ID : MRU_ 432344 | Date : Dec, 2025 | Pages : 248 | Region : Global | Publisher : MRU

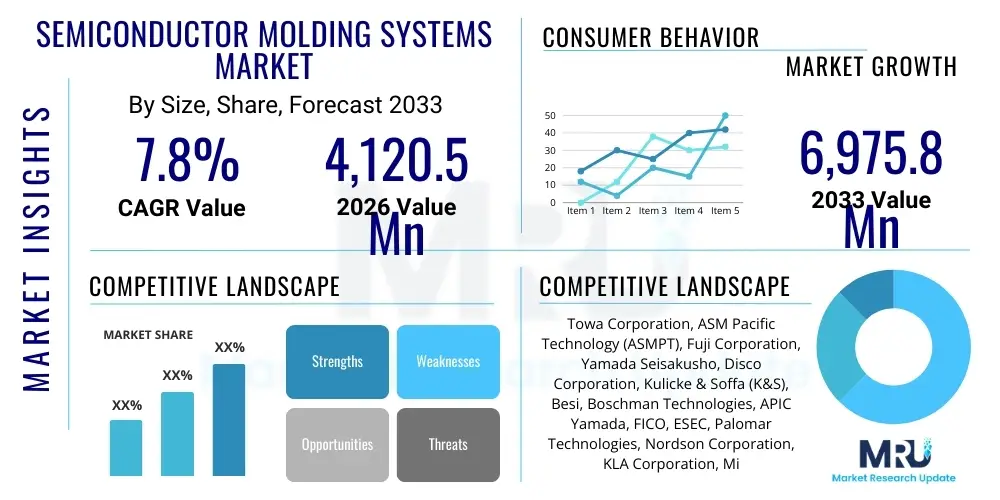

The Semiconductor Molding Systems Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2026 and 2033. The market is estimated at USD 4,120.5 Million in 2026 and is projected to reach USD 6,975.8 Million by the end of the forecast period in 2033. This robust growth trajectory is fundamentally driven by the escalating demand for advanced packaging technologies, particularly in high-performance computing (HPC), automotive electronics, and consumer devices requiring smaller, faster, and more reliable integrated circuits (ICs). The molding process, essential for protecting sensitive semiconductor components from environmental factors and mechanical damage, is undergoing significant technological evolution to support denser and three-dimensional (3D) packaging structures.

The Semiconductor Molding Systems Market encompasses specialized equipment used in the back-end manufacturing process of semiconductors to encapsulate integrated circuits (ICs) and other microelectronic devices. This encapsulation, typically achieved using epoxy molding compounds (EMCs), provides mechanical protection, heat dissipation, and isolation from moisture and contaminants, thereby significantly extending the lifespan and reliability of the final electronic product. Molding systems range from conventional transfer molding machines to highly advanced compression molding and vacuum molding systems utilized for complex package types such as wafer-level packages (WLPs), system-in-package (SiP), and fan-out wafer-level packaging (FO-WLP). These machines must deliver precision, speed, and consistency to meet the stringent quality requirements of modern microelectronics.

The primary product description of these systems includes automated molding equipment (AME), which integrates loading, pre-heating, molding, curing, and de-flashing stages into a high-throughput manufacturing line. Key applications span across the entire electronics spectrum, notably in computing (servers, data centers), communications (5G infrastructure, smartphones), industrial automation, and the rapidly expanding electric vehicle (EV) and autonomous driving sectors. The essential benefit derived from utilizing sophisticated molding systems is the enhanced thermal management capabilities and superior package reliability, which are critical as chip power density increases and package sizes continue to shrink. Furthermore, these systems are vital in ensuring compliance with industry standards for miniaturization and performance optimization across diverse semiconductor applications.

Major driving factors propelling this market include the global surge in semiconductor capital expenditure, particularly in Asia Pacific, driven by government incentives and localized supply chain strengthening. The continuous innovation in advanced packaging techniques, necessitated by Moore’s Law limitations and the push toward heterogenous integration, mandates the adoption of next-generation molding solutions capable of handling thin wafers and high-precision stacking. The increasing prevalence of complex packages, such as 2.5D and 3D packages (e.g., High Bandwidth Memory – HBM), requires molding equipment that can operate under vacuum conditions and exert extremely precise pressure control, ensuring void-free encapsulation and minimized warpage, further solidifying the necessity for advanced molding systems across the semiconductor ecosystem.

