ID : MRU_ 433588 | Date : Dec, 2025 | Pages : 241 | Region : Global | Publisher : MRU

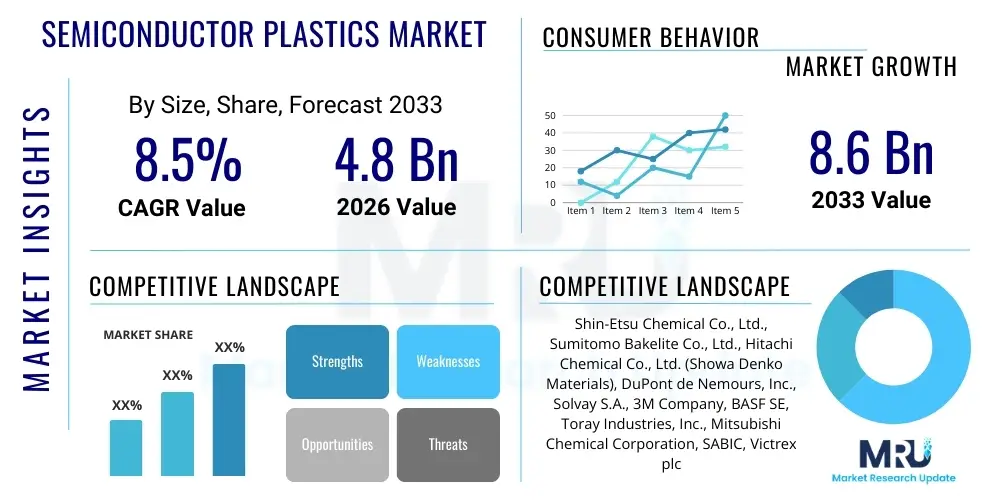

The Semiconductor Plastics Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2026 and 2033. The market is estimated at USD 4.8 Billion in 2026 and is projected to reach USD 8.6 Billion by the end of the forecast period in 2033. This significant expansion is primarily driven by the relentless miniaturization trends in integrated circuits (ICs) and the corresponding increase in demand for high-performance, chemically inert, and thermally stable materials necessary for advanced semiconductor manufacturing processes, including lithography, etching, and chemical mechanical planarization (CMP).

The Semiconductor Plastics Market encompasses the specialized polymers and high-performance engineering thermoplastics utilized extensively across the entire semiconductor fabrication and packaging value chain. These materials are critical components, serving roles from handling, protection, and insulation during wafer processing to encapsulation, thermal management, and structural support in the final device assembly. Key product categories include ultra-high molecular weight polyethylene (UHMWPE), polyether ether ketone (PEEK), polyimides (PI), fluoropolymers (PTFE, PFA, PVDF), and various epoxy molding compounds (EMCs).

Major applications for semiconductor plastics span highly corrosive environments in wet processing stations, precision components in wafer carriers and handling tools, insulation layers in advanced packaging, and molding compounds for robust device protection. The unique benefits these plastics offer—such as exceptional purity, low outgassing, superior chemical resistance to aggressive solvents and acids (like hydrofluoric acid and nitric acid), excellent dielectric properties, and high mechanical strength at elevated temperatures—make them indispensable in meeting the stringent purity and performance requirements of modern semiconductor manufacturing processes, particularly as geometries shrink below 10nm.

Driving factors for market growth include the massive global expansion of data centers, the proliferation of 5G infrastructure, the surging adoption of Internet of Things (IoT) devices, and the increasing complexity of advanced semiconductor packaging technologies like fan-out wafer-level packaging (FO-WLP) and 3D stacking. These trends necessitate plastics with tighter tolerances, enhanced thermal conductivity, and greater resistance to extreme processing conditions, pushing material innovation and subsequent market value upwards throughout the forecast period.

The Semiconductor Plastics Market is experiencing robust business trends characterized by a critical shift towards high-purity, specialty polymers capable of supporting sub-micron fabrication techniques and advanced thermal management solutions. Increased capital expenditure in new fabrication facilities (Fabs), particularly in Asia Pacific, acts as a primary catalyst, fueling demand for materials used in wafer processing equipment and contamination control systems. Key segments, such as encapsulation materials and engineering plastics used for mechanical parts, are witnessing accelerated growth due to the complexity of heterogeneous integration and the necessity for superior thermal dissipation in high-power devices like GPUs and AI accelerators. Strategic partnerships between chemical suppliers and semiconductor equipment manufacturers are becoming increasingly important to tailor polymer formulations precisely to evolving industry standards.

