ID : MRU_ 432230 | Date : Dec, 2025 | Pages : 257 | Region : Global | Publisher : MRU

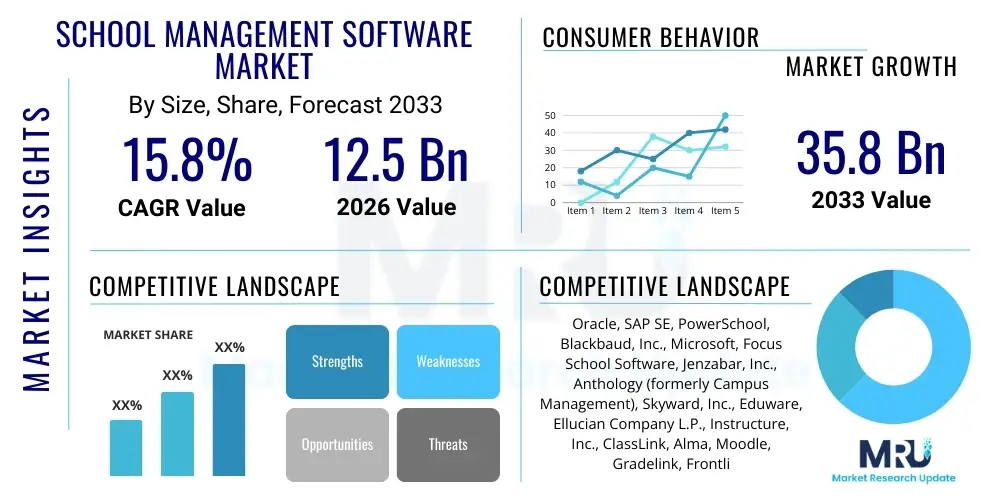

The School Management Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2026 and 2033. The market is estimated at USD 12.5 Billion in 2026 and is projected to reach USD 35.8 Billion by the end of the forecast period in 2033.

This robust growth trajectory is underpinned by the accelerating global imperative for digital transformation within the education sector, necessitating integrated platforms capable of managing complex administrative, academic, and financial operations. Institutions worldwide, spanning K-12 and higher education, are increasingly recognizing the strategic value of unified software solutions to enhance transparency, improve resource allocation, and drive student success metrics. The shift from fragmented, manual processes to centralized, automated digital environments is the core driver propelling market expansion, especially as regulatory bodies impose stricter requirements for data reporting and privacy compliance.

Furthermore, the increased adoption of cloud computing technologies significantly lowers the barrier to entry for smaller institutions, facilitating widespread deployment across diverse geographical regions, including emerging markets in Asia Pacific and Latin America. The demand for modular systems that can seamlessly integrate specialized functionalities, such as advanced analytics, remote learning tools, and specialized communication portals, contributes substantially to the overall market valuation. Market projections reflect continuous investment in research and development by key players, focusing on AI-powered features and mobile compatibility to capture the evolving needs of modern educational ecosystems.

The School Management Software (SMS) Market focuses on comprehensive, integrated digital platforms designed to automate and manage core operations of educational institutions. These solutions typically combine functionalities like Student Information Systems (SIS), Learning Management Systems (LMS), financial management, HR, and parent communication tools into a singular interface. The major applications span managing student enrollment and records, facilitating virtual and blended learning environments, processing fees, scheduling classes, and generating compliance reports. Benefits derived from implementation include heightened operational efficiency, significant reduction in manual errors, enhanced data security, improved stakeholder communication, and the provision of actionable insights necessary for strategic decision-making. The market is primarily driven by the worldwide push for educational digitalization, increased demand for streamlined administrative workflows, and regulatory requirements demanding transparent institutional data management.

The market is currently undergoing a significant technological evolution, characterized by a rapid migration from legacy on-premise systems to highly scalable, cloud-native (SaaS) architectures, aligning with global business trends favoring subscription-based models for accessibility and continuous updates. Regional trends highlight North America and Europe maintaining revenue leadership due to high technological maturity and strict regulatory compliance mandates, while the Asia Pacific region exhibits the highest growth potential, spurred by massive governmental investment in digital educational infrastructure. Segment trends indicate robust growth in the application segment, particularly for specialized modules integrating AI for personalized learning and predictive analytics, moving SMS solutions beyond basic record-keeping toward sophisticated educational intelligence platforms.

Common user inquiries concerning Artificial Intelligence (AI) in School Management Software frequently probe its efficacy in optimizing administrative load, enabling truly personalized student experiences, and ensuring equitable resource distribution. Users are keenly interested in predictive analytics capabilities—specifically, how AI algorithms can reliably forecast student academic performance, identify early indicators of disengagement, and automate complex tasks like optimized timetable generation. Underlying these questions are critical concerns regarding data privacy, algorithmic transparency, and the potential for bias in AI-driven assessment tools, necessitating vendors to emphasize ethical data governance and explainable AI models.

