ID : MRU_ 393081 | Date : May, 2025 | Pages : 368 | Region : Global | Publisher : MRU

The SCR Denitrification Catalyst market is poised for significant growth from 2025 to 2032, projected at a CAGR of 8%. This growth is fueled by stringent environmental regulations globally aimed at reducing nitrogen oxide (NOx) emissions, a major contributor to air pollution and acid rain. Power plants, cement factories, and other industrial facilities are under increasing pressure to adopt cleaner technologies, driving demand for SCR denitrification catalysts. Technological advancements in catalyst design, including the development of more efficient and durable materials like vanadium-based and titanium-based catalysts, are also contributing to market expansion. These improvements enhance NOx reduction efficiency, extend catalyst lifespan, and lower operating costs, making SCR technology more attractive to industries. The market plays a crucial role in addressing global challenges related to air quality and public health. By effectively reducing NOx emissions from various industrial sources, SCR denitrification catalysts contribute to cleaner air, improved respiratory health, and a better overall environment. Furthermore, the increasing awareness of the detrimental effects of air pollution on climate change is also bolstering the demand for these catalysts. The global push towards cleaner energy sources and the commitment to reducing greenhouse gas emissions indirectly boost the market by promoting the adoption of cleaner technologies, such as those incorporating SCR systems. The markets future is bright, driven by both regulatory mandates and the increasing recognition of the environmental and economic benefits of cleaner air. The continued innovation in catalyst materials and system designs will further propel the markets expansion.

The SCR Denitrification Catalyst market is poised for significant growth from 2025 to 2032, projected at a CAGR of 8%

The SCR Denitrification Catalyst market encompasses the manufacturing, distribution, and application of catalysts used in selective catalytic reduction (SCR) systems. These systems are employed to reduce NOx emissions from various sources, primarily industrial processes like power generation, cement production, and metal refining. The markets scope includes diverse catalyst types, including honeycomb, plate, and corrugated catalysts, each with unique characteristics influencing their application and performance. The applications span a broad range of industries, including power plants (coal-fired, natural gas-fired), cement plants, steel plants, glass manufacturing facilities, chemical processing plants, and increasingly, transportation (heavy-duty vehicles). The markets significance lies in its contribution to global efforts to combat air pollution. In the broader context of global trends, this market aligns perfectly with the worldwide shift towards environmental sustainability and responsible industrial practices. The increasing emphasis on regulatory compliance, coupled with growing corporate social responsibility initiatives, underscores the importance of this market. The markets future growth is inextricably linked to the global commitment to reducing greenhouse gas emissions and improving air quality, making it a key component of a larger sustainable development agenda. Furthermore, the growing focus on circular economy principles is creating opportunities for catalyst regeneration and recycling, adding another layer to the markets complexity and growth potential.

The SCR Denitrification Catalyst market refers to the commercial sector involved in the production, sale, and implementation of catalysts specifically designed for selective catalytic reduction (SCR) systems. These catalysts are crucial components within SCR systems, facilitating the chemical reaction that converts harmful nitrogen oxides (NOx) into less harmful nitrogen (N2) and water (H2O) in the presence of a reductant such as ammonia (NH3) or urea. The market includes the manufacturers of these catalysts, which are typically composed of various metal oxides, notably vanadium, tungsten, and titanium oxides, supported on a substrate (honeycomb, plate, or corrugated). The market also encompasses the suppliers of related equipment and services, including installation, maintenance, and regeneration or replacement of spent catalysts. Key terms associated with this market include NOx, SCR, ammonia slip, catalyst deactivation, surface area, pore volume, and active sites. Understanding these terms is crucial to evaluating catalyst performance, lifespan, and overall system efficiency. Different types of catalysts exhibit varying levels of activity, selectivity, and resistance to poisoning, and their selection depends heavily on the specific application and operating conditions. The market is driven by the increasing stringency of environmental regulations, particularly regarding NOx emission limits, making the understanding of these parameters and their economic implications highly relevant.

The SCR Denitrification Catalyst market can be segmented by catalyst type, application, and end-user. These segments offer a granular view of market dynamics and growth drivers. Understanding these segments is crucial for targeted marketing strategies and investment decisions within the market.