Regionally, Asia Pacific (APAC) dominates the market, driven by the concentration of leading semiconductor foundries, Outsourced Semiconductor Assembly and Test (OSAT) providers, and major consumer electronics manufacturing hubs in countries like Taiwan, South Korea, China, and Japan. This region is projected to maintain its fastest growth trajectory due to continuous government investments supporting local semiconductor self-sufficiency. North America and Europe, while possessing advanced R&D and leading materials science capabilities, focus primarily on high-end, specialty material production and applications in specialized equipment manufacturing, contributing significantly to the average selling price (ASP) of plastic components globally.

Segment trends highlight the strong performance of fluoropolymers (due to their unparalleled chemical resistance in wet processes) and advanced epoxy molding compounds (EMCs), which are essential for protecting sensitive dies and wire bonds in complex packaging architectures. Furthermore, the rise in demand for large-diameter silicon wafers (300mm and beyond) necessitates larger, precision-molded wafer carriers and handling components, providing significant opportunities for high-performance engineering plastics like PEEK. Sustainability concerns are also beginning to influence the segment, with a growing focus on materials that offer longer lifespan, recyclability, and reduced leaching potential, aligning with broader environmental, social, and governance (ESG) goals within the technology sector.

Common user questions regarding AI's impact on the Semiconductor Plastics Market center on how the massive increase in AI-driven processing power affects material requirements, specifically concerning thermal management, high-frequency signal integrity, and manufacturing volume scaling. Users frequently inquire about which plastics are best suited for packaging AI chips (GPUs, TPUs, ASICs) that generate extreme heat, and how AI-related demand volatility influences polymer supply chains. The consensus themes reveal that AI is a powerful demand generator, necessitating materials with extremely low dielectric loss (for high-speed signal transmission) and dramatically improved thermal performance (to wick heat away efficiently). This translates into expectations for increased R&D investment in advanced polymer composites and high-performance thermosets, moving away from conventional materials towards specialized, expensive solutions tailored for AI hardware infrastructure.

The Semiconductor Plastics Market is shaped by significant Drivers, Restraints, and Opportunities (DRO), which collectively form the Impact Forces dictating its growth trajectory. Key drivers include the exponential increase in IC complexity and transistor density, adhering to Moore’s Law and its variants, which necessitates ultra-pure materials for smaller nodes. Simultaneously, the restraints revolve around the inherently high cost of specialty polymer synthesis, stringent contamination control standards requiring expensive, certified materials, and the relatively long qualification cycles required by semiconductor manufacturers before adopting new plastic formulations. The primary opportunities lie in developing next-generation thermally conductive plastics and bio-based polymers, positioning the market for sustained high-value growth.

The core drivers are fundamentally tied to the proliferation of high-tech devices—from autonomous vehicles requiring specialized sensor chips to the deployment of massive 5G and 6G networks, all demanding more powerful and efficient semiconductors. These technological leaps place extreme performance demands on the materials used in manufacturing, ensuring that materials that offer even marginal improvements in purity, heat resistance, or dielectric performance command a significant premium and market share. However, the reliance on complex, petrochemically derived raw materials makes the market vulnerable to fluctuations in global oil and chemical supply chains, often constraining rapid expansion.

The impact forces are predominantly positive, favoring market expansion. Technology obsolescence cycles in the electronics industry are rapid, constantly renewing demand for new fabrication equipment and high-performance components. Opportunities in advanced packaging (especially System-in-Package, SiP, and heterogeneous integration) are particularly lucrative, requiring novel, low-stress, and high-Tg (glass transition temperature) epoxy compounds. Furthermore, the global drive for supply chain resilience means localized production of high-purity plastics in regions like North America and Europe, countering the historical concentration in Asia, and providing new market entry points for regional polymer specialists.

The Semiconductor Plastics Market is comprehensively segmented based on material type, application, and end-use sector, providing a granular view of specific industry demands and technological niches. Segmentation by material type is crucial as it dictates the functional capability, with segments such as fluoropolymers catering to chemical resistance in wet benches, while epoxy resins dominate device encapsulation. Application segmentation highlights the difference in material requirements between front-end processing (wafer handling, fluid delivery) and back-end processing (assembly and packaging). End-use segmentation tracks the demand originating from foundries, Integrated Device Manufacturers (IDMs), and OSAT companies, showcasing the primary purchasing power within the ecosystem. The overall segmentation landscape reflects the extreme specialization required across the diverse and complex semiconductor manufacturing environment.

