ID : MRU_ 433400 | Date : Dec, 2025 | Pages : 246 | Region : Global | Publisher : MRU

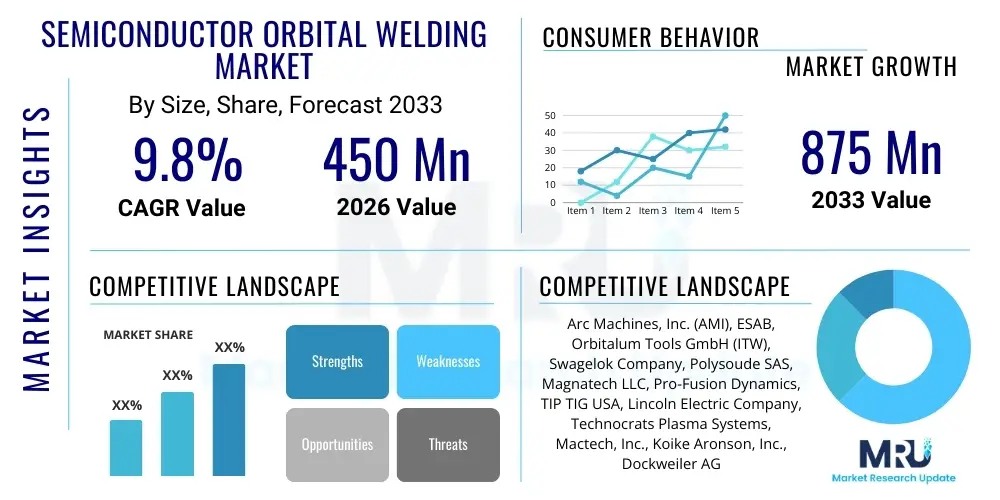

The Semiconductor Orbital Welding Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2026 and 2033. The market is estimated at $450 Million in 2026 and is projected to reach $875 Million by the end of the forecast period in 2033.

The Semiconductor Orbital Welding Market encompasses the specialized segment of precision welding technology essential for fabricating Ultra-High Purity (UHP) fluid and gas delivery systems required in modern semiconductor manufacturing facilities (fabs). Orbital welding ensures uniform, high-integrity, and defect-free welds, which are critical for maintaining the stringent purity standards necessary for preventing contamination of sensitive semiconductor processes. The integrity of these welded joints directly impacts chip yield and operational longevity, positioning this technology as indispensable for advanced fabrication nodes, particularly those handling corrosive or inert specialty gases used in etching and deposition processes.

Orbital welding products specifically tailored for semiconductor applications include automated welding heads, power supplies, and specialized purging equipment designed to operate in cleanroom environments. Key applications span the construction and maintenance of gas panels, valve manifold boxes (VMBs), process piping, and cooling systems within semiconductor manufacturing plants. The primary benefits include consistency, traceability, reduced human error compared to manual welding, and the ability to handle small diameter tubing (down to 1/8 inch) with exceptional precision, facilitating the miniaturization and complexity of modern semiconductor infrastructure.

Driving factors for this market expansion include the global surge in semiconductor capital expenditure, particularly in Asia Pacific (APAC), driven by the proliferation of 5G, AI, and IoT devices, necessitating higher capacity foundry construction. Furthermore, the transition to smaller process nodes (e.g., 3nm and 2nm) mandates ever-increasing purity levels for process gases, making highly repeatable and contaminant-free orbital welding techniques non-negotiable. Regulatory requirements concerning system uptime and safety in high-pressure gas handling environments also contribute significantly to the adoption rate of advanced orbital welding systems.

The Semiconductor Orbital Welding Market is characterized by robust growth primarily fueled by aggressive capacity expansion across major global foundry players and increasing technological requirements related to sub-5nm fabrication processes. Business trends indicate a strong focus on automation, integration with digital manufacturing platforms, and the development of compact, portable welding systems that can perform reliably in diverse cleanroom settings. Key market participants are concentrating on providing comprehensive validation and traceability packages to meet rigorous industry standards (e.g., SEMI guidelines), shifting the competitive landscape toward solution providers rather than just equipment manufacturers.

