ID : MRU_ 433840 | Date : Dec, 2025 | Pages : 243 | Region : Global | Publisher : MRU

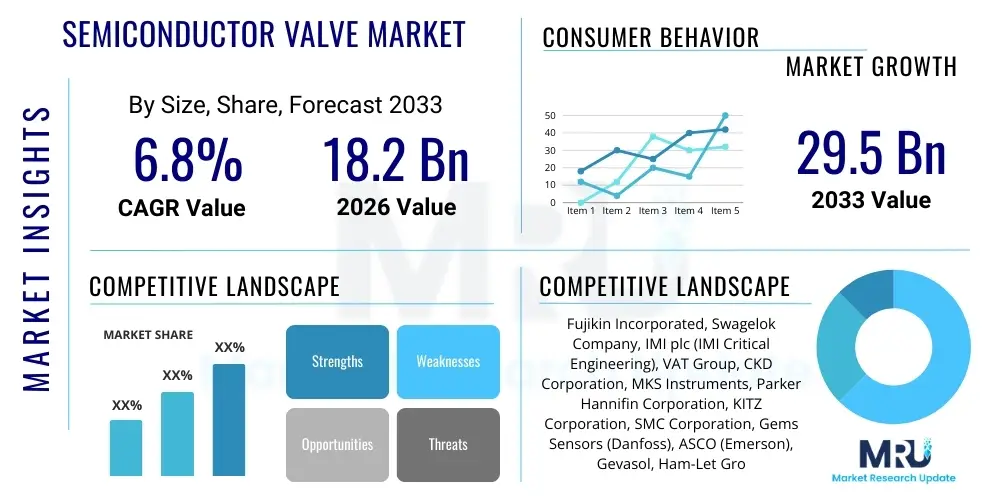

The Semiconductor Valve Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2026 and 2033. The market is estimated at 18.2 Billion USD in 2026 and is projected to reach 29.5 Billion USD by the end of the forecast period in 2033.

The Semiconductor Valve Market encompasses highly specialized flow control components essential for the manufacturing processes of microelectronics, including integrated circuits (ICs), memory chips, and display panels. These valves are critical for controlling the precise flow, pressure, and containment of ultra-high purity (UHP) gases and corrosive specialty chemicals used throughout fabrication facilities (fabs). Given the extreme sensitivity of semiconductor manufacturing to contaminants, these valves must exhibit exceptional leak integrity, corrosion resistance, and particle-free operation, often operating under vacuum or high-pressure conditions. Their application spans critical stages such as Atomic Layer Deposition (ALD), Chemical Vapor Deposition (CVD), Physical Vapor Deposition (PVD), etching, and cleaning processes, ensuring consistency and high yield rates in advanced semiconductor fabrication. The primary function is to isolate or regulate the flow of input materials, ensuring that material consumption is precisely controlled and environmental parameters are strictly maintained, which is paramount for producing components at the nanometer scale.

The driving factors for market growth are intrinsically linked to the global expansion of the electronics industry, specifically the robust demand for advanced computing devices, 5G technology infrastructure deployment, and the rapid proliferation of the Internet of Things (IoT). The continuous miniaturization of transistors (Moore’s Law progression) necessitates increasingly sophisticated and demanding fabrication techniques, which in turn require higher performance and reliability from fluidic control systems. Furthermore, major technological transitions, such as the shift from planar to 3D NAND and the adoption of Gate-All-Around (GAA) structures, place stringent demands on the cleanliness and precision of valve mechanisms. These next-generation manufacturing processes often employ more aggressive precursor materials and require faster cycle times, pushing manufacturers to invest in durable, high-speed valves, particularly those employing actuation technologies like pneumatic and motorized systems. The escalating capital expenditure (CapEx) in new fab construction globally, particularly in Asia Pacific and North America, serves as a direct catalyst for increased valve adoption and market expansion.

