ID : MRU_ 434910 | Date : Dec, 2025 | Pages : 242 | Region : Global | Publisher : MRU

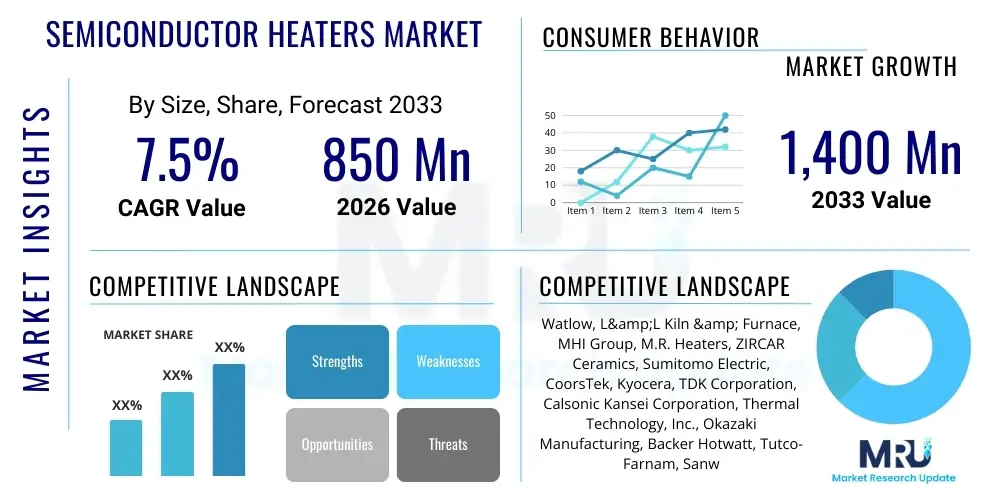

The Semiconductor Heaters Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.5% between 2026 and 2033. The market is estimated at USD 850 million in 2026 and is projected to reach USD 1,400 million by the end of the forecast period in 2033.

The Semiconductor Heaters Market encompasses specialized thermal management components critical for maintaining precise temperature uniformity and stability during various semiconductor manufacturing processes, including deposition (CVD, PVD, ALD), etching, ion implantation, and thermal annealing. These high-precision heating elements, often custom-designed using advanced materials like quartz, aluminum nitride (AlN), silicon carbide (SiC), and specialized alloys, are essential for ensuring the structural integrity, electrical performance, and overall yield of integrated circuits (ICs). The relentless pursuit of miniaturization, particularly the transition to sub-10nm fabrication nodes and the increasing complexity of 3D device architectures such as 3D NAND and FinFETs, mandates stringent thermal control, directly driving the demand for sophisticated, reliable, and energy-efficient semiconductor heating solutions. Product innovation focuses heavily on achieving faster thermal ramp-up and cool-down rates, extended operational lifecycles under extreme vacuum or corrosive chemical environments, and exceptional temperature uniformity across large wafer surfaces to minimize defects during critical process steps.

Semiconductor heaters function primarily to facilitate chemical reactions, control material deposition rates, and activate dopants within the silicon wafer structure. For instance, in Atomic Layer Deposition (ALD) and Chemical Vapor Deposition (CVD), precise temperature regulation is paramount for dictating the film thickness and material properties being deposited onto the wafer. Any deviation in temperature uniformity can lead to inconsistencies in film stress, non-uniform layer thicknesses, and ultimately, a reduced yield of functional dies. Major applications are concentrated within semiconductor fabrication facilities (fabs) and original equipment manufacturers (OEMs) specializing in semiconductor processing equipment. The foundational benefits of these advanced heaters include vastly improved process repeatability, enhanced wafer throughput due to faster thermal cycling capabilities, and a significant reduction in device manufacturing costs associated with defects. Furthermore, the adoption of wide-bandgap (WBG) materials like SiC and GaN, which require extremely high-temperature processing, is accelerating the development of specialized, ultra-high-temperature resistant heating elements.