AI integration is fundamentally redefining the scope and intelligence of SMS platforms, transitioning them from static databases into dynamic, predictive tools. Machine learning models are being deployed across various modules, most notably in personalized learning pathways where systems analyze vast amounts of student performance data, engagement metrics, and learning styles to recommend optimal content, pacing, and intervention strategies tailored to individual needs. This enables educators to manage diverse classroom needs effectively, shifting the pedagogical focus from standardized instruction to highly individualized educational support. Furthermore, AI streamlines traditionally time-consuming administrative functions, such as automated attendance verification via facial recognition or real-time intelligent routing of inquiries to relevant departments, drastically improving institutional response times and efficiency.

In the realm of institutional management, AI-powered analytics modules are critical for strategic planning. These tools enable complex scenario modeling for resource allocation, including optimizing facility usage, forecasting staffing needs based on anticipated enrollment trends, and analyzing the effectiveness of specific educational programs against predefined key performance indicators (KPIs). The successful deployment of these sophisticated AI tools hinges on the quality and integrity of the data collected and managed within the core SMS. Therefore, vendors are aggressively enhancing data processing pipelines and security frameworks to ensure compliance with stringent data protection acts globally, guaranteeing that AI operations are both effective and ethically sound, mitigating risks related to data breaches or unfair algorithmic outcomes.

The School Management Software market expansion is critically fueled by global governmental mandates for educational digitalization and the necessity for centralized data systems to meet complex regulatory reporting requirements. However, growth is substantially restrained by the high upfront investment required for full system implementation and the inertial resistance to change within deeply traditional educational organizations. Significant opportunities emerge from the expansion into developing economies and the creation of highly specialized, modular solutions addressing niche institutional needs like student well-being and advanced alumni tracking. These dynamics exert strong impact forces, chiefly driving intense competition focused on feature differentiation, ease of integration, and aggressive pricing strategies within the burgeoning cloud segment.

Drivers: The paramount driver is the worldwide shift toward streamlined administrative processes using integrated digital tools. Educational institutions are under pressure to operate more like efficient corporate entities, demanding comprehensive Enterprise Resource Planning (ERP) capabilities tailored for the education environment. Regulatory compliance, specifically concerning financial auditing, student tracking, and privacy standards (like GDPR and COPPA), necessitates robust, verifiable software systems. Furthermore, the mass transition to hybrid and remote learning environments, accelerated by global events, has made integrated Learning Management Systems (LMS) and communication tools within the core SMS platform non-negotiable for continuity of education, thereby sustaining high market demand.

Restraints: The most significant impediment remains the high initial cost associated with procurement, customization, staff training, and especially the migration of historical data from legacy systems, which can be prohibitive for budget-constrained public institutions. This is compounded by inherent resistance among long-serving administrative staff and educators who lack technological literacy or fear job displacement due to automation, leading to slow adoption cycles. Crucially, the sensitive nature of student data heightens concerns around cybersecurity vulnerabilities and vendor reliability, leading to extensive and cautious vetting processes that lengthen sales cycles and amplify the perceived risk of large-scale system transitions.

Opportunity: The market offers vast opportunities in two key areas: geographic expansion and technological specialization. Emerging economies, particularly in Southeast Asia and Africa, represent large untapped markets where government investment in public education digitalization is rapidly increasing. Technologically, opportunities lie in developing highly specialized vertical modules, such as advanced financial aid calculation tools, sophisticated alumni engagement platforms that track lifelong student journeys, and mobile-first administrative interfaces optimized for low-bandwidth environments. Integrating technologies like blockchain for secure transcript verification and digital credentialing offers vendors a unique competitive edge in higher education markets.

Market segmentation provides a clear view of where investment and growth are concentrated within the School Management Software ecosystem. The market is primarily divided by deployment type (Cloud vs. On-Premise), application focus (SIS, LMS, Fee Management, etc.), and end-user category (K-12 vs. Higher Education). Cloud solutions dominate the deployment landscape due to their superior scalability and reduced infrastructure overhead. End-user analysis highlights the K-12 segment as the largest user base, driven by the massive scale and standardization requirements of public school systems globally, whereas Higher Education seeks greater complexity in financial and research management modules.

In the application segment, the boundary between SIS and LMS is increasingly blurring, leading to demand for comprehensive, unified platforms that provide seamless data flow between administrative functions and academic delivery. Institutions prioritize systems that offer strong integration capabilities, particularly with third-party tools for collaboration (e.g., Microsoft Teams, Google Classroom) and specialized academic resources. The shift towards outcome-based education models also drives demand for sophisticated examination and assessment management modules that allow for real-time tracking of student progress against learning objectives, requiring robust reporting and data visualization features within the core software.