The global Semiconductor Valve Market is experiencing significant upward momentum, driven predominantly by structural changes within the business landscape, sustained geopolitical emphasis on supply chain resilience, and cyclical growth in memory and logic chip demand. Business trends indicate a strong focus on advanced material science, particularly the utilization of specialized alloys and polymer seals to enhance resistance against highly corrosive fluorine and chlorine chemistries used in deep etching. Manufacturers are also increasingly prioritizing modular designs and smart valve technologies, integrating sensors and diagnostic capabilities (Condition Monitoring) to facilitate predictive maintenance and minimize costly downtime in UHP environments. Strategic mergers and acquisitions remain prevalent as companies seek to consolidate technological expertise, broaden geographical reach, and secure long-term supply agreements with leading Tier 1 Foundries and Original Equipment Manufacturers (OEMs).

Regional trends highlight the undeniable dominance of the Asia Pacific (APAC) region, led by massive investments in China, South Korea, and Taiwan, which collectively house the majority of global semiconductor fabrication capacity. Government initiatives promoting domestic chip production, such as those in the U.S. (CHIPS Act) and Europe (European Chips Act), are simultaneously fueling CapEx in North America and Europe, causing these regions to register above-average growth rates during the forecast period as new fabrication plants become operational. Segment trends illustrate a crucial shift towards high-purity diaphragm and bellows valves, particularly those optimized for harsh chemical delivery systems and precise flow regulation in emerging deposition techniques. The pneumatic actuation segment maintains the largest market share due attributed to its reliability and rapid response time, while the demand for large-diameter butterfly and gate valves used in complex vacuum systems associated with advanced lithography and sputtering processes is also escalating steadily.

Overall, the market remains highly competitive, characterized by high barriers to entry due to the necessity of establishing stringent UHP material certifications and long qualification cycles with major device manufacturers. The transition to larger wafer sizes (300mm to future 450mm) and the implementation of sophisticated process control software require continuous innovation from valve suppliers. Successful market participants are those who can provide comprehensive solutions that combine hardware reliability with embedded digital intelligence, catering to the exacting requirements of sub-10nm manufacturing nodes. The consistent requirement for facility upgrades and the cyclical nature of semiconductor CapEx will continue to define the market trajectory through 2033.

Common user questions regarding AI’s impact on the Semiconductor Valve Market center on how artificial intelligence and machine learning (ML) optimize manufacturing processes, extend valve lifespan, and enhance predictive maintenance capabilities in critical fabrication environments. Users are primarily concerned with the implementation feasibility of AI-driven control loops replacing traditional PID controllers, and how this will affect the required responsiveness and reliability specifications of the valve itself. Key themes include the role of AI in analyzing sensor data (pressure, temperature, flow rate, vibration) generated by smart valves to preemptively detect component wear, thus minimizing sudden equipment failure and maximizing operational uptime, which is vital in high-volume, high-cost fab operations. Expectations revolve around achieving unprecedented levels of precision control, potentially reducing material waste, and streamlining the complex sequencing and timing required in multi-step processes like ALD.

The integration of AI fundamentally changes the paradigm of fluid control from reactive maintenance to proactive optimization. AI algorithms are trained on vast datasets encompassing historical operational metrics, material properties, and environmental conditions to develop highly accurate degradation models for valve components such as diaphragms, seals, and seats. This ability to predict the Remaining Useful Life (RUL) of a valve allows maintenance crews to schedule replacement during planned downtime rather than suffering catastrophic failures during live production runs. Furthermore, sophisticated AI models are being used to fine-tune the dosing and mixing ratios of specialty gases and liquid precursors. By analyzing real-time process outputs (e.g., film thickness uniformity), AI can instruct motorized or pneumatic valves to make minute, instantaneous adjustments to flow rates far beyond the capabilities of manual or basic automated control systems, leading to improvements in wafer yield and overall process efficiency.

