ID : MRU_ 436337 | Date : Dec, 2025 | Pages : 255 | Region : Global | Publisher : MRU

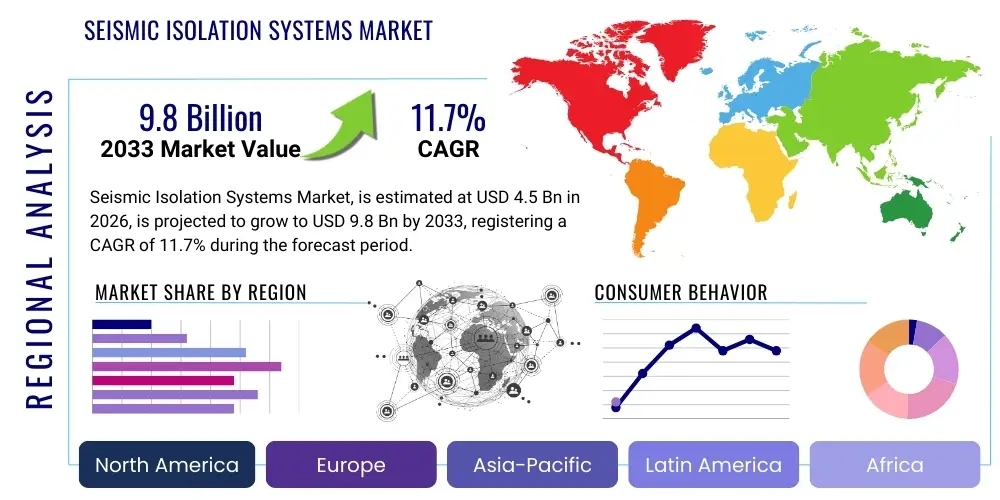

The Seismic Isolation Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.7% between 2026 and 2033. The market is estimated at $4.5 Billion in 2026 and is projected to reach $9.8 Billion by the end of the forecast period in 2033.

The Seismic Isolation Systems Market encompasses the design, manufacture, and deployment of specialized structural components engineered to decouple a structure from ground motion, particularly during seismic events. These systems function by introducing flexibility at the base of a building or structure, significantly reducing the transmission of seismic energy to the superstructure. Key products include various types of bearings—such as Lead Rubber Bearings (LRB), High Damping Rubber Bearings (HDRB), and sliding isolation systems—alongside energy dissipation devices like viscous and friction dampers. The primary objective is not only to prevent collapse but also to minimize structural damage and ensure immediate post-earthquake operability, especially crucial for critical infrastructure.

Major applications of seismic isolation systems span critical infrastructure and high-value architectural projects. This includes the robust protection of essential facilities like hospitals, emergency response centers, data centers, and power generation facilities, where uninterrupted functionality after a quake is paramount. Furthermore, significant applications are found in large-scale civil engineering projects such as long-span bridges, elevated highway systems, and liquid natural gas (LNG) tanks, where large mass and complex dynamics necessitate precise vibration mitigation strategies. The increasing urbanization in seismically active zones globally, coupled with more stringent building codes mandated by governmental regulatory bodies, fuels the adoption rate of these sophisticated protective technologies.

The market growth is primarily driven by heightened global awareness regarding seismic risk mitigation and the demonstrable efficacy of base isolation technology in saving lives and property. Benefits include reduced repair costs after an earthquake, enhanced structural resilience, and superior safety margins compared to traditional fixed-base designs. Further driving factors include technological advancements leading to the development of highly efficient, durable, and cost-effective isolation materials, alongside government investments in retrofitting existing, vulnerable infrastructure to meet modern seismic standards.

The Seismic Isolation Systems Market is experiencing robust growth, primarily propelled by increasing regulatory emphasis on earthquake-resistant construction in high-seismic regions and substantial investments in resilient infrastructure globally. Current business trends indicate a strong shift towards hybrid isolation systems that combine the benefits of different damping and isolation technologies, offering optimized performance for varying structural characteristics and regional seismic profiles. Innovation in material science, particularly the development of high-performance elastomeric compounds and advanced sliding materials, is reducing manufacturing costs and enhancing the longevity and effectiveness of isolation bearings, making these systems more commercially viable for a broader range of applications, including high-rise residential buildings.