Driving factors for sustained market growth include unprecedented global investment in new fabrication plant construction, particularly in Asia Pacific and increasingly in North America and Europe, supported by government initiatives aimed at strengthening domestic chip supply chains. The proliferation of advanced electronic devices across consumer electronics, automotive, industrial IoT, and data center infrastructure is necessitating higher performance chips, thus fueling the requirement for more advanced, high-precision thermal solutions. Additionally, the shift toward larger wafer sizes (e.g., 300mm and the eventual potential for 450mm) increases the complexity of maintaining uniform temperature profiles, thereby necessitating superior heater designs and materials. Environmental concerns are also influencing product design, pushing manufacturers towards developing energy-efficient heaters that reduce power consumption during operation while maintaining strict process tolerances.

The Semiconductor Heaters Market is characterized by robust expansion driven primarily by significant capital expenditure across the global semiconductor industry, particularly the intense race to achieve technological leadership in advanced node manufacturing. Business trends indicate a strong emphasis on strategic material partnerships and supply chain resilience, as manufacturers seek to secure consistent access to high-purity, specialized materials like refractory metals and advanced ceramics essential for heater construction. Key industry players are focusing on developing intelligent heating systems integrated with real-time feedback and control mechanisms to accommodate the extremely tight process windows required for sub-7nm fabrication. Segment trends show substantial growth in advanced ceramic heaters (such as those based on AlN and SiC) due to their superior thermal conductivity and chemical resistance, positioning them as critical components replacing traditional metallic or quartz-based elements in demanding applications like plasma etching and high-temperature annealing. The increasing complexity of 3D integration technologies, including hybrid bonding and stacked die packaging, further necessitates specialized, localized heating solutions designed for extremely fast and localized thermal treatments.

Regionally, Asia Pacific (APAC) continues to dominate the market share, fueled by the presence of major semiconductor manufacturers in countries like South Korea, Taiwan, China, and Japan, which are aggressively expanding their production capacities for memory chips, logic chips, and advanced packaging solutions. While APAC remains the primary demand driver due to its established manufacturing ecosystem, North America and Europe are exhibiting accelerating growth, largely spurred by substantial government incentives (like the US CHIPS Act and the EU Chips Act) aimed at incentivizing the construction of new mega-fabs within these regions. This shift is creating localized demand for sophisticated equipment, including specialized thermal subsystems. Furthermore, the market is experiencing a competitive dynamic focused on intellectual property related to heater lifetime extension and material purity. Manufacturers that can demonstrate prolonged durability and minimal contamination risk are gaining significant competitive advantages, particularly as the cost of process interruption and component replacement in modern fabs is extremely high.

In summary, the market outlook is overwhelmingly positive, tied intrinsically to the cyclical yet fundamentally upward trajectory of global chip demand. The convergence of macro trends—digital transformation, the build-out of 5G infrastructure, exponential growth in data centers, and the rapid electrification of the automotive industry—ensures sustained investment in advanced fabrication techniques, which in turn solidifies the necessity for high-performance thermal control systems. Successful market navigation requires companies to prioritize innovation in material science, focus on integration capabilities with existing process tools, and establish strong localized support services to address the high-stakes, time-sensitive environment of semiconductor fabrication.

Common user questions regarding AI’s impact on the Semiconductor Heaters Market typically revolve around optimizing complex thermal recipes, predicting component failure, and maximizing energy efficiency in thermal processes. Users are keenly interested in how Artificial Intelligence and Machine Learning (AI/ML) algorithms can move beyond standard PID control to achieve highly dynamic and localized temperature uniformity in real-time, especially when dealing with increasingly heterogeneous wafer materials and complex stacked structures. Furthermore, there is significant inquiry into using AI for predictive maintenance—calculating the remaining useful life (RUL) of expensive heater components based on operational data (e.g., current load, thermal cycling history, drift rates) to schedule replacement proactively, thereby minimizing costly unplanned downtime. The underlying expectation is that AI integration will transform heaters from passive components into intelligent thermal subsystems that adapt dynamically to process variations and material characteristics, ultimately boosting overall equipment effectiveness (OEE) and significantly increasing yield consistency across large batches of wafers.