The dynamics of the Semiconductor Valve Market are shaped by a complex interplay of growth drivers, constraining factors, emerging opportunities, and pervasive impact forces, resulting in a generally positive but volatile growth trajectory. Key drivers include the massive global capacity expansion in 300mm and upcoming 450mm wafer fabs, particularly in East Asia, driven by heightened demand for memory (DRAM, NAND) and advanced logic processors essential for AI, high-performance computing (HPC), and next-generation consumer electronics. The shift towards multi-patterning techniques, increased use of highly corrosive and exotic process gases, and the stringent requirements for ultra-high purity fluid systems further necessitate the adoption of state-of-the-art, high-integrity valves designed for extreme environments. These factors collectively push the market forward, compelling manufacturers to continuously upgrade their fluid handling systems to meet evolving semiconductor fabrication standards.

Restraints primarily revolve around the cyclical nature inherent to the semiconductor industry, characterized by periods of aggressive capital spending followed by temporary slowdowns (inventory adjustments), which can temporarily depress demand for ancillary components like valves. Furthermore, the high entry barriers and the necessity for lengthy, costly qualification cycles (often taking 18–36 months) with major equipment manufacturers and foundries limit the quick introduction of new or disruptive valve technologies. Pricing pressure remains a constant restraint, especially for standard valve types, due to intense competition among established players. The stringent material requirements and reliance on complex, limited supply chains for specialized UHP materials, such as specific grades of stainless steel and exotic polymer seals, pose significant logistical and cost constraints, especially during periods of global material shortages.

Opportunities in the market are significant, driven by the escalating adoption of advanced deposition and etching techniques, such as ALD and deep reactive ion etching (DRIE), which require highly specialized and precise flow control instruments, including micro-valves and integrated manifold solutions. The push for localized and resilient supply chains in North America and Europe presents a unique avenue for regional valve suppliers to secure contracts based on geopolitical stability and proximity, offsetting the traditional dominance of Asian suppliers. Moreover, the burgeoning trend towards smart manufacturing and Industry 4.0 provides opportunities for integrating advanced sensor technology and digital communication protocols into valves, enabling real-time monitoring and predictive diagnostics, creating a new, high-margin product category often termed 'Smart Valves'. The transition to sustainable manufacturing practices also opens opportunities for valves optimized for solvent recycling and efficient resource management within fab facilities.

Impact forces influencing the market include profound geopolitical tensions, particularly the trade relationship dynamics between the US and China, which directly influence technology transfer, export controls, and fab investment locations, drastically shifting market demand geographically. Regulatory compliance requirements, especially related to the handling and containment of highly toxic and flammable process gases (e.g., NF3, silane), exert strong pressure on valve manufacturers to prioritize safety certifications and leak integrity standards. Technological disruption, notably the rapid advancement in sub-10nm processing, forces an accelerated rate of innovation in material science and actuation speed, directly impacting product lifecycles and R&D investment. Lastly, the consolidation within the OEM and end-user segments dictates purchasing power and procurement standards, requiring valve suppliers to maintain robust quality control and scalable production capacity to meet bulk orders from dominant industry players.

The Semiconductor Valve Market is comprehensively segmented based on Type, Operation, Application, and Size, reflecting the diverse and highly specific requirements across different semiconductor manufacturing stages. Analysis across these segments is crucial for understanding current demand patterns and future growth vectors. The Type segmentation highlights the dominance of diaphragm and bellows valves due to their superior hermetic sealing and ability to prevent particle generation, making them ideal for UHP environments. The operation segment reveals a heavy reliance on pneumatic actuators for speed and reliability, though motorized valves are gaining traction in applications requiring ultra-fine, repeatable control over a long duration.

The Application segment is perhaps the most dynamic, with high-growth driven by the Deposition and Etching stages, which consume the largest volume of specialty gases and precursors. The Size segmentation reflects the distinction between point-of-use micro-valves embedded within gas sticks and manifold systems, versus larger bore valves used in bulk gas delivery and vacuum isolation systems. Understanding the interaction between these segments allows suppliers to tailor their offerings, such as developing high-flow bellows valves specifically designed for the vacuum lines of large-scale CVD reactors, or highly compact, solenoid-actuated diaphragm valves for integration into smaller, multi-channel gas panel assemblies that feed advanced lithography tools.

