ID : MRU_ 433719 | Date : Dec, 2025 | Pages : 258 | Region : Global | Publisher : MRU

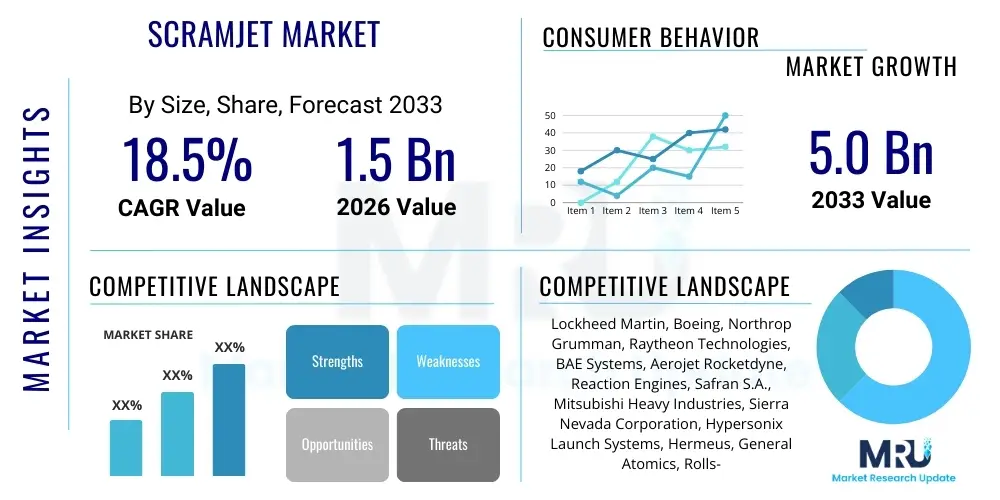

The Scramjet Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2026 and 2033. The market is estimated at $1.5 Billion in 2026 and is projected to reach $5.0 Billion by the end of the forecast period in 2033.

The Scramjet (Supersonic Combustion Ramjet) Market encompasses the research, development, testing, and potential deployment of air-breathing propulsion systems designed to operate efficiently at hypersonic speeds, typically above Mach 5. These advanced engines utilize the kinetic energy of the incoming air compressed by the vehicle's forward motion, allowing fuel to combust supersonically within the engine chamber. The core products include engine prototypes, high-temperature materials, computational fluid dynamics (CFD) software optimized for hypersonic flow, and integrated test articles. Major applications center around defense programs, including hypersonic missiles and reconnaissance vehicles, as well as potential future applications in high-speed, cost-effective access to space for both military and commercial payloads.

The primary benefits of Scramjet technology include significantly increased speed and range compared to traditional jet engines or rockets, lower launch costs due to reduced reliance on onboard oxidizer, and the ability to operate within the atmosphere, offering maneuverability advantages. The development of reliable Scramjet engines is crucial for maintaining technological superiority in strategic defense capabilities globally. These systems address the growing need for rapid global strike capabilities and enhanced space accessibility.

Driving factors for this specialized market are predominantly driven by escalating geopolitical competition, particularly the hypersonic arms race involving major powers like the United States, China, and Russia. Furthermore, sustained high levels of government funding for fundamental aerospace research, coupled with advancements in material science—especially ultra-high temperature ceramics and composites necessary to withstand the extreme thermal and pressure loads—are propelling market growth. The increasing commercial interest in point-to-point suborbital travel and rapid payload delivery also contributes to the sustained investment in core Scramjet research and prototyping.

The Scramjet Market is currently characterized by significant government investment and accelerated technology demonstrators, signaling a shift from fundamental research to operational prototype development. Business trends indicate strong vertical integration among defense prime contractors who are acquiring specialized material science and propulsion technology firms to secure proprietary knowledge in critical high-temperature components. Regional trends show North America and Asia Pacific dominating R&D spending, driven by established defense budgets in the U.S. and rapidly expanding programs in countries like China and India, making these regions the epicenter of technological advancement and market commercialization. Segment trends emphasize the propulsion component segment, specifically the combustor and nozzle systems, due to the high complexity and proprietary nature of achieving stable supersonic combustion, while the application segment is overwhelmingly dominated by the military sector focused on missile and reconnaissance platform integration.