The market trajectory is significantly influenced by a balanced combination of Drivers (D), Restraints (R), Opportunities (O), and potent Impact Forces. Key drivers include the massive global investment in advanced fabrication capabilities, particularly the construction of high-volume manufacturing (HVM) fabs focusing on 300mm wafers and below-7nm technology nodes, which necessitate highly specialized and durable thermal subsystems. The continuous growth in complex device architectures, such as advanced memory technologies (e.g., High Bandwidth Memory, 3D NAND) and sophisticated logic devices (e.g., FinFET successors), requires thermal processing at extremely high temperatures and with unprecedented uniformity, pushing the limits of current heater materials and design, thus fueling replacement and upgrade cycles. Simultaneously, the restraints revolve primarily around the extremely high purity requirements and the finite lifespan of specialized heater components. Contamination released by the heater material itself—especially at high operating temperatures—can severely impact wafer yield, necessitating the use of extremely expensive, high-purity materials (like high-purity quartz or advanced ceramics), which significantly increases initial capital expenditure and replacement costs for fabs. Furthermore, supply chain complexity for these niche, high-performance materials poses a periodic risk.

Opportunities for growth are concentrated in emerging applications and geographical expansion. The proliferation of electric vehicles (EVs) and 5G/6G infrastructure is driving massive demand for power semiconductors (based on SiC and GaN), which require specialized high-temperature processing tools and subsequently, tailored heating solutions capable of operating reliably above 1,500°C. Furthermore, expansion into new fabrication regions, specifically the establishment of domestic supply chains in North America and Europe, presents significant opportunity for localized sales and service provision for complex thermal components. The major impact forces shaping the market include strict regulatory demands concerning energy consumption and the geopolitical competition surrounding semiconductor manufacturing leadership. Geopolitical shifts incentivize rapid domestic capacity expansion, directly translating into increased procurement of new fabrication equipment, including high-end heater systems. The rapid evolution of heating element technology, moving towards dynamic, digitally controlled systems, represents another critical impact force that differentiates leading market players and accelerates technology obsolescence among legacy heating solutions.

In essence, while the market benefits from the fundamental and irreplaceable role heaters play in chip manufacturing, scaling challenges, especially maintaining uniformity over 300mm wafers at advanced nodes, present continuous technological hurdles. The necessity for zero-contamination, ultra-uniform heating across various corrosive and high-vacuum processes ensures that only a limited number of specialized manufacturers can meet these stringent specifications, contributing to the high-value nature of the components. Addressing these challenges through innovative materials science and smart integration with process control systems will be key determinants of future market leadership.

The Semiconductor Heaters Market segmentation provides a granular view of demand across various product types, applications, and regional consumption patterns, reflecting the specialized requirements of modern semiconductor fabrication. The market is primarily segmented based on the type of heating element material utilized, such as ceramic, quartz, metallic, and others, with ceramic and quartz heaters dominating due to their high thermal stability, purity, and resistance to chemical environments common in deposition and etching chambers. Segmentation by application highlights the dominant role played by deposition processes (CVD, PVD, ALD), followed by etching, rapid thermal processing (RTP), and diffusion/oxidation steps, each requiring distinct heater characteristics concerning temperature range, ramp rate, and structural profile. Analyzing these segments is crucial for understanding technological focus areas and identifying lucrative niches, such as the growing demand for SiC-based heaters capable of handling extremely high-temperature annealing required for wide-bandgap semiconductors used in power electronics.