The Semiconductor Molding Systems Market is currently characterized by intense innovation focused on addressing challenges associated with miniaturization and advanced packaging. Business trends indicate a strong pivot towards automated and highly modular equipment designed for high-mix, low-volume manufacturing environments, alongside specialized systems tailored for wafer-level packaging (WLP) and panel-level packaging (PLP). Key industry stakeholders are prioritizing R&D investments in compression molding and vacuum-assisted molding technologies to minimize defects and improve the structural integrity of advanced packages. Furthermore, there is a growing consolidation among equipment providers seeking to offer integrated solutions that span the entire back-end workflow, from die attach to final molding and trimming, streamlining the supply chain for outsourced semiconductor assembly and test (OSAT) firms and integrated device manufacturers (IDMs).

Regional trends unequivocally highlight Asia Pacific (APAC) as the dominant and fastest-growing market hub, primarily fueled by massive expansion in fabrication capacity across China, Taiwan, South Korea, and Southeast Asia. Government-led initiatives in these regions, aimed at achieving semiconductor self-sufficiency, have spurred significant investment in back-end infrastructure, directly boosting the demand for advanced molding equipment. North America and Europe, while smaller in manufacturing volume, maintain strong demand for highly specialized, niche molding systems used in critical sectors like defense, aerospace, and high-reliability automotive components, emphasizing performance and compliance over sheer volume. The competitive landscape in APAC, however, necessitates equipment suppliers to maintain cost-effectiveness while adhering to rapidly evolving technological specifications.

In terms of segment trends, the Compression Molding segment is witnessing rapid adoption due to its superior capabilities in handling thinner substrates and achieving high planarity, critical for advanced packaging structures like FOWLP (Fan-Out Wafer Level Packaging). By application, the memory and logic segments remain major consumers, driven by the proliferation of artificial intelligence (AI) and high-performance computing (HPC) technologies, which demand high-density interconnection and robust thermal protection. The segment dedicated to Automotive Electronics is projected to exhibit the highest CAGR, reflective of the increased deployment of advanced driver-assistance systems (ADAS), infotainment, and power management ICs requiring certified high-reliability molding processes. This structural shift towards reliability and miniaturization mandates continuous innovation across all equipment types and material formulations used in the molding process.

Common user inquiries regarding AI’s impact on Semiconductor Molding Systems typically center on achieving zero-defect manufacturing, optimizing cycle times, and predicting equipment failure. Users are concerned with how machine learning algorithms can enhance process control parameters—such as pressure profiles, temperature uniformity, and cure times—to drastically reduce yield losses, particularly when molding complex, high-value packages like HBM stacks or FOWLP. There is significant expectation that AI integration will shift the market towards predictive maintenance (PdM) rather than reactive or preventative approaches, minimizing costly downtime. Additionally, users inquire about AI’s role in material science, specifically in optimizing the mixing and dispensing of epoxy molding compounds (EMCs) to ensure optimal viscosity and flow characteristics, thereby addressing challenges related to void formation and wire sweep, which are persistent quality issues in the molding process.

AI is fundamentally transforming the operations and maintenance of Semiconductor Molding Systems by introducing sophisticated predictive analytics and real-time process optimization capabilities. Advanced machine learning models are deployed to analyze vast datasets collected from various sensors monitoring temperature, pressure, flow rates, and vibration within the molding machinery. This data integration allows systems to identify subtle deviations indicative of potential flaws in the encapsulated product or imminent mechanical failures in the equipment. By applying AI, manufacturers can move beyond statistical process control (SPC) to true adaptive process control (APC), where molding parameters are dynamically adjusted during the encapsulation process based on the input condition of the component being molded, ensuring consistently high yield rates even with varied input materials and ambient conditions.

Furthermore, the integration of AI-powered vision systems is revolutionizing quality assurance in post-molding inspection. These sophisticated systems utilize deep learning algorithms to detect minute surface defects, incomplete encapsulation, or dimensional inaccuracies far more reliably and rapidly than traditional human inspection or simpler machine vision techniques. This capability is crucial for high-reliability applications, such as medical implants or automotive safety components, where failure is unacceptable. The implementation of AI not only boosts operational efficiency by reducing manual intervention and increasing throughput but also drives demand for next-generation molding systems equipped with the necessary computational hardware and data infrastructure to support complex AI model execution at the edge, thereby shaping the future procurement strategies of major OSAT and IDM players globally.

