term technological focus is heavily skewed towards vehicle electrification and the associated infrastructure management solutions. The transition to Electric Buses (E-Buses) necessitates new technologies for managing charging infrastructure, battery health monitoring, and optimizing vehicle deployment based on range capabilities. Specialized software is required to plan routes that incorporate necessary charging stops without compromising schedule adherence. This shift not only reduces carbon footprint but also lowers long-term operational costs due to decreased fuel consumption and simplified maintenance, making technological investment in EV infrastructure a critical strategic imperative for market leaders.

The primary driver is the stringent governmental push for reduced carbon emissions, coupled with significant public and corporate emphasis on Environmental, Social, and Governance (ESG) compliance. Grants and subsidies in regions like North America and Europe incentivize fleet operators to transition to ZEVs, despite higher initial capital costs.

AI improves safety through predictive driver behavior monitoring, utilizing cameras and sensors to identify distractions or aggressive driving in real time. It also optimizes routes to avoid high-risk traffic areas and integrates with ADAS to proactively mitigate potential collisions, significantly lowering accident rates.

The School Transportation End-User segment historically holds the largest market share due to its non-discretionary nature and mandated regulatory requirements, ensuring a stable, high-volume base demand across developed economies and rapidly expanding enrollment in emerging markets.

The most significant challenge is the persistent global shortage of qualified and appropriately licensed commercial bus drivers. This scarcity drives up labor costs, necessitates competitive compensation packages, and requires substantial investment in driver recruitment, retention, and specialized safety training programs.

The School and Employee Bus Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.1% between 2026 and 2033, driven by outsourcing trends, technological integration, and increasing demographic shifts, particularly in the Asia Pacific region.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.