Regional trends highlight the continued dominance of the Asia Pacific (APAC) region, driven by substantial investments from Taiwan (TSMC), South Korea (Samsung), and mainland China, which account for the majority of new fab construction projects. However, strategic initiatives in North America (US CHIPS Act) and Europe (European Chips Act) are fostering significant localized growth in these regions, aiming to establish more resilient domestic supply chains. This geopolitical realignment is driving demand for highly trained orbital welding service providers and advanced, certified equipment to support new facility development outside traditional manufacturing hubs.

Segment trends underscore the criticality of power supply technology, with inverter-based, microprocessor-controlled systems dominating due to their precision and consistency. From an application perspective, piping systems for specialty gas delivery and Vacuum Ultra-High Purity (V-UHP) environments are the largest growth areas, demanding extremely precise weld bead profiles and zero-tolerance for internal oxidation. The services segment, including calibration, rental, and training, is also experiencing high growth as the specialized skill set required for operating and maintaining these complex systems remains scarce.

User inquiries regarding the integration of Artificial Intelligence (AI) in the Semiconductor Orbital Welding Market often center on its ability to enhance weld quality consistency, reduce cycle times, and minimize human dependency in critical high-purity environments. Key themes include the potential for AI-driven predictive maintenance for welding equipment, automated defect detection using machine vision integrated with welding heads, and the optimization of welding parameters (such as arc voltage, rotation speed, and pulse duration) in real-time based on material inputs and environmental factors. Users are specifically concerned about how AI can handle the inherent variability in tube tolerances and gas purge dynamics to guarantee consistent UHP standards required for 3nm and beyond fabrication nodes.

The direct application of AI is primarily focused on quality assurance and process control. By leveraging deep learning algorithms trained on thousands of orbital weld images and corresponding sensor data (current, voltage, pressure), AI systems can instantly classify weld quality, flagging microscopic flaws or inconsistencies that traditional inspection methods might miss. This proactive quality control not only increases yield rates in the fabrication of UHP systems but also provides comprehensive data logs necessary for regulatory compliance and system validation. Furthermore, AI facilitates autonomous parameter adjustment, moving beyond preset schedules to dynamically compensate for thermal shifts or subtle material changes during the welding cycle.

Beyond the welding process itself, AI contributes significantly to operational efficiency through predictive equipment lifecycle management. AI models analyze usage patterns, maintenance logs, and component stress data to accurately forecast potential equipment failures, especially concerning sensitive components like welding head motors or power supply rectification circuits. This transition from scheduled maintenance to condition-based maintenance minimizes unexpected downtime in capital-intensive semiconductor fabrication projects, a major concern for end-users seeking maximal tool utilization and construction efficiency.

The market is significantly driven by the relentless pursuit of miniaturization and density in semiconductor chips, mandating Ultra-High Purity (UHP) environments, which only orbital welding can reliably ensure. Restraints include the extremely high initial capital investment required for automated orbital welding systems and the persistent shortage of highly specialized labor trained in cleanroom UHP practices. Opportunities emerge from the growth of 3D integration technologies (like 3D NAND and wafer-level packaging) and the development of facilities for next-generation materials like Silicon Carbide (SiC) and Gallium Nitride (GaN), which require specific, high-temperature-resistant welded systems. The combined impact forces strongly favor market growth, given that welding integrity is a core prerequisite for advanced semiconductor output quality, outweighing concerns regarding high cost.

Drivers are primarily linked to technological mandates. As chip geometry shrinks, contaminants smaller than a few nanometers can destroy wafer yields. Orbital welding guarantees the required inert internal environment by performing consistent, penetration-controlled welds with minimal heat-affected zones (HAZ) and virtually no internal oxidation (sugaring), provided appropriate purge gas management is utilized. The increasing use of hazardous and corrosive specialty gases in advanced etching and deposition processes also necessitates the mechanical robustness and leak-proof nature that only high-quality orbital welds can provide, pushing fab operators toward automated solutions.

However, the market faces structural hurdles. Restraints are centered around cost and expertise. A complete, high-end orbital welding system with integrated data logging, specialized tooling, and UHP certification represents a significant capital expenditure, often prohibitive for smaller contractors or service firms. Furthermore, operating and calibrating these systems in complex cleanroom settings requires technicians who possess both advanced welding certifications and specialized semiconductor fabrication knowledge, a global talent pool that remains critically limited, necessitating high investment in specialized training and certification programs.