The value chain for the Semiconductor Plastics Market is highly specialized, beginning with upstream analysis where petrochemical suppliers provide base monomers and specialty chemical companies synthesize high-purity polymer resins (e.g., fluoropolymer resins, PEEK pellets, epoxy precursors). This upstream stage is characterized by high barriers to entry due to the necessity for ultra-high purity synthesis techniques and rigorous quality control to prevent trace metal or organic contamination, which could destroy semiconductor dies. These specialized resin producers, often large diversified chemical conglomerates, establish specifications based on the demanding requirements of the semiconductor industry, focusing on attributes like low extractables, high thermal stability, and specific mechanical properties.

Downstream analysis involves compounding, molding, and fabrication, where resin materials are converted into precision components such as wafer carriers, chemical tanks, piping systems, and encapsulation molds. Molders and fabricators must utilize highly controlled cleanroom environments and precision machinery to maintain dimensional accuracy and surface finish. A critical downstream activity is the formulation of Epoxy Molding Compounds (EMCs) by specialized producers, which integrate the resin with various fillers (silica), hardeners, and additives to achieve the necessary thermal, electrical, and mechanical performance required for protecting the sensitive semiconductor chips during final assembly and subsequent operation.

The distribution channel operates through a mix of direct and indirect engagement. High-volume, standard plastic components like wafer boxes or tubing are often distributed indirectly via specialized industrial distributors who maintain localized inventory and cleanroom logistics. Conversely, complex or highly customized materials, particularly advanced EMCs and components for cutting-edge lithography equipment, are typically managed through direct sales relationships between the polymer manufacturer and the Integrated Device Manufacturers (IDMs) or large equipment OEMs (Original Equipment Manufacturers). This direct engagement ensures strict quality assurance, rapid technical support, and the co-development of materials tailored for next-generation process nodes, reinforcing the strategic importance of polymer suppliers in the technological roadmap of the semiconductor industry.

The primary end-users and buyers of semiconductor plastics span the entire electronics manufacturing ecosystem, dominated by entities involved in the production and packaging of integrated circuits. Integrated Device Manufacturers (IDMs) like Intel and Samsung are major buyers, utilizing plastics for internal wafer fabrication and often maintaining high internal standards for material specifications. These customers require plastics for internal handling, cleanroom consumables, and proprietary packaging processes, often demanding unique formulations that fit their internal manufacturing equipment and processes.

Foundries (e.g., TSMC, GlobalFoundries) represent another colossal customer base. As the core manufacturers of custom chips for fabless companies, their operations are characterized by extremely high throughput and reliance on specialized equipment, driving immense demand for highly durable, chemically resistant fluoropolymers used in wet processing and PEEK for precision mechanical parts in automated systems. The sheer volume of wafers processed daily mandates continuous replenishment of plastic components subject to wear and chemical degradation, securing steady, high-volume orders for material suppliers.

Finally, Outsourced Semiconductor Assembly and Test (OSAT) providers (e.g., ASE, Amkor) are critical end-users, primarily consuming Epoxy Molding Compounds (EMCs), bonding tapes, and test sockets. As the complexity of final device packaging increases, driven by multi-chip modules and System-in-Package (SiP) solutions, OSATs require advanced polymeric materials that offer superior thermal stability, moisture resistance, and mechanical protection. Their purchasing decisions are highly influenced by material cost-performance ratios and the ability of the plastic to conform to strict reliability standards mandated by the final electronics product manufacturers.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | USD 4.8 Billion |

| Market Forecast in 2033 | USD 8.6 Billion |

| Growth Rate | 8.5% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Shin-Etsu Chemical Co., Ltd., Sumitomo Bakelite Co., Ltd., Hitachi Chemical Co., Ltd. (Showa Denko Materials), DuPont de Nemours, Inc., Solvay S.A., 3M Company, BASF SE, Toray Industries, Inc., Mitsubishi Chemical Corporation, SABIC, Victrex plc, Daikin Industries, Ltd., Asahi Kasei Corporation, Ensinger GmbH, Evonik Industries AG, Greene, Tweed & Co., Saint-Gobain S.A., DSM (now part of Kendo), Rogers Corporation, and Sekisui Chemical Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technology landscape of the Semiconductor Plastics Market is constantly evolving, driven by the need for materials that can withstand increasingly aggressive processing conditions and perform optimally within advanced electronic devices. A primary technological focus is on enhancing the purity and reducing extractable ions in fluoropolymers (like PFA and PTFE), essential for maintaining ultra-clean fluid delivery systems in front-end fabrication. Suppliers are investing heavily in new polymerization techniques and post-processing methods to achieve ppq (parts per quadrillion) levels of purity, necessary to prevent defects in sub-5nm chip manufacturing processes. Furthermore, there is a technological push toward optimizing the surface energy and chemical compatibility of these plastics to ensure they do not react with or adsorb sensitive process chemicals.