The value chain for the Semiconductor Heaters Market is highly specialized and spans from the sourcing of ultra-high-purity raw materials to the final integration of the thermal subsystem into complex fabrication tools. Upstream activities are dominated by niche suppliers of advanced ceramics (AlN, SiC powders), refractory metals, and high-purity quartz. These materials require rigorous purification processes to meet the stringent contamination standards of the semiconductor industry, making this stage a critical bottleneck and a significant cost driver. Midstream manufacturing involves precision machining, deposition of heating tracks (e.g., Molybdenum Silicide), hermetic sealing, and integration of complex sensor arrays (thermocouples) within the heater structure, often requiring proprietary techniques to achieve the necessary temperature uniformity and longevity. Expertise in thin-film technology and materials science is paramount at this stage, as the heater’s performance directly impacts the wafer yield.

Downstream distribution is heavily reliant on close partnerships between heater manufacturers and Original Equipment Manufacturers (OEMs) of semiconductor processing equipment (e.g., ASML, Applied Materials, Lam Research, KLA). These OEMs integrate the custom-designed heaters into their deposition or etching chambers, making them the primary direct customers. Indirect distribution channels primarily involve servicing and spare part replacements for existing fabs, often handled by specialized service providers or directly by the heater manufacturer to ensure proper installation and calibration. The complexity of the components and the critical nature of their function necessitate a strong direct support model. Optimization of this value chain focuses on minimizing material impurities, accelerating component qualification cycles with OEMs, and enhancing aftermarket service responsiveness to maintain high uptime in fabs globally.

The value capture tends to be highest at the midstream (manufacturing of the finished component, due to intellectual property in design and processing) and the downstream service provision (due to the high cost of replacement and maintenance services). Manufacturers are increasingly seeking vertical integration or long-term exclusive supply agreements with OEMs to stabilize demand and streamline the qualification process, acknowledging that the heater is a mission-critical, highly customized part of the multi-million dollar fabrication tool.

Potential customers for semiconductor heaters are concentrated overwhelmingly within the core semiconductor manufacturing ecosystem, spanning from the companies that build the fabrication tools to those that operate the high-volume manufacturing lines. The most crucial customer segment consists of Original Equipment Manufacturers (OEMs), who design and assemble the sophisticated processing chambers (CVD, PVD, Etch systems) into which these highly customized heaters are integrated. These OEMs, such as Applied Materials, Lam Research, Tokyo Electron (TEL), and Hitachi High-Tech, require heaters to meet precise mechanical and thermal specifications tailored to their specific tool designs and process recipes, making them the largest initial purchasers of new heating technology.

The second major group includes Integrated Device Manufacturers (IDMs) and Foundries, such as TSMC, Samsung, Intel, Micron, and SK Hynix. While these entities primarily purchase processing tools from OEMs, they also constitute the major end-users who drive the demand for replacement heaters, consumables, and upgrade components throughout the operational life of their fabrication facilities. The high cost of unplanned downtime means these fabs require rapid and reliable sourcing of replacement heaters that maintain strict performance specifications. Finally, emerging customers include specialized manufacturers focusing on power electronics (SiC/GaN devices), advanced packaging, and microelectromechanical systems (MEMS), all of which require thermal processing capabilities but often utilize specialized, lower-volume tools requiring tailored heating solutions.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 850 Million |

| Market Forecast in 2033 | USD 1,400 Million |

| Growth Rate | 7.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Watlow, L&L Kiln & Furnace, MHI Group, M.R. Heaters, ZIRCAR Ceramics, Sumitomo Electric, CoorsTek, Kyocera, TDK Corporation, Calsonic Kansei Corporation, Thermal Technology, Inc., Okazaki Manufacturing, Backer Hotwatt, Tutco-Farnam, Sanwa Electric, Kanthal, Durex Industries, Tempco Electric Heater Corporation, Honeywell International, Chromalox. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Semiconductor Heaters Market is defined by the critical need for ultra-high purity materials, precise temperature control, and enhanced component longevity, particularly as processing temperatures escalate and dimensional tolerances shrink. The primary technological focus involves the evolution of heating element materials. Advanced ceramic heaters, particularly those utilizing Aluminum Nitride (AlN) and Silicon Carbide (SiC), represent a significant advancement. AlN offers superior thermal conductivity, enabling rapid thermal cycling necessary for advanced deposition techniques like ALD, while SiC is favored for its exceptional mechanical strength and chemical inertness at temperatures exceeding 1,200°C, making it essential for processing WBG power semiconductors. These ceramic technologies often incorporate embedded heating elements, where the resistive trace is sealed within the ceramic body, providing high structural integrity and minimizing particulate contamination risk compared to external metallic elements.