Regional analysis highlights Asia Pacific (APAC) as the leading and fastest-growing region, driven by massive infrastructure development in countries like China, Japan, and India, which are highly susceptible to major seismic events. North America and Europe demonstrate mature markets characterized by stringent building safety standards and a focus on retrofitting aging critical infrastructure, particularly bridges and historical buildings. Latin America and the Middle East are emerging as critical growth areas due to large-scale construction booms and mandatory incorporation of seismic design principles in new projects, stimulated by significant oil and gas investments requiring robust infrastructure protection.

Segmentation trends show that the Elastomeric Bearings segment, particularly High Damping Rubber Bearings (HDRB), dominates the market share due to their proven reliability, cost-effectiveness, and ease of installation. However, the Sliding Bearings segment is anticipated to witness the highest growth rate, especially in infrastructure projects requiring significant horizontal movement capacity and high vertical load support. In terms of application, the Infrastructure segment (bridges, highways, dams) maintains a significant market presence, although the Building Construction segment is rapidly expanding as seismic isolation moves beyond just critical facilities into general commercial and high-end residential developments.

User inquiries regarding the impact of Artificial Intelligence (AI) on the Seismic Isolation Systems Market primarily revolve around how AI can enhance design optimization, predictive maintenance, and real-time monitoring of isolated structures. Common questions address the use of machine learning (ML) algorithms for simulating complex seismic responses under various scenarios, thereby optimizing bearing characteristics and damper placement with greater precision than traditional finite element methods. Users also express interest in AI-driven structural health monitoring (SHM) systems that can predict potential component failure or degradation, ensuring timely intervention and maximizing the service life of isolation hardware. The key themes summarized from user concerns are the precision gains in design, the efficiency of deployment, and the ability of AI systems to process vast sensor data for immediate post-earthquake assessment and vulnerability mapping.

AI’s influence is moving beyond theoretical modeling into tangible operational improvements. For instance, AI algorithms are being integrated into Building Information Modeling (BIM) platforms to automatically evaluate thousands of isolation system configurations based on site-specific soil data, structural type, and targeted performance levels, leading to significant time and cost savings in the design phase. Furthermore, the development of 'smart' seismic isolation systems is contingent upon AI; these systems utilize integrated sensors feeding data into neural networks to potentially adjust damping forces or stiffness parameters instantaneously during a seismic event, offering adaptive resilience which is a major leap forward from passive isolation technologies.

The long-term expectations suggest that AI will democratize high-performance seismic design. By automating complex calculations and incorporating probabilistic risk assessments, AI tools will allow engineering firms of all sizes to implement highly sophisticated isolation strategies previously restricted to large, specialized consultancies. This integration will drive standardization while simultaneously fostering customization, ensuring that isolation systems are perfectly tailored to local seismic hazards and minimizing over-engineering or inadequate protection. This synergy between physical engineering and computational intelligence is crucial for the next generation of resilient structures.

The dynamics of the Seismic Isolation Systems Market are fundamentally shaped by a confluence of strong regulatory drivers and technical constraints, alongside significant opportunities in emerging economies and retrofitting projects. The primary driver is the accelerating frequency and severity of global seismic events, which pushes governments and private developers to prioritize structural resilience. Regulatory mandates, such as updated Eurocodes and International Building Codes (IBC), are increasingly making base isolation a standard consideration, especially for essential facilities. Conversely, the high initial capital expenditure associated with these systems, particularly when compared to conventional reinforced concrete structures, acts as a significant restraint, often leading developers in cost-sensitive markets to opt for lower-cost, fixed-base designs, despite the long-term benefits of isolation.