Opportunities are driven by emerging technologies and geopolitical shifts. The transition towards advanced packaging, including fan-out wafer-level packaging (FOWLP) and hybrid bonding, requires new, complex UHP fluid delivery systems. Geographically, the strong governmental push in North America and Europe to onshore semiconductor production creates massive greenfield opportunities for equipment sales and comprehensive service contracts, moving beyond the established dominance of Asian markets. Furthermore, the burgeoning demand for power semiconductors (SiC, GaN) in electric vehicles and renewable energy also requires new, high-specification welding capabilities.

The Semiconductor Orbital Welding Market is strategically segmented based on crucial dimensions, including product type, application, end-user, and welding method, enabling targeted analysis of growth trajectories and competitive positioning. Product segmentation highlights the dominance of advanced power sources, which incorporate features such as programmable logic controllers (PLCs) and integrated quality control software, distinguishing them from basic models. Application segmentation emphasizes the critical role of these systems in gas delivery pipelines and UHP water systems, reflecting the core purity requirements of front-end fabrication processes.

The market structure is highly specialized due to the unique purity demands of the semiconductor industry. Segmentation by welding method reveals Gas Tungsten Arc Welding (GTAW) as the predominant technology, specifically tailored for orbital applications due to its precise heat control and inert atmosphere requirements, crucial for stainless steel and high-nickel alloy piping. End-user segmentation shows that Integrated Device Manufacturers (IDMs) and pure-play foundries account for the largest share of equipment procurement, while outsourced assembly and testing (OSAT) providers are emerging as rapid growth consumers due to their expanding role in advanced packaging infrastructure.

Understanding these segments is vital for suppliers to tailor equipment specifications—for example, focusing on extremely lightweight and portable weld heads for hard-to-reach installation areas within existing fabs, or developing high-throughput, heavy-duty systems for large greenfield fab construction projects. The service segment, including long-term calibration and maintenance agreements, is gaining significance as companies prioritize system reliability over initial cost, driven by the astronomical expense associated with unexpected downtime in a high-volume manufacturing environment.

The value chain for the Semiconductor Orbital Welding Market begins with upstream suppliers providing critical raw materials, primarily high-grade stainless steel (316L, VIM/VAR) tubing and specialized fittings necessary for UHP applications, alongside electronic components for advanced power supplies. Material quality is paramount; any contamination or imperfection in the tubing feedstock directly compromises the integrity of the final welded system, necessitating extremely stringent quality checks at this initial stage. Key upstream players include specialized metal producers and electronic component manufacturers who adhere to specific cleanroom manufacturing protocols to minimize particle generation.

Midstream activities involve the core market participants: orbital welding equipment manufacturers and specialized system integrators. Equipment manufacturers design, assemble, and certify the automated welding systems (power sources, weld heads, and accessories). System integrators or dedicated UHP piping contractors take this equipment and execute the actual fabrication, installation, and certification of the gas/fluid delivery lines within the semiconductor fab. This stage requires significant intellectual capital, advanced cleanroom procedures, and strict adherence to ASME B31.3 and SEMI F77 standards for UHP piping installation.

The downstream segment involves the direct end-users—IDMs, Foundries, and EPC firms—who utilize the installed UHP systems. Distribution channels are typically a mix of direct sales for major global accounts and reliance on specialized, highly certified local distributors or agents who provide necessary localized support, calibration services, and training. Direct distribution is favored for high-value equipment and complex contracts, ensuring quality control and direct technical support. Indirect channels are crucial for consumables and smaller accessory sales, leveraging established distribution networks within regional cleanroom supply chains, often requiring specialized, authorized service providers to maintain equipment warranties and performance standards.

The primary consumers of orbital welding equipment and services are the large-scale organizations responsible for designing, building, and operating semiconductor fabrication facilities (fabs). These include Integrated Device Manufacturers (IDMs) such as Intel and Micron, and pure-play foundries like TSMC and Samsung Foundry, who undertake massive capital expenditure projects requiring thousands of feet of UHP piping infrastructure. These organizations prioritize system reliability, documented weld quality, and the ability to scale up installations rapidly, making them high-volume buyers of premium, automated orbital welding solutions.

A second major customer category includes Engineering, Procurement, and Construction (EPC) firms, and specialized Mechanical, Electrical, and Plumbing (MEP) contractors hired to manage the complex build-out of new fabs. These firms procure welding equipment, often on a rental or project basis, and employ specialized UHP welding technicians. Their purchase criteria focus on system durability, portability, and adherence to aggressive construction timelines. Since EPC firms often handle multiple projects simultaneously, they seek standardized equipment and comprehensive service agreements from equipment suppliers.