Users commonly inquire about how Artificial Intelligence (AI) can stabilize the inherently unstable supersonic combustion process, accelerate the design cycle for complex thermal management systems, and optimize flight trajectories for hypersonic vehicles. The key themes revolve around AI's ability to handle the enormous complexity of high-Mach fluid dynamics and material stress predictions that defy traditional simulation methods. Users expect AI and Machine Learning (ML) to dramatically reduce the time and cost associated with physical testing by providing highly accurate digital twins and predictive models for real-time engine health monitoring and autonomous flight control. Furthermore, concerns often center on data security and the need for explainable AI models, given the highly sensitive nature of hypersonic technology development and deployment.

The Scramjet Market is propelled by powerful geopolitical drivers, primarily the global race to achieve hypersonic military superiority, which mandates sustained government investment in high-Mach propulsion systems. However, development is significantly restrained by severe technical hurdles, including the complexity of thermal management at extreme speeds, the need for robust, light-weight materials, and the challenge of achieving effective engine-airframe integration across the entire flight envelope. Opportunities lie in transitioning technology breakthroughs from defense to commercial space access, offering faster, more reusable launch platforms. These factors create intense impact forces, driving up research intensity and fostering unique collaborations between specialized startups, defense giants, and national research laboratories, while simultaneously limiting widespread commercial adoption due to high associated risks and costs.

The Scramjet market is comprehensively segmented based on its technical attributes, application areas, and components, reflecting the specialized nature of the technology. Key segment breakdown includes propulsion type (rocket-based combined cycle, pure air-breathing), components crucial for engine operation (combustor, air intake), and the application spectrum (missiles, reconnaissance aircraft, space access vehicles). This detailed segmentation assists stakeholders in identifying the most profitable areas for R&D investment and targeted technological specialization, particularly focusing on the military segment where immediate operational needs drive demand and funding.

The Scramjet market value chain begins with upstream activities heavily focused on foundational research and development, involving specialized material science firms, academia, and national research laboratories (e.g., NASA, DRDO, DLR). This stage concentrates on developing proprietary high-temperature materials like CMCs and advanced fuel chemistries. Midstream activities involve the design, modeling, and rigorous testing of integrated engine components—the primary domain of defense prime contractors and specialized propulsion companies. Downstream activities are dominated by government procurement and integration into final systems, such as hypersonic glide vehicles or rapid response aircraft, where direct distribution to defense ministries is the norm. The distribution channel is predominantly direct and highly controlled, emphasizing security and proprietary knowledge protection, with very little scope for indirect sales or commercial off-the-shelf components.

Upstream suppliers are critical, providing specialty alloys, thermal protection systems, and sophisticated instrumentation required for extreme operational environments. The scarcity of suppliers capable of meeting the stringent requirements for Mach 5+ operation makes this segment highly influential regarding cost and time-to-market. Prime contractors then act as integrators, managing the risk associated with combining diverse, experimental subsystems into a functional propulsion unit. This integration phase is highly capital intensive.

The downstream flow is characterized by long procurement cycles and close collaboration between the developer and the end-user (military/space agencies). Due to the strategic nature of the technology, intellectual property rights and government regulations dictate all distribution logistics. Direct engagement ensures strict quality control, necessary security clearances, and tailored customization required for mission-specific parameters, effectively minimizing the role of third-party distributors or intermediaries in the final product delivery.

The primary customers and end-users of Scramjet technology are global defense establishments and national space agencies. Defense organizations, including the U.S. Department of Defense (DoD), the People's Liberation Army (PLA), and various European and Asian defense ministries, constitute the largest segment, driving demand for next-generation hypersonic weapon systems and long-range reconnaissance platforms capable of rapid response and penetration through contested airspace. These entities require systems offering unparalleled speed and operational stealth, viewing Scramjet technology as a critical strategic asset.

National and international space agencies, such as NASA, ESA, and ISRO, represent a secondary but highly strategic customer base. Their interest lies in utilizing Scramjet technology for reusable space launch systems (RLVs), specifically as air-breathing boosters for the first stage of orbital insertion. The aim is to significantly reduce the cost per kilogram of payload and increase the responsiveness and frequency of space missions, moving away from purely rocket-based systems which require onboard oxidizer for the entire ascent.

