ID : MRU_ 438849 | Date : Dec, 2025 | Pages : 245 | Region : Global | Publisher : MRU

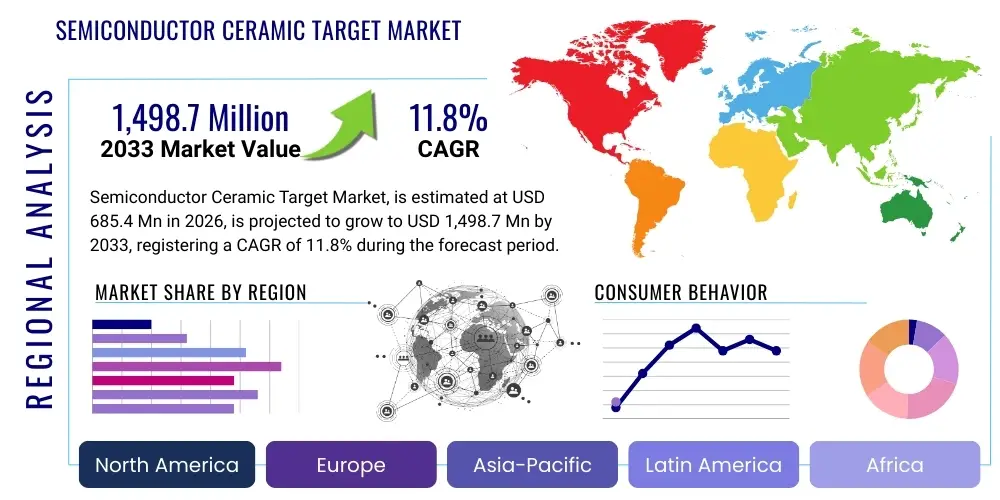

The Semiconductor Ceramic Target Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.8% between 2026 and 2033. The market is estimated at USD 685.4 Million in 2026 and is projected to reach USD 1,498.7 Million by the end of the forecast period in 2033.

The Semiconductor Ceramic Target Market encompasses the manufacturing and distribution of specialized ceramic materials used as sputtering targets in physical vapor deposition (PVD) processes critical for semiconductor fabrication. These targets are essential precursors for depositing thin films of metallic, dielectric, or protective materials onto silicon wafers, forming the foundational layers of integrated circuits (ICs), advanced memory chips (DRAM, NAND), and micro-electro-mechanical systems (MEMS). Ceramic targets, often composed of materials like alumina (Al2O3), titanium oxide (TiO2), silicon nitride (Si3N4), or specialized complex oxides, are valued for their exceptional purity, density, mechanical stability, and thermal resilience, ensuring film uniformity and minimizing defects during the high-vacuum deposition process.

Product descriptions emphasize ultra-high purity (>99.999%), fine grain structure, and customized geometries designed to integrate seamlessly with various PVD tools, including magnetron sputtering systems used extensively in high-volume production lines. Major applications span critical semiconductor manufacturing steps, including barrier layers, contact plugs, advanced interconnects, and specialized packaging technologies. The demand is intrinsically linked to the increasing complexity of chip architecture, the relentless drive toward miniaturization (sub-10nm nodes), and the proliferation of advanced computing devices requiring high-performance ICs, such as those used in 5G infrastructure, electric vehicles, and high-performance computing (HPC) data centers.

Key benefits driving market adoption include the ability of ceramic targets to produce films with superior stoichiometry and adhesion compared to traditional metallic targets in specific applications, particularly for complex dielectric stacks. The driving factors involve robust global investments in advanced fabrication facilities (fabs), particularly in the Asia Pacific region, accelerated demand for next-generation memory and logic chips, and technological advancements enabling high-speed data processing and energy-efficient computing. Furthermore, the shift towards wider bandgap semiconductor materials (like SiC and GaN) for power electronics necessitates specialized ceramic deposition precursors, further diversifying the application landscape and driving innovation within the target manufacturing ecosystem.

The Semiconductor Ceramic Target Market is experiencing vigorous expansion, primarily driven by tectonic shifts in the global technology landscape, particularly the expansion of high-performance computing and the ongoing digital transformation accelerated by 5G deployment and the Internet of Things (IoT). Business trends indicate a strong focus on strategic vertical integration and specialized material science innovation, as chipmakers demand increasingly complex, defect-free deposition materials for sub-7nm node manufacturing. Key manufacturers are prioritizing enhanced purity levels and tight compositional control to meet stringent specifications required for extreme ultraviolet (EUV) lithography infrastructure and advanced packaging technologies, fostering intense R&D investment aimed at developing novel multi-component ceramic compositions.