Another crucial area of innovation is the development of dynamic and localized temperature control systems. Modern fabrication requires not just uniform temperature but the ability to create precise thermal gradients or localized hot spots across the wafer to facilitate heterogeneous integration and advanced packaging processes. This is achieved through sophisticated multi-zone heating plates, which divide the heater surface into numerous individually controlled zones, managed by complex digital power supplies and highly accurate fiber optic temperature sensors. Furthermore, the integration of real-time monitoring and advanced feedback loops (often utilizing predictive control algorithms or AI) is becoming standard, ensuring that instantaneous thermal corrections can be made to compensate for process variations, thus drastically improving within-wafer and wafer-to-wafer repeatability. This shift from simple resistive heating to intelligent thermal systems is a key differentiator in the market.

Material science continues to push boundaries with the introduction of new refractory metals and alloys designed for extreme environments, especially those involving plasma etching or corrosive chemical precursors. For quartz-based heaters used in radiant thermal processing (RTP), technological progress focuses on improving lamp efficiency, spectral control, and longevity under rapid thermal cycling stress. Overall, the technological trajectory is moving toward highly integrated thermal components that function as smart subsystems—combining the heating element, advanced insulation, high-speed temperature sensing, and robust digital control interfaces into a single, high-performance unit optimized for the harsh, vacuum, and chemically aggressive environments characteristic of modern semiconductor manufacturing tools.

Semiconductor heaters are essential thermal management components that provide extremely precise and uniform temperature control for wafer processing steps such as deposition (CVD/ALD), etching, and annealing. Maintaining thermal uniformity across the wafer is critical for defect prevention, ensuring consistent film thickness, and activating dopants, thereby directly impacting the final yield and performance of advanced logic and memory chips.

Silicon Carbide (SiC) and Aluminum Nitride (AlN) are increasingly preferred due to their superior properties compared to traditional materials. AlN offers high thermal conductivity for rapid heating and cooling cycles, while SiC provides exceptional chemical inertness and mechanical stability at the ultra-high temperatures (often exceeding 1,200°C) required for processing wide-bandgap (WBG) semiconductors like SiC and GaN, and for advanced plasma processes.

The transition to 300mm (12-inch) wafers significantly increases the surface area over which temperature uniformity must be maintained, compounding the technical difficulty. This necessitates highly complex multi-zone heating systems, often integrated with advanced process control software, to ensure temperature variation remains within fractions of a degree across the entire large surface, driving demand for technologically superior, customized heaters.

The primary constraint is the stringent requirement for ultra-high purity and zero particulate contamination. High operating temperatures, combined with corrosive process gases, cause degradation and release contaminants from the heater material. This limits the lifespan of the component, necessitates the use of expensive, high-purity materials, and results in high replacement costs and critical scheduled maintenance for high-volume manufacturing facilities.

The deposition processes segment, specifically Chemical Vapor Deposition (CVD) and Atomic Layer Deposition (ALD), drives the highest demand. These processes rely heavily on precise, repeatable thermal cycles to control film growth at the atomic scale. As device complexity increases (e.g., 3D NAND and FinFETs), the number of deposition steps multiplies, requiring a corresponding increase in the use of high-performance thermal elements.

Geopolitical tensions and the desire for national supply chain resilience (e.g., US CHIPS Act, EU Chips Act) are accelerating the construction of new fabrication plants in North America and Europe. This shift generates immediate, localized demand for new equipment, including advanced heaters. While APAC manufacturers still dominate production, new regional fabs are diversifying the demand base and fostering localized supply networks for critical components like specialized heaters.