Opportunities for growth are vast, centered around the massive infrastructure needs of rapidly urbanizing regions in Asia Pacific and Latin America, where population density intersects with high seismic risk. The retrofitting market also presents a lucrative pathway, targeting existing vulnerable infrastructure like hospitals, heritage sites, and major transport bridges that require upgrading to modern seismic standards without full replacement. The key challenge lies in the specialized engineering expertise required for design, installation, and inspection of these systems, which presents a market entry barrier for smaller construction firms and necessitates continuous education and training across the industry.

The market is further influenced by Porter’s Five Forces analysis, demonstrating high bargaining power of suppliers for specialized materials (e.g., high-quality natural rubber, PTFE) but moderate rivalry among manufacturers due to the technological complexity and high barrier to entry. The threat of substitutes is low, as seismic isolation offers a unique, superior level of protection unmatched by traditional damping or shear wall construction. However, the bargaining power of buyers (large government infrastructure departments and major developers) is significant, demanding high quality, proven performance, and long-term warranties. Technological innovation and standardization are critical impact forces determining future market structure and competitive advantage among key players.

The Seismic Isolation Systems Market is structurally segmented based on the mechanism of isolation, the components' material composition, and the diverse end-use applications they serve. Understanding these segments is crucial for manufacturers to target their R&D investments and marketing strategies. Segmentation by type reflects the operational principles—ranging from simple elastomeric pads that offer flexibility to complex sliding mechanisms providing friction damping and energy dissipation devices that absorb kinetic energy. The application segmentation clearly delineates the demand derived from civil engineering needs (infrastructure) versus vertical construction needs (buildings), each having distinct performance requirements related to vertical load capacity, horizontal displacement allowance, and lifespan expectation.

The market analysis reveals that segmentation by material is increasingly significant due to advances in polymer science and metallurgy. High-performance materials are essential for ensuring durability, reliability, and specific mechanical properties required by stringent performance standards. For instance, the demand for high-quality natural rubber used in Lead Rubber Bearings (LRB) is heavily driven by building regulations that mandate specific yield strength and damping capabilities. Similarly, the segment incorporating high-grade steel and advanced PTFE (Polytetrafluoroethylene) finds immense applicability in bridge and infrastructure bearings where heavy loads and significant thermal expansion/contraction must be accommodated alongside seismic movement.

The complexity within the market segmentation underscores the need for highly customized solutions. Unlike mass-produced construction materials, seismic isolation systems are often bespoke engineered solutions designed for specific site conditions and structural requirements. This customization drives higher average selling prices and reinforces the necessity of specialized engineering consultation as part of the product offering, solidifying the market’s reliance on expert knowledge across all major segment categories.

The value chain for the Seismic Isolation Systems Market begins with specialized raw material procurement and highly technical manufacturing, extending through detailed engineering consulting, distribution, and complex, site-specific installation. Upstream analysis focuses on the sourcing of critical materials such as high-grade natural rubber, specialized steel plates for laminates, and advanced polymers like PTFE. Suppliers of these components wield moderate power, as the quality and certification of these inputs are non-negotiable for system performance and longevity. The manufacturing stage requires precision engineering, vulcanization processes, and rigorous quality control testing to ensure the bearings and dampers meet specific load and displacement capacities demanded by structural engineers.

Midstream activities involve the design and consulting phase, which is perhaps the most critical component of value creation. Structural engineers and specialist consultants translate project requirements into specific isolation system specifications. Manufacturers often collaborate closely with these consultants, sometimes providing integrated design-supply services. Distribution channels are typically direct or utilize highly specialized construction material distributors rather than broad-market channels, given the technical nature and high value of the products. Direct channels are favored for large infrastructure projects, allowing manufacturers to maintain tight control over logistics and quality assurance.

Downstream analysis centers on installation and post-installation services. Installation is complex, requiring specialized lifting equipment and detailed construction sequencing, often managed by skilled contractors. Post-sales services include routine inspection, structural health monitoring (increasingly incorporating AI), and the provision of long-term warranties. The dominance of direct sales in major projects ensures that manufacturers maintain a significant level of influence throughout the installation and operational lifecycle, reinforcing quality control and capturing high-margin service revenues.