Regional trends highlight the dominance of the Asia Pacific (APAC) region, specifically countries such as China, South Korea, Taiwan, and Japan, which collectively host the vast majority of global semiconductor fabrication capacity. Massive governmental subsidies and private sector investments pouring into establishing domestic semiconductor supply chains, notably in China and the US (through the CHIPS Act), are fueling unprecedented demand for high-quality ceramic sputtering targets. North America and Europe, while smaller in production volume, represent critical hubs for innovation and advanced material development, focusing on specialized, high-margin niche applications like power semiconductors and defense electronics, thereby maintaining a strong influence on technological standards.

Segment trends reveal that the Logic and Memory fabrication sectors remain the largest consumers, with the transition to 3D NAND and next-generation DRAM requiring complex dielectric films deposited using ceramic targets, driving volume demand significantly. Furthermore, segmentation by material type shows strong growth in high-purity complex oxide targets (e.g., HfO2, ZrO2) used for high-k gate dielectrics and ferroelectric materials, reflecting the ongoing evolution towards materials with higher dielectric constants. Supply chain stability, raw material scarcity, and geopolitical risks associated with critical minerals continue to influence procurement strategies, pushing buyers toward diversified sourcing and long-term supply agreements with established, high-reliability suppliers capable of ensuring consistent quality and volume.

User inquiries concerning the impact of Artificial Intelligence (AI) on the Semiconductor Ceramic Target Market frequently center around two major themes: the dramatic increase in demand for advanced chips that power AI applications, and the application of AI and Machine Learning (ML) techniques within the target manufacturing process itself. Users are primarily concerned with how generative AI, high-performance computing (HPC), and accelerated computing architectures will translate into specific material volume requirements, particularly for GPUs, TPUs, and specialized AI accelerators that rely on dense, high-efficiency ICs. A key concern is whether the current manufacturing capacity for ultra-high purity targets can scale quickly enough to meet the exponential growth in AI data centers and edge device deployment, potentially creating supply bottlenecks.

Furthermore, there is significant interest in how AI can optimize the complex, sensitive process of ceramic target production. Questions often address the use of ML algorithms for predictive maintenance on sputtering equipment, optimizing sintering profiles to achieve desired density and grain size uniformity, and ensuring real-time quality control checks for material purity and defect detection. Users expect AI integration to enhance manufacturing yield, reduce material waste, and accelerate the development cycle for new, complex ceramic compositions required for future AI hardware generations, establishing a feedback loop where AI drives chip demand and simultaneously refines the manufacturing supply chain.

The dynamics of the Semiconductor Ceramic Target Market are shaped by a complex interplay of Drivers (D), Restraints (R), Opportunities (O), and structural Impact Forces. The primary driver is the accelerating proliferation of advanced electronics across consumer, industrial, and automotive sectors, underpinned by the global deployment of 5G, the rapid growth of cloud computing infrastructure, and the massive data generation associated with IoT. This drives relentless demand for more powerful, smaller, and energy-efficient semiconductor chips, directly necessitating ultra-high purity ceramic targets for critical deposition processes. Opportunities abound in the development of targets for emerging materials like ferroelectric HfO2 and specialized targets for advanced packaging techniques such as fan-out wafer-level packaging (FOWLP) and 3D stacking, enabling manufacturers to capture high-margin niches.

However, the market faces significant restraints. The exceptionally high barrier to entry due to the stringent purity requirements, demanding capital expenditure for manufacturing facilities, and the necessity for deep material science expertise limits competition. Furthermore, the volatility and concentrated nature of the raw material supply chain—specifically for high-purity metals and rare earth oxides—pose risks to production costs and supply consistency. Geopolitical tensions and trade restrictions impacting the global semiconductor supply chain introduce substantial uncertainty, requiring localized manufacturing redundancies which often increase operational expenses, tempering potential growth rates despite underlying high demand.

Impact forces, especially technological advancements and competitive intensity, exert considerable pressure. Moore’s Law dictates continuous scaling and material innovation, forcing ceramic target producers to constantly refine microstructure, density, and purity to meet successive technology node requirements (e.g., 3nm, 2nm). Competitive dynamics are characterized by global oligopolistic structures where a few key players dominate due to their established intellectual property and deep relationships with major foundries (TSMC, Samsung, Intel). This competitive force encourages continuous process optimization and R&D investment but makes it challenging for new entrants to gain traction, ultimately stabilizing the market structure while ensuring rapid material evolution.