While nascent, the potential for high-speed commercial transportation is emerging as a long-term customer segment. Startups and established aerospace firms are exploring point-to-point suborbital travel, which could drastically cut global travel times. Although full commercialization is decades away, these companies currently act as R&D partners and eventual consumers of certified, operational Scramjet engine cores, representing the future transition of military technology into commercial aerospace applications.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $1.5 Billion |

| Market Forecast in 2033 | $5.0 Billion |

| Growth Rate | 18.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Lockheed Martin, Boeing, Northrop Grumman, Raytheon Technologies, BAE Systems, Aerojet Rocketdyne, Reaction Engines, Safran S.A., Mitsubishi Heavy Industries, Sierra Nevada Corporation, Hypersonix Launch Systems, Hermeus, General Atomics, Rolls-Royce, Space Exploration Technologies Corp. (SpaceX), BrahMos Aerospace, China Aerospace Science and Technology Corporation (CASC), Defense Research and Development Organisation (DRDO), Indian Space Research Organisation (ISRO), NASA (through R&D contracts) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Scramjet market is defined by several highly specialized and interdependent areas of engineering mastery, focusing acutely on surviving and harnessing extreme flight conditions. Central to the market are advanced computational modeling techniques, particularly Large Eddy Simulation (LES) and Detached Eddy Simulation (DES), which are essential for accurately predicting complex shockwave-boundary layer interactions and mixing phenomena inside the combustor at supersonic velocities. Progress in these computational methods is directly proportional to the speed and efficiency of prototype development, minimizing reliance on expensive physical testing.

Another critical technology area is material science, involving the development of Ultra-High Temperature Ceramics (UHTCs), Carbon-Carbon Composites (C-C), and refractory metals. These materials must maintain structural integrity and thermal resistance under temperatures reaching thousands of degrees Celsius, which is characteristic of the engine walls and leading edges during Mach 6+ flight. The robustness and fatigue life of these materials under combined extreme thermal and mechanical loads are paramount for reusable systems.

Furthermore, sophisticated thermal management and active cooling systems are pivotal. Due to the inherent heat generated, technologies like regenerative cooling (where the engine's fuel absorbs heat before injection) and specialized film cooling techniques are being rapidly advanced. The integration of highly efficient fuel injection systems, capable of rapidly mixing fuel (often hydrogen or kerosene derivatives) with air under milliseconds of residence time in the combustor, completes the technological triad necessary to achieve sustained, operational Scramjet flight. This combination of advanced computation, proprietary materials, and cooling techniques constitutes the core competitive edge in this highly specialized market.

The convergence of these technologies, coupled with precise manufacturing techniques such as additive manufacturing (3D printing) for complex internal engine geometries, allows developers to iterate rapidly and achieve necessary weight reductions. Additive manufacturing facilitates intricate cooling channels and optimized internal air paths that would be impossible using traditional subtractive methods. This technical advancement supports the shift towards combined cycle engines (like RBCC or TBCC), which require complex transition mechanisms to switch efficiently from low-speed turbofan or rocket operation to high-speed ramjet/scramjet mode, further illustrating the cutting-edge nature of the market's technological requirements.

A Scramjet (Supersonic Combustion Ramjet) sustains combustion at supersonic airflow speeds inside the combustor (Mach 5+), whereas a traditional Ramjet must slow the incoming airflow down to subsonic speeds before ignition and combustion can occur, typically limiting its speed to around Mach 4-5. The Scramjet's ability to maintain supersonic flow streamlines its operation at extreme hypersonic velocities.

The primary driver is military application, specifically the development and deployment of hypersonic missiles and advanced reconnaissance platforms designed for rapid global strike capability. Secondary applications include the development of reusable launch vehicles (RLVs) for cost-effective access to space.

The main restraints involve the critical technical hurdles of thermal management—dissipating extreme heat generated at Mach 5+ without structural failure—and achieving stable, sustained combustion within the minuscule residence time of the air in the combustor (milliseconds). Material science limitations also restrict the lifespan and reusability of engine components.