The primary end-users and buyers of seismic isolation systems are government bodies and large private development corporations responsible for critical and high-value assets in seismically active areas. Government departments, specifically Ministries of Transportation, Public Works, and Infrastructure Development, constitute a major customer base, particularly for applications concerning bridges, highways, rail networks, and public utilities such as water treatment plants and electrical substations. The need for operational continuity during disaster scenarios makes these entities primary targets for advanced isolation solutions, favoring technologies with proven long-term performance and minimal maintenance requirements.

In the private sector, potential customers include healthcare corporations investing in hospital infrastructure, large technology firms building critical data centers, and energy companies constructing industrial facilities like LNG storage tanks and nuclear power plants. These sectors prioritize performance over initial cost, driven by the enormous financial and societal consequences of system failure or downtime following a seismic event. Furthermore, architectural firms specializing in iconic, high-rise, or historical building preservation are significant purchasers, as isolation systems allow for superior architectural flexibility and protection without resorting to overly massive or aesthetically compromising structural members.

The emerging customer demographic includes high-end residential developers in regions like California, Japan, and New Zealand, where the demand for absolute safety and asset protection justifies the premium cost of base isolation in luxury properties. These buyers are motivated by market differentiation, offering 'seismic resilience' as a key selling feature, thereby broadening the market beyond traditional critical infrastructure applications into the luxury consumer segment. Customization and integration with 'smart building' technologies are key requirements for attracting this consumer segment.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $4.5 Billion |

| Market Forecast in 2033 | $9.8 Billion |

| Growth Rate | 11.7% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Bridgestone Corporation, Trelleborg AB, Fip Industriale S.p.A., Earthquake Protection Systems Inc., Maurer SE, GERB Schwingungsisolierungen GmbH, Robinson Seismic Ltd., Kawakin Core-Tech Co., Ltd., R. C. Insulators Inc., Damping Technologies, Inc., Sanwa Tekki Corporation, OILES Corporation, Zhongjing New Material Co., Ltd., OVM Group, VSL International AG, CIVEA SpA, Zaoqiang Dacheng Rubber Co., Ltd., Cosmo Kogyo Co., Ltd., Aviles Manufacturing Corp., Disys Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Seismic Isolation Systems Market is characterized by continuous refinement in passive isolation techniques and incremental advancements towards semi-active and active control systems. Passive systems, which include Lead Rubber Bearings (LRB) and High Damping Rubber Bearings (HDRB), remain the industry standard. Recent technological improvements focus on enhancing the material science of the elastomers, such as developing compounds that offer better low-temperature performance, increased durability against ozone and UV exposure, and higher damping ratios without compromising flexibility. This refinement aims to extend the service life of these components beyond 100 years, meeting the longevity demands of critical infrastructure like major bridges and long-term public facilities.

A significant area of technological evolution is the hybrid isolation approach, integrating multiple component types to achieve optimal performance. For instance, combining Friction Pendulum Systems (FPS) with Fluid Viscous Dampers allows engineers to control both displacement capacity and energy dissipation rate more precisely. FPS technology itself is evolving, with advances in multi-concave sliders and specialized low-friction materials enabling much larger displacement capacities and re-centering forces, which are essential for structures facing very high seismic hazards or requiring extremely low levels of acceleration transmission to sensitive internal equipment (e.g., data centers).

Looking forward, the integration of smart technologies is shaping the next wave of innovation. This includes the development of sensors embedded directly within the isolation bearings or dampers, enabling real-time structural health monitoring and immediate post-earthquake assessment. Furthermore, research into semi-active systems, utilizing magnetorheological (MR) or electrorheological (ER) fluid dampers, aims to provide adaptive stiffness and damping characteristics. While these technologies are currently expensive and complex, they represent a technological frontier that promises optimal, structure-specific seismic response tailored moment-by-moment during an earthquake, offering unparalleled resilience and control.