| Report Attributes | Report Details |

| Base year | 2024 |

| Forecast year | 2025-2032 |

| CAGR % | 8 |

| Segments Covered | Key Players, Types, Applications, End-Users, and more |

| Major Players | Johnson Matthey, BASF Cormetech, Hitachi Zosen, Ceram-Ibiden, Haldor Topsoe, JGC C&C, Shell (CRI), Tianhe (Baoding), Hailiang, Datang Environmental, Guodian Longyuan, Jiangsu Wonder, Tuna, Dongfang KWH, Chongqing Yuanda, Gem Sky, Beijing Denox, CHEC |

| Types | Honeycomb Catalyst, Plate Catalyst, Corrugated Catalyst |

| Applications | Power Plant, Cement Plant, Steel Plant, Glass Industry, Chemical Industry, Transportation |

| Industry Coverage | Total Revenue Forecast, Company Ranking and Market Share, Regional Competitive Landscape, Growth Factors, New Trends, Business Strategies, and more |

| Region Analysis | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

Stringent environmental regulations globally are the primary driver, mandating NOx emission reductions. Technological advancements in catalyst materials and designs lead to improved efficiency and longer lifespans. The increasing awareness of the health and environmental consequences of air pollution is fueling demand for cleaner technologies, further propelling the markets growth. Government incentives and subsidies are also playing a role in promoting the adoption of SCR systems. The continuous development of more effective and cost-efficient catalysts contributes to overall market expansion.

High initial investment costs for installing SCR systems can be a barrier, particularly for smaller businesses. The need for skilled labor for installation, operation, and maintenance can be challenging in some regions. The potential for catalyst poisoning and deactivation by contaminants present in the exhaust gas stream can impact performance and lifespan. Furthermore, the availability of appropriate reductants (ammonia or urea) can also influence market penetration in specific regions.

The development of more efficient and durable catalysts, potentially using innovative materials and nanotechnology, is a significant opportunity. Expanding into new applications, particularly in emerging economies with growing industrial sectors, offers considerable potential. The development of cost-effective catalyst regeneration and recycling technologies will contribute to sustainability and reduce waste. Further innovation in SCR system design to optimize efficiency and reduce operational costs will also drive market growth. The potential for synergy with other emission control technologies presents another opportunity.

Maintaining catalyst performance over time is a significant challenge due to potential deactivation mechanisms such as poisoning by impurities in exhaust gases (e.g., heavy metals, dust). The fluctuation in raw material prices for catalyst components can impact manufacturing costs and profitability. Competition among catalyst manufacturers necessitates continuous innovation and cost optimization. Ensuring the safe handling and disposal of spent catalysts are critical environmental concerns that require addressing. The regulatory landscape continues to evolve, requiring manufacturers to adapt to changing standards and compliance requirements. Meeting the diverse needs of various industrial applications with customized catalyst solutions presents a technological challenge. Achieving a balance between optimizing performance, minimizing pressure drop, and maintaining cost-effectiveness is crucial for market competitiveness. Lastly, integrating SCR technology seamlessly into existing industrial processes, especially in older plants, can present logistical and engineering hurdles.

The market is witnessing a trend toward the development of high-performance catalysts with enhanced activity, selectivity, and resistance to poisoning. The integration of advanced materials like zeolites and metal-organic frameworks is being explored for improved efficiency. Theres also a growing focus on catalyst regeneration and recycling to enhance sustainability and reduce environmental impact. The use of data analytics and machine learning for optimizing catalyst performance and predicting catalyst life is gaining traction. Furthermore, the development of miniature SCR systems for smaller applications, particularly in mobile sources, is an emerging trend.

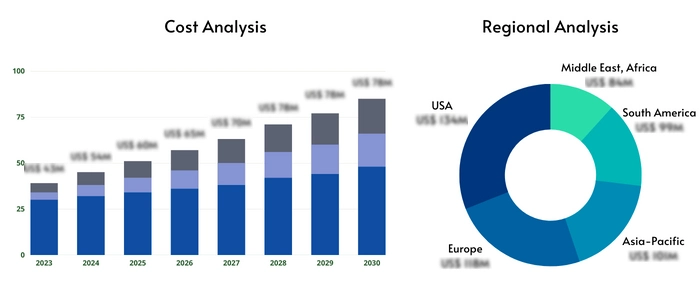

Asia Pacific is expected to dominate the market due to rapid industrialization and stringent emission regulations in countries like China and India. North America and Europe are also significant markets with established regulatory frameworks and a high adoption of SCR technology. Latin America, the Middle East, and Africa are projected to witness moderate growth driven by increasing industrial activities and government initiatives focused on improving air quality. However, varying levels of economic development and regulatory enforcement across different regions will impact market penetration. The availability of skilled workforce and infrastructure will also play a significant role in regional market dynamics. Cultural factors and local preferences for specific catalyst types may also contribute to regional variations in market share. The specific regulatory environment in each region will influence the type of catalysts preferred and the rate of adoption of SCR technology.

The market is projected to grow at a CAGR of 8% from 2025 to 2032 (replace with your chosen CAGR).

Stringent environmental regulations, technological advancements in catalyst materials, and the increasing focus on sustainability are key drivers.

Honeycomb, plate, and corrugated catalysts are commonly used, each suited to specific applications and system requirements.

The Asia Pacific region is projected to lead the market due to its rapid industrialization and stringent environmental regulations.