The dynamics within the end-user segmentation are nuanced. K-12 institutions typically require highly standardized, easy-to-deploy solutions suitable for district-wide mandates and focused primarily on core administrative functions, parental communication, and regulatory compliance (e.g., immunization tracking, truancy reports). Conversely, Higher Education institutions, encompassing colleges and large universities, demand highly customizable, complex solutions that can handle intricate course catalogs, research management, massive student record volumes, and sophisticated integrations with specialized ERP systems and legacy financial platforms. The procurement cycles and required technical support levels vary dramatically between these two end-user groups, requiring vendors to tailor their sales and service strategies accordingly.

The School Management Software value chain begins with foundational technology providers (upstream), including cloud infrastructure hosts (AWS, Azure) and core database technology licensors, which provide the essential computational backbone. Midstream activities involve intensive software development, quality assurance, module design, and regulatory compliance integration. Downstream elements focus heavily on market distribution, which utilizes both direct sales teams for large contracts and indirect channels (VARs/System Integrators) for localized support, culminating in crucial post-implementation services such as data migration, extensive staff training, and long-term technical support managed through recurring service contracts.

The upstream segment is critical as vendors must secure highly reliable, scalable, and secure cloud environments to host their SaaS applications, emphasizing robust Service Level Agreements (SLAs) regarding uptime and data resilience. Strategic partnerships with specialized technology firms providing AI engines, advanced security threat intelligence, or proprietary communication protocols are becoming increasingly common to enhance the core platform capabilities. Vendors must strategically manage these relationships to minimize reliance on any single supplier and ensure continuous technological advancement without compromising the security or stability of the institutional client base.

The distribution and downstream execution phases are where competitive differentiation is often achieved. Direct sales are preferred for high-value university and major district contracts, allowing vendors to offer deep customization and dedicated implementation consultancy. Conversely, indirect channels are vital for penetrating smaller private school markets or geographically diverse regions where local expertise in regulatory frameworks and language support is essential for successful adoption. Given the SaaS nature of the majority of new deployments, maximizing customer satisfaction and minimizing churn through proactive technical support, continuous feature releases, and specialized training programs defines long-term profitability and market retention for SMS providers.

Potential customers for School Management Software represent a broad spectrum of educational organizations, ranging from small, independent private kindergartens to multi-campus, publicly funded university systems enrolling hundreds of thousands of students. The primary purchasing decision-makers are typically institution heads, district superintendents, CFOs, and IT directors who are ultimately accountable for operational efficiency, compliance, and technological modernization. They seek solutions that offer a demonstrable Return on Investment (ROI) through automation, error reduction, and superior data capabilities for reporting to stakeholders and governmental bodies.

Within the K-12 sector, potential customers are often divided between decentralized private schools and centralized public school districts. Public districts require robust, scalable systems that can manage complex multi-site data requirements, adhere strictly to state and federal funding metrics, and facilitate seamless data transfer during student movement. These contracts are frequently won through rigorous public bidding processes based heavily on compliance history and total cost of ownership. Private schools, while smaller in scale, often prioritize user experience, mobile apps for parent engagement, and highly integrated fundraising and enrollment marketing tools.

Higher Education institutions constitute a highly valuable customer segment characterized by demanding functional requirements. Universities typically require systems that integrate academic administration (registrations, grading) with highly specialized modules for research management, grant tracking, financial aid disbursements, housing allocation, and sophisticated alumni networking platforms. Vendors targeting this segment must demonstrate deep domain expertise and provide highly reliable systems capable of integrating with existing large-scale ERP platforms like Oracle or SAP, ensuring the SMS acts as a central hub for all academic and student lifecycle data management across complex institutional structures.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 35.8 Billion |

| Growth Rate | 15.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Oracle, SAP SE, PowerSchool, Blackbaud, Inc., Microsoft, Focus School Software, Jenzabar, Inc., Anthology (formerly Campus Management), Skyward, Inc., Eduware, Ellucian Company L.P., Instructure, Inc., ClassLink, Alma, Moodle, Gradelink, Frontline Education, Foradian Technologies, TADS, DreamClass |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The modern School Management Software landscape is defined by its reliance on cloud infrastructure, specifically leveraging multi-tenant, microservices architecture to ensure high scalability and quick deployment across diverse educational settings. A critical technological focus is interoperability, achieved through adherence to open standards (like OneRoster and LTI) and the development of robust Application Programming Interfaces (APIs), allowing seamless data exchange with the hundreds of specialized EdTech tools used by contemporary schools. Furthermore, mobile optimization is paramount, enabling secure and functional access for students, parents, and teachers using smartphones and tablets, recognizing the dominance of mobile devices in accessing educational services globally.