The Asia Pacific region currently dominates the global Seismic Isolation Systems Market and is anticipated to maintain the fastest growth rate throughout the forecast period. This dominance is directly linked to the high frequency of major earthquakes, particularly across the Pacific Ring of Fire, affecting densely populated nations like Japan, China, Indonesia, and the Philippines. Regulatory environments, especially in Japan and New Zealand, are highly mature, often mandating the use of advanced seismic countermeasures for critical facilities and high-rise structures, thereby driving consistent demand for high-quality isolation products. China’s substantial investments in urbanization and large-scale infrastructure projects—including high-speed rail networks, massive bridge construction, and commercial complexes—have positioned it as a colossal market for both elastomeric and sliding isolation bearings.

A key trend in APAC is the focus on hybrid systems and localized manufacturing. To reduce costs and lead times, local manufacturers in India and China are scaling up production capabilities, often under technology transfer agreements with established global leaders. The market in South Korea and Taiwan is characterized by strong adoption in advanced technology manufacturing facilities, where minimizing vibration and ensuring production continuity is critical. This region's growth is sustained not only by new construction but also by governmental programs dedicated to retrofitting older, seismically vulnerable schools, hospitals, and heritage structures, ensuring a diversified demand portfolio across public and private sectors.

The North American market, concentrated primarily in the US (especially California, Alaska, and the Pacific Northwest) and parts of Canada, represents a highly mature market characterized by stringent performance requirements and a strong emphasis on professional liability and long-term reliability. Adoption rates are exceptionally high for critical facilities such as hospitals (mandated by OSHPD regulations in California), major transportation infrastructure (bridges, elevated highways), and high-value commercial and data center constructions. Lead Rubber Bearings (LRB) and Friction Pendulum Systems (FPS) are the preferred technologies, valued for their proven performance during significant seismic events over the past three decades.

The current market focus in North America is increasingly shifting towards the retrofitting segment. Numerous aging highway bridges, many constructed decades ago, are now undergoing extensive seismic upgrade programs to meet modern resilience standards. Furthermore, the market benefits from the intellectual property and R&D capabilities concentrated within US institutions, driving innovation in advanced materials and monitoring technologies. While new construction remains steady, the high cost of specialized labor and materials compared to APAC often means that isolation systems are reserved for truly critical or high-value projects where the cost justification for superior resilience is undeniable.

The European market for seismic isolation is governed by the Eurocode 8 standards, focusing primarily on countries in the Mediterranean region (Italy, Greece, Turkey, Romania) which experience high seismic activity. Italy and Turkey are key markets, showing robust growth driven by mandatory seismic design requirements for public buildings and the reconstruction efforts following recent destructive earthquakes. The application scope often includes the use of isolation for preserving historical and architectural heritage structures, where decoupling the massive superstructure from ground movement is essential to prevent internal damage without altering the building's facade or structural integrity.

The challenge in Europe lies in the fragmented nature of the construction market and diverse national interpretations of Eurocode requirements. However, the consistent long-term investment in transnational infrastructure, such as bridges and tunnels connecting various parts of the continent, ensures a reliable demand stream for large-scale isolation components. Manufacturers in Europe often emphasize specialized, custom-engineered solutions that meet demanding architectural constraints and site-specific geological conditions, positioning the European market as a hub for highly customized and specialized high-damping technologies.

LAMEA represents the emerging frontier for seismic isolation, characterized by accelerating infrastructure development and growing awareness of seismic risk. Latin American countries, particularly Chile, Peru, and Mexico, are rapidly adopting isolation technologies, driven by their location along major fault lines and increasing regulatory oversight. Chile, with its history of severe earthquakes, is often cited as a leader in mandated seismic resilience for new construction, mirroring the mature markets of North America and Japan.

In the Middle East and Africa, the demand is primarily concentrated in industrial and critical infrastructure projects, particularly in oil, gas, and power generation facilities, notably in regions like Saudi Arabia and the UAE. While seismic hazard might be lower than in the Pacific Rim, the immense value of these industrial assets justifies the use of sophisticated isolation systems to ensure operational continuity. The growth driver here is primarily driven by international engineering consultants adhering to global best practices (such as ASCE and Eurocodes) for designing high-value, long-lifespan facilities, even if local building codes are less stringent. However, market penetration is slower due to limited local manufacturing capabilities and the reliance on imports for high-end systems.