The Semiconductor Molding Systems Market is driven by the relentless progression of advanced packaging technologies, restrained by high capital costs and technological complexity, and presented with opportunities in emerging markets and specialized material integration. The primary driving force is the global demand for high-performance and miniaturized electronic devices, requiring superior protection for complex integrated circuits (ICs) like 2.5D/3D stacks and high-density memory modules. Restraints include the extremely high initial investment required for sophisticated molding equipment and the technical challenges associated with handling thin, fragile wafers and ensuring precise alignment during compression molding, which demands high operational expertise and specialized infrastructure. The collective impact forces show that drivers, particularly technological mandates from leading chip designers, currently outweigh the restraining factors, leading to sustained market expansion.

Key drivers include the massive global build-out of 5G infrastructure, requiring high-reliability power amplifiers and RF modules, all necessitating precise molding solutions. Simultaneously, the automotive sector's shift towards electrification and autonomous driving systems mandates the use of highly robust, thermally efficient, and environmentally resistant encapsulated components, driving demand for specialized molding compounds and the equipment to handle them effectively. The necessity to improve thermal dissipation in high-power components, coupled with the industry's focus on heterogeneous integration (combining different types of chips in one package), forces molding equipment manufacturers to innovate rapidly, offering solutions such as mold-underfill processes and systems capable of ultra-low pressure operation to prevent damage to delicate internal structures.

However, the market faces significant restraints. The complexity of integrating molding systems into fully automated back-end lines, coupled with the need for specialized vacuum and material handling systems, imposes significant barriers to entry for new players and requires continuous high-level training for technicians. Furthermore, the inherent variability in molding compounds and their interaction with different package substrates necessitates intensive testing and calibration, leading to longer development cycles for new package types. Opportunities abound in the development of equipment tailored for panel-level packaging (PLP), which offers cost efficiencies over traditional wafer-level processing, and in the integration of specialized systems for highly abrasive or thermally conductive molding compounds crucial for power electronics, providing avenues for market diversification and specialization for key vendors.

The Semiconductor Molding Systems Market is extensively segmented based on the type of molding technology utilized, the level of automation, the substrate material being processed, and the specific application segment it serves. Technological segmentation is crucial as it dictates the package types that can be effectively processed; transfer molding remains dominant for conventional packages, while compression molding and vacuum molding are essential for high-end, advanced packaging structures requiring exceptional precision and minimal stress. Segmentation by automation level distinguishes between fully automatic, semi-automatic, and manual systems, reflecting the scale and maturity of the manufacturing facility, with the trend overwhelmingly favoring fully automated, high-throughput systems to reduce human error and maximize efficiency in mass production environments, especially within the OSAT sector.

Further segmentation by substrate type includes wafer molding and non-wafer molding (e.g., lead frames, substrates, and strip molding). Wafer molding, crucial for WLP and FOWLP technologies, represents the fastest-growing segment due to the increasing adoption of chips that are molded before being diced. Application segmentation provides insights into end-user spending priorities, categorized into Memory, Logic, MEMS/Sensors, and Power Devices, with Logic and Memory historically constituting the largest revenue share due to the sheer volume of production driven by data centers and consumer electronics. Understanding these segment dynamics is vital for equipment manufacturers to tailor their product offerings, whether focusing on high-volume, cost-effective solutions for standard packages or highly specialized, precision equipment for next-generation interconnect architectures.

The strategic segmentation helps market players identify niche areas of growth, such as the rapid need for specialized molding equipment for gallium nitride (GaN) and silicon carbide (SiC) power devices, which require unique thermal management and high-temperature tolerance during the molding process. Similarly, the MEMS and Sensor segment demands ultra-low-stress molding to avoid any shift or deformation that could compromise sensor calibration or performance. The continuous technological overlap between these segments, driven by system-in-package (SiP) trends, necessitates molding systems that offer flexibility and rapid retooling capabilities, ensuring that equipment investment remains viable across multiple product generations and packaging formats, sustaining the demand for versatile and sophisticated machinery.