Embedded heating elements are resistive traces (often refractory metals or specialized pastes) sealed within a monolithic, high-purity ceramic body, typically AlN or Alumina. Their primary benefit is superior cleanliness and mechanical protection; the sealed design prevents the heating trace from releasing particulates or reacting directly with corrosive process gases, thereby minimizing wafer contamination and extending component lifetime in harsh environments.

AI is utilized to implement predictive maintenance by analyzing operational sensor data to forecast potential heater failure, thus preventing unplanned downtime. Additionally, AI algorithms are deployed for advanced thermal recipe optimization, enabling real-time, dynamic adjustments to maintain perfect thermal profiles under fluctuating process conditions, far surpassing the capabilities of conventional PID controllers.

Processing Gallium Nitride (GaN) requires extremely high temperatures, often exceeding 1,400°C, and involves highly reactive precursors. Heaters used in these applications must demonstrate extraordinary thermal stability, resistance to harsh chemical erosion, and maintain structural integrity under prolonged ultra-high temperature exposure, leading to increased adoption of SiC and specialized Molybdenum-based heating systems.

Thermocouple technologies are critical for accurate feedback and control. Modern semiconductor processes rely heavily on highly responsive, low-drift temperature sensors, often specialized fiber optic probes or high-stability noble metal thermocouples, integrated directly into the heater assembly. Their accuracy is essential for achieving the required temperature repeatability and for enabling advanced multi-zone control systems.

Original Equipment Manufacturers (OEMs) primarily drive the initial demand for new heater designs and high-volume procurement as they integrate them into new tool platforms. Foundries (the chipmakers) drive replacement and aftermarket demand; their focus is on long-term reliability, low total cost of ownership (TCO), and rapid availability of spare parts to ensure continuous production with minimal downtime.

RTP is a process used for annealing, oxidation, and silicidation, characterized by extremely short process times and rapid thermal ramp-up and cool-down rates. RTP typically utilizes high-intensity radiant heaters, such as quartz halogen lamps or specialized resistive elements, designed for high power density and spectral matching to ensure quick, uniform energy transfer to the wafer, minimizing thermal budget exposure.

Energy consumption regulations push manufacturers to innovate toward more energy-efficient designs. This includes developing heaters with superior thermal insulation (reducing wasted heat), implementing AI-driven optimization to minimize power draw during idle periods, and improving the efficiency of resistive materials to reduce required input power while maintaining high thermal output and fast response times.

The "More than Moore" trend involves integrating different functions onto a chip (e.g., sensors, power) and advancing packaging technologies (e.g., 3D stacking). This requires specialized, non-uniform, localized heating solutions for processes like hybrid bonding and localized annealing, creating new, high-value market niches for customizable, high-precision thermal tools.

Quartz heaters are used primarily in radiant heating applications (RTP) and some wet processes. The purity of the quartz is paramount because any trace impurities, especially metallic contaminants, can leach out or vaporize at high temperatures and deposit onto the wafer surface, causing severe defects and contamination, particularly detrimental in sub-7nm fabrication environments.

Competitive intensity is high but segmented. It manifests primarily through technological superiority (achieving higher uniformity and durability), securing long-term qualification agreements with major OEMs, and protecting intellectual property related to advanced materials and embedded heating technologies. Pricing is less flexible due to the criticality and complexity of the components.

Many semiconductor processes occur under high vacuum. Heaters must be designed to minimize outgassing—the release of gases absorbed or trapped in the material—which could contaminate the vacuum chamber. This requires extremely high-purity, often fully dense materials and specialized manufacturing processes to ensure the heater component remains vacuum-compatible and non-contaminating during operation.

3D NAND flash memory relies on stacking many layers, requiring deep, high aspect ratio etching and numerous high-temperature deposition steps. This increases the total thermal budget exposure and necessitates heaters that can handle prolonged, high-temperature operations with perfect repeatability, pushing demand towards highly durable ceramic (SiC) and specialized metallic heating platforms.