Data security forms the foundational technology layer. Leading vendors utilize advanced cybersecurity protocols, including zero-trust architectures, behavioral analytics for access control, and adherence to ISO 27001 standards, specifically tailored to meet the stringent requirements of educational privacy acts like FERPA and GDPR. Technological evolution is also concentrated in the embedded analytics capabilities, utilizing big data platforms and machine learning to offer sophisticated reporting dashboards that move beyond historical data, providing predictive insights into budget variances, staffing efficiency, and student academic trajectories, supporting data-driven policy changes.

Looking forward, the technology landscape is expanding to include integration with technologies beyond traditional software. This encompasses incorporating Internet of Things (IoT) sensors for smart campus management, such as environmental controls and physical asset tracking, linked back to the core SMS for maintenance and resource optimization. Additionally, blockchain technology is being piloted for secure, decentralized digital transcript and credential management, offering tamper-proof records and streamlining the process of academic verification, marking a major technological shift in how educational achievements are recorded and shared globally.

The global School Management Software market exhibits distinct regional adoption patterns influenced by economic factors, technological readiness, and governmental policy. While North America and Europe provide mature, high-value markets demanding sophisticated, compliance-heavy solutions, Asia Pacific and Latin America are the engines of volume growth, driven by expansive governmental investment aimed at universal access to digital education. The Middle East demonstrates a high propensity for adopting premium, specialized systems in line with national vision plans to create world-class educational institutions. Understanding these regional variances is key for vendors to tailor marketing, pricing, and localization strategies effectively.

North America: This region maintains its position as the largest revenue generator, characterized by widespread deployment across massive K-12 districts and leading universities. The market is saturated but highly competitive, with demand centered on platform consolidation, advanced AI-driven student success tools, and robust compliance features (especially concerning FERPA and state-level reporting mandates). The technological environment favors highly integrated, cloud-based systems that offer excellent API support for interoperability with specialized instructional tools, reflecting a high degree of technological maturity among users and administrators.

Europe: The European market is highly sensitive to regulatory mandates, particularly GDPR, which dictates strict rules on data sovereignty and storage, leading to strong demand for local data hosting options and clear data governance policies. The market structure is fragmented due to diverse national curriculum requirements and varying IT spending levels. Western Europe (UK, Nordics) shows rapid adoption of full-SaaS models, while Southern and Eastern European countries are focused on achieving cost efficiencies through modular, government-subsidized solutions. Customization for multi-lingual user interfaces is a critical requirement across the continent.

Asia Pacific (APAC): The fastest-growing regional market, APAC's momentum is derived from huge population bases and strong governmental pushes toward educational modernization, such as India’s National Education Policy (NEP) and similar initiatives in China and Indonesia. The primary demand is for highly scalable, yet affordable, cloud-based solutions capable of managing vast student enrollment figures. Market entry strategies often require extensive localization, partnerships with local service providers, and solutions designed to function reliably in environments with varying levels of internet bandwidth and infrastructure quality.

Latin America (LATAM) and Middle East & Africa (MEA): LATAM's growth is accelerating as public and private institutions seek to modernize management practices, driven by urbanization and increasing mobile penetration. The demand focuses on bilingual systems and integrated financial tools to handle complex regional taxation and fee structures. The MEA region, particularly the Gulf nations, represents a premium market where institutions frequently invest in top-tier global solutions offering maximum security, advanced features, and tailored modules for managing both local and expatriate student populations, often supported by high governmental educational expenditure.

The primary factor is the superior scalability and reduced Total Cost of Ownership (TCO) offered by cloud solutions, eliminating the need for institutions to invest heavily in physical hardware, simplifying maintenance, and enabling rapid, continuous deployment of new features and security updates.

Vendors ensure compliance by implementing robust security frameworks, including end-to-end encryption, utilizing strict multi-factor authentication, providing data residency options compliant with GDPR and FERPA requirements, and maintaining comprehensive, auditable access logs to track all sensitive data interactions.

Higher Education institutions typically place the highest demand on customization capabilities, requiring highly flexible software to manage complex research grants, diverse degree structures, and specialized integrations with existing large-scale Enterprise Resource Planning (ERP) and alumni relations systems.

Interoperability is critical, allowing the SMS to seamlessly exchange data with specialized third-party EdTech tools (like digital assessment platforms or communication apps) using open APIs and industry standards (e.g., LTI, OneRoster), thereby avoiding vendor lock-in and maximizing the utility of existing technology investments.

The most significant restraint in developing countries is the substantial initial implementation cost, which includes necessary IT infrastructure upgrades, extensive staff training requirements, and challenges related to inconsistent internet connectivity hindering the deployment and reliable operation of cloud-based solutions.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.