The value chain for the Semiconductor Valve Market is highly specialized and complex, beginning with upstream material suppliers who provide ultra-high purity stainless steels (typically 316L VIM/VAR), specialized alloys like Hastelloy, and advanced fluoropolymer sealing materials (e.g., PFA, PTFE). Rigorous material sourcing and qualification are paramount, as even minute impurities can compromise wafer yield. Following material preparation, the primary valve manufacturers engage in sophisticated precision machining, electropolishing, and extensive cleaning processes conducted within certified cleanrooms (Class 100 or better) to achieve the UHP surface finish required. This high degree of technical manufacturing complexity serves as a significant barrier to entry for new competitors. Quality control and hermetic sealing verification are critical intermediate steps before final assembly and packaging in a clean environment.

The distribution channel involves both direct and indirect routes. Direct sales are often utilized for large, custom orders or highly specialized valve systems sold directly to Tier 1 Semiconductor Equipment Manufacturers (OEMs) such as Applied Materials, LAM Research, and Tokyo Electron. These OEMs integrate the valves into their multi-million dollar processing tools (e.g., CVD reactors, etch systems). Indirect distribution involves specialized distributors and certified representatives who handle smaller volume sales, spare parts, and aftermarket support directly to the Fabs (end-users) for facility maintenance, utility systems, and replacement needs. Maintaining a strong network of technically capable distributors is vital for offering localized support and fast response times, given the 24/7 operational nature of semiconductor fabs.

The downstream segment encompasses the end-users: Integrated Device Manufacturers (IDMs) like Intel and Samsung, Pure-Play Foundries like TSMC and GlobalFoundries, and Memory Manufacturers like Micron and SK Hynix. The relationship between the valve manufacturer and the downstream customer is often dictated by the OEM, as the valve typically remains qualified as part of the total tool package. Continuous collaboration across the chain—from material suppliers ensuring purity, to manufacturers guaranteeing mechanical integrity, and finally to OEMs validating performance under process conditions—is essential for sustaining market competitiveness and ensuring the long-term reliability required for 5-to-10-year operational cycles in modern semiconductor facilities.

Potential customers and primary buyers of semiconductor valves are categorized into three distinct, yet interconnected, groups: major semiconductor fabrication facilities (Fabs), the Original Equipment Manufacturers (OEMs) that build the processing tools, and specialized UHP system integrators. Fabs, whether they are operating as Integrated Device Manufacturers (IDMs) such as Intel and Samsung, or as pure-play foundries like TSMC and UMC, represent the ultimate end-users, driving demand both through new fab construction (CapEx) and replacement/maintenance activities (OpEx). Their purchasing decisions are critically influenced by valve reliability, cleanliness certification, and proven performance history under specific process conditions, as valve failure can result in millions of dollars in yield loss.

Semiconductor Equipment OEMs constitute the most immediate and largest direct customer base for high-volume, specialized valves. Companies such as Applied Materials, LAM Research, KLA, and Tokyo Electron purchase valves in bulk to integrate into their high-precision manufacturing tools (etch, deposition, metrology). The OEM qualification process is rigorous and highly technical, focusing on minimizing footprint, maximizing cycle life, and ensuring integration compatibility with complex fluid control manifolds. Valve manufacturers often engage in co-development programs with these OEMs to design proprietary or highly customized valve solutions tailored to the next generation of fabrication processes, securing long-term supply contracts.