Furthermore, Original Equipment Manufacturers (OEMs) of semiconductor processing tools (e.g., deposition, etching, lithography machines) are critical potential customers. While they do not construct the entire fab, they require orbital welding for internal sub-systems, gas panels, and complex valve manifold boxes (VMBs) built into their machinery. These OEMs demand the highest precision orbital welding for components that operate under extreme conditions (high temperature, corrosive gases), placing a premium on specialized weld heads capable of handling small-diameter tubing and exotic materials, often requiring certified equipment capable of achieving SEMI F77 compliance documentation.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | $450 Million |

| Market Forecast in 2033 | $875 Million |

| Growth Rate | 9.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Arc Machines, Inc. (AMI), ESAB, Orbitalum Tools GmbH (ITW), Swagelok Company, Polysoude SAS, Magnatech LLC, Pro-Fusion Dynamics, TIP TIG USA, Lincoln Electric Company, Technocrats Plasma Systems, Mactech, Inc., Koike Aronson, Inc., Dockweiler AG, Orbital Services, Inc., Suzhou Aotai Welding Technology. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of semiconductor orbital welding is defined by precision control, data integration, and automation crucial for Ultra-High Purity (UHP) fluid handling systems. Gas Tungsten Arc Welding (GTAW or TIG) remains the foundational process due to its ability to generate high-quality, spatter-free welds in an inert environment, specifically utilizing specialized pulsing techniques (pulsed GTAW) to control heat input and weld bead profile. The key differentiation lies in the power supply technology, where modern inverter-based, digital power sources offer highly stable arc control and the capacity to store and recall thousands of certified welding programs (schedules), ensuring absolute repeatability across different projects and operators, a cornerstone requirement for cleanroom operations.

Advancements are heavily focused on enhancing traceability and quality verification. Current generation welding systems integrate advanced sensors to monitor critical variables—such as oxygen levels in the purge gas, rotational speed, and instantaneous amperage—in real-time. This sensor data is logged and cross-referenced with machine vision systems (often integrated into the weld head) that capture visual data of the weld seam as it is being performed. This holistic data package facilitates comprehensive electronic documentation, essential for meeting stringent semiconductor industry validation standards (like SEMI F78 for quality assurance) and minimizing manual inspection requirements.

Further technological refinement includes the development of compact, lightweight closed-head welding machines capable of handling increasingly smaller diameter tubing (less than 1/4 inch) with extremely low clearances, reflecting the shrinking footprint of process equipment within new fabs. Specialized features like orbital tube squaring and facing machines, which prepare the tubing ends with micrometer precision prior to welding, are equally critical. The seamless integration of these preparatory tools with the welding unit through sophisticated software ecosystems is the emerging technological standard, driving efficiency and minimizing the risk of particulate contamination introduced during preparation.

Orbital welding is used to create Ultra-High Purity (UHP) and Ultra-High Vacuum (UHV) fluid and gas delivery systems in semiconductor fabrication plants (fabs). Its function is to produce consistent, high-integrity, and repeatable welds in stainless steel tubing, minimizing contamination risk and ensuring leak-proof performance critical for sub-5nm manufacturing nodes.

Gas Tungsten Arc Welding (GTAW or TIG) is preferred because it uses an inert gas shield and a non-consumable electrode, allowing for extremely precise heat input control and producing spatter-free, clean internal weld beads. This process is essential for preventing the 'sugaring' (oxidation) of the internal pipe surface, which would otherwise introduce critical contaminants into the specialty gas lines.

The Asia Pacific (APAC) region leads the global market in demand, driven by massive capital expenditure and ongoing construction of new mega-fabs in Taiwan (TSMC), South Korea (Samsung/SK Hynix), and Mainland China. These investments in leading-edge semiconductor capacity necessitate large-scale UHP infrastructure implementation.

Software and traceability are critical for validation and regulatory compliance. Modern systems employ integrated software to store certified weld schedules, log real-time sensor data (current, purge pressure, oxygen levels), and provide comprehensive documentation proving that every weld meets strict industry standards (e.g., SEMI F77/F78) before a system can be commissioned.

The primary restraints include the extremely high initial investment cost required for advanced, automated UHP orbital welding equipment and the significant global shortage of highly specialized, certified technicians capable of operating and maintaining these complex systems in strict cleanroom environments.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.