The value chain for the Semiconductor Molding Systems Market begins with upstream raw material suppliers, predominantly focusing on high-grade specialty metals, precision machinery components (e.g., hydraulics, robotics), and sophisticated control electronics necessary for building high-precision molding equipment. The crucial upstream element is the development and supply of high-performance epoxy molding compounds (EMCs) and mold release agents, provided by chemical companies, which dictates the thermal and mechanical characteristics of the final packaged chip. The equipment manufacturers (OEMs) then design, assemble, and integrate these components, adding proprietary software and advanced automation features to create the final molding systems. Efficiency and quality control in this upstream phase are paramount, as the precision of the system directly impacts the yield rate of highly sensitive semiconductor packages, necessitating close collaboration between equipment providers and raw material vendors to ensure material compatibility and process stability.

Midstream activities involve the equipment manufacturing and system integration phase, where R&D focusing on speed, throughput, and process control (e.g., vacuum effectiveness, pressure uniformity) is concentrated. Major equipment suppliers compete intensely based on technological differentiation, especially concerning compression molding capabilities required for wafer-level processing. The distribution channel is predominantly direct, especially for high-value, complex systems, where sales often involve long consultative processes, factory acceptance testing (FAT), and continuous after-sales service and maintenance contracts. Indirect distribution might involve local agents or distributors in smaller emerging markets, primarily handling lower-volume or older generation semi-automatic equipment, but the overwhelming trend for advanced systems is direct sales due to the necessity of specialized installation and training provided by the OEM.

The downstream sector is dominated by the end-users: primarily large Outsourced Semiconductor Assembly and Test (OSAT) providers like ASE, Amkor, and SPIL, and major Integrated Device Manufacturers (IDMs) like Intel and Samsung, who utilize the molding systems for mass production. These downstream entities rely heavily on the performance and reliability of the molding equipment to achieve competitive cost structures and meet stringent client specifications regarding package integrity and thermal performance. The continuous feedback loop from downstream users concerning defects, warpage issues, and throughput requirements drives the next generation of technological innovation upstream. Therefore, successful market navigation requires OEMs to maintain deep, collaborative relationships across the entire value chain, from compound suppliers to large-scale OSATs, ensuring system compatibility with evolving packaging demands and material science breakthroughs.

Potential customers for Semiconductor Molding Systems primarily comprise entities involved in the back-end processing phase of semiconductor manufacturing, crucially needing advanced encapsulation solutions to protect their integrated circuits. The largest customer segment consists of Outsourced Semiconductor Assembly and Test (OSAT) providers, who handle the assembly, testing, and packaging of chips designed by fabless companies. These OSATs operate globally on high-volume, high-mix models, requiring molding equipment that offers maximum throughput, flexibility, and robust automation features to manage diverse package types efficiently. Their purchasing decisions are heavily influenced by the system's Mean Time Between Failures (MTBF), total cost of ownership (TCO), and its demonstrated capability to handle the latest advanced packaging formats, such as FOWLP and SiP, driving demand for specialized, highly reliable vacuum compression molding machines.

Integrated Device Manufacturers (IDMs), such as major memory and logic producers who perform both front-end fabrication and back-end assembly in-house, constitute the second major customer base. While IDMs may produce fewer packages overall compared to large OSATs, their demand often focuses on proprietary or highly specialized molding systems tailored for unique internal packaging requirements, particularly for high-value components like next-generation processors or high-density memory modules (e.g., HBM). These customers prioritize equipment that offers unparalleled precision and seamless integration into highly sensitive, complex manufacturing workflows, often driving customization requests for molding systems that incorporate features optimized for extreme environmental control and specific material handling protocols not readily available in commercial off-the-shelf equipment.

A burgeoning segment of potential customers includes specialized electronics manufacturers focusing on niche, high-reliability applications, notably automotive component suppliers (Tier 1 suppliers) and aerospace/defense contractors. These clients require molding systems that meet extremely rigorous quality and traceability standards (e.g., AEC-Q100, ISO standards). Although their volume requirements are lower, their demand for failure-proof encapsulation drives premium pricing and specialized technological requirements, particularly for molding systems designed for power modules (SiC/GaN) where thermal management and void control are critically important. Furthermore, research institutes and university cleanrooms also represent smaller, niche customers, often seeking highly flexible, lower-volume, and research-grade systems to develop and test experimental packaging methodologies and new material combinations.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4,120.5 Million |