The third group includes system integrators and specialized utility providers who design, assemble, and maintain the facility-wide ultra-high purity Gas and Chemical Delivery Systems (GCDS) and bulk gas distribution networks that feed the fab tools. These customers focus on large-scale isolation valves, bulk gas valves, and facility hook-up components. They require high-flow, durable valves capable of handling high pressures and large volumes of commodity and specialty gases. Their purchasing criteria emphasize long-term operational lifespan, regulatory compliance (especially SEMI standards), and ease of maintenance within the facility infrastructure.

| Report Attributes | Report Details |

|---|---|

| Market Size in 2026 | 18.2 Billion USD |

| Market Forecast in 2033 | 29.5 Billion USD |

| Growth Rate | 6.8% CAGR |

| Historical Year | 2019 to 2024 |

| Base Year | 2025 |

| Forecast Year | 2026 - 2033 |

| DRO & Impact Forces |

|

| Segments Covered |

|

| Key Companies Covered | Fujikin Incorporated, Swagelok Company, IMI plc (IMI Critical Engineering), VAT Group, CKD Corporation, MKS Instruments, Parker Hannifin Corporation, KITZ Corporation, SMC Corporation, Gems Sensors (Danfoss), ASCO (Emerson), Gevasol, Ham-Let Group, Hi-Lok, Rotork, Festo, Kurt J. Lesker Company, Pfeiffer Vacuum, Entegris, TEL (Tokyo Electron) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Enquiry Before Buy | Have specific requirements? Send us your enquiry before purchase to get customized research options. Request For Enquiry Before Buy |

The technological landscape of the Semiconductor Valve Market is characterized by intense focus on optimizing sealing mechanisms, actuation speed, and material compatibility to handle increasingly aggressive chemistries and precise flow requirements. A key advancement is the widespread adoption of high-cycle diaphragm and bellows designs manufactured from proprietary alloys, specifically engineered to withstand highly fluorinated and chlorinated precursors used in etching and cleaning steps without degradation or particle shedding. These designs often incorporate proprietary surface treatments, such as specialized polishing or coatings (e.g., thermal spray coatings or passivation layers), to enhance corrosion resistance and maintain extremely low levels of outgassing, which is critical for ultra-high vacuum (UHV) applications associated with PVD and lithography tools. The drive for smaller feature sizes mandates valves capable of operating with near-zero dead volume to ensure swift gas transition and precise dose control, particularly in ALD processes where flow pulses must be delivered and sealed rapidly and repeatedly.

Actuation technology is rapidly advancing, moving beyond basic pneumatic systems to incorporate sophisticated digital controls. Pneumatic valves are now frequently paired with high-speed solenoid pilots and digital communication interfaces (such as DeviceNet or EtherCAT) to achieve cycle speeds measured in milliseconds, essential for throughput optimization. Concurrently, the use of motorized and piezoelectric actuators is increasing in applications demanding extremely fine resolution and repeatable positioning for continuous flow adjustments, often linked directly to advanced Process Control Systems (PCS). Furthermore, there is a strong trend toward modular valve systems and integrated manifold technologies (often called Gas Sticks or Gas Panels). These integrated assemblies reduce the number of potential leak points, minimize system footprint, and allow for easier maintenance, contributing directly to higher fab uptime and improved process reliability by simplifying complex fluid routing into a single, compact block.

Another crucial technological focus area is the development of ‘smart’ or ‘intelligent’ valves. These valves integrate micro-sensors for real-time monitoring of parameters such as internal temperature, cycle count, vibration patterns, and even internal pressure drops. This data is leveraged for sophisticated predictive maintenance models, often facilitated by embedded edge computing capabilities, allowing the valve itself to signal potential failure before process parameters are compromised. Compliance with stringent industry standards, such as SEMI F57 (defining vacuum and pressure compatibility) and SEMI F20 (addressing surface cleanliness and particle control), requires continuous innovation in cleaning protocols, welding techniques (orbital welding being the standard), and final testing methodologies, ensuring that every valve destined for a fab meets the exacting standards required for producing advanced microchips.

The primary driver is the unprecedented global investment in new semiconductor fabrication capacity (fabs), fueled by government subsidies (e.g., CHIPS Acts) and the escalating demand for high-performance chips used in artificial intelligence, 5G infrastructure, and data centers. The transition to smaller process nodes (sub-7nm) necessitates more complex manufacturing steps, requiring a higher density and greater precision from ultra-high purity (UHP) valves.