The Semiconductor Ceramic Target Market is meticulously segmented based on material composition, application area, and end-user industry, reflecting the specialized requirements of the semiconductor fabrication process. Segmentation by material is crucial, as the performance and purity of the deposited thin film are directly linked to the target precursor. Key materials include various pure ceramics (like alumina and silicon nitride) and complex oxides (like hafnium oxide and zirconium oxide), each serving unique functions, such as acting as high-k dielectrics or specialized barrier layers. The end-user classification, particularly distinguishing between integrated device manufacturers (IDMs) and foundries, dictates purchasing volumes and specification rigidity, with foundries typically demanding targets compatible with diverse client specifications.

Application-based segmentation is critical for market sizing and strategy development. The largest segment remains the fabrication of Logic and Memory chips, which are the fundamental building blocks of almost all digital devices. However, specialized sectors like Power Electronics (driven by SiC/GaN) and MEMS (used in sensors and actuators) represent fast-growing, high-value segments requiring custom target formulations optimized for non-traditional wafer materials or unique deposition environments. Understanding this multilayered segmentation allows market players to focus their R&D efforts on materials that address the bottleneck challenges associated with next-generation semiconductor device architecture, ensuring market relevance and sustaining premium pricing structures.

The value chain for the Semiconductor Ceramic Target Market is highly specialized and sequential, commencing with the rigorous upstream processing of ultra-high purity (UHP) raw materials. Upstream analysis focuses on securing the supply of critical metal oxides and compounds, which must undergo extensive purification processes, often involving chemical synthesis, precipitation, and thermal treatments, to achieve the necessary five-nines (99.999%) purity essential for semiconductor applications. Key suppliers in this phase are specialized chemical and advanced materials companies that possess proprietary purification technologies. The quality and cost of these raw materials critically determine the final target performance and manufacturing yield, making long-term strategic sourcing partnerships essential.

The midstream phase involves the sophisticated manufacturing of the ceramic targets themselves, which includes powder compaction, high-temperature sintering, and specialized machining to precise specifications. This phase demands advanced manufacturing equipment, cleanroom environments, and intensive intellectual property related to grain structure control and bonding techniques (e.g., target bonding to backing plates). Distribution channels are primarily direct, involving tight cooperation between the target manufacturer and the end-user (foundries or IDMs). Direct sales ensure technical support, customized specifications, and secure supply chain logistics, reflecting the mission-critical nature of the component in high-cost fabrication environments.

Downstream analysis centers on the integration of these targets into PVD systems within fabrication facilities. The end-users require targets that deliver optimal film quality, high utilization efficiency, and predictable lifespan. While direct channels dominate, specialized distributors and agents sometimes handle sales for smaller or regional foundries, particularly in emerging markets. The feedback loop from the downstream users—concerning target erosion, film defects, and sputtering rate stability—is crucial for upstream innovation, driving continuous improvement in target composition and manufacturing processes. The high investment in R&D and quality control at every stage underscores the highly technical, low-volume, high-value nature of this market.

The primary potential customers and end-users of Semiconductor Ceramic Targets are global semiconductor manufacturing entities, which can be broadly categorized into pure-play foundries, Integrated Device Manufacturers (IDMs), and, to a lesser extent, specialized outsourced assembly and test (OSAT) providers focusing on advanced packaging. Foundries, such as TSMC, Samsung Foundry, UMC, and GlobalFoundries, represent the largest volume purchasers. These companies operate massive fabrication plants (fabs) and require diverse portfolios of targets to satisfy the varied deposition needs of their global client base, which spans logic, memory, and specialized IC production, necessitating bulk orders and strict adherence to industry standards.

IDMs, including tech giants like Intel, Micron, SK Hynix, and Texas Instruments, also constitute a significant customer base. Unlike foundries, IDMs manufacture chips primarily for their own product lines, demanding targets customized for their proprietary process flows and advanced memory (NAND/DRAM) or logic architectures. Their purchasing decisions are highly centralized and focused on materials that enhance performance and yield within their specific, often cutting-edge, manufacturing nodes. The adoption of advanced packaging techniques further expands the customer base to OSAT companies needing targets for depositing underfill and protection layers.