| Market Forecast in 2033 | USD 6,975.8 Million |

| Growth Rate | 7.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Towa Corporation, ASM Pacific Technology (ASMPT), Fuji Corporation, Yamada Seisakusho, Disco Corporation, Kulicke & Soffa (K&S), Besi, Boschman Technologies, APIC Yamada, FICO, ESEC, Palomar Technologies, Nordson Corporation, KLA Corporation, Micronic, Hanmi Semiconductor, Shin-Etsu Polymer, Hitachi High-Tech. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The current technology landscape in the Semiconductor Molding Systems Market is predominantly defined by the shift from traditional transfer molding to advanced compression molding, particularly Wafer-Level Compression Molding (WLCM), which is critical for next-generation packaging geometries. Transfer molding remains the workhorse for standard, high-volume packages (like QFN and SOIC), offering high throughput and established reliability. However, compression molding systems utilize specialized vacuum chambers and precise platen control to exert uniform pressure across the entire wafer or panel. This capability minimizes material flow distance, drastically reducing the chances of wire sweep, and, critically, achieves the necessary planarity and low stress required for ultra-thin, stacked die packages (2.5D/3D integration), where minute imperfections can lead to functional failure. The advancement in compression technology directly addresses the warpage challenges inherent in Fan-Out Wafer Level Packaging (FOWLP) and other large-area, high-density interconnection structures.

A second crucial technological trend is the integration of high-vacuum encapsulation (vacuum molding). This technology is essential for ensuring void-free encapsulation when dealing with complex geometries, large substrates, or highly porous mold compounds. Vacuum molding systems effectively evacuate air and volatile gases from the mold cavity before and during compound injection, guaranteeing full material penetration and contact with all substrate features, which is especially important for high-reliability components where even microscopic voids can lead to moisture ingress and premature failure. Furthermore, the push towards increased automation and smart factory integration is driving the adoption of sophisticated control systems incorporating machine vision, IoT connectivity, and sophisticated human-machine interfaces (HMIs). These systems facilitate remote diagnostics, predictive process tuning, and seamless data exchange across the manufacturing execution system (MES), enhancing overall operational efficiency.

The future technology trajectory is pointing towards panel-level molding (PLM) solutions, which utilize rectangular substrates (panels) rather than circular wafers to maximize material utilization and potentially reduce the overall cost per package. Panel-level compression molding (PLCM) requires a complete redesign of existing equipment, demanding larger, more robust, and even more precise platen control mechanisms to ensure uniform pressure across a significantly larger area without introducing warpage or non-uniformity. Concurrently, there is continuous innovation in dispensing and compound handling technologies, including sophisticated multi-component dispensing systems that allow for simultaneous use of different molding compounds (e.g., soft materials for stress relief and hard materials for structural integrity) within a single package structure, enabling highly customized protective layers and reinforcing the market's focus on material science integration within the molding process.

The escalating requirement for advanced packaging technologies, such as Fan-Out Wafer Level Packaging (FOWLP) and 2.5D/3D die stacking, drives demand for compression molding. These advanced packages require superior planarity, ultra-low stress, and void-free encapsulation, which traditional transfer molding cannot reliably achieve for thin wafers.

The transition to electric vehicles (EVs) and autonomous driving necessitates power modules (SiC/GaN) and ADAS sensors that require certified high-reliability encapsulation. This shift demands specialized molding systems capable of handling thermally conductive materials and meeting stringent AEC-Q100 reliability standards.

Asia Pacific (APAC) dominates the market, primarily due to the vast concentration of Outsourced Semiconductor Assembly and Test (OSAT) providers and Integrated Device Manufacturers (IDMs) in countries like China, Taiwan, and South Korea, coupled with significant governmental investment in expanding back-end manufacturing capacity.

AI is utilized for implementing real-time Adaptive Process Control (APC) and Predictive Maintenance (PdM). AI algorithms analyze sensor data to dynamically optimize molding parameters and forecast equipment failures, significantly boosting yield rates and minimizing unplanned downtime for complex packages.

Panel-Level Packaging (PLP) involves processing chips on large, rectangular substrates (panels) instead of traditional round wafers, offering better material utilization and cost efficiency. This trend necessitates the development of specialized Panel-Level Compression Molding (PLCM) systems capable of handling larger surface areas with high precision and warpage control.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.