Traditional single-zone heaters apply uniform power across the surface, leading to inherent temperature drop-offs at the edges (edge effects). Multi-zone heaters divide the surface into multiple independent heating circuits, allowing power to be adjusted differentially (e.g., boosting edge power) to achieve active thermal gradient control and maintain superior temperature uniformity across the entire wafer, essential for large 300mm substrates.

Significant opportunities lie in non-silicon processing, particularly in the manufacturing of microelectromechanical systems (MEMS), advanced sensors, photonics components, and emerging materials like 2D transition metal dichalcogenides. These fields often require highly specialized, lower-volume, customized thermal tools with unique and often extremely localized heating requirements.

The primary resistive materials sealed within advanced ceramic heaters often include refractory metals like Molybdenum or Tungsten, or specialized compounds such as Molybdenum Silicide (MoSi2). MoSi2 is favored for its excellent oxidation resistance at high temperatures and compatibility with the embedding ceramic matrix, offering a balance of performance and longevity.

TCO is a critical factor, often outweighing the initial purchase price. High-performance heaters, despite their cost, are chosen based on expected lifespan, energy efficiency, yield consistency (reduced scrap), and predictability of failure. A longer-lasting, more reliable heater minimizes expensive unplanned downtime and high replacement labor costs, offering a lower TCO over the equipment's lifespan.

Plasma etching involves highly reactive chemical plasmas that are extremely corrosive. Heaters used in these environments must be highly resistant to plasma erosion and chemical attack. Silicon Carbide (SiC) heaters are highly valued here due to their robustness, minimizing material sputtering and contamination risk, thereby preventing performance degradation.

Leading companies utilize rigorous quality control processes including non-destructive testing, advanced metrology systems (such as high-resolution thermal mapping), statistical process control (SPC), and strict material certification procedures. Every component is meticulously qualified to ensure its thermal profile matches design specifications precisely before integration into the fabrication tool, guaranteeing process repeatability for end-users.

The "thermal budget" refers to the total amount of heat exposure a wafer can tolerate during all fabrication steps without damaging sensitive structures or electrical properties. Advanced heaters help manage the thermal budget by offering extremely fast ramp-up and cool-down rates (high thermal responsiveness) and localized heating capabilities, minimizing the time the wafer spends at high temperatures.

Yes. Environmental trends are driving the adoption of energy-efficient heater designs, including better insulation materials (to reduce radiant heat loss), improved power supply systems for precise modulation, and the use of optimized materials that minimize power requirements while achieving necessary processing temperatures. Focus is also placed on minimizing hazardous materials in the component manufacturing phase.

In ultra-high vacuum (UHV) applications, standard electrical feedthroughs cannot be used due to potential leaks and outgassing. Specialized hermetic feedthroughs, often utilizing ceramic-to-metal bonding or glass-to-metal seals, are required to maintain the vacuum integrity of the chamber while delivering the high electrical power necessary for the heating element.

The transition to 450mm wafers has been significantly delayed due to substantial cost and technical complexities. While 300mm remains the standard, if 450mm adoption proceeds, it would require monumental leaps in heater technology, as maintaining uniformity over an even larger area presents unprecedented thermal engineering challenges, creating a massive, though currently dormant, opportunity for innovation.

The Asia Pacific region, specifically Taiwan, South Korea, and China, holds the most active demand for replacement and maintenance services. This is due to the highest concentration of mature, high-volume fabrication facilities globally, leading to frequent component wear and tear, and a corresponding high demand for reliable, specialized aftermarket support and spare parts inventory management.

A specific challenge with Aluminum Nitride (AlN) heaters is the difficulty in achieving high-quality, large-area bonding between the ceramic material and the high-power resistive element. Manufacturing processes must ensure zero voids or defects at this interface, as these imperfections can lead to localized hotspots, premature failure, and reduced thermal uniformity across the wafer surface during high-stress operations.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.