Bellows valves and diaphragm valves both offer hermetic sealing crucial for UHP applications. Bellows valves typically offer higher flow rates and superior performance in vacuum isolation applications, often utilized in deposition and etching vacuum lines. Diaphragm valves are generally preferred for precise, low-flow control and corrosive chemical delivery systems due to their minimal internal volume and quick-response cycle times.

The Deposition (CVD/PVD) and Etching application segments consume the largest volume of specialized valves. These processes involve the highly precise control of numerous specialty gases and aggressive chemical precursors, requiring complex gas delivery manifolds and continuous replacement of components subject to wear from corrosive environments and high thermal loads.

Manufacturers face challenges in developing materials that resist the increasingly harsh and exotic process chemistries (e.g., highly reactive fluorine compounds) while maintaining UHP standards. This requires specialized alloys (like ultra-clean stainless steel and Hastelloy) and advanced, particle-free sealing polymers capable of enduring extreme temperature cycles and high cycle counts without material degradation or outgassing.

Automation is driving the adoption of smart valves integrated with sensors for real-time diagnostics (temperature, pressure, vibration). This integration enables predictive maintenance, minimizing unplanned downtime. Furthermore, advanced motorized and digitally controlled valves are essential for achieving the ultra-fine, repeatable flow adjustments required by AI-driven process optimization loops in advanced lithography and deposition tools.

Research Methodology

The Market Research Update offers technology-driven solutions and its full integration in the research process to be skilled at every step. We use diverse assets to produce the best results for our clients. The success of a research project is completely reliant on the research process adopted by the company. Market Research Update assists its clients to recognize opportunities by examining the global market and offering economic insights. We are proud of our extensive coverage that encompasses the understanding of numerous major industry domains.

Market Research Update provide consistency in our research report, also we provide on the part of the analysis of forecast across a gamut of coverage geographies and coverage. The research teams carry out primary and secondary research to implement and design the data collection procedure. The research team then analyzes data about the latest trends and major issues in reference to each industry and country. This helps to determine the anticipated market-related procedures in the future. The company offers technology-driven solutions and its full incorporation in the research method to be skilled at each step.

The Company's Research Process Has the Following Advantages:

The step comprises the procurement of market-related information or data via different methodologies & sources.

This step comprises the mapping and investigation of all the information procured from the earlier step. It also includes the analysis of data differences observed across numerous data sources.

We offer highly authentic information from numerous sources. To fulfills the client’s requirement.

This step entails the placement of data points at suitable market spaces in an effort to assume possible conclusions. Analyst viewpoint and subject matter specialist based examining the form of market sizing also plays an essential role in this step.

Validation is a significant step in the procedure. Validation via an intricately designed procedure assists us to conclude data-points to be used for final calculations.

We are flexible and responsive startup research firm. We adapt as your research requires change, with cost-effectiveness and highly researched report that larger companies can't match.

Market Research Update ensure that we deliver best reports. We care about the confidential and personal information quality, safety, of reports. We use Authorize secure payment process.

We offer quality of reports within deadlines. We've worked hard to find the best ways to offer our customers results-oriented and process driven consulting services.

We concentrate on developing lasting and strong client relationship. At present, we hold numerous preferred relationships with industry leading firms that have relied on us constantly for their research requirements.

Buy reports from our executives that best suits your need and helps you stay ahead of the competition.

Our research services are custom-made especially to you and your firm in order to discover practical growth recommendations and strategies. We don't stick to a one size fits all strategy. We appreciate that your business has particular research necessities.

At Market Research Update, we are dedicated to offer the best probable recommendations and service to all our clients. You will be able to speak to experienced analyst who will be aware of your research requirements precisely.

Market Research Update is market research company that perform demand of large corporations, research agencies, and others. We offer several services that are designed mostly for Healthcare, IT, and CMFE domains, a key contribution of which is customer experience research. We also customized research reports, syndicated research reports, and consulting services.