Beyond the core silicon industry, key customers include manufacturers of power electronics (e.g., using SiC and GaN materials for electric vehicles and renewable energy infrastructure), advanced optical devices, and sophisticated MEMS sensors used in automotive and medical applications. These specialized end-users often require niche, high-performance ceramic compositions not typically used in mass-market silicon, driving demand for customizable, low-volume, high-specification targets from specialized material suppliers. The critical nature of these components means purchasing cycles are long, based heavily on demonstrated material performance, technical support, and proven ability to maintain ultra-high purity consistency over extended supply contracts.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 685.4 Million |

| Market Forecast in 2033 | USD 1,498.7 Million |

| Growth Rate | 11.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | JX Nippon Mining & Metals, Praxair Surface Technologies, Materion, Honeywell Electronic Materials, Umicore, Tosoh SMD, Plansee SE, H.C. Starck Solutions, AGC Inc., CeramTec, Lesker Company, Kurt J. Lesker Company, Mitsubishi Materials, JSR Corporation, JMC Corporation, Fuji Electric Co., Ltd., Shin-Etsu Chemical Co., Ltd., Sumitomo Chemical Co., Ltd., CoorsTek, Inc., J.P. Nystrom AB |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Semiconductor Ceramic Target Market is defined by the relentless pursuit of superior material purity and physical properties, necessary to facilitate high-yield deposition processes for increasingly smaller feature sizes (down to 3nm and below). A key technology is the utilization of advanced powder metallurgy techniques, including highly controlled wet chemical synthesis and co-precipitation methods, to produce precursor powders with nano-scale particle size uniformity and exceptional elemental purity, often exceeding 99.999%. These techniques are critical for preventing the formation of macro-defects and ensuring the resulting thin films deposited on the wafer possess consistent electrical and structural characteristics, directly impacting chip performance and reliability.

Another crucial technological area involves high-density forming and high-temperature sintering processes. Techniques such as Hot Isostatic Pressing (HIP) and Vacuum Sintering are employed to achieve theoretical maximum density in the ceramic targets, which is vital for minimizing internal porosity. Reduced porosity translates directly to smoother sputtering rates, reduced particle generation (arcing), and extended target life, all essential metrics in a high-volume manufacturing environment. Furthermore, specialized bonding technologies, typically using exotic solders or diffusion bonding methods, are necessary to securely attach the brittle ceramic target to a copper or aluminum backing plate for efficient thermal management and mechanical stability within the PVD chamber.

The emerging technological focus is on developing multi-component or composite ceramic targets designed for complex, stack-layer depositions used in advanced 3D NAND and next-generation logic devices. This requires mastering complex stoichiometry control to ensure that multiple elements are transferred precisely during the sputtering process. Furthermore, the industry is witnessing the integration of smart manufacturing, leveraging sensor technology and data analytics to monitor and optimize every step of the target production process—from raw material blending to final polishing—enhancing traceability and predictive quality control, thereby aligning target manufacturing precision with the strict demands of leading-edge semiconductor lithography and deposition cycles.

Regional analysis reveals a distinct concentration of demand in areas with robust semiconductor fabrication capabilities, while R&D and high-purity material sourcing remain geographically diverse, creating complex supply chain dynamics that influence market stability and pricing.

The primary ceramic materials include ultra-high purity Alumina (Al2O3), Silicon Nitride (Si3N4), Silicon Dioxide (SiO2), Titanium Oxide (TiO2), and complex functional oxides like Hafnium Oxide (HfO2) and Zirconium Oxide (ZrO2), crucial for high-k dielectrics and specialized barrier layers.

Ultra-high purity (>99.999%) is mandatory to prevent defects, contamination, and electrical failure in sub-10nm chip architectures. Impurities even at the parts-per-million level can compromise the integrity and electrical performance of thin films, leading to low manufacturing yields.

The Memory Device Fabrication segment, encompassing both DRAM and 3D NAND flash, typically drives the highest volume demand due to the complex, multi-layered dielectric stacks required in advanced memory cell architectures and their high manufacturing throughput requirements.

Advanced packaging technologies, such as FOWLP and 3D integration, necessitate specialized deposition processes for stress-buffer and interconnect layers, thereby increasing the demand for ceramic targets optimized for lower temperature PVD processes and complex composite materials.

APAC is the largest consuming region globally, accounting for the majority of market share due to the highest concentration of global semiconductor fabrication capacity, particularly in Taiwan, South Korea, and Mainland China, fueled by massive ongoing capacity expansion projects.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.