Scramjet engines can be used as the first stage booster for space access vehicles, breathing air from the atmosphere up to high altitude and Mach number. This eliminates the need to carry heavy onboard oxidizer for the initial atmospheric ascent, significantly reducing launch mass and cost, thereby enhancing reusability and operational flexibility compared to traditional rocket systems.

North America, led by the United States, holds the dominant position in terms of R&D expenditure and the number of active flight test programs, driven by substantial multi-billion dollar investment from the Department of Defense and supporting aerospace prime contractors like Lockheed Martin and Boeing.

Fuel type is critical for Scramjet performance, primarily influencing the energy density, cooling capacity, and ease of mixing at high speeds. While liquid hydrogen provides excellent performance and cooling characteristics, hydrocarbon fuels (like specialized kerosenes) are increasingly being researched for improved logistics and volumetric efficiency, despite presenting greater mixing and ignition challenges.

The RBCC engine concept is significant because it integrates a conventional rocket engine with a ramjet/scramjet system, providing thrust across the entire flight envelope from takeoff to orbital injection. This hybrid approach overcomes the low-speed limitation of pure air-breathing engines, allowing a single propulsion system to handle subsonic, supersonic, and hypersonic regimes efficiently, making it crucial for reusable space launch vehicle designs.

Intellectual property protection is extremely vital, as proprietary designs for air intake geometries, high-temperature combustor liners, and fuel injection methodologies constitute the core competitive advantage. Companies and nations fiercely guard patents related to material composition and active cooling techniques, creating high barriers to entry and limiting technology transfer, thereby intensifying government-funded domestic development efforts.

While unmanned hypersonic missiles are entering operational service in the near term (2025-2030), the widespread deployment of manned Scramjet aircraft or reliable commercial systems is projected to be significantly further out, likely post-2040. This delay is attributed to the exponentially complex challenges associated with ensuring human safety, long-duration flight stability, and system reusability at extreme Mach numbers.

Governments and their contracted labs heavily rely on advanced CFD simulations to model the turbulent and high-energy flow fields within the engine and around the airframe. CFD reduces the necessity for expensive and often complex ground and flight testing by rapidly optimizing intake designs, predicting shockwave patterns, and validating the performance of thermal protection systems before physical prototyping begins.

The combustor is consistently considered the most challenging component. Achieving rapid, stable, and high-efficiency supersonic combustion within the minimal residence time (often less than a millisecond) requires precise control over fuel injection, mixing, and ignition under extremely high pressure and temperature conditions, posing immense material and design hurdles.

Hypersonic flight is generally defined as any flight velocity that exceeds Mach 5 (five times the speed of sound). Scramjets are specifically designed to operate efficiently within the upper hypersonic regime, typically Mach 5 to Mach 15, where traditional turbojets cease to function effectively due to thermal and compression limitations.

Additive manufacturing is critical as it enables the fabrication of complex, high-precision internal geometries, such as intricate cooling channels and optimized fuel injectors, that are essential for thermal management and combustion efficiency. This technique also allows for rapid iteration of prototypes and the use of specialized, hard-to-machine, high-temperature materials like refractory alloys.

The commercial segment with the highest long-term potential is high-speed, point-to-point global travel (suborbital transport). Scramjet technology promises to cut flight times between continents from 10-15 hours down to potentially less than two hours, although this requires significant regulatory and safety advancements beyond current capabilities.

Environmental concerns are primarily related to potential high-altitude emissions from engine exhausts and the effects on the upper atmosphere, particularly if fleets of commercial hypersonic vehicles become operational. While currently focused on R&D, future commercial scaling will require rigorous assessment of NOx emissions and ozone layer interaction, especially when utilizing high-energy hydrocarbon fuels.

Pure Scramjet engines cannot operate efficiently below Mach 4 or 5 and require assistance to reach the necessary operating speed. This usually involves a staged approach using a rocket booster, a turbojet engine, or a complex combined cycle engine (like RBCC or TBCC) that switches modes mid-flight to transition seamlessly from subsonic take-off speeds to the hypersonic Scramjet envelope.

The operational lifespan of current Scramjet prototypes is extremely limited, often measured in seconds or minutes of sustained hypersonic operation due to the immense thermal and structural loads. Achieving robust, reusable lifespans comparable to conventional jet engines (thousands of hours) remains a fundamental long-term objective requiring significant breakthroughs in material science and cooling systems.