The primary function of seismic isolation systems, often called base isolation, is to decouple a structure from the intense horizontal ground motions caused by an earthquake. By introducing a flexible layer (like specialized bearings) between the foundation and the superstructure, the system significantly lengthens the structure's natural period of vibration. This shift in period moves the structure out of resonance with the typical destructive frequencies of seismic waves, dramatically reducing the acceleration forces transmitted up through the building. The key benefit is enhanced structural resilience and reduced damage, ensuring the building remains functional immediately after a major seismic event, which is crucial for hospitals and data centers. Furthermore, isolation minimizes damage to non-structural elements and sensitive internal equipment, offering superior asset protection compared to conventional fixed-base designs.

The main types of seismic isolation bearings are categorized into Elastomeric Bearings and Sliding Isolation Systems. Elastomeric Bearings, such as Lead Rubber Bearings (LRB) and High Damping Rubber Bearings (HDRB), consist of laminated layers of rubber and steel plates. LRBs incorporate a lead core to provide high damping (energy absorption) while the rubber offers flexibility and re-centering capability. HDRBs use special rubber compounds to achieve energy dissipation, eliminating the need for a lead core. Sliding Isolation Systems, like the Friction Pendulum System (FPS), work on the principle of friction and curvature. FPS uses curved sliding surfaces, allowing large displacements while the friction dissipates energy and gravity provides the powerful re-centering force. The choice between these systems depends on the structure's height, weight, and the target performance level, balancing damping, flexibility, and displacement capacity.

The initial installation cost of seismic isolation systems is significantly higher—often 5% to 15% more than conventional construction—primarily due to the specialized hardware, complex foundation design, and required engineering expertise. However, this high upfront investment is typically offset by drastically reduced repair costs, faster recovery times, and minimized downtime after a major earthquake. For critical facilities, the life-cycle cost analysis often favors isolation systems due to these resilience benefits. Seismic isolation is highly suitable and increasingly common for retrofitting existing structures, particularly historically significant buildings, hospitals, and bridges. Retrofitting involves installing isolation bearings either at the foundation level or at specific points along the structure. While challenging due to the need to temporarily support the structure during installation, retrofitting extends the useful life of the asset and brings it up to modern seismic performance standards without complete demolition and rebuild.

The Asia Pacific (APAC) region currently drives the highest global demand and exhibits the fastest market growth rate. This is largely due to the high population density and concentration of critical infrastructure in seismically active zones, especially along the Pacific Ring of Fire (Japan, China, Indonesia). Government mandates in countries like Japan and New Zealand enforce rigorous seismic safety standards, ensuring constant investment in advanced isolation technologies. China's enormous scale of infrastructure projects, including high-speed rail and commercial towers, also contributes significantly to this demand. North America, particularly the West Coast of the US, remains a mature market characterized by high standards, but APAC’s pace of new construction and infrastructural development positions it as the dominant region for future market expansion and technological deployment.

Advanced technology, particularly AI and smart monitoring systems, is crucial for the future evolution of seismic isolation. AI is being deployed in the design phase, utilizing machine learning algorithms to optimize bearing selection and placement, efficiently analyzing thousands of site-specific seismic simulations to achieve the most cost-effective and highest-performing design. Smart monitoring involves embedding sensors (IoT devices) within isolation bearings and dampers to continuously track their health, identify subtle degradation, and predict maintenance needs, transitioning the industry from reactive to predictive maintenance strategies. Furthermore, research is focused on integrating AI with semi-active dampers, creating adaptive isolation systems that can adjust their stiffness and damping characteristics in real-time during an earthquake, maximizing the protective effect based on the incoming ground motion characteristics. This integration promises a higher degree of engineered resilience.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.