In the back-end technology landscape, innovation is concentrated on Epoxy Molding Compounds (EMCs) tailored for advanced packaging geometries such as Fan-Out Wafer-Level Packaging (FOWLP) and Chip-on-Wafer-on-Substrate (CoWoS). Key advancements include the development of low-stress, low-warpage EMCs that maintain dimensional stability across thermal cycles, crucial for preventing mechanical damage to stacked dies. Another significant technological area is the integration of specialized fillers to create thermally conductive plastics (TCPs). These materials are vital for high-performance processors (like those used in AI and HPC) where traditional thermal solutions are insufficient, allowing the plastic housing or encapsulation layer itself to efficiently dissipate heat away from the sensitive silicon junction.

A burgeoning technological trend involves the exploration and commercialization of bio-based or sustainable polymers adapted for cleanroom use. While purity remains paramount, manufacturers are exploring high-performance polymers derived from sustainable feedstocks to address environmental mandates. This research area is challenging due to the inherent difficulty in achieving semiconductor-grade purity from non-traditional sources. Additionally, advancements in 3D printing technologies are enabling the rapid prototyping and production of customized plastic tooling and fixtures used in semiconductor assembly and testing, particularly those made from PEEK and polyimides, shortening equipment lead times and increasing manufacturing agility.

The global semiconductor industry’s geographical distribution heavily influences the Semiconductor Plastics Market, with manufacturing clusters acting as significant demand centers. Asia Pacific (APAC) stands as the undisputed hub, accounting for the largest market share due to the dominance of manufacturing ecosystems in countries like China, South Korea, Taiwan, and Japan. This region hosts the majority of global wafer fabrication facilities, assembly and test houses (OSATs), and critical equipment supply chains. Continuous massive capital investment by regional governments and industry giants to boost domestic chip production ensures that the demand for high-purity plastics for chemical management and device packaging remains exceptionally high and drives overall global volume growth.

North America is characterized by robust demand originating from leading Integrated Device Manufacturers (IDMs), major equipment suppliers, and cutting-edge research and development organizations. While manufacturing capacity is lower than in APAC, the region focuses on developing and producing the highest-specification, specialty polymer components, often commanding premium prices. Demand here is strongly tied to advanced technologies, including microelectromechanical systems (MEMS), specialized military and aerospace semiconductors, and materials for next-generation AI and quantum computing hardware, requiring materials with unparalleled technical performance and stringent quality certification.

Europe holds a strategically important position, primarily driven by strong automotive semiconductor manufacturing, industrial automation, and the headquarters of several key semiconductor equipment (OEM) providers (e.g., ASML). European demand focuses on specialized engineering plastics and high-temperature polymers required for advanced machinery components and power electronics used in electric vehicles (EVs). Furthermore, strict European regulatory frameworks regarding chemical safety and sustainability are accelerating the demand for low-emission and environmentally friendly polymeric solutions within the semiconductor value chain.

The primary drivers are the increasing complexity and miniaturization of integrated circuits (ICs), requiring ultra-pure materials to prevent contamination at advanced process nodes (sub-7nm), coupled with the escalating demand from high-growth sectors like 5G infrastructure, AI computing, and electric vehicle electronics, which necessitates specialized thermal management and encapsulation polymers.

Fluoropolymers, specifically PFA (Perfluoroalkoxy) and PTFE (Polytetrafluoroethylene), are most crucial for front-end wafer processing. Their exceptional chemical inertness, high purity, and resistance to aggressive acids and solvents used in wet etching and cleaning processes make them indispensable for fluid handling components, piping, and chemical storage tanks within the cleanroom environment.

Advanced packaging (such as 2.5D and 3D integration) drastically increases thermal density and mechanical stress. This requires specialized back-end materials, predominantly advanced Epoxy Molding Compounds (EMCs) and Polyimides (PIs), that offer low coefficient of thermal expansion (CTE), high glass transition temperature (Tg), and superior thermal conductivity to ensure device reliability and efficient heat dissipation.

The main restraining factor is the extremely lengthy and rigorous material qualification process required by semiconductor manufacturers and foundries. Due to the high cost of potential contamination or failure, new polymeric materials must undergo years of testing and certification to prove zero impact on yield and long-term device reliability, creating high barriers to entry for new suppliers.

The Asia Pacific (APAC) region dominates the Semiconductor Plastics Market because it houses the vast majority of the world’s major wafer fabrication plants (Fabs), OSAT providers, and integrated semiconductor supply chains, particularly in Taiwan, South Korea, and China, leading to the highest concentration of high-volume manufacturing demand for specialized polymers.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.