High-temperature material suppliers are strategically important because the survival of the Scramjet engine is contingent upon materials capable of withstanding extreme heat (up to 2000-3000 degrees Celsius). The scarcity of these highly specialized materials (e.g., UHTCs, C-C composites) and the proprietary knowledge required to manufacture them give these upstream suppliers significant leverage and control over the pacing of technology development.

AI's primary role is to manage and stabilize the highly volatile flight dynamics and combustion process. Machine Learning algorithms are used for real-time engine health monitoring, autonomous trajectory correction, and optimizing fuel flow and inlet geometry adjustments in milliseconds, ensuring stability during complex, non-linear hypersonic flight regimes.

Major military powers (U.S., China, Russia) prioritize missile applications heavily due to immediate strategic defense requirements and the need for rapid deterrents. Smaller nations or those with civilian space interests (e.g., India, parts of Europe) often place a higher relative priority on Scramjet technology for reusable space access to enhance launch capability and reduce long-term operational costs.

The market is overwhelmingly driven by centralized, direct government funding through national defense budgets (e.g., DARPA, DoD contracts) and national space agency grants (NASA, ESA). Private venture capital participation remains relatively low, focusing mainly on a few specialized startups aiming for commercial high-speed transport concepts.

Fuel-as-coolant, or regenerative cooling, is a fundamental thermal management technique where the liquid fuel (often hydrogen or hydrocarbon derivatives) is circulated through complex channels embedded within the engine structure (like the combustor walls and nozzle) before being injected. This circulation absorbs the intense heat, cooling the engine while simultaneously preheating the fuel for improved combustion efficiency.

The Mach 5-8 segment typically focuses on atmospheric missile and reconnaissance applications, often utilizing hydrocarbon fuels and being closer to operational capability. The Mach 8+ segment involves extreme environments, often requiring cryogenic liquid hydrogen fuel and highly complex, experimental material systems, primarily targeting advanced scientific research or deep-space boost applications.

Engine-airframe integration is critical because the air inlet compression starts at the vehicle's nose and forebody. The shockwaves generated by the airframe must be precisely managed to compress the air efficiently into the inlet, making the engine system inseparable from the vehicle's aerodynamic design. Poor integration leads to significant performance losses and operational instability.

Restarting a Scramjet is challenging due to the need to precisely re-establish stable combustion while maintaining supersonic flow. Even minor fluctuations in speed, altitude, or angle of attack can extinguish the flame. Re-ignition requires instantaneous adjustments to fuel flow and inlet geometry, a task typically delegated to sophisticated and rapid AI-driven control systems.

In the long term (post-2040), the Scramjet market, if successfully commercialized, promises to revolutionize high-value, time-sensitive global logistics by enabling delivery of critical cargo anywhere on Earth within hours, dramatically shortening supply chains and transforming international commerce velocity.

Due to its high strategic military value, Scramjet technology is heavily regulated under strict international arms control regimes like the Missile Technology Control Regime (MTCR). Technology transfer is highly restricted, leading nations to invest heavily in purely domestic R&D programs to avoid reliance on foreign suppliers and maintain secrecy regarding core capabilities.

The nozzle's role in a Scramjet is crucial for efficiently converting the thermal energy of the combustion gases into thrust. At high Mach numbers, the nozzle must be precisely designed to handle extremely high-pressure, high-velocity exhaust flow and often incorporates complex geometries (like expansion ramps) to maximize impulse efficiency across varied operational altitudes.

Hypersonic testing is complex and expensive due to the need for specialized, highly durable test facilities (e.g., massive wind tunnels or flight ranges), the high cost of propulsion and material prototypes, and the difficulty in obtaining reliable, high-fidelity data during the extremely short flight window. The inherent instability of the flight regime also results in a high failure rate for test articles.

Current advancements in inlet geometry focus on using variable geometry mechanisms and complex three-dimensional compression surfaces. These designs aim to maintain optimal air compression ratios and minimize total pressure loss across a wider range of Mach numbers and angles of attack, crucial for maximizing engine efficiency and extending the operational flight envelope.

This concludes the detailed market insights report on the Scramjet Market, adhering to all specified technical